Sample Category Title

Market Morning Briefing: Dollar Yen Saw A Low Of 108.05

STOCKS

Dow (24190.90, +1.38%) may trade within 24500-23000 region and try to attempt levels above 24500 in the near term. Note support near 23200 on the 3-day candles which if holds, may take it higher towards 24800 in the coming sessions. .

Dax (12107.48, -1.25%) is sharply down and is likely to find some support in the 11900-11800 region from where a bounce could be expected in the coming sessions.

Nikkei (21382.62, -2.32%) is also likely to move up while support near 21000 holds for now. A bounce towards 22200 or higher looks possible.

Shanghai (3139.38, +0.30%) dropped sharply last week breaking below the channel support on the weekly charts. While it trades lower, a test of 3000 is possible. A break below 3000, if seen could be vulnerable for a sharper fall in the near to medium term. Watch price action near 3000.

Nifty (10454.95, -1.15%) and Sensex (34005.76, -1.18%) are likely to hold above current support levels near 10320 and 33500 respectively. While these supports hold in the coming sessions, a short term bounce is possible.

COMMODITIES

WTI (59.88) has moved up slightly from levels near 58. In case we see a dip below 58, WTI is likely to test 56-54 as visible on the 3-day charts before a bounce from there is seen.

Brent (63.43) on the other hand has been stable above 62-61 levels which seem to be a decent support for the medium term.

Brent-WTI Spread (3.53) has risen from support levels near 3. There is some scope of re-testing 3.00 in the near term before again starting to bounce back to higher levels.

Gold (1326.10) is likely to trade above 1300-1305 region and may inch up towards 1340-1360 levels in the coming sessions. Near term looks bullish.

Copper (3.0785) is trying to move above 3.0750 and if that happens, the price may again start moving up towards 3.15; else failure to move above 3.0750-3.0800 just now could push it down further towards 3.00-2.97 levels in the medium term.

FOREX

Dollar Index (90.176) is currently consolidating around 90.20 and could slowly move towards resistance near 90.5-90.75 on the daily candles .

Euro (1.2281) has seen some strengthening since Friday when it saw a low of 1.2206. It might again attempt a test of support near 1.220-1.225 on the daily candles this week.

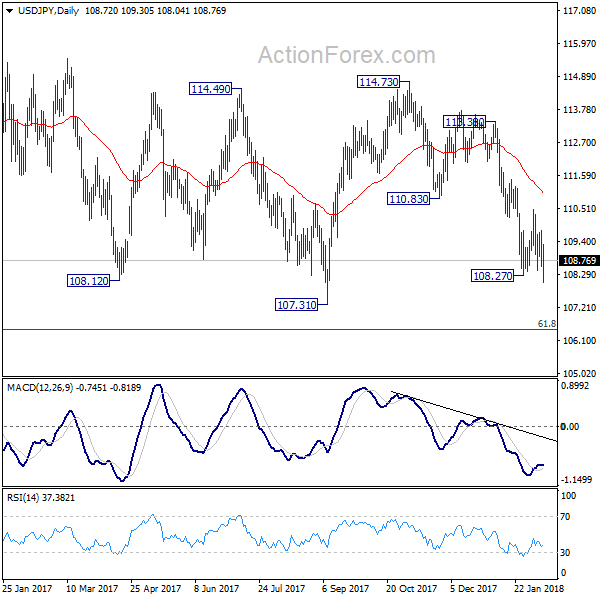

Dollar Yen (108.70) saw a low of 108.05 on Friday, thereby breaking immediate support on daily candles near 108.5 and testing support on the 3 day candles near 108. As stated previously, 108.0-108.5 are strong support levels (which is reflected on the weekly line chart as well) and Dollar Yen could see a bounce from here towards resistance near 110.5-111.0 on the weekly line charts in the next 1-2 weeks.

Euro Yen (133.60) has gone back up above support near 133 on the daily candles. We see that there is decent support being provided by horizontal trend lines on the daily and 3 day candles near 131.5-132, which has held. We could see Euro Yen move up towards 134 in the coming sessions since the Yen could weaken relatively more against the Dollar as compared to the Euro in this week.

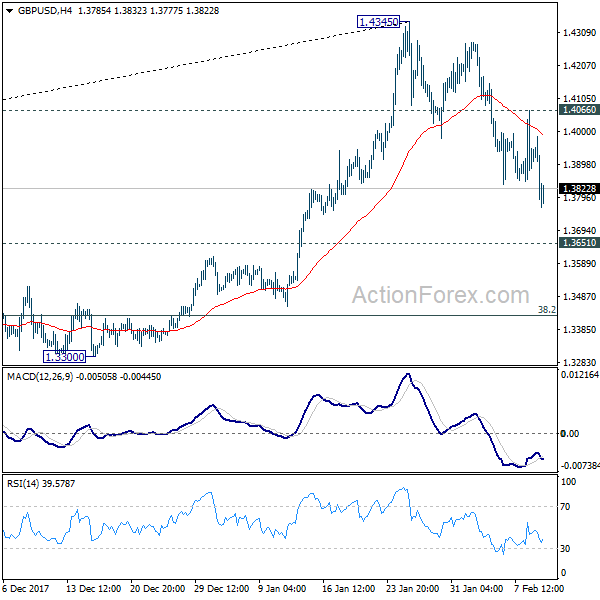

The Pound (1.3846) is again trending downwards after seeing 2 days of consolidation near 1.39. Infact it reached a low of 1.3765 on Friday and could test support on daily candles near 1.37 this week.

Dollar Rupee (64.4025) - is likely to trade below 64.50 while resistance near 64.50/40 may hold in the early sessions this week.

INTEREST RATES

US 10 Year Yield (2.8512), US 30 year Yield (3.1596), US 5 year yield (2.5433), US 2 year yield (2.0732) : US longer term yields moved up further 2 basis points on Friday while the nearer term yields both saw slight declines. There has been little volatility in the past 3-4 days as compared to the week prior. The short period of US govt shutdown on Friday also didn’t impact the yield movement much. We hence again repeat our expectation for the 4 yields to respect their long term resistance levels (2.85, 3.20 (changed from 3.15 previously), 2.7 (changed from 2.6 previously) and 2.2 respectively) in this month.

US 10-5 Year Yield Spread (0.31) is moving up fairly quickly towards the upside target at resistance near 0.35. However, there might be a dip in the coming days as the 10 Yr could move below current levels (near 2.85).

US CPI data release on Wednesday could be an important event for Bond yields. Higher inflation could increase the possibility of the next rate hike to happen in March.

German 10 Year bond yield (0.745) has dipped from resistance near 0.76 and the ranging between 0.7 and 0.76 could continue in this week.

Dollar and Yen Mildly Lower as Markets Tread Water

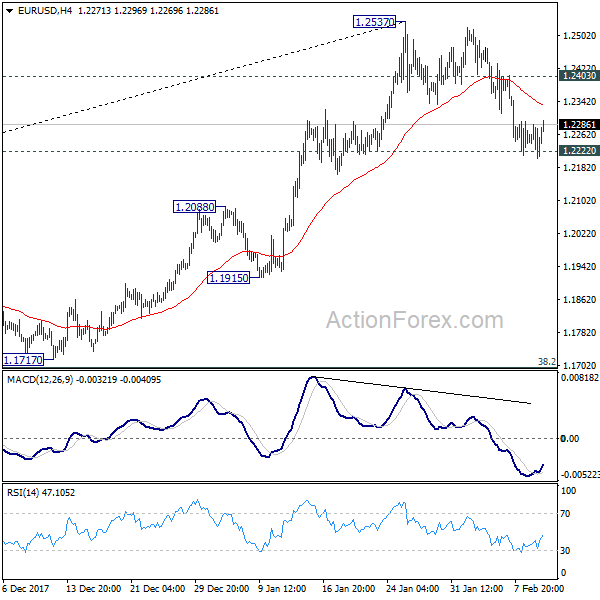

The Asian markets are rather quiet with Japan on holiday. Dollar and Yen are paring back some of last week's gains. Meanwhile, Euro and Aussie are recovering. It now looks like EUR/USD is holding on to 1.2222 key support for the moment. Elsewhere in the Asian Pacific markets are steadily mixed with Hong Kong HSI trading up 1%, South Korea KOPSI up 1.1%, China SSE down -1.3% at the time of writing. The economic calendar is light today, with Swiss CPI as the main feature. Speeches of UK MPC member Ian McCafferty and Gertjan Vlieghe will catch some attention.

UK May planning a series of speeches on Brexit

In the UK, a series of speeches are planned by Prime Minister Theresa May and her cabinet officials in the coming weeks regarding Brexit. International Development Secretary Penny Mordaunt said that "what the public want is, they want the vision and they want some meat on the bone," and, "and that's what they are going to get." The topic of whether to stay in the EU customs union heated up in the past two weeks. EU negotiator Michel Barnier warned on Friday that a transition deal is not a given and that prompted selloff in the Pound. Locally, May is facing objections from Brexiteers on staying the custom union. And, Mordaunt said that May could face defeat in the House of Commons regarding the kind of Brexit that she wants, if "she's not careful".

ECB concerned with US political influence on exchange rate

ECB Governing Council member Ewald Nowotny said the central bank is "certainly concerned about attempts by the United States to politically influence the exchange rate." And he added "that was a theme of economic discussions in Davos, where the ECB addressed this, and it will certainly be a theme at the upcoming G20 summit." Regarding the US economy, Nowotny said that President Donald Trump "started with a good inheritance" from the pervious government. And the current low unemployment, robust growth and tame inflation stem from Trump's predecessor, not his own policies.

German Merkel defended her painful concessions

German Chancellor Angela Merkel defended her concessions to the SPD for reforming the grand coalition. The concessions include handing the finance minister foreign ministry. She described those as "painful" concessions and she "understand the disappointment" of her conservatives. In particular, the government's strict fiscal discipline enforced by former finance minister Wolfgang Schaeuble could be loosen up. But Merkel said that "we have also approved the policies and the finance minister cannot simply do as he likes." Also, she emphasized that "we need to show the we can start a new team".

Looking ahead

Inflation and GDP data will be two key focuses this week. Swiss, UK and US will release CPI. Japan and Eurozone will release GDP. In addition, Australia employment will also be watched. Here are some highlights for the week:

- Monday: Swiss CPI

- Tuesday: Japan PPI, machine tools orders; Australia NAB business confidence; Swiss PPI; UK CPI, PPI

- Wednesday: Japan GDP; New Zealand inflation expectation; German GDP; Eurozone GDP; US CPI, retail sales, business inventories

- Thursday: Australia employment; Eurozone trade balance; US PPI, Empire State manufacturing, Philly Fed manufacturing, industrial production, NAHB Housing index

- Friday: New Zealand manufacturing index; UK retail sales; Canada manufacturing sales; US housing starts and building permits, import prices, U of Michigan sentiment

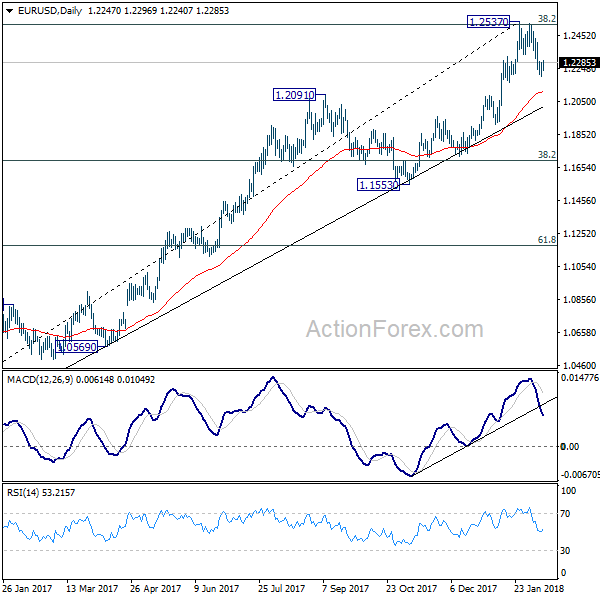

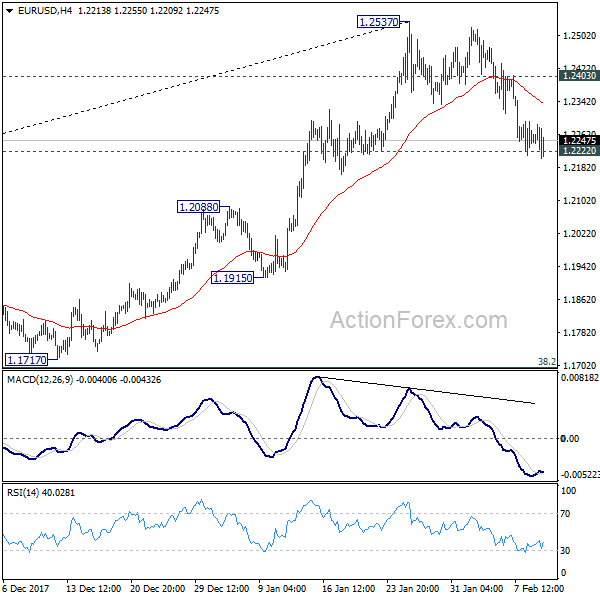

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2208; (P) 1.2248 (R1) 1.2290; More....

EUR/USD continues to draw support from 1.2222 and recovers today. Intraday bias stays neutral with focus on 1.2222. Sustained break there should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:15 | CHF | CPI M/M Jan | -0.20% | 0.00% | ||

| 08:15 | CHF | CPI Y/Y Jan | 0.80% | 0.80% | ||

| 19:00 | USD | Federal Budget Balance Jan | 50.2B | -23.2B |

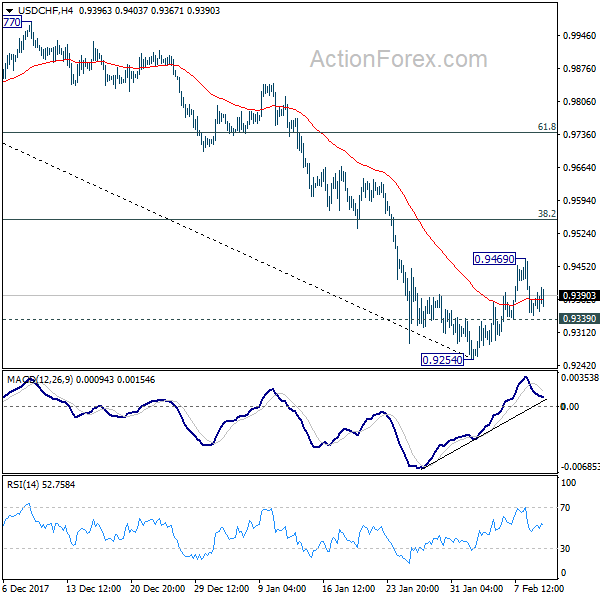

USDCHF – Retains Corrective Upside Pressure

USDCHF - With the pair closing higher the past week, it looks to build up on that gain in the new week. On the downside, support lies at the 0.9350 level. A turn below here will open the door for more weakness towards the 0.9300 level and then the 0.9250 level. On the upside, resistance resides at the 0.9450 level where a break will clear the way for more strength to occur towards the 0.9500 level. Further out, resistance comes in at the 0.9550 level. Above here if seen will turn attention to 0.9550. All in all, USDCHF faces further recovery higher.

EURUSD – Vulnerable On Correction Though With Caution

EURUSD - The pair closed lower the past week leaving risk of more weakness on the cards. We faces price hesitation with a move higher in the new week. On the upside, resistance comes in at 1.2300 level with a cut through here opening the door for more upside towards the 1.2350 level. Further up, resistance lies at the 1.2400 level where a break will expose the 1.2450 level. Conversely, support lies at the 1.2200 level where a violation will aim at the 1.2150 level. A break of here will aim at the 1.2100 level. Below here will open the door for more weakness towards the 1.2050. Its weekly RSI is bearish and pointing lower suggesting more weakness. All in all, EURUSD faces further pullback threats.

GOLD – Weakens, Remains On The Defensive

GOLD - The commodity saw price weakness for a second week in a row the past week. On the downside, support comes in at the 1,310.00 level where a break will turn attention to the 1,300.00 level. Further down, a cut through here will open the door for a move lower towards the 1,290.00 level. Below here if seen could trigger further downside pressure towards the 1,280.00 level. Conversely, resistance resides at the 1,320.00 level where a break will aim at the 1,330.00 level. A turn above there will expose the 1,340.00 level. Further out, resistance stands at the 1,350.00 level. All in all, GOLD looks to weaken further.

This Too Shall Pass

This too shall pass

It seems anytime I left my desk last week the market was sure to fall apart but after witnessing 25 years + of market corrections, I know storms don’t last forever, and as far as the recent bout of market mayhem is concerned, this too shall pass.

Traders quickly conjectured that the ‘crash’ was mainly due to over-crowded positioning in short equity volatility trades and, therefore, was a relatively isolated event. But this does not mean equity markets are out of the weeds just yet.

With US cash flow models factoring in higher US bond yields, equity markets repricing was always on the cards, but unequivocally the rapidity of the move higher in yields was stifling and stop losses were combatively triggered. And when factored with the unbridled use of leverage in equity positions it likely caused everyone to head for the exits due to cash and margin requirements. The great unknown in the debate is just how much equity froth is based on leverage and to what extent will higher US bond yields squeeze these positions either from a cash position or through asset rotation perspectives.

It was a crazy week for US rate markets, but with powerful US economic signals and interest rates most certainly to rise quicker than expected, last week tumult could be little more than the start of the equity rollercoaster. If cumulative boost from tax reform and fiscal stimulus nudges GDP outline 1.5% higher over the next six to 9 months how does the Fed possibly stick to their three dot plot projections for 2018?

Bond markets are only in the early stages of buying into the global reflation theme, and increasing inflation expectations are driving nominal yields higher. Last week there was a significant topside move in US yields which suggest we could easily tack on another 30-35 basis points 2’s through 10’s given the US fiscal stimulus backdrop. But even without inflation, global central banks will move rates higher, and this will add to higher yield environment, higher inflation or not.

The Feds seem undeterred from the path of gradual normalisation by the recent market turmoil, and we should not expect a Powell ” Put.” given the economic indicators remain strong. And with FED Dudley chiming in, the recent Stock market volatility is ” no big potatoes.” , just imagine a big potato !!

Oil Markets

U.S. crude oil fell below $59 a barrel for the first time in 2018.Rising US production and a resurgent dollar have stacked pressure on oil prices amid a broad financial market sell-off. And on Friday WTI nosedived after the U.S. rig count rose by 26 rigs in the week through Feb. 9 to a total of 791, supporting the EIA revised production forecast that the US would reach the lofty 11 million bpd by the end of 2018

Also, the possible demise of the OPEC agreement has traders on pins and needles after The head of Russian energy giant Gazprom Neft on Friday said producers could adjust their commitments under the deal as soon as next quarter.

Gold Markets

Without question last week was a stressful week in the Gold markets which saw a little appeal for traditional haven assets as Wall streets sinkhole expanded.

At the moment higher US yields continue to weigh negatively on gold’s appeal over the short term, but the recent market tumult likely has overleveraged equity positions scrambling for margin top-ups, and to a degree, there was cause for some cross-asset unwinds including gold allocations which were probably used to fund margins.

In the more extended run with inflation expectations increasing on the back of US stimulus, this should be a consideration for growing one’s gold portfolio.

At the retail levels, Mainland Gold consumption is rising in preparation for Chinese Lunar New Year holidays, not to mention a last-minute splurge for Valentine’s day should keep retailers busy.

Currency Markets

Currency markets were more or less a mixed bag last week, a potpourri of events but not one convincing driver. And with little to glean from Friday close, currency traders could remain sidelined watching equities markets swings in wonderment at least until this week’s US CPI. Given all this rukus started with an uptick in the wage growth component from this months NFP release; this weeks US inflation data will be a monster of a print.

Japanese Yen

Funding positions continue to unwind which at least in the case of JPY, is having a more significant influence over USDJPY than higher US yields. The reappointment of Kuroda could retrace some speculations on the policy adjustments; the Yen will remain the puppet whose strings are manipulated by equities and fixed income price movements.

Australian Dollar

RBA and SOMP behind us and signalling nor rush to hike for a considerable period given the slight dovish lean in the inflation outlook. The AUD should, therefore, be back trading off risk sentiment, commodity prices and ultimately the underlying USD movements. While the Aussie bounced higher above 78 on positive US equity close on Friday, we should expect commodity currencies trade poor amid the recent volatile market. Rallies will likely remain subdued near-term, so the Aussie should remain vulnerable.

Long Euro short Aussie trade set up should return in vogue over the short term given divergent central bank policy expectations.

Malaysian Ringgit

The market continues to grapple with growth versus the inflation narrative, and as this volatility irons itself out, Asian markets tend to exhibit a higher sensitivity to global fluctuations.

And while the Ringgit is better positioned than regional peers to withstand the recent uptick in Global volatility due to strong Marco foundations and the BNM on the path to interest rate normalisation, The domestic economic landscape will come under intense glare when Q4 GDP is released on Wednesday.

While March a rate hike expectations are low due to the dovish inflation overtones expressed by BNM in January, but a notable above consensus print on this weeks GDP will increase the odds of a rate hike later in 2018 and strengthen the Ringgit. ( Consensus is 5.8 )

While oil prices continue to move lower due to US supply concerns, I believe this is more technical driven as dollar index is holding above 90 cents, putting pressure on all commodities. Once this period of excess volatility decreases, the global growth narrative should reassert and commodity prices should rise.

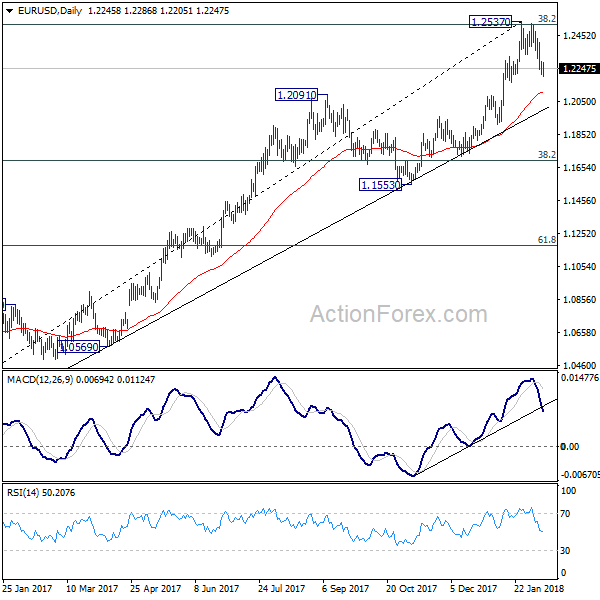

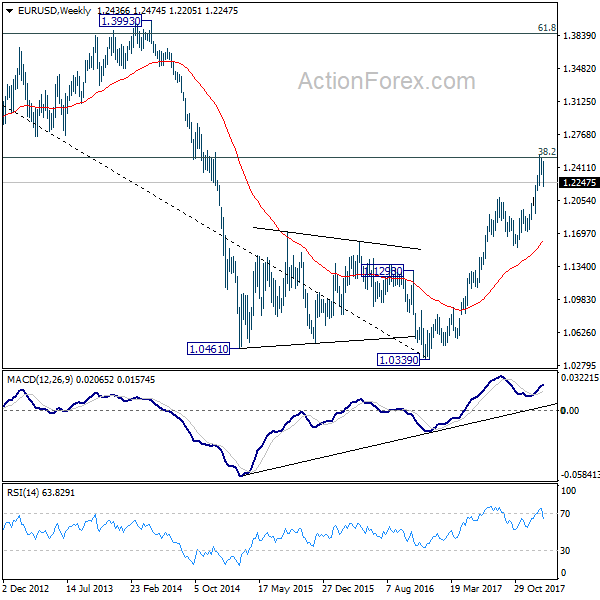

EUR/USD Weekly Outlook

EUR/USD dropped to as low as 1.2205 last week but failed to sustain below 1.2222 key support so far. Initial bias remains neutral this week first, with focus on 1.2222. Sustained break there should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

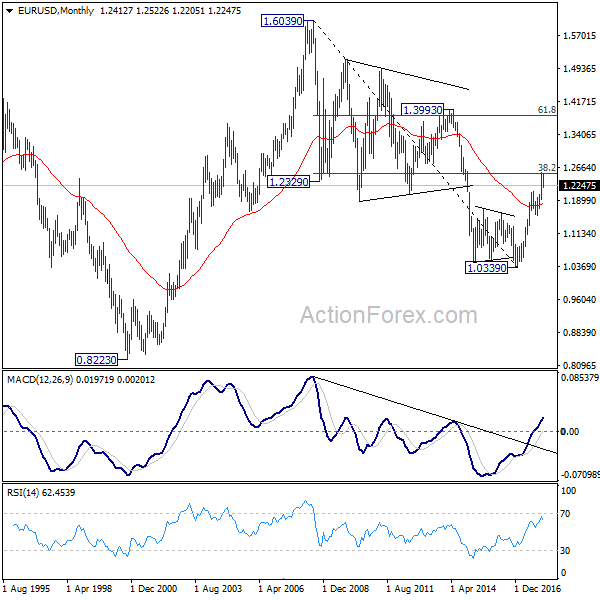

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

In the long term picture, 1.0339 is seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action from 1.0339 is developing into a corrective or impulsive pattern. Reaction to 38.2% retracement of 1.6039 to 1.0339 at 1.2516 will give important clue to the underlying momentum.

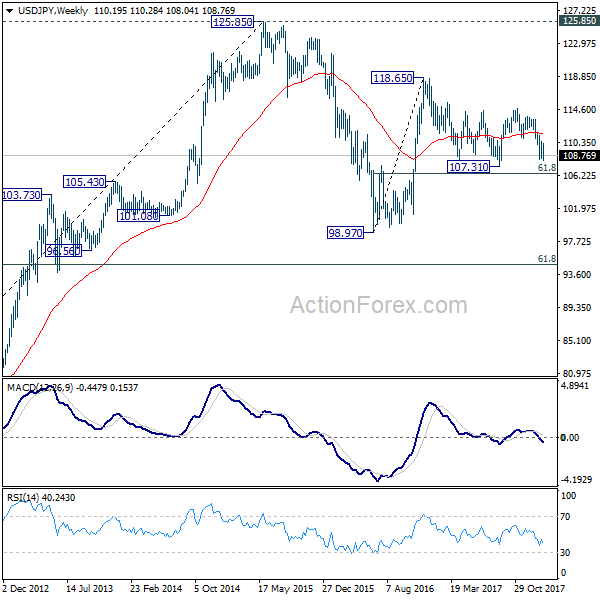

USD/JPY Weekly Outlook

USD/JPY's break of 108.27 low last week indicates resumption of larger fall from 114.73. Initial bias remains on the downside this week. Such decline is part of the pattern from 118.65 high and should target 106.48 fibonacci level. On the upside, break of 110.47 resistance is needed to indicate near term reversal. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

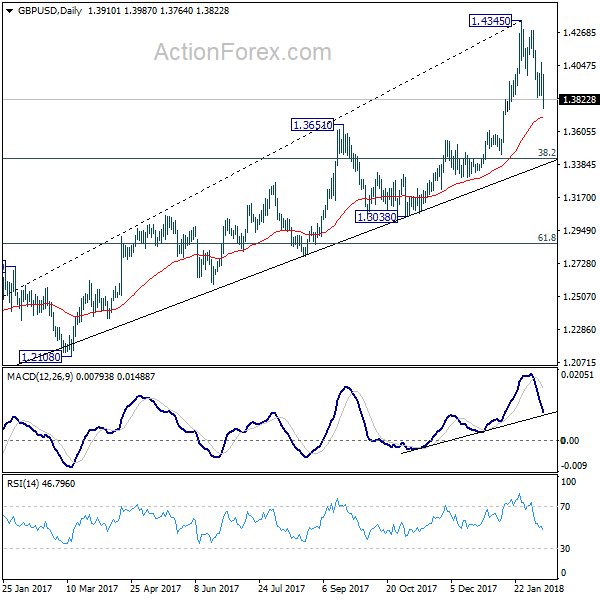

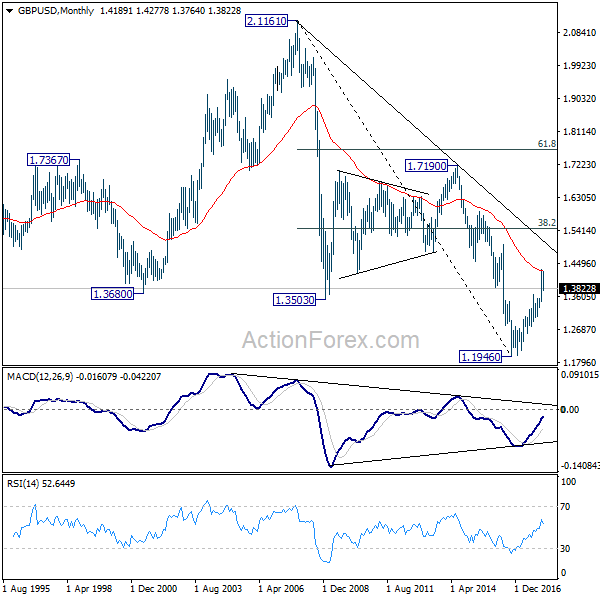

GBP/USD Weekly Outlook

GBP/USD's corrective fall from 1.4345 extended lower last week. Initial bias remains on the downside this week for 1.3651 resistance turned support. At this point, it's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. For the moment, further decline will remain expected as long as 1.4066 minor resistance holds.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

In the longer term picture, rise from 1.1946 should at least be correcting the whole long term down trend form 2.1161 and should target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. It too early to tell if it's developing into a long term up trend. We'll monitor the upside momentum and reaction to 1.5466 to decide later.

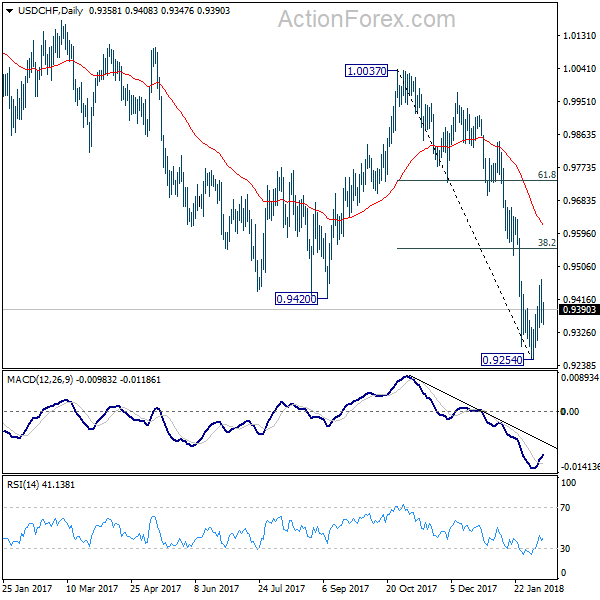

USD/CHF Weekly Outlook

USD/CHF recovered to 0.9469 last week but lost momentum and retreated. Initial bias is neutral this week first. At this point, there is no clear sign of trend reversal yet. Therefore, in case of another rise, we'd be e cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring decline resumption. On the downside, below 0.9339 minor support will turn bias to the downside for 0.9254. Nonetheless, firm break of 0.9553 will bring stronger rebound to 55 day EMA (now at 0.9616).

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

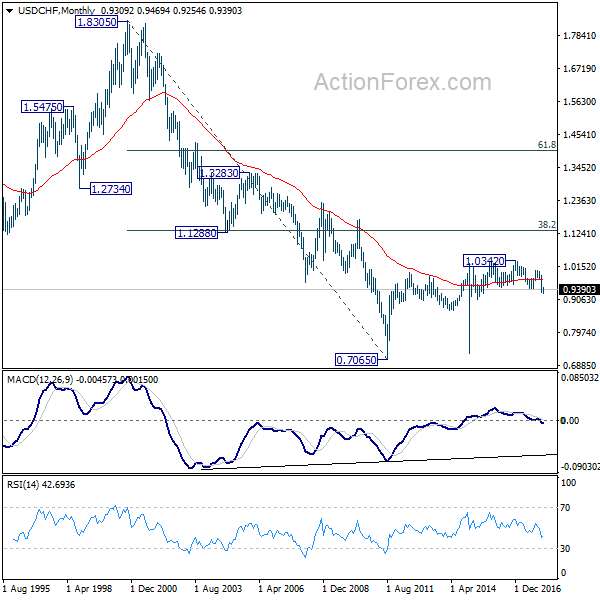

In the long term picture, the strong break of 0.9420 support and downside acceleration turns the long term outlook rather bearish. Corrective rebound from 0.7065 (2011 low) could have already completed at 1.0342. 0.8698 support will be a key level to watch. Sustained break there could bring retest of 0.7065.