Sample Category Title

Sterling Reversed Post BoE Gains, Tumbles Broadly on Barnier’s Brexit Transition Warning

Sterling tumbles sharply today after EU Brexit negotiator Michel Barnier warned that a transition deal is "not a given". That came as Barnier concludes the week long technical discussion between civil servants of UK and EU. And he pointed out there are three "substantial" disagreements remained over the transition period. Firstly, UK wants the rights of EU citizens coming in during the transition period to be different from those who come in before. Secondly, UK wants to retain the right to object to new EU laws during the period. Thirdly, it's uncertain how UK could have a role in new EU justice and home affairs policies during the transition.

US budget deal approved after midnight drama

After some mid-night drama and temporary government shutdown, the US Congress finally approved the 2 year budget deal that would also suspend the debt limit through March 1, 2019. A delay was forced upon by Rand Paul in the Senate as he demanded a vote to keep budget caps in place. Finally, Senate voted 71 to 28 while House voted 240 to 186. Included in the bill is a short term funding for the government through March 23. And the lawmakers now have six weeks to detail the legislation regarding funding at the new level.

RBA lowered unemployment forecast

In the monetary statement published today, RBA lowered unemployment rate forecasts but kept projections on growth and inflation unchanged. Year average GDP growth is projected to be at 3% in 2018 and 3.25% in 2019. CPI is projected to be at 2.25% by the end of 2018 and stay at 2.25% by the end of 2019. Unemployment rate, though, is forecast to drop from current 5.5% to 5.25% by the end of 2018, revised down from 5.50%. Unemployment is forecast to stay at 5.25% till end of 2019.

RBA noted that "financial market volatility has picked up in recent days, most notably in equity markets as market participants have begun to reassess the outlook for global inflation and the withdrawal of monetary accommodation". And, "an important consideration for the outlook is how far inflation picks up as the global economy strengthens." It added that "a larger-than-expected increase in inflation would have implications both for financial market pricing and exchange rates."

On the data front

Canada employment dropped -88k in January, much worse than expectation of 10k rise. Unemployment rate also jumped 0.2% to 5.9%. UK industrial production dropped -1.% mom, rose 0.0% yoy in December, manufacturing production rose 0.3% mom, 1.4% yoy. Trade deficit widened to GBP -13.6b in December. Swiss unemployment rate was unchanged at 3.0% in January. Japan tertiary industry index dropped 00.2% mom in December, M2 rose 3.4% yoy in January. Australia home loans dropped -2.3% mom in December. China CPI slowed to 1.5% yoy in January, PPI slowed to 4.3% yoy.

Also from Australia, home loans dropped more than expected by -2.3% mom in December.

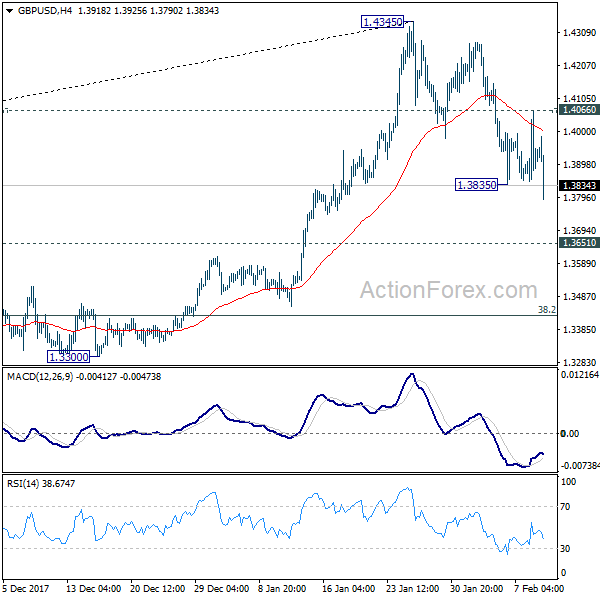

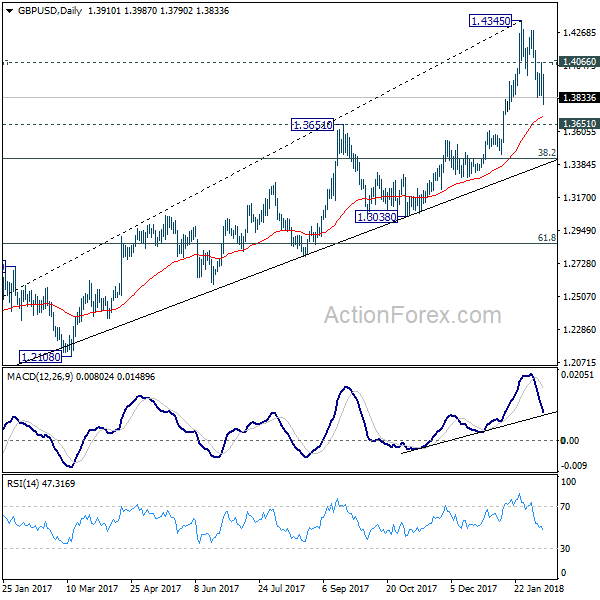

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3814; (P) 1.3940; (R1) 1.4035; More.....

GBP/USD's recovery was limited by 4 hour 55 EMA. Subsequent break of 1.3835 indicates resumption of decline from 1.4345 and intraday bias is turned to the downside for 1.3651 resistance turned support. At this point, it's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. For the moment, further decline will remain expected as long as 1.4066 minor resistance holds.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish 38.2% retracement of 1.1946 to 1.4345 at 1.3429, in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jan | 3.40% | 3.60% | 3.60% | |

| 00:30 | AUD | Home Loans M/M Dec | -2.30% | -1.00% | 2.10% | 1.60% |

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 01:30 | CNY | CPI Y/Y Jan | 1.50% | 1.50% | 1.80% | |

| 01:30 | CNY | PPI Y/Y Jan | 4.30% | 4.20% | 4.90% | |

| 04:30 | JPY | Tertiary Industry Index M/M Dec | -0.20% | 0.10% | 1.10% | |

| 06:45 | CHF | Unemployment Rate Jan | 3.00% | 3.00% | 3.00% | |

| 09:30 | GBP | Industrial Production M/M Dec | -1.30% | -0.90% | 0.40% | 0.30% |

| 09:30 | GBP | Industrial Production Y/Y Dec | 0.00% | 0.40% | 2.50% | 2.60% |

| 09:30 | GBP | Manufacturing Production M/M Dec | 0.30% | 0.30% | 0.40% | 0.20% |

| 09:30 | GBP | Manufacturing Production Y/Y Dec | 1.40% | 1.20% | 3.50% | 3.80% |

| 09:30 | GBP | Construction Output M/M Dec | 1.60% | -0.10% | 0.40% | 0.10% |

| 09:30 | GBP | Visible Trade Balance (GBP) Dec | -13.6B | -11.5B | -12.2B | -12.5B |

| 12:00 | GBP | NIESR GDP Estimate Jan | 0.50% | 0.50% | 0.60% | |

| 13:30 | CAD | Net Change in Employment Jan | -88.0K | 10K | 78.6K | |

| 13:30 | CAD | Unemployment Rate Jan | 5.90% | 5.80% | 5.70% | |

| 15:00 | USD | Wholesale Inventories M/M Dec F | 0.20% | 0.20% |

Dollar Edges Up as US Government Re-Opens; European Stocks Tumble Again

Here are the latest developments in global markets:

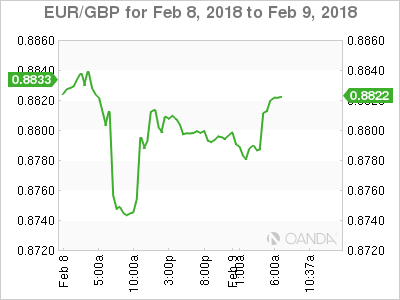

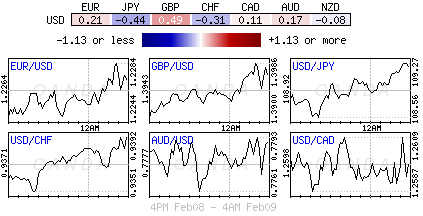

FOREX: The dollar was gaining versus its major counterparts during early European trading hours, posting moderate gains after the US Congress reached a bipartisan deal on a two-year spending bill. The plan promises to increase the debt ceiling and funding on military and domestic programs, though, the markets are concerned that the bill will widen nation's deficit. The dollar index edged up to 90.33 (+0.12%), while dollar/yen and dollar/swissie changed hands higher at 109.13 (+0.35%) and 93.74 (+0.16%) respectively after deep falls yesterday. Pound/dollar could not sustain Thursday's rally triggered by hopes that the BOE will raise interest rates faster than expected following hawkish BOE comments. Today's encouraging British industrial production figures could not support the pair either, with pound/dollar giving up yesterday's gains and slipping back to 1.3875 (-0.22%). Euro/pound was up at 0.8820 (+0.25%), while euro/dollar pared earlier gains sliding to at 1.2241 (-0.03%). Dollar/loonie extended its uptrend towards a fresh five-week high of 1.2615 (+0.04%). Aussie/dollar was slightly up at 0.7785 (+0.09%) (large option expiries are expected to take place today), while kiwi/dollar was last seen at 0.7222 (+0.08%).

STOCKS: The fresh sell-off in the US and Asian equity markets amid rising bond yields and inflation fears spread to the European stocks once again. The pan-European STOXX 600 which lost over 4.0% this year, was trading 0.40% lower at 1045 GMT driven by losses in financials, utilities, and energy, while the blue-chip Euro STOXX 50 was down by 0.36%. The Spanish IBEX 35 declined by 0.35%, the French CAC 40 fell by 0.19%, and the German DAX 30 inched down by 0.09%. US stock futures were in the red, pointing to a negative open.

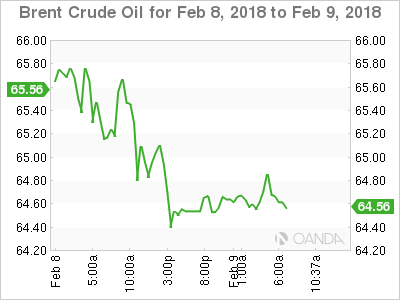

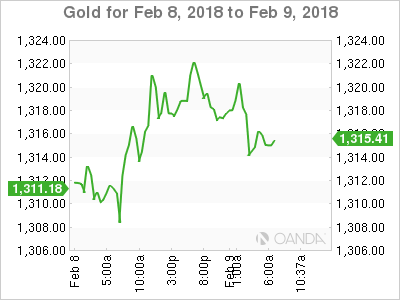

COMMODITIES: Oil prices were on track to post the worst weekly performance in ten months as concerns over a rising global supply rose after the Energy Information Administration (EIA) stated on Wednesday that the US crude oil production per day touched a record high. Thursday's news that OPEC's member Iran is planning to raise production the next four years added further pressure to the market. WTI crude oil dived by 1.0% on the day to $60.52/barrel, remaining near five-week lows and Brent dropped by 0.62% to $64.41/barrel. In precious metals, gold retreated by 0.32% to $1,314.70/ounce.

Day ahead: Canada's employment data pending

Looking at the economic calendar, Canada will see the release of employment figures at 1330 GMT. However, forecasts show that analysts remain cautious on the labor market despite recent evidence surpassing their projections. Particularly, they believe that the number of employees will increase by 10,000 in January after a strong rise of 78,600 in December, while regarding the unemployment rate, projections are for the measure to inch up by 0.1 percentage points to 5.8%. Note that the Canadian unemployment rate is currently at the lowest level seen in four decades.

In other data, the US will publish readings on wholesale inventories for the month of December at 1500 GMT, while Baker Hughes will report on the US oil rig counts at 1800 GMT, adding further volatility to oil prices.

Regarding today's public appearances, Jon Cunliffe, the Bank of England's Deputy Governor for Financial Stability will be speaking at 1645 GMT.

Corporations continue to release quarterly results as the equity market turmoil persists.

Global Equity Markets Resume Rollercoaster Ride, Gold Sinks Lower

It has certainly been a chaotic trading week for the global equity markets, amid fears of mounting inflationary pressures and higher interest rates.

Asian shares suffered heavy losses during early trading on Friday following Wall Street's steep declines overnight.

Wall Street experienced severe losses on Thursday with the Dow Jones Industrial Average plunging more than 1000 points. Now US stock markets have officially entered "correction territory", investors are wondering whether the long-awaited stock market correction could be upon us. This fear will also likely encourage investors to reconsider whether to potentially purchase stocks at these lower levels, with it being a possibility that the current selloff might be more than just a short-term correction.

Sterling bulls run out of steam

Sterling weakened against the Dollar on Friday, as market excitement over the Bank of England raising interest rates sooner than expected slowly fizzled out.

Although the possibility of higher UK rates could continue supporting the Pound, headwinds around global market volatility and ongoing Brexit uncertainty have the ability to limit upside gains. There was a more muted reaction from investors following the manufacturing and industrial production figures for December, suggesting that investors are not paying as much attention towards the UK economy when speculating over which way Sterling could possibly go next.

From a technical perspective, the GBPUSD failed to achieve a daily close above the 1.4000 level on Thursday. Sustained weakness below 1.4000 suggests that sellers can drive the Pound lower over the coming sessions.

Dollar smiles into weekend

The Dollar edged higher against a basket of major currencies on Friday, thanks to renewed market expectations of higher US interest rates this year.

While there is scope for the Dollar to venture higher amid heightened US rate hike expectations, political uncertainty in Washington could expose the currency to downside risks. Taking a look at the technical picture, the Dollar Index is slowly turning bullish on the daily charts. A solid breakout and weekly close above 90.55 could encourage an incline towards 91.00 and 92.40, respectively.

Commodity spotlight - Gold

Gold weakened on Friday with prices sinking towards $1314 despite equity markets across the globe suffering heavy losses.

It is becoming increasingly clear that the yellow metal remains pressured by a stabilising Dollar and rising expectations of higher US interest rates. Investors would usually expect Gold to benefit from increased stock market volatility, but this has so far not been the case.

If speculation continues to increase over developed central banks increasing respective interest rates, Gold is at risk to further selling pressure.

Focusing on the technical picture, the yellow metal is bearish on the daily charts. Previous support at $1324.15 could transform into a possible "top", potentially encouraging further declines towards the lower $1300s.

EURUSD: Remains Vulnerable On Bear Pressure

EURUSD: The pair closed lower on further weakness on Thursday leaving risk of more weakness on the cards. On the upside, resistance comes in at 1.2300 level with a cut through here opening the door for more upside towards the 1.2350 level. Further up, resistance lies at the 1.2400 level where a break will expose the 1.2450 level. Conversely, support lies at the 1.2200 level where a violation will aim at the 1.2150 level. A break of here will aim at the 1.2100 level. Below here will open the door for more weakness towards the 1.2050. Its daily RSI is bearish and pointing lower suggesting more weakness. All in all, EURUSD faces further pullback threats.

Pound Falls Below 1.39, Delated by Downbeat UK Data

Cable fell below 1.3900 handle in Europe, deflated by downbeat trade balance/IP data. Trade deficit widened to 13.5 billion pounds in Dec from forecasted 11.5 billion gap, while industrial production fell by 1.3% in Dec, falling below forecasted 0.9% fall and against downward-revised previous month's 0.3% release.

Fresh easing after recovery failed under 1.40 pivot and loss of 1.39 handle weakens near-term structure and turns near-term focus lower again, after hawkish comments from BoE on Thu/Fri showed limited and short-lived positive impact on sterling.

Temporary base at 1.3840 zone, reinforced by rising 30SMA is coming under increased pressure as risk of continuation of pullback from 1.4277 lower top is intensifying.

Thursday's strong upside rejection above 1.40 which left daily candle with long upper shadow, weighs on near-term action for renewed attack at 1.3840 base.

Firm break here would open next strong support at 1.3796 (Fibo 61.8% of 1.3457/1.4344 upleg) and could trigger stronger bearish acceleration on break lower.

Broken 1.39 point now acts as initial resistance and guarding pivotal barrier at 1.4000 (20SMA / psychological barrier).

Res: 1.3900; 1.3986; 1.4000; 1.4033

Sup: 1.3854; 1.3835; 1.3796; 1.3667

Canadian Dollar in Holding Pattern Ahead of Key Job Reports

The Canadian dollar has ticked higher in the Friday session. Currently, the pair is trading at 1.2609, up 0.05% on the day. On the release front, the focus is on Canadian employment indicators, with the release of Employment Change and the unemployment rate.

This week's market selloff has boosted the US dollar, at the expense of the Canadian dollar and most other major currencies. The Canadian dollar has dropped 1.4% this week, and is down 2.5% in February, erasing the gains we saw in January. Interestingly, the catalyst for the current turbulence has been solid economic data in the US, namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

After some spectacular readings, Canada's economy is expected to show more modest job creation in January, with an estimate of 10.3 thousand. The unemployment rate is forecast to edge up from 5.7% to 5.8%. If these predictions are within expectations, the Canadian dollar could gain some ground on Friday, and end a tough week on a positive note.

Technical Outlook: Spot Gold – Bears To Resume After A Breather, Thick Hourly Cloud Weighs Heavily

Spot Gold fell to European session low at $1313, coming under renewed pressure after recovery attempts were repeatedly rejected at $1322 (Thu/Fri).

Yesterday’s long-tailed Doji signaled a breather in broader downtrend, with fresh easing keeping near-term bias with bears.

Weaker dollar on the second US government shutdown in 2018 showed little impact to the yellow metal which keeps focus at the downside.

However, bearish continuation requires stronger signal which will be generated on close below cracked $1316 pivot (Fibo 38.2% of $1236/$1366 ascend) and would expose 55SMA ($1302) and psychological $1300 support.

Near-term action is heavily pressured by thick falling hourly cloud (spanned between $1317 and $1327) which is expected to limit stronger recovery attempts.

Thin calendar from the US on Friday signals lack of fundamentals and suggests the yellow metal’s price would be driven by technicals.

Res: 1317, 1322, 1327, 1330

Sup: 1313, 1307, 1302, 1300

US Futures Higher After Second Plunge This Week

- Indices Remain Vulnerable After Entering Correction;

- US Congress Passes Funding Bill Ending Brief Government Shutdown;

- Sterling Dips After Worrying Manufacturing Data.

Indices Remain Vulnerable After Entering Correction

US futures are trading slightly in the green ahead of the open on Friday, a day after stock markets once again tumbled leaving indices in correction territory.

As we saw on Thursday, this isn't necessarily indicative of calm returning to the markets. The Dow recorded declines of more than 1,000 points for the second time this week, having never done so before, despite futures prior to the open being relatively unchanged on the previous days close.

Clearly there remains a lot of volatility and nervousness in the markets and I don't expect this to ease up heading into the weekend. Stock markets will likely remain vulnerable to further shocks heading into today's close and possible even next week. That said, with a 10% correction having now completed, I wonder whether investors will now start looking to buy the dips as the fundamental backdrop remains strong.

US Congress Passes Funding Bill Ending Brief Government Shutdown

On a more positive note, the House and the Senate approved a new funding bill in the early hours of Friday morning that will see the government through to 23 March and increase spending limits for two years, ending a showdown that came into effect overnight.

Markets haven't been too concerned about the prospect of a shutdown since the start of the year despite two having now taken place so I don't expect to see any boost now that a deal has been reached. This is merely just another self-inflicted risk that's been temporarily averted.

Sterling Dips After Worrying Manufacturing Data

It's a slightly quieter day in terms of notable economic events. The Canadian jobs data will be of interest given that the central bank has been relatively aggressively raising interest rates over the last six months. The UK GDP estimate from NIESR will also be of interest, given that the pound has continued to rise even as the economy experiences a notable slowdown.

The manufacturing and industrial production figures from the UK this morning showed another dip in December, with the latter in particular experiencing no year on year growth. Given that these are among the areas that have benefited since the referendum, it may be a minor concern. The pound dipped after the releases having failed to hold above 1.40 against the dollar in recent days.

Equities Lose $5 Trillion As Bulls Slay Bulls

Friday February 9: Five things the markets are talking about

Stateside, the House of Representatives has approved the bill to fund the U.S government and has raised spending limits over two-years, it is now sending the measure to President Trump.**

Investors should expect market turbulence to continue this year as pullbacks and volatility become more common in the wake of rising central bank interest rates and sovereign bond yields.

The growing consensus is that increasing market volatility should not be capable of derailing the underlying economic expansion or fundamentally dent risk assets, it does however make many things less predictable.

Ahead of the U.S open, European stocks have pared their decline and U.S stock futures have gained despite an Asian session seeing red, with China's bourses tumbling the most in 24-months.

Elsewhere, Treasury yields have backed up to trade atop of their four-year highs as the 'buck' edged lower. Crude oil is heading towards its worst week in 12-months on concerns of over growing U.S supply and gold prices have temporarily stopped the bleeding.

On Tap: Canadian employment numbers are out at 08:30 am EDT. Is the market about to see a deep revision to the last two-months of massive job gain headlines?

1. Stocks Sea of red

In Japan, the Nikkei share average tumbled again overnight, mirroring Wall Street's losses, with oil-related equities leading the broad declines as crude prices slumped. The Nikkei finished down -2.3%, bringing its weekly loss to -8.1%. The broader Topix was -1.9%, down -7.1% for the week.

Down-under, Aussie shares slumped to a near four-month low overnight hammered by renewed selling on worries of higher inflation and interest rates. The S&P/ASX 200 index fell -0.9%. The benchmark has declined -4.6% on the week, its biggest loss in over 24-months. In S. Korea, the Kospi index fell -1.8%.

In Hong Kong, stocks crumble and cap the biggest weekly fall since the global financial crisis. At close of trade, the Hang Seng index was down -3.1%, the Hang Seng China Enterprises index fell -3.87%. For the week, the Hang Seng tumbled -9.5%, the biggest weekly loss since October 2008, while the HSCE posted a weekly loss of -12.01%.

In China, stocks were crushed and suffered their worst day in almost two-years, with blue-chip led carnage dragging the markets into correction territory. The benchmark Shanghai Composite Index tumbled -4.0% and the blue-chip CSI300 ended the day down -4.3%.

In Europe, regional indices trade mostly lower, but are off their session lows after a rebound in U.S futures ahead of the open stateside. Increased outlook for higher rates from the Bank of England (BoE) is weighing on the FTSE.

Indices: Stoxx600 -0.5% at 372.1, FTSE -0.4% at 7144, DAX -0.3% at 12221, CAC-40 -0.4% at 5129, IBEX-35 -0.7% at 9689, FTSE MIB -0.3% at 22407, SMI +0.1% at 8768, S&P 500 Futures +0.7%

2. Oil slides towards steep weekly loss as supply fears mount, gold higher

Oil prices are on track for their biggest weekly loss in 10-months after hitting new lows overnight after data this week showed U.S crude output had reached record highs and the North Sea's largest crude pipeline reopened following an outage.

Brent futures are down -30c at +$64.51 a barrel. Yesterday, Brent fell -1.1% to its lowest close since Dec. 20. U.S West Texas Intermediate (WTI) crude is down -42c at +$60.73 a barrel, having settled down -1% Thursday, its lowest close since Jan. 2.

Note: Brent futures have lost around -9% from their four-year January high print of +$71. Futures positions suggest that investors are sitting on the largest 'bullish position in history.

Earlier this week, the U.S. Energy Information Administration (EIA) upped its 2018 average output forecast to +10.59m bpd, up +320k bpd from its last forecast 10-days ago.

Note: The output is now higher than the previous bpd record from 1970 and above that of top exporter Saudi Arabia.

Ahead of the U.S open, gold prices have edged a tad higher after hitting more than one-month lows yesterday, as the correction in equities drove investors towards safe-haven assets like gold. However, gold 'bulls' should expect a stronger U.S dollar and concerns over rising global interest rates to keep gains somewhat capped. Spot gold is up +0.1% at +$1,320.72 an ounce.

Note: On Thursday, gold prices touched their lowest since Jan. 4 at +$1,306.81 an ounce.

3. Equity pain brings relief to bonds

The Eurozone and U.S bond yields have edged a tad lower as renewed global stock selling has managed to lend some support to safe-haven debt markets.

Bond yields have been backing up aggressively all week as investors brace for an end to easy-monetary policies by G7 central banks.

Note: Yesterday's more hawkish than expected Bank of England (BoE) was the latest catalyst to cause fixed income to steepen sovereign yield curves.

The yield on U.S 10-year Treasuries has decreased less than -1 bps to +2.84%. In Germany, the 10-year Bund yield fell -1 bps to +0.76%, while in the U.K the 10-year Gilt yield declined -2 bps to +1.617%.

4. Dollar jives and dips

Market risk aversion sentiment remains to the fore, but the G10 forex pairs continue to stay locked within their recent ranges. The U.S dollar bull, and they are dwindling; maintain that it's the Fed who may be caught behind the curve on rates. Next week's U.S CPI may very well put the 'cat amongst the pigeons.'

Note: The greenback has caught a bid now that the House of Representatives has approved the bill to fund the U.S government.

Elsewhere, the EUR/USD (€1.2254) is little changed, the pound continues to benefit, albeit struggling after the U.S funding announcement, from the Bank of England saying on Thursday that it expected to “increase interest rates earlier and faster' than previously projected, seen by many to mean a likely May rate rise.

The Chinese currency is on track for its first weekly loss in nine-weeks as the yuan (¥6.3400) has weakened against the dollar in thin volume.

5. U.K industrial output falls on North Sea pipeline shutdown

Data this morning showed that U.K. manufacturing continued to grow in the final month of 2017, but overall industrial production fell by more than anticipated due to an emergency shutdown of a North Sea pipeline.

In monthly terms, U.K. factory output grew by +0.3%, in line with market expectations, the eighth consecutive month of growth.

However, overall industrial production, meanwhile, declined by -1.3%, +0.4% more than forecast.

Separately, the ONS said that the U.K.'s trade deficit widened in December, driven by increased oil imports and rising prices. The December goods trade deficit stood at -£13.6B – significantly wider than expected (-£11.8B e)

CAC Loses Ground As Global Sell-Off Continues

The CAC index has posted losses in the Friday session. Currently, the index is at 5124.00, down 0.54% on the day. On the release front, French Industrial Production came in at 0.5%, above the estimate of 0.1%.

It's been a tumultuous week for global stock markets, and the CAC has dropped 3.6% percent this week. February has been dismal for European markets, and the CAC has shed 6.9%. Earlier this week, the CAC dropped to its lowest level since early September. The CAC has lost ground on Friday, following losses in the North American and Asian stock markets. Ironically, the catalyst for the current sell-off has been solid economic data in the US; namely, improved payrolls and wage growth reports. This has raised concerns of inflation, which could lead to a quicker pace of rate hikes from the Federal Reserve. This sentiment has sent the bond markets higher, while weighing on global stock markets.

A rebound in the global economy has been a boon for eurozone exports, and this has boosted France's manufacturing setor. This was underscored by a solid French industrial production report, which gained 0.5% in December. We'll get a look at Eurozone Industrial Production next week. The November reading surged to 1.0%, marking a 3-month high.

After months of intense negotiations, President Angela Merkel appears to have put together a new coalition government. Earlier this week, Merkel's conservative party and the socialist SDP announced that they had finalized a coalition agreement. In the last government, the SDP was the junior partner of the conservatives, but this time around the SDP has extracted major concessions from Merkel, including the finance and foreign affairs ministries. This could present a unique opportunity for French President Macron, as the new German government will likely undergo a significant shift in its stance towards the eurozone. Under the previous government, there was a reluctance to provide large bailouts to weaker eurozone members, such as Cyprus and Greece. However, struggling members will likely find a sympathetic ear for financial help from the SDP. As well, Macron's vision of a more integrated Eurozone, complete with a budget and finance minister, may dovetail nicely with the SDP's stance towards the eurozone.