Sample Category Title

EURUSD Intraday Analysis

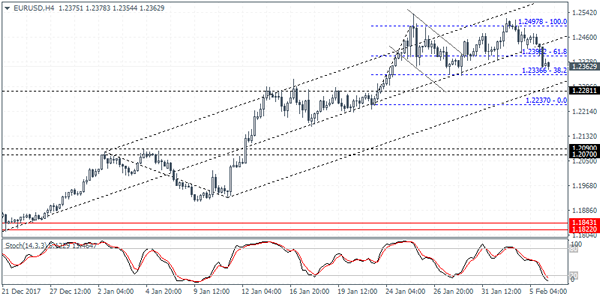

EURUSD (1.2362): The EURUSD has confirmed the failed bullish flag pattern with price action failing to breakout above the 1.2497 level. The declines yesterday pushed the euro to the previous support formed at 1.2398. A break down below this level is required for the EURUSD to confirm the downside. Initial support is seen at 1.2281 which could be tested in the near term. Following this, EURUSD could be extending the declines to the lower support level at 1.2090 - 1.2070 area of support which is pending a retest.

RBA Keeps Interest Rates Unchanged

The U.S. dollar was seen strengthening yesterday. Data from the U.S. showed that the ISM nonmanufacturing PMI rose to 59.9 beating estimates of 56.5. January's PMI data was also stronger than December's print of 55.9.

In the UK, the services PMI came out slightly better than expected. The services sector activity rose to 54.7 in January, beating forecasts of 53.6 and accelerating slightly from December's 53.9.

Earlier today, Australia's retail sales figures showed a 0.5% decline on the month. This was a bigger than expected decline of 0.2%. However, revisions to previous month's data showed an increase of 1.3%. The RBA's monetary policy meeting was also held earlier today. The central bank kept interest rates unchanged at 1.50%.

Looking ahead, New Zealand's unemployment data will be released later this evening. Estimates point to an increase in New Zealand's unemployment rate at 4.7% while the quarterly employment change is expected to rise at a slower pace of 0.4%

GBPUSD Bears Drive The Market, Downside Correction In Progress

GBPUSD fell as low as 1.3936, a level that is standing near the 20-day simple moving average during today’s Asian session. The pair tumbled aggressively in the last couple of days and the risk is still to the downside as price continues to move with weak movement. Also, the short-term technical indicators are bearish and point to more downside correction in the market.

In the daily timeframe, the parabolic SAR indicator is signaling further losses as the price is trading below it. The RSI indicator completed a steep downside movement, however, currently is pointing slightly to the upside. The MACD oscillator is heading down and posted a bearish crossover with its trigger line in the positive territory.

Remaining in the same timeframe, the bearish phase remains in play especially if cable continues to trade below the 1.3980 resistance level. The next pause to have in mind is the 23.6% Fibonacci retracement level at 1.3817 of the upleg from 1.2100 to 1.4345. A slip below that level could open the door for the 1.3660 support barrier, which is near the 40-day SMA.

To the upside, if price surpasses 1.3980, it could move towards the 1.4280 barrier. A break above the aforementioned obstacle could take the price towards the 1.4345 strong resistance level, the highest level since June 2016.

Currencies: USD Little Affected By Global Risk-Off Correction

Sunrise Market Commentary

- Rates: Huge sell-off on US stock markets triggers short squeeze in bonds

The sell-off on US stock markets accelerated yesterday evening (-4% and more) and caused a huge short squeeze in an oversold US Treasury market with yields ending up to 15 bps lower. Risk aversion could support core bonds somewhat short term and cause a revisit of previous range tops in yield terms. Any downleg in yields is expected to stop there. - Currencies: USD little affected by global risk-off correction

The focus for global trading remains on equities and bonds/yields. FX markets are little affected by the aggressive risk-off correction. EUR/USD stays within the established range. The euro is holding strong. USD/JPY loses slightly ground, but yen gains are still blocked by ongoing verbal monetary interventions from BOJ officials

The Sunrise Headlines

- US stocks suffered their worst fall in more than six years (-4% to -4.5%), erasing gains for the year. Asian equity indices can't escape the sell-off this morning and record losses of 3% to 5% (Japan).

- Industrial workers and employers in southwestern Germany struck a deal on pay and working hours, setting a benchmark for others. The agreement foresees a 4.3% raise from April and other payments spread over 27 months.

- ECB Draghi warned that the euro's recent surge creates 'new headwinds' and should be closely watched. The comments are the latest sign that a stronger euro could slow ECB efforts to unwind its giant monetary stimulus program.

- The Australian central bank kept its policy rate unchanged at 1.5%. RBA governor Lowe reiterated that a return of rapid wage growth remains a distant prospect despite strengthening business investment and a hiring bonanza.

- The House intelligence committee voted to release a memo that rebuts Republican criticisms of the FBI probe into Russian interference in the 2016 election, setting the stage for a potential clash with President Trump.

- German coalition negotiations were extended for a second day as SPD leaders seek to wring concessions on labor and health-insurance rules from Merkel's Christian Democratic-led bloc. A yes-or-no decision is expected today.

- Today's eco calendar contains the US trade balance. Austria, Germany, Greece (?), Finland (?) and the US tap the market. ECB Weidmann and Fed Bullard are scheduled to speak

Currencies: USD Little Affected By Global Risk-Off Correction

USD little affected by global risk-off correction

Equity sentiment turned negative in Europe yesterday, but the decline developed orderly. Bonds rebounded off last week's lows. The dollar continued trading mixed, gaining slightly ground against the euro, but struggling against the yen. Even so, the rise of the yen was hampered by soft comments from Japanese officials. This trading pattern basically persisted in US dealings as equities nosedived and as yields declined sharply. EUR/USD finished the session at 1.2367. The yen finally attracted some safe haven flows. USD/JPY closed at 109.09 (from 110.17 on Friday). Still, the rise of the yen was modest given global panic.

In extremely volatile trading, Asian equities are losing up to 5% (losses were even bigger earlier in the session). US yields decline further, but the pace slows. EUR/USD (currently near 1.2375) still holds a tight range. Yen gains remain modest. USD/JPY dropped to the mid-108 area, but already rebounded slightly. The swings on other markets (e.g commodities) are also modest. The Reserve bank of Australia kept its policy unchanged. Economic growth remains on track, but the RBA maintains a wait-and- see approach. AUD/USD (0.7850 area) lost further ground, but this is probably due to the risk-off sentiment.

Today's eco calendar is thin. The US trade deficit is expected at a huge $52.1 bn. Trade imbalances might become more important for FX trading but today's data will be overshadowed by the equity story. Current volatility is in the first place an equity correction. The impact on FX is modest. Dollar bulls/euro bears might be disappointed that risk-off didn't help the dollar more against. At the same time, investors are cautious to row against verbal monetary interventions from the BOJ, preventing further JPY gains. Over the previous days, we were looking for a technical sign in EUR/USD. This sign isn't there yet despite big swings on other markets. It suggests that the downside in EUR/USD remains quite solid for now. Technical picture: the dollar decline slowed of late, but no meaningful rebound occurred. EUR/USD 1.2537/98 remains the first topside resistance. A break would signal more trouble for USD short term. EUR/USD 1.2323/35 is a minor support A break below 1.2165 would call off the ST downside alert (for USD).

The sterling correction accelerated yesterday. Brexit noise, global risk-aversion and a disappointing services PMI were to blame. EUR/GBP rebounded to the 0.8870 area. Sterling's decline against the euro might slow ahead of the BOE meeting. EUR/GBP 0.8928 is first resistance.

EUR/USD: holding a tight range despite rise in global volatility

Volatility Continues As Risk-Off Reigns

The shock in stock markets continues, as yesterday was the worst since August 2011. US stock markets were some of the worst hit, with the US 30 (DOW) falling -4.60% or 1175.2 points. WTI Crude Oil futures fell 2.70% or $1.82, while Gold has a modest rise given the volatility, up $5.88 or 0.44% to $1339.00. Bitcoin was down again, at $7175, dropping $890, with a close below its 200-Day moving average. The USD strengthened along with the JPY, which outperformed all comers. Safety was sought in US Debt with yield moving lower, 10-year by 2.709%, -13.1 basis points. The high yield reached 2.8831%.

Spanish Markit Services PMI (Jan) was 56.9 v an expected 55.4, from a prior reading of 54.6.

German Markit PMI Composite (Jan) was 59.0 v an expected 58.8, from a previous reading of 58.8. Markit Services PMI (Jan) was 57.3 v an expected 57.0, from a previous reading of 57.0.

Eurozone Markit PMI Composite (Jan) was 58.8 v an expected 58.6, from a previous reading of 58.6. Markit Services PMI (Jan) was 58.0 v an expected 57.6, from a previous reading of 57.6. EURUSD fell to 1.24559 before recovering to 1.24746, while the Germany 30 Index fell to 12708.00 and then recovered to 12755.20 due to this data release.

UK Markit Services PMI (Jan) was 53.0 v an expected 54.3, from a prior reading of 54.2. GBPUSD closed at a daily high of 1.41501 just before the release of this data and started its decline when the data was released to reach a low of 1.39867 some hours later.

US Markit Services PMI (Jan) was as expected, unchanged at 53.3. Markit PMI Composite (Jan) was 53.8 v an expected 53.9, from a previous reading of 53.8. US ISM Non-Manufacturing PMI (Jan) was 59.9, beating the expected 56.5, from 56.0 previously, which had been revised up from 55.9. USDJPY continued its climb higher to 110.259 before selling off.

Australian Retail Sales s.a. (MoM) (Dec) was -0.5% v an expected -0.2%, from a prior 1.2%, which was revised up to 1.3%. Trade Balance (Dec) was -1358M, a large miss compared to the expected 200M, from a previous -628M, which was revised up to 36M. Imports (Dec) were 6% from 1% previously. Exports (Dec) were 2% from 0% previously. AUDUSD dropped from 0.78898 to 0.78692 following the data release.

Royal Bank of Australia Interest Rate Decision was left unchanged at 1.5%. The Rate statement was released at the same time. RBA said that AUD remains within the range it has been in over the past two years on a trade-weighted basis. Rising AUD would result in a slower economy and inflation. AUDUSD was moved down from 0.78740 to 0.78351 by this release.

EURUSD is up 0.10% overnight, trading around 1.23790.

USDJPY is down -0.14% in the early session trading at around 108.898.

GBPUSD is up 0.11% to trade around 1.39722.

USDCAD is unchanged overnight, trading around 1.25390.

AUDUSD is down -0.33% overnight at around 0.782881.

Gold is up 0.28% in early morning trading at around $1,342.99.

WTI is down -0.09% this morning, trading around $63.24.

Major data releases for today:

At 09:00 GMT, German Bundesbank President Weidmann will speak in Frankfurt. He will deliver opening remarks at a Buba lecture.

At 13:30 GMT, US Trade Balance (Dec) is expected to be $-52.0B from a previous $-50.5B.

At 13.30 GMT, Canadian International Merchandise Trade (Dec) is expected to be $-2.20B from a prior reading of $-2.54B.

At 13:50 GMT, US Fed’s Bullard will be speaking. USD crosses could experience volatility around this time in reaction to his comments.

At 15:00 GMT, Canadian Ivey Purchasing Managers Index (Jan) was 49.3 previously. Ivey Purchasing Managers Index s.a. (Jan) is expected at 61.0 from a previous 60.4. CAD pairs may be moved by this release.

At 21:45 GMT, New Zealand Unemployment Rate (Q4) is expected to be unchanged at 4.6%. Employment Change (Q4) is expected to be 0.2% from a prior 2.2%. Participation Rate (Q4) is expected to be 70.8% from a prior 71.1%. NZD can see a spike in volatility after this data is released.

At 22:30 GMT, Australian AiG Performance of Construction Index (Jan) will be released, with a prior value of 52.8. AUD can move to test key levels with this data acting as a catalyst.

The Higher VIX Leads To A Big Fall In Short VIX Products

Market movers today

The key focus in markets will continue to be the recent market rout and how far it can go.

German factory orders should confirm the picture of robust manufacturing growth. The data is very volatile though, so one should looked at the smoothed trend rather than one month's data.

US trade balance may come into focus as we get the December number and thus have the total for all of 2017. It may reveal that the trade deficit with China has reached a new high, triggering further ammunition for Trump to take protectionist measures against China.

In the afternoon, the Fed's Bullard (non-voter, dovish) will speak on the US economy and monetary policy. Bullard has proven one of the most dovish members of the Fed and cautioned against too aggressive rate hikes. He will vote on policy next year.

In Scandi, we get releases for Swedish industrial orders as well as Danish house prices.

Selected market news

Yesterday, we experienced a major risk off day in the financial markets. S&P500 fell 4.1% (the biggest decline since August 2011) erasing the gains in January thus ending the ‘honeymoon phase' in the stock markets where we have not seen a big market correction since Brexit. In Asia, it was also red across the board this morning. S&P500 futures have recovered slightly but are still down around 1%. US 10-year Treasury yields have continued to fall overnight and are now trading at 2.68% versus 2.88% at their peak yesterday. The equity volatility index VIX more than doubled from around 17 to 37, higher than during the US election, Brexit and the Chinese slowdown in early 2016 – we have to go back to the flash crash on 24 August 2015 to find a higher VIX. The higher VIX leads to a big fall in short VIX products. Brent oil is now trading slightly below 67 dollars per barrel (versus slightly above 70 at its peak).

The question is whether the big risk sell-off reflects an economic slowdown. We do not think so. Economic optimism is high and both European PMIs and the US non-manufacturing ISM are at very high levels, suggesting economic growth is still strong. However, an increasing concern is whether the time of low inflation is over, not least after the stronger-than-expected wage growth numbers from the US on Friday. It is not unnatural for markets to take a break after a long period of big increases (and especially the equity markets have had a very strong start to 2018), as investors take home some profits. Long equities have been a crowded trade for some time with markets looking stretched and overbought. Despite the big falls, the S&P500 is still marginal above its 100-day moving average and still close to 30% higher than before Trump won the election. While the correction may not be over yet, we think it is short-lived.

Yesterday, Jerome Powell was sworn in as Fed chair. In the short term, he is going to stick to the current monetary policy by raising the Fed funds target range three times this year (the first one in March) but look out for the increasing discussions about shifting to a price level target instead of the current inflation target, see Flash Comment US: Powell is “Yellen in disguise” amid discussions about price-level targeting, 24 January.

Global Markets Crashing After Dow Jones Fell 1175 Points

Markets are panicking, and investors are finding few places to hide after the Dow Jones Industrial Average plunged more than 1,500 intraday before closing 1,175 points lower at 4.6% on Monday. The hysterical sell-off showed no signs of letting up in Asia with the Nikkei and Topix indices falling more than 6% with the Nifty, ASX and STI straights all declining more than 3%.

With U.S. equities wiping out all gains for January and turning lower for the year, new Fed Chief, Jay Powell will be under a leadership test. The key trigger for the sell-off was the fear of rising inflation, and thus the Fed will need to tighten monetary policy at a faster pace.

Although economic data releases from the U.S. are continuing to impress following last week’s jobs report, with the U.S. ISM non-manufacturing index hitting 59.9 in January, this didn’t help to calm the markets.In fact, it had an opposite impact, suggesting that monetary policy needs to tighten faster to avoid the economy from overheating.

Bond yields, which have been a key source of pressure on stocks over the week declined significantly as investors found few places to go for. U.S. 10-year yields declined more than 20 basis points from yesterday’s highs, and if more outflows occur from stocks, I expect to see yields declining further.

We have been anticipating a correction for a long time now, but when markets become over-confident, corrections also become steeper. It’s hard to tell how far markets may decline, but given that economic fundamentals remain strong, I think investors will start buying the dips sooner than later.

Cryptocurrencies are also being dumped with Bitcoin falling towards $6,000 early Monday. The most famous digital currency has fallen 69% from December’s record high, and almost 56% from the start of the year. The slide comes after many banks in the U.S. and U.K. considered banning customers from buying cryptocurrencies using their credit cards. It seems the war against the crypto-world is far from over, and how the situation involves from here remains unknown, but risks are certainly high.

Currency markets have been relatively quiet when compared to the action in equities and bonds, but expect the Yen to strengthen further, if stocks continue to plunge throughout the U.S. trading session.

Daily Wave Analysis: US Dollar Shows Mixed Signals Of Weakness And Strength

Currency pair EUR/USD

The EUR/USD is building a larger WXY (blue) correction within a wave 4 (purple) unless price breaks below the 50% of wave 4 vs 3. The Fibs and the previous top (green) could provide potential support. A break above the resistance (red) could indicate an uptrend continuation within wave 5 (purple).

The EUR/USD could be building a bearish ABC (green) correction within wave 4 (purple). A bullish bounce at support (green/Fibs) and bullish break above resistance (red) could start a continuation of the uptrend.

Currency pair GBP/USD

The GBP/USD broke below the support trend line (dotted blue) and has retraced towards the 38.2% Fibonacci level. The Fib levels could provide support if price is indeed building a wave 4 (green) correction. A break below the 50% Fib makes a wave 4 less likely.

The GBP/USD is probably building a bearish ABC (grey) zigzag correction.A break above resistance (red) could indicate the start of wave 5 (green).

Currency pair USD/JPY

The USD/JPYmade a strong bearish fall, which could indicate a downtrend. However, price did not manage to break the support zone (green) as yet so the wave pattern is still favouring a wave 1-2 (purple) for the moment.

The USD/JPYmade a bullish continuation but price failed to break above the larger resistance level (orange) and then fell below support. The bearish momentum could be part of a zigzag within wave 2 (purple), which may not break below the 100% Fib otherwise it is invalidated.

Market Update – Asian Session: Equities Tracking US Declines

Headlines/Economic Data

General Trend: Various Asian indices decline over 5%

S&P500 Futures decline over 3% in Asia

Financial and Energy stocks underperform

(CN) China coal names under pressure after report China was considering a price cap

US equities remain volatile in Asian trading: Japan Exchange said circuit breaker was triggered on Dow Jones futures; Circuit breaker Also triggered on Tokyo Stock Exchange Mother futures

Asian gov't bond yields move lower amid gains in Treasury prices and equity declines

Japan 40-year JGB yield hits lowest level since April 2017

BoJ Gov Kuroda declines comment on daily stock price movements

Japan

Nikkei 225 opened -1.8%; closed -4.7%

TOPIX Information and Communications Index declines over 4% amid losses of over 5% in shares of Softbank

Financials decline:TOPIX Securities Index declines over 5%; Mitsubishi UFJ, Mizuho Financial and Sumitomo Mitsui Financial decline over 3%.

Toyota [7203.JP]: Declines over 3% ahead of expected earnings report

(JP) Japan Econ Min Motegi:Want to closely watch financial market moves and impact on the economy

(JP) Japan Fin Min Aso: Coincheck is not a bank,so needs real time inspection; no comment on market moves

(JP) Japan MoF sells ¥400B v ¥400B indicated in 10-yr 0.1% inflation-indexed bonds; lowest yield -0.464%; bid to cover 3.38x

(JP) Japan Securities Clearing Corp (JSCC) said to issue intraday margin call related to Topix and Nikkei 225 Futures - US financial press

(JP) Bank of Japan (BOJ) Gov Kuroda: No comment on daily moves of stock prices; Japan equities are being impacted by moves in the US - Parliament

Korea

Kospi opened -2.2%

Financials decline by over 3%:Hana Financial down over 5%

Weakness in the chip sector: Samsung declines over 2%, while Hynix drops by more than 1.5%

Samsung Electronics [005930.KR]: China NDRC saidto sign MOU with the company regarding chip cooperation - China Daily [**Note:Samsung and the NDRC were said to have signed the MOU related to cooperation inthe DRAM market, said a Korean press report from Feb 2nd. The report said theMOU may include Samsung agreeing to moderate DRAM price increases in order tohelp contain costs for smartphone makers in China]

(KR) South Korea Ministry of Trade, Industry and Energy: to foster midsized firms to add 130,000 jobs by 2022 - Korean press

(KR) Bank of Korea (BoK) Gov Lee to monitor impact of US equity markets ondomestic market - South Korean Press

(KR) South Korea Finance Ministry: To scrap/delay earlier plans to imposetougher capital gains tax on foreigners

(KR) South Korea sells 30-yr pre-issuance govt bonds at 2.69%

(KR) ~8% of virtual bank accounts for cryptocurrency trading in South Koreahave been converted to real-name bank accounts, 1-week after the govt ended theability to have anonymous accounts - Korean press

(KR) South Korea International Trade Association: South Korea faces far moreimport restrictions from the United States than any other country - Korean press

(KR) South Korea sells KRW1.1T in 30-yr govt bonds, avg yield 2.67%

China/Hong Kong

Hang Seng opened -3.8%, Shanghai Composite -2.0%

Hang Seng Energy Index -4.8%, Information Tech -4.5%, Property/Construction -4.3%, Consumer Goods -4.1%, Materials -4%, Financials -4%

(CN) Shanghai Exchange to increase oversight of dividend payments,to promote the listed company cash dividends - Chinese Press

(CN) Local provinces in China said to conduct checks on implicit government debts - China Securities Times

(CN) China PBoC: Skips OMO (9th straightsession) v skipped prior; Net drain CNY80B v CNY40B prior

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3072 v6.3019 PRIOR

(CN) China Premier Li: China will remain committed to the policy of reform andopening up and provide more convenience for foreign experts to work in China –Xinhua

Australia/New Zealand

ASX 200 opened -1.6%; closed %

ASX 200 Energy Index -3.8%, Financials -3.2%, Consumer Discretionary -3.6%, Telecom -2.9%, Resources-2.7%

(AU) RBA LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED

(UK) PM May seeking developmentof trade relations with Australia post Brexit

(AU) AUSTRALIA DEC TRADE BALANCE (A$) -1.36B V +200ME

(AU) AUSTRALIA DEC RETAIL SALES M/M: -0.5% V -0.2%E

(AU) AUSTRALIA Q4 RETAIL SALES EX-INFLATION Q/Q: 0.9% V 1.0%E

LifeHealthcare, LHC.AU To be acquired by PacificEquity Partners at A$3.75/shr cash; to declare fully franked special dividendof A$0.18/share; Also reports H1 results; +41%

(AU) Australia Treasurer Morrison: I drew upon his "own experience and understanding" in dismissing Treasury's expert advice on negative gearing

New Zealand closed for holiday

Looking Ahead: New Zealand Q4 Employment Change, Labor Cost Index and Unemployment Rate due to be released on Wed

Other Asia

(MY) Malaysia PM Razak: To waive stamp duty on some stocks for 3-yrs; to allow all investors do intraday shortselling

(TW) Taiwan Govt backedbanks said to have bought stocks on Monday including TSMC and Hon Hai (closed-1.6% after falling more than 2% in the session)

SIA Engineering [SIE.SG] To form JV with GE Aviation toform an engine overhaul joint venture based in Singapore

(SG) Singapore Deputy PM: No strong case to bancryptocurrency, closely studying cryptocurrency

North America

US equity markets ended lower: Dow -4.6%, S&P500 -4.1%, Nasdaq -3.8%, Russell 2000-3.6%

S&P500 Financials -5%, Industrial -4.5%

Micron [MU]: Gained over 2% in the afterhours: Raises Q2 $2.70-2.75 v $2.57e, Rev $7.20-7.35B v $7.02Be (prior $2.51-2.65, Rev$6.80-7.20B)

(US) White House: Pres Trump's focus is on long-term economic fundamentals, which remain exceptionally strong

(US) Fed's Kashkari (dove, non-voter): Friday's job report last week showed hint wages could be rising; Dollar could create inflationary pressures - TV interview

(US) Jerome Powell formally sworn in as the new Fed Chair

(US) Congressional source: Debt ceiling is unlikely to be added as a rider to the stopgap spending bill; The House is meeting tonight to discuss a stopgap spending bill that will keep the govt funded into March – press

(US) US House expected to vote on Tuesday on short-term measure to fund government through March 23rd and avert shutdown - financial press

Looking Ahead: US weekly API Crude OilInventories due to be released

Europe

(EU) ECB's Draghi: euro area economy is expanding robustly with stronger growth rates than previously anticipated and significantly above potential; We cannot yet declare victory on inflation front; Also, new headwinds have arisen from the recent volatility in the exchange rate, whose implications for the medium-term outlook for price stability require close monitoring.- comments to EU Parliament

(UK) Brexit Sec Davis: our teams will work intensively to agree on Brexit implementation period by March

(UK) Prime Min May: the UK and EU have discussed agreement on future trade as soon as possible, working towards Oct timetable

(UK) JAN BRC SALES LFL Y/Y:0.6% V 0.7%E

(DE) Germany coalition govt talks extended for a second time; talks said to be continuing with an eye to conclude negotiations on Tues - Germany press

(DE) Germany Labor Union IG Metall: Agreed to labor deal which provides for a 4.3% pay increase for workers that stretches over a 27 month period

(UK) Telegraph published leaked EU rules that it could be forced to accept during Brexit, speculating it could trigger new disagreements in Cabinet who have said they will not accept such rules

Levels as of 01:00ET

Nikkei225 -4.7%, Hang Seng -4.1%; Shanghai Composite -2.7%; ASX200 -3.2%, Kospi -1.5%

Equity Futures: S&P500 -0.5%; Nasdaq100 +0.1%,Dax -1.3%; FTSE100 -1.0%

EUR 1.2388-1.2351; JPY 109.30-108.45; AUD 0.7892-0.7835;NZD 0.7302-0.7257

Apr Gold +0.7% at $1,345/oz; Mar Crude Oil -1.0%at $63.52/brl; Mar Copper -0.2% at $3.18/lb

RBA Maintained The Key Interest Rate Unchanged At 1.50%

For the 24 hours to 23:00 GMT, the AUD declined 0.5% against the USD and closed at 0.7883.

LME Copper prices declined 0.2% or $16.0/MT to $7050.0/MT. Aluminium prices declined 1.2% or $26.0/MT to $2202.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7862, with the AUD trading 0.27% lower against the USD from yesterday's close, after data showed that Australia unexpectedly posted a huge deficit in December.

Earlier today, the Reserve Bank of Australia (RBA), at its February monetary policy meeting, opted to keep the official cash rate at record low of 1.50%, citing continuing concerns about weak household consumption. In its post-meeting statement, the central bank indicated that while business conditions and investment were improving in the economy, household consumption remained a source of uncertainty.

On the economic front, Australia surprisingly posted a seasonally adjusted trade deficit of A$1358.0 million in December, amid a surge in imports and confounding market expectations for a surplus of A$200.0 million. The nation had registered a revised surplus of A$36.0 million in the prior month. Moreover, the nation's seasonally adjusted retail sales retreated 0.5% on a monthly basis in December, exceeding market expectations for a fall of 0.2%. Retail sales had advanced 1.2% in the previous month.

The pair is expected to find support at 0.7825, and a fall through could take it to the next support level of 0.7787. The pair is expected to find its first resistance at 0.7927, and a rise through could take it to the next resistance level of 0.7991.

Going ahead, traders would eye the release of Australia's AiG performance of construction index for January, slated to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.