Sample Category Title

Market Update – European Session: Awaiting US House To Approve Spending Bill To Reopen Govt

Notes/Observations

Market volatility remained elevated as concern simmer that central banks were not keeping up with global economic growth.

Senate passed a two-year budget deal in the wee hours of Friday morning; after the government was forced into a technical shut down at midnight due to a political stunt by Sen. Rand Paul (R-KY); Government would reopen once the bill cleared the House in the predawn hours

Asia:

RBA Quarterly Statement on Monetary Policy (SOMP) made little resison to its growth and inflation outlook. Outlook for global growth was positive despite volatility in equity markets: Reiterated an appreciating A$ would dampen domestic growth and inflation

China Jan CPI in-line at 1.5% y/y - China PBoC again skipped its Open Market Operation (OMO) for the 12th straight session (12th straight session)

China PBoC noted that it had released Temporary liquidity worth almost CNY2.0T to help satisfy cash demand before Lunar New Year

Japan Economy Min Motegi: Economic fundamentals were strong both in the US and Japan; reiterated monitoring impact of financial markets on economy

Japan PM Abe Adviser Hamada noted that the BOJ should stick with current easy settings; recent stock declines could make BoJ cautious about raising rates

Europe:

UK Govt spokesperson: Business representatives expressed importance of time-limited implementation period in providing clarity

Labour party Jeremy Corbyn (opposition) said to have told EU’s Barnier he was open to keeping Britain in the customs union after Brexit; wlling to allow the UK to submit to ECJ rulings should he become PM

Americas:

Senate approved a far-reaching budget deal that would reopen the federal government and boost spending by hundreds of billions of dollars

Bank of Canada (BOC) Wilkins: high household debt was the largest vulnerability to the Canadian economy

Mexico Central Bank raised the Overnight Rate by 25bps to 7.50% (as expected) for its 12th hike in the current tightening cycle.

Economic Data:

(NL) Netherlands Dec Manufacturing Production M/M: 0.6% v 1.1% prior; Y/Y: 5.2% v 4.4% prior, Industrial Sales Y/Y: 0.7% v 12.9% prior

(CH) Swiss Jan Unemployment Rate: 3.3% v 3.4%e, Unemployment Rate (seasonally Adj): 3.0% v 3.0%e

(FI) Finland Dec Industrial Production M/M: 0.0% v 0.8% prior; Y/Y: 4.2% v 4.2% prior

(NO) Norway Jan CPI M/M: -0.1% v +0.1%e; Y/Y: 1.6% v 1.6%e

(NO) Norway Jan CPI Underlying M/M: -0.8% v -0.2%e; Y/Y: 1.1% v 1.5%e

(NO) Norway Q4 GDP Q/Q: -0.3%v 0.8% prior; Mainland GDP Q/Q: 0.6% v 0.6%e

(CN) Weekly Shanghai copper inventories (SHFE): 186.1K v 172.6K tons prior

(FR) France Dec Industrial Production M/M: 0.5% v 0.1%e; Y/Y: 4.5% v 3.5%e

(FR) France Dec Manufacturing Production M/M: +0.3% v -0.5%e; Y/Y: 4.7% v 3.4%e

(IT) Italy Dec Industrial Production M/M: 1.6% v 0.8%e; Y/Y: -1.3% v +2.3% prior, Industrial Production WDA Y/Y: 4.9% v 1.9%e

(UK) Dec Industrial Production M/M: -1.3% v -0.9%e; Y/Y: 0.0% v 0.3%e

(UK) Dec Manufacturing Production M/M: 0.3% v 0.3%e; Y/Y: 1.4% v 1.2%e

(UK) Dec Construction Output M/M: +1.6% v -0.1%e; Y/Y: -0.2% v -1.9%e

(UK) Dec Visible Trade: -£13.6B v -£11.6Be, Overall Trade Balance: -£4.9B v -£2.4Be, Trade Balance Non EU: -£5.2B v -£4.1Be

Fixed Income Issuance:

(IN) India sold total INR110B vs. INR110B indicated in 2024 and 2028 bonds

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.5% at 372.1, FTSE -0.4% at 7144, DAX -0.3% at 12221, CAC-40 -0.4% at 5129 , IBEX-35 -0.7% at 9689, FTSE MIB -0.3% at 22407 , SMI +0.1% at 8768, S&P 500 Futures +0.7%]

Market Focal Points/Key Themes: European Indices trade mostly lower but off the session lows after a rebound in US Futures overnight after sharp falls yesterday. Increased outlook for higher rates in the UK weigh on the FTSE, as the index under performs. Ont he corporate front Maersk trades lower after Q4 results; Ceconomy also trades lower after a fall in profits. To the upside Trinity Mirror outperforms after its trading update, Flow Traders trades over 10% higher after strong y/y growth. In the M&A space Hogg Robinson trades sharply higher after receiving a bid from American Express Global, representing a 54% premium to prior close. Looking ahead earners include PG&E, Tenneco and Moody's.

Movers

Consumer Discretionary [ Hogg Robinson [HRG.UK] +49% (To be acquired for 120p/shr], Trinity Mirror [TNI.UK] +7.3% (Trading update, acquisition), Ceconomy [CEC.DE] -2.0% (Earnings), L'Oreal [OR.FR] +0.8% (Earnings), Bechtle [BC8.DE] +1.0% (Prelim earnings)]

Industrials [Maersk [MAERSKB.DK] -2.9% (Earnings), Victrex [VCT.UK] +1.2% (Prelim results)]

Technicals [Fingerprint Cards [FINGB.SE] +1.1% (Earnings)]

Financials [Flow Traders [FLOW.NL] +13.0% (Earnings)]

Speakers

BoE Deputy Gov Broadbent reiterated MPC stance that rate hikes could come sooner than expected but will remain limited and gradual

UK PM May said to be planning Brexit meeting with senior cabinet ministers in two weeks’ time. Meeting requested after trade sub-committee ended without a decision

Czech Central Bank Feb Minutes: Interest rate outlook conditional on pace of CZK currency appreciation. Slow return of ECB to normal rates could inhibit Czech rate growth

Romania Central Bank gov Isarescu: Inflation acceleration was broad-based. Reiterated view that RON currency (Leu) had no more room for appreciation

Italy's Berlusconi Forza (Italia party): Gentiloni should stay as PM if no majority achieved at the March election

Currencies

Risk aversion sentiment remained on the front burner but the major FX pairs stayed locked within recent ranges. The USD maintaining its recent strength as some analysts believe the Fed might be behind the curve on rates. One analyst noted that given how sensitive markets were to a slightly hawkish BoE yesterday, one can only imagine the turmoil on Wednesday next week if US CPI comes in ahead of expectations

EUR/USD was slightly higher by 0.2% at 1.2270

GBP/USD at 1.3920

USD/JPY at 109.03

Fixed Income

Bund Futures trades down 7 ticks at 158.07 as the bearish trend remains intact. Upside targets 159.85, while a continued move lower targets the157.25 level.

Gilt futures trade at 121.09 down 8 ticks, as the BoE turns more hawkish. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.75 then 123.25.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.901T from €1.895T prior. Use of the marginal lending facility rose to €70M from €50M prior.

Corporate issuance saw 5 issuers raise $8.5B in the primary market.

Looking Ahead

(MX) Mexico Jan Nominal Wages: No est v 5.2% prior

(UR) Ukraine Jan CPI M/M: No est v 1.0% prior; Y/Y: No est v 13.7% prior

05:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cuts Key 1-Week Auction Rate by 25bps to 7.50%

06:00 (BR) Brazil Dec Retail Sales M/M: -0.5%e v +0.7% prior; Y/Y: 4.6%e v 5.9% prior

06:00 (BR) Brazil Dec Broad Retail Sales M/M: -0.9% v +2.5% prior; Y/Y: 5.7%e v 8.7% prior

06:00 (UK) DMO to sell combined £3.0B in 1-month, 3-month and 6-month Bills (£0.5, £0.5B and £2.0B respectively)

06:30 (IN) India Weekly Forex Reserves

06:30 (EU) EU chief Brexit negotiator Barnier to hold press conference

06:45 (US) Daily Libor Fixing

07:00 (UK) Jan NIESR GDP Estimate: 0.5%e v 0.6% prior

08:00 (RU) Russia Dec Trade Balance: $13.0Be v $11.5B prior

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond auction (held on Thurs)

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Jan Net Change in Employment: +10.0Ke v +64.8K prior (revised from +78.6K); Unemployment Rate: 5.8%e v 5.8% prior (revised from 5.7%)

09:00 (MX) Mexico Dec Industrial Production M/M: +0.4%e v -0.1% prior; Y/Y: -0.7%e v -1.5% prior, Manufacturing Production Y/Y: 2.5%e v 2.4% prior

10:00 (US) Dec Final Wholesale Inventories M/M: 0.2%e v 0.2% prelim, Wholesale Trade Sales M/M: 0.4%e v 1.5% prior

11:00 (EU) Potential sovereign rating after European close (Czech and Finland Sovereign Debt to be rated by Fitch

11:45 (UK) BOE’s Cunliffe in CA

13:00 (US) Weekly Baker Hughes Rig Count data

14:00 (CO) Colombia Central Bank Jan Minutes 21:00 (US) Fed’s George (non-voter, hawk) on economy

Technical Outlook: WTI OIL In Narrow Consolidation, Broader Bears Remain Intact And Threaten For Attack At Rising Daily Cloud

WTI oil is holding within narrow consolidation above fresh five-week low at $60.26 on Friday, after suffering heavy losses during the week.

Oil remains under strong pressure on increased US oil production, with fresh pressure coming from announcement of Iran's plans to boost production.

Steep two-week fall from recovery peak at $66.64, posted on 25 Jan, threaten of further extension through key supports at $60.00 zone (psychological support / Fibo 61.8% of $55.81/$66.64 ascend) and $59.51 (top of rising daily Ichimoku cloud).

Bears may take a stronger breather as ascending daily cloud underpins and daily slow stochastic is deeply oversold, but so far lacking stronger bullish signal.

Extended consolidation could be likely scenario as weekly indicators turned south after emerging from overbought territory and show plenty of space at the downside.

In addition, oil is on track for strong weekly bearish close (the second straight week in red and the biggest one week loss since early March 2017), which heavily weighs.

Broken 30SMA marks initial resistance at $60.90, with stronger upticks to be capped under previous pivotal support at $62.50 (broken Fibo 38.2% of $55.81/$66.64 rally).

Res: 60.90, 61.23, 62.07, 62.50

Sup: 60.26, 60.00, 59.51, 59.02

DAX Slide Continues As US Markets See Red

The DAX index has posted sharp losses in the Friday session. Currently, the index is trading at 12,210.00, down 0.41% on the day. On the release front, there are no German or Eurozone indicators on the schedule.

Nervous investors continues to watch the massive sell-offs in the markets, and European markets have been following the downward trend in the North American and Asian sessions. It’s been a blue February for the DAX, which has plunged 7.8 percent. On Thursday, the DAX dropped to its lowest level since early September. Interestingly, the catalyst for the current turbulence has been solid economic data in the US, namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

It’s been a slow process, but Germany finally is on the verge of forming a new government. On Wednesday, the socialist SDP and Angela Merkel’s conservatives announced that they had finalized a coalition agreement. In the last government, the SDP was the junior partner of the conservatives, but this time around the SDP has extracted major concessions from Merkel, including the finance and foreign affairs ministries. This will likely mark a shift in Germany’s eurozone policy, which had been marked by a conservative stance under former finance minister Wolfgang Schaeuble. The weaker members of the eurozone, such as Greece, will likely find a more sympathetic ear for financial help from the SDP than they did from Schauble. The coalition agreement still requires the consent of a majority of the 464,000 members of the SDP, but is expected to pass this final hurdle.

Euro Steady, Nervous Investors Brace For More Stock Market Losses

The euro has posted slight gains in the Friday session, erasing the losses on Thursday. Currently, the pair is trading at 1.2266, up 0.16% on the day. On the release front, there are no major releases on the schedule. French Industrial Production improved to 0.5%, above the estimate of 0.1%. Italian Industrial Production impressed with a gain of 1.6%, well above the estimate of 0.7%. In the US, the sole event is Final Wholesale Inventories, which is expected to slow to 0.2%.

A rebound in the global economy has been a boon for eurozone exports, and this has boosted the bloc’s manufacturing setor. This was underscored by strong manufacturing reports out of France and Italy in December. Industrial production in both countries improved compared to November, beating the estimates. The Italian reading of 1.6% marked the strongest gain since August 2016. We’ll get a look at Eurozone Industrial Production next week. The November reading surged to 1.0%, marking a 3-month high.

The euro has been under pressure for most of the week, and is down 1.5 percent against the US dollar. The greenback has benefited from sharp volatility in global stock markets this week. The week started with a massive sell-off, and the markets have been in the red for most of the week. This has weighed on the euro, with investors anticipating a faster pace of rate hikes from the Federal Reserve in order to ward off inflation. The Fed had forecast raising interest rates three times in 2018, but if inflation does move higher and the US economy continues its robust performance, we could see four rate hikes this year.

After months of political uncertainty, Germany appears on the verge of forming a new government. On Wednesday, the socialist SDP and Angela Merkel’s conservatives announced that they had finalized a coalition agreement. In the last government, the SDP was the junior partner of the conservatives, but this time around the SDP has extracted major concessions from Merkel, notably control of the powerful finance ministry. This will likely mark a shift in Germany’s eurozone policy, which had been marked by a conservative stance under former finance minister Wolfgang Schaeuble. The weaker members of the eurozone, such as Greece, will likely find a more sympathetic ear for financial help from the SDP than they did from Schauble. The coalition agreement still requires the consent of a majority of the 464,000 members of the SDP, but is expected to pass this final hurdle.

Technical Outlook: AUDUSD – Broader Bears May Take A Breather Ahead Of Key 0.7850/40 Support Zone

The Australian dollar bounced from new 2018 low at 0.7758 posted on Friday, signaling hesitation ahead of strong supports at 0.7750/40 (200SMA/Fibo 61.8% of 0.7500/0.8135/rising daily cloud top). The pair is moving in steep two-week descend from 0.8135 peak, which could take a breather on oversold studies and week-end profit-taking. Initial barrier at 0.7800 has been tested, with 0.7850 zone coming next and extended upticks to be capped under 0.7900 zone (Fibo 38.2% of 0.8135/0.7758 fall/06/07 Feb double upside rejection) to keep overall bears intact.

Res: 0.7800, 0.7847, 0.7910, 0.7937

Sup: 0.7758, 0.7750, 0.7740, 0.7687

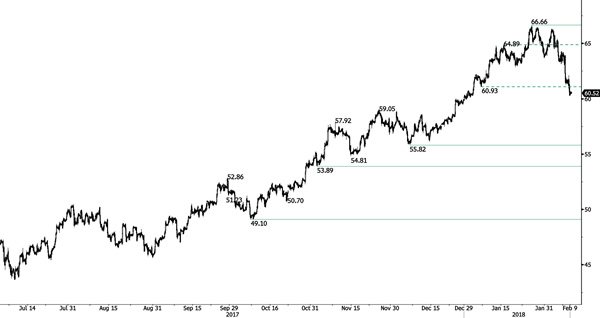

CRUDE OIL Decline Still In Place

Crude oil has broken the key support at 60.93 (05/01/2018 low). Hourly resistances stand at 62.80 (08/02/2018). Strong support is located at 55.82 (06/12/2017 low). Expected to keep increasing as demand remains strong.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Weak Bounce

Silver keeps heading lower and trades now below 16.50. The short-term technical structure is turning negative. Hourly resistance lies at 18.21 (08/09/2017 high). The technical structure suggests further short-term decrease.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Recovery Bounce

Gold is recovering after its recent strong sell-off. Resistance is located at 1326 (04/01/2018). Support is now at 1306 (12/01/2018 low). The technical structure suggests however further downside moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Solid Recovery Bounce

Bitcoin is now retracing above 8200. Strong support stands at 5605 (13/11/2017 low) .Hourly resistance remains at 18628 (08/02/2018). The short-term technical structure suggests further upside moves.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading above its 200 DMA (6'000 range).

EUR/CHF A New Phase Of Weakness Is Expected

EUR/CHF stabilizes. has broken the key resistance area between 1.1525 and 1.1649. This validates a bearish reversal pattern with an upside potential at 1.1388. Hourly resistance can now found at 1.1593. Next resistance is given at 1.1685 (26/01/2018 high).

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).