Sample Category Title

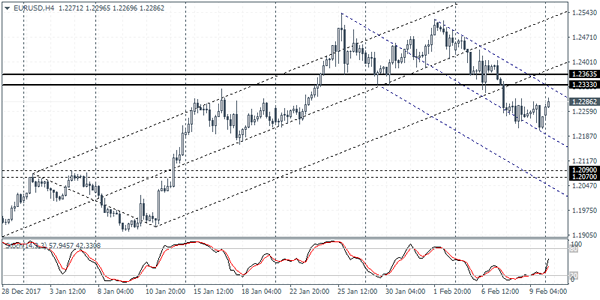

EURUSD Only Intraday Bullish Above 1.2290

The euro currency has opened the new trading week sharply higher against the U.S dollar as risk-on sentiment returns, with European equity markets set to open with triple digit gains. The EURUSD is also being helped by weakness in the U.S dollar index, with price-action now trading around the 1.2290 region, after the pair found strong support at the 1.2205 level on Friday. With a lack of market moving macroeconomic data from the eurozone and the United States on Monday, traders will look to the direction of the U.S dollar index and the broader equity market.

The EURUSD pair will turn intraday bullish only once above the 1.2290 level, further upside towards 1.2332 and 1.2364 then appears likely.

Should EURUSD price-action be contained by the 1.2290 resistance level, we may see a move back towards the 1.2255 and 1.2205 support levels.

Slow Monday Schedule Offers Little In The Way Of Data

From a calendar perspective, the global financial markets will be off to a slow start this week, with only a few important data releases scheduled.

Action begins at 08:00 GMT with a report on Swiss consumer inflation. Switzerland's consumer price index (CPI) is forecast to fall 0.2% in January following a flat-line reading the month before. In annualized terms, this translates into a gain of 0.8%.

Portugal will also release its January CPI report on Monday, with the official data set scheduled for 11:00 GMT.

In North America, the only major data release on the economic calendar is the US Monthly Budget Statement for January. The report is expected to show a budget surplus of $108.8 billion, following a deficit of 23 billion in December.

The calendar of events picks up later in the week with key reports on US inflation and Eurozone gross domestic product (GDP). In the meantime, investors can use the lack of fundamental drivers to reflect on recent turmoil in global equities.

In currencies, the US dollar has managed to recover sharply from multi-year lows, as investors continue to bet on an imminent rate hike by the Federal Reserve. The Federal Open Market Committee (FOMC) will hold its next policy meeting in March. The official rate statement will be accompanied by a revised summary of economic projections covering GDP, unemployment and inflation.

The US dollar index (DXY) was down at the start of Monday trading, falling 0.2% to 90.22. After last week's gains, DXY trimmed its year-to-date loss down to 2%.

EUR/USD

Europe's common currency experienced a broad pullback last week, dragging prices back toward the 1.2200 handle. The EUR/USD bounced back on Monday, gaining 0.2% to 1.2276. However, the pair is down roughly 150 pips from last week's highs north of 1.2400. Furthermore, it is down more than 200 pips from the 1 February high above 1.2500. The pair remains in a general uptrend, but appears to have established a new trading range between 1.2100 and 1.2600.

GBP/USD

Cable fell to nearly four-week lows on Friday, as the dollar rebounded sharply against a basket of world peers. The GBP/USD exchange rate briefly fell below 1.3800 but has since clawed back above those levels. It was last seen trading at 1.3836.

USD/JPY

For all its gains against other currencies, the dollar fell to fresh five-month lows against the yen last week week as prices touched 1.0800 for the first time since September. The yen is clearly benefiting from risk-off sentiment following one of the worst weeks in equities since the financial crisis. The USD/JPY was last seen trading at 108.68, where it was down 0.1% from the previous close.

EUR/USD Bullish Rally At 50% Fibonacci Support Zone

The EUR/USD bounced at the 50% Fibonacci level and has broken above the bearish trend channel which could indicate a bullish reversal. Price could be completing a bullish wave 4-5 pattern if price manages to continue above the weekly Pivot Point.

The GBP/USD is showing stronger bearish momentum than the EUR/USD and could confirm one more lower low within a falling wedge chart pattern whereas the USD/JPY remains very corrective and choppy and requires price to either break above resistance or below support on the daily chart before the long-term direction becomes clear.

Technical Outlook: EURUSD – Doji Reversal Pattern Is Forming On Daily Chart But Stronger Upside Needed For Confirmation

The Euro stands at the front foot on Monday and ticked above initial barrier at 1.2280 (Fibo 23.6% of 1.2522/1.2205 downleg. Initial signal of basing is developing on daily chart after near-term bears off 1.2522 repeatedly failed to clearly break below rising 30SMA and Friday's action ended in Doji candle. Fresh attempts higher signal formation of reversal pattern which requires stronger upside and firm bullish close. Near-term price action is holding within thick hourly chart (1.2258/1.2309) with firm break above cloud needed to generate stronger bullish signal. Stronger reversal signal above cloud could be expected on break above daily Tenkan-sen (1.2363) which would confirm bullish near-term scenario and shift focus higher. Slow stochastic is attempting to reverse from oversold territory, adding on bullish signals, however, weakening 14-d momentum warns. Ascending 30SMA continues to underpin and marks initial support at 1.2237. Negative scenario sees increased downside risk on break below 30SMA and Friday's low at 1.2205 which would signal extension of pullback from 1.2522 towards next pivotal support at 1.2153 (Fibo 61.8% of 1.1915/1.2537 upleg. Bigger picture shows formation of reversal pattern on weekly chart and growing risk of deeper correction as long bearish weekly candle that was left last week after sixth straight bullish weeks.

Res: 1.2280, 1.2309, 1.2326, 1.2363

Sup: 1.2237, 1.2205, 1.2153, 1.2089

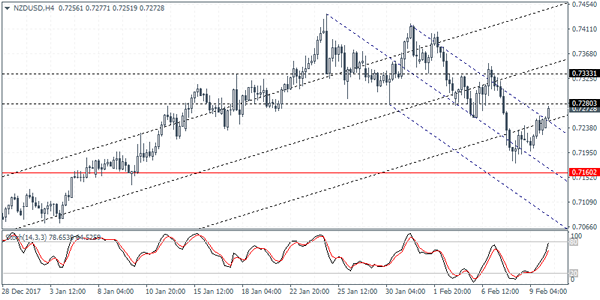

NZDUSD Intraday Analysis

NZDUSD (0.7272): The NZDUSD currency pair was seen forming a bottom with prices attempting to retrace the losses. In the short term, the reversal could see NZDUSD rising back to the price area of 0.7333 - 0.7280. With resistance most likely to be established here, NZDUSD could be seen either moving sideways in the short term or posting a reversal off this level. The downside target for NZDUSD remains at 0.7160 with the potential for further declines. This could push the kiwi dollar towards the next lower support level at 0.6943

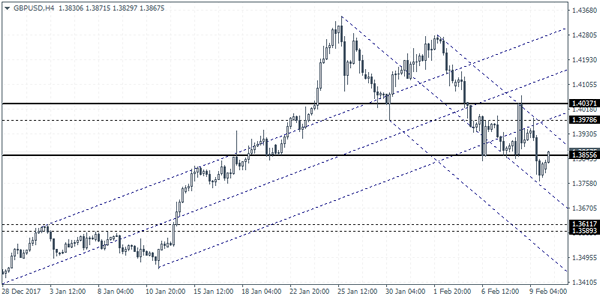

GBPUSD Intraday Analysis

GBPUSD (1.3867): The GBPUSD currency pair reached the target of 1.3855 on Friday. Price action closed below this level posting a modest reversal. The inside bar pattern formed on Friday's close indicates that prices could be seen retesting the break out level of 1.2855. A reversal off this level could signal further downside in GBPUSD. Support at 1.2611 - 1.3589 will be the next downside target in the currency pair. In the event that GBPUSD manages to close above 1.3855 on a daily basis, we could expect some sideways consolidation taking place. The downside bias will be invalidated only on a close above 1.3978.

EURUSD Intraday Analysis

EURUSD (1.2286): The EURUSD closed on Friday with the doji pattern. The prices were trading within the range from Thursday. The doji pattern comes after the EURUSD fell sharply through the week. A reversal off this doji pattern could potentially signal a short-term retracement in the EURUSD. To the upside, the gains are likely to be limited to the 1.2363 level which previously served as support. Establishing resistance at this level could signal the end of the correction with prices likely to correct lower. Support at 1.2090 will remain the initial target for the decline in the EURUSD.

Canada’s Unemployment Rate Rises

The U.S. dollar managed to hold its ground but, was trading mixed on Friday. The EURUSD posted declines into the close while the equity markets saw another volatile day. On the economic front, data from the UK showed that manufacturing production rose 0.3% on the month as expected. The previous month's figures were revised down from 0.2% from the initially reported 0.4% increase. Construction output seemed to be better, rising by 1.6%, which beat estimates of a 0.7% increase while industrial production declined 1.3% on the month.

Canada's monthly employment figures surprised the public to the downside. The economy was seen losing 88,000 jobs in January with the unemployment rate rising to 5.9% up from 5.7% in December.

Looking ahead, the economic calendar is relatively quiet today with no major releases expected. Switzerland will be releasing its monthly inflation data. Forecasts predict a 0.1% decline in consumer prices. Later in the day, Japan's producer price index data will be coming up with forecasts showing a slower pace of growth at 2.7%.

Currencies: Dollar Rally Slows

Sunrise Market Commentary

- Rates: Core US and European bonds hover near recent correction low

On Friday, core bonds hardly profited from ongoing turbulence on the equity markets. A late session rebound of US equities even reversed minimal intraday gains. Today, the eco calendar is empty. Price action in Asia suggests that global market volatility might ease. However, it won't help core bonds. Wednesday's US CPI is the next milestone for global bond markets. - Currencies: dollar rally slows

EUR/USD dropped to the low 1.22 area on Friday, but the dollar rally did run into resistance as equities rebounded. Short-term, we expect EUR/USD to settle in a 1.22/24 consolidation pattern going into Wednesday's key US CPI release. Uncertainty on the UK ‘road to Brexit' continues to weigh on sterling

The Sunrise Headlines

- US equitiesUS equities rebounded in the US afternoon session on Friday, finishing a turbulent week on a positive tone. The major US indices showed gains of about 1.5%. Asian equities and US equity futures are trying to extend Friday's WS rebound this morning. Japanese markets are closed for a holiday.

- Australia's big banks are responding to a revenue crunch by cutting jobs and other costs, prompting fears on the eve of an inquiry into their businesses that the industry's tarnished reputation is about to take another hit.

- China will boost its job creation effort and promote entrepreneurship this year. Meng Wei of the National and Development Reform Commission (NDRC) said China needs to create jobs for 9.7 mln registered as unemployed and 8.2 mln new college graduates, as well as workers affected by industrial capacity cuts.

- ECB's Nowotny sees recent setback in equities 'as a normalization, a reasonable wake-up signal to show that stock markets can't just keep rising all the time. According to Nowotny the task of central banks isn't to satisfy markets but to ensure overall economic stability. So if necessary, interest rates will have to rise and markets will adapt to that”

- Prime Minister Theresa May will attempt to unite her cabinet and convince the European Union that Britain knows what it wants from Brexit. The UK Prime Minister and other senior ministers will give six speeches in the next few weeks to clarify what Britain sees as ‘The Road to Brexit'.

- Today's eco calendar is almost empty with no important eco data in Europe and in the US. Markets are mainly looking forward to the key US CPI report to be published on Wednesdaylendar is almost empty with no important eco data in Europe and in the US. Markets are mainly looking forward to the key US CPI report to be published on Wednesday

Currencies: Dollar Rally Slows

USD rebound slows

On Friday, the repositioning on bond and equity markets still gave no clear guidance for the USD. EUR/USD filled bids in the low 1.22 area as US equities set new ST lows, but rebounded in line with equities toward the US close. EUR/USD finished the day little changed (1.2252). USD/JPY showed a similar pattern. The pair dropped to the low 108 area but closed at 108.80. The yen gains slightly ground at times of extreme equity stress, but returned the intraday gains when tensions eased.

Asian equity markets entered calmer waters after Friday's late session rebound in the US. Regional equities show gains of up to 1%+. Japanese markets are closed for a holiday. Easing tensions are weighing on the US dollar. EUR/USD rebounds to the high 1.22 area. USD/JPY hardly profits. The pair trades in the 108.70 area.

There are no important data in the US and Europe today. So, FX trading will still look for guidance from global (equity) markets. Later this week, the US CPI (Wednesday) will take center stage. Headline inflation is expected to ease from 2.1% Y/Y to 1.9%. The core measure is expected to soften from 1.8% Y/Y to 1.7%. At the same time, US January retail sales will be released. EMU (Thursday) and Japan (Wednesday) will publish Q4 GDP growth. Markets will also monitor CB speeches, looking for guidance on the CB's reaction function after recent market turmoil.

Last week, the combination of higher yields and an aggressive risk-off was a mildly USD positive. This morning, the dollar is ceding slightly ground as global tensions are easing. However, with US yields near recent peaks, the correction shouldn't go very far. We assume EUR/USD to settle in a wait-and see modus in the 1.22/1.24 area going into the CPI release. Technically, the dollar decline slowed. EUR/USD dropped below the 1.2323/35 support. A break below 1.2165 would call off the ST downside alert (for USD).

On Friday, the sterling declined further as EU's Barnier warned Britain that a post-Brexit transition period is not a given. EUR/GBP spiked higher to the 0.8875/80 area. Today, there are no UK data. Over the next weeks, UK PM May will try to bring clarification on the ‘road to Brexit' that Britain wants to walk. For now, it is far from sure that this will bring back calm to the UK political scene. EUR/GBP is trending higher in the 0.8690/0.9033 trading range, with intermediate resistance at 0.8930. We hold our basic view that the 0.8690 support probably won't be easy to break without big progress on Brexit.

EUR/USD: dollar rebounds slows

Forex Analysis: U.S. Inflation Data In Focus

A quiet week ahead on the data front at first glance but US Inflation on Wednesday will be a major market mover. Market participants will view this data point as an indicator given the reaction to higher inflation on bonds and Central Bank policy. Higher Inflation would impact the pace of rate hikes from the Fed and change the attractiveness of Bonds for investors. This would subsequently spill across other markets including equities and FX. As a result of the move to risk-off we have seen over the last two weeks, this data has become crucial in determining market sentiment.

Today is a light data day and could experience lighter volumes, due to holidays in Japan, Brazil, Argentina (Carnival) and Canada (Family Day).

UK Industrial Production (YoY) (Dec) was 0.0% v an expected 0.3%, from a previous 2.5%, which was revised up to 2.6%. Manufacturing Production (MoM) (Dec) was as expected at 0.3%, from 0.4% previously, which was revised down to 0.2%. Industrial Production (MoM) (Dec) was -1.3% v an expected -0.9%, from 0.4% previously, which was revised down to 0.3%. Manufacturing Production (YoY) (Dec) was 1.4% v an expected 1.2%, from 3.5% previously, which was revised up to 3.8%. GBPUSD broke under support at 1.39425 following this release and reached a low of 1.37644 in the session.

The Russian Interest Rate Decision was released on Friday, with the Interest Rate lowered to 7.5% as expected from 7.75%.

UK NIESR GDP Estimate (3M) (Jan) was 0.5% v an expected 0.3%, from 0.6% prior.

Canadian Unemployment Rate (Jan) was released at 5.9% v an expected 5.8%, from a previous 5.7%. Participation Rate (Jan) was 65.5% v an expected 65.7%, from 65.8% prior. Net Change in Employment (Dec) was -88.0K v an expected 10.0K, from a prior 78.6K, which was revised down to -2.2K. USDCAD spiked to a high of 1.26868, from 1.25918, before dropping to a low of 1.25596 on this data release.

Baker Hughes US Oil Rig Counts was released with a headline number of 791 from 765 last week. WTI Oil moved back under $60.00 to a low of $58.07 on Friday.

EURUSD is up 0.31% overnight, trading around 1.22873.

USDJPY is down -0.10% in early session trading at around 108.666.

GBPUSD is up 0.24% to trade around 1.38572.

AUDUSD is up 0.24% overnight, trading around 0.78313.

Gold is up 0.59% in early morning trading at around $1,323.41.

WTI is up 1.17% this morning, trading around $59.89.

Major data releases for today:

At 08:00 GMT, Swiss Consumer Price Index (YoY) (Jan) is expected unchanged at 0.8%. Consumer Price Index (MoM) (Dec) is expected at -0.1% from 0.0% previously. CHF could see volatility increase following this release.

At 19:00 GMT, US Monthly Budget Statement (Jan) is expected to be $108.8B from a previous reading of $-23.0B.

At 21.50 GMT, Australian RBA Assistant Governor Ellis will speak about the economic outlook at the Australian Business Economists Forecasting Conference, in Sydney. AUD crosses may be affected.

Major data releases for this week:

On Tuesday, at 09:30 GMT, UK Consumer Price Index (YoY) (Jan) is expected at 2.9% against 3.0%.

On Wednesday, at 10:00 GMT, Eurozone Gross Domestic Product s.a. (YoY) (Q4) is expected to be 2.7% from 2.6% prior. Gross Domestic Product s.a. (QoQ) (Q4) is expected to be unchanged at 0.6%.

At 13:30 GMT, US Consumer Price Index (YoY) (Jan) is expected unchanged at 2.1%. Consumer Price Index Ex Food & Energy (YoY) (Jan) is expected unchanged at 1.8%. Retail Sales ex Autos (MoM) (Jan) is expected to be 0.5% from 0.4% prior.

On Thursday, at 01:30 GMT, Australian Unemployment Rate s.a. (Jan) is expected to be 5.3% from 5.5% previously. Employment Change s.a. (Jan) is expected to be 25.5K from 34.7K prior.