Sample Category Title

Daily Wave Analysis: EUR/USD Completes Wave 2 And Prepares For Bullish Wave 3

Currency pair EUR/USD

The EUR/USD challenged the short-term resistance trend line (red) but failed to break and made a new retest of the support trend line (blue). Price bounced at the support trend line, which could be part of a wave 2 (blue) pullback. A bullish breakout could start a bullish wave 3 (blue).

The EUR/USD seems to have completed a wave 2 (blue) correction and a bullish break above the resistance trend lines (red) could trigger a bullish breakout and momentum.

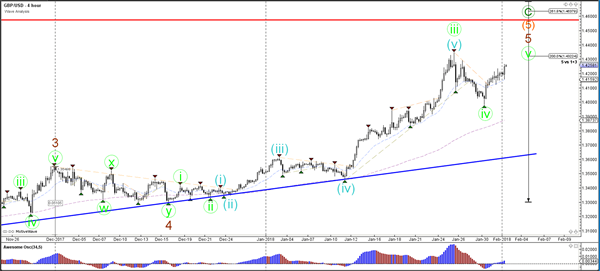

Currency pair GBP/USD

The GBP/USD uptrend is continuing higher and will soon retest the Fibonacci targets of waves 5.

The GBP/USD broke above the resistance trend line (dotted orange) which could be starting a bullish wave 3 (blue) momentum.

Currency pair USD/JPY

The USD/JPYis testing the larger resistance trend line (red) of the downtrend channel after price broke above the triangle pattern (dotted orange).

The USD/JPY is in a potential wave 3 (purple) if price manages to break above the resistance trend line (red).

Market Update – European Session: PMI Manufacturing Data Mixed But Continues To Show Europe On Path To Recovery

Notes/Observations

European Jan Manufacturing PMI data mixed in session but overall continued to provide evidence of support the region’s recovery (Beats: France, Swiss, Norway, Czech; Misses: Germany, UK, Spain, Sweden, Poland; In-line: Euro-Zone, Russia )

Asia:

South Korea Jan CPI M/M: 0.4% v 0.7%e v 0.3% prior; Y/Y:1.0% v 1.3%e

China Jan Caixin Manufacturing PMI: 51.5 v 51.5 prior

(JP) Japan Jan Final Manufacturing PMI: 54.8 v 54.4 prelim (highest since Feb 2014)

Europe:

ECB’s Coeure (France): Currency war is always a losing proposition; reiterates view of expecting rates to really remain very low for extended period of time

European Banking Authority (EBA) released macroeconomic scenarios related to 2018 EU-wide stress test

EU said to be threatening sanctions to stop Britain undercutting the Europe’s economy after Brexit

Forza Italia party denies reports about Berlusconi's ill health

Italy’s 5-star leader said to have told investors he would be willing to govern with Forza Italia, PD in broad coalition (**Note: story later denied but would ask other parties to agree on policies, support his government

Americas:

FOMC held its Target Range steady between 1.25-1.50% (as expected) in an unanimous vote; Labor market had continued to strengthen; dropped language on expecting inflation to remain below 2% in near term

Canada Foreign Min Freeland: still cautiously optimistic about NAFTA talks; significant differences remain on NAFTA

Energy:

EIA report noted that US crude output rose above 10M bpd in Nov, a 47-year high

Economic Data:

(IN) India Jan Manufacturing PMI: 52.4 v 54.7 prior (6th month of expansion)

(PE) Peru Jan CPI M/M:0.1% v 0.2%e; Y/Y: 1.3% v 1.3%e

(IE) Ireland Jan Manufacturing PMI: 57.6 v 59.1 prior (moved off from record highs)

(RU) Russia Jan Manufacturing PMI: 52.1 v 52.1e (18th month of expansion)

(CH) Swiss Jan SECO Consumer Confidence: 5 v 2e (7-year high)

(UK) Jan Nationwide House Price Index M/M: 0.6% v 0.1%e; Y/Y: 3.2% v 2.5%e

(TR) Turkey Jan Manufacturing PMI: 55.5e

(TH) Thailand Jan CPI M/M: 0.1% v 0.1%e; Y/Y: 0.7% v 0.8%e; CPI Core Y/Y: 0.6% v 0.7%e

(SE) Sweden Jan Manufacturing PMI: 57.0 v 61.0e

(NL) Netherlands Jan Manufacturing PMI: 62.5 v 62.2 prior (53rd month of expansion and a record high)

(NO) Norway Jan Manufacturing PMI: 59.0 v 56.6e

(PL) Poland Jan Manufacturing PMI: 54.6 v 55.3e (39th month of expansion)

(HU) Hungary Jan Manufacturing PMI: 60.9 v 60.5 prior (26th month of expansion)

(ES) Spain Jan Manufacturing PMI: 55.2 v 55.6e (51st month of expansion)

(CH) Swiss Dec Real Retail Sales Y/Y: 0.6% v 0.3% prior

(CZ) Czech Jan Manufacturing PMI: 59.8 v 59.0e (18th month of expansion)

(CH) Swiss Jan Manufacturing PMI: 65.3 v 64.2e (25th month without a contraction)

(HK) Hong Kong Dec Retail Sales Value Y/Y: 5.8% v 6.7%e; Retail Sales Volume Y/Y: 4.3% v 6.0%e

(IT) Italy Jan Manufacturing PMI: 59.0 v 57.4e (17th month of expansion)

(FR) France Jan Final Manufacturing PMI: 58.4 v 58.1e (Confirmed 16th month of expansion)

(DE) Germany Jan Final Manufacturing PMI: 61.1 v 61.2e (Confirmed 38th month of expansion)

(EU) Euro Zone Jan Final Manufacturing PMI: 59.6 v 59.6e (confirmed 54th month of growth)

(GR) Greece Jan Manufacturing PMI: 55.2 v 53.1 prior (8th month of expansion and highest since Oct 2007)

(ZA) South Africa Jan Manufacturing PMI: 49.9 v 47.4e (7th month of contraction)

(IS) Iceland Q4 Unemployment Rate: 2.6% v 2.2% prior

(UK) Jan Manufacturing PMI: 55.3 v 56.5e (18th month of expansion but lowest since Jun)

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €3.295B vs. €3.0-4.0B indicated range in 2021, 2025 and 2041 Bonds

Sold €1.19B in 0.05% Jan 2021 bond; Avg yield: -0.021% v -0.005% prior, Bid-to-cover: 2.57x v 2.28x prior

Sold€1.21B in 2.15% Oct 2025 bond; Avg Yield: 1.039% v 1.461% prior; Bid-to-cover: 2.08x v 2.62x prior

Sold €895M in 4.70% July 2041 bonds; Avg Yield: 2.262% v 2.427% prior; Bid-to-cover: 1.65x v 1.61x prior

(ES) Spain Debt Agency (Tesoro) sold €775M vs. €0.5-1.0B indicated range in 0.65% Nov I/L 2027 bonds; Real Yield:0.000% v 0.241% prior; Bid-to-cover: 2.69x v 2.54x prior

(FR) France Debt Agency (AFT)sold total €8.874B vs. €8.0-9.0B indicated range in 2028, 2034 and 2066 Oats

Sold €3.621B in 0.75% 2028 Oat; Avg Yield: 0.98% v 0.79% prior; Bid-to-cover: 2.02x v 1.44x prior

Sold €3.31B in new 1.25% 2034 Oat; Avg Yield: 1.33%; Bid-to-cover: 1.34x prior (no history)

Sold €1.943B in 1.75% 2066 Oat; Avg Yield: 1.91% v 2.14% prior, Bid-to-cover: 1.24x v 1.99x prior

(SE) Sweden sold SEK500M in 0.125% I/L 2026 bond; Avg Yield: -1.1921% v -1.2792% prior; Bid-to-cover: 2.06x v 2.33x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.4% at 397.1, FTSE +0.1% at 7540, DAX +0.4% at 13237, CAC-40 +0.5% at 5507 , IBEX-35 +0.5% at 10507, FTSE MIB +0.9% at 23717 , SMI +0.4% at 9376, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade higher across the continent rebounding from weakness over the past few sessions tracking higher US futures and a stronger Nikkei 225 overnight. Earnings continued to be the dominant theme, with Daimler, Vodafone and Roche reporting underwhelming results, while Dassault Systems reported strong growth, with shares advancing more than 7%. Nokia advances after reporting a beat on the top and bottom line, and provided 2018 and 2020 outlooks. Novo Nordisk, Skanska, Unilever were among other notable names that reported. Looking ahead notable earners include AliBaba, Ralph Lauren, Cigna and Mastercard.

Movers

Consumer Discretionary [Unilever [UNA.NL] -0.6% (Earnings), Kesko [KESKOB.FI] +3% (Earnings)]

Industrials [Daimler [DAI.DE] -1.3% (Earnings), Dassault Systems [DSY.FR] +7.2% (Earnings)]

Telecom [Vodafone [VOD.UK] -1.6% (Q3 update), Nokia [NOKIA.FI] +6.7% (Earnings), TDC [TDC.DK] -10% (Earnings, acquisition)]

Healthcare [Novo Nordisk [NOVOB.DK] -5.2% (Earnings)]

Speakers

PM May: To push forward a global strategic relationship with China

EU's Dombrovskis: EU Commission was preparing for cliff-edge scenario for Brexit among other views. Saw Brexit transition being linked to the budget and noted that it would not be the Norway model for the UK

India Fin Min Jaitley Budget speech saw 2nd half FY2017/18 GDP growth between 7.2-7.5% (Oct-Mar period).He noted that the country was firmly on course to achieve growth of 8% plus this year. Forecasted FY19/20 GDP growth at 7.2% with fiscal deficit of 3.3%. The govt set FY19/20 Gross Market Borrowing at INR6.06T; Net borrowings at INR4.62T

Taiwan Central Bank Dec Minutes: Members concerned over US-Taiwan interest rate spread. 1 member believed that rate hike would add to TWD currency gains

Currencies

USD saw its gains from the Fed’s hawkish hold ebbed away during the European session. Dealers noted that the current course of Fed rate hike path is baked in. The greenback could find some room if the Minutes of yesterday’s Fed meeting reflected growing concern about them being behind the curve

EUR/USD back above the 1.24 level as European Jan Manufacturing PMI data continued to provide evidence of support the region’s recovery. The pair also aided by views from some analysts that Eurozone inflation data might have bottomed.

GBP higher by 0.5% at 1.4245. Some analysts noted some optimisim on Brexit talks. UBS analyst brought forward its forecast of next BOE rate hike to May but noted the forecast was conditional on a Brexit transitional agreement in March

USD/JPY above the 109.50 level with dealers attributing the USD rally in response to a hawkish-hold FOMC statement. The pair seemed to be locked in a 107-110 range for the time being

Fixed Income

Bund Futures trades down 40 ticks at 158.29 as the downward trend resumes. Continued upside targets 159.85, while a move lower targets the157.75 level.

Gilt futures trade at 121.57 down 37 ticks, as the 10-year yield hits the highest level since 2016. Support continues to stand at 121.25 then 120.75, with upside resistance at 122.75 then 123.25.

Thursday’s liquidity report showed Wednesday’s excess liquidity rose to €1.892T from €1.869T prior. Use of the marginal lending facility rose to €75M from €56M prior.

Corporate issuance saw 6 issuers raise $4.9B in the primary market.

Looking Ahead

(EU) ECB’s Praet (Belgium, chief economist)

(IT) Italy Jan Budget Balance: No est v €14.9B prior

(RO) Romania Jan International Reserves: No est v $37.1B prior

(RU) Russia Jan Sovereign Wealth Funds: Reserve Fund: No est v $0.0B prior; Wellbeing Fund: No est v $65.2B prior

06:00 (IE) Ireland Jan Live Registry Monthly Change: No est v -2.9K prior; Live Registry Level: No est v 241.3K prior

06:00 (BR) Brazil Dec Industrial Production M/M: 1.9%e v 0.2% prior; Y/Y: 3.3%e v 4.7% prior

06:00 (ZA) South Africa Dec Electricity Production Y/Y: No est v 1.7% prior; Electricity Consumption Y/Y: No est v 0.9% prior

06:45 (US) Daily Libor Fixing

07:00 (CZ) Czech Central Bank (CNB) Interest Rate Decision: Expected to raise Repurchase Rate by 25bps to 0.75%

07:00 (CA) Canada Dec MLI Leading Indicator M/M: No est v 0.5% prior

07:00 (BR) Brazil Dec CNI Capacity Utilization: No est v 78.3% prior

(US) Jan Wards Domestic Vehicle Sales; Total Vehicle Sales

07:30 (US) Jan Challenger Job Cuts: No est v 32.4K prior; Y/Y: No est v -3.6% prior

08:00 (BR) Brazil Jan Manufacturing PMI: No est v 52.4 prior

08:00 (CZ) Czech Jan Budget Balance (CZK): No est v -6.2B prior

08:00 (RU) Russia Gold and Forex Reserve w/e Jan 26th: No est v $442.8B prior

08:00 (ZA) South Africa Jan Naamsa Vehicle Sales Y/Y: No est v -2.4% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 235Ke v 233K prior; Continuing Claims: 1.93Me v 1.937M prior

08:30 (US) Q4 Preliminary Nonfarm Productivity: 0.7%e v 3.0% prior; Unit Labor Costs: +0.9%e v -0.2% prior

09:30 (CA) Canada Jan Manufacturing PMI: No est v 54.7 prior

09:45 (US) Jan Final Markit Manufacturing PMI: 55.5e v 55.5 prelim

10:00 (US) Dec Construction Spending M/M: 0.4%e v 0.8% prior

10:00 (US) Jan ISM Manufacturing: 58.6e v 59.3 prior (revise from 59.7); Prices Paid: 68.8e v 69.0 prior

10:00 (MX) Mexico Dec Total Remittances: $2.5Be v $2.3B prior

10:30 (MX) Mexico Jan Manufacturing PMI: No est v 51.7 prior

10:30 (US) Weekly EIA Natural Gas Inventories

12:00 (IT) Italy Jan New Car Registrations Y/Y: No est v -3.2% prior

12:00 (BR) Brazil Jan Trade Balance: $2.9Be v $5.0B prior

12:30 (UK) BOE’s Breazier in London

13:00 (MX) Mexico Jan IMEF Manufacturing Index: 52.0e v 51.7 prior; Non-Manufacturing Index: 51.9e v 52.0 prior

13:30 (AR) Argentina Jan Government Tax Revenues (ARS: 262.4B v 235.2B prior

16:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to leave Overnight Rate Target unchanged at 2.50%

16:00 (NZ) New Zealand Jan ANZ Consumer Confidence: No est v 121.8 prior

Technical Outlook: AUDUSD – Extended Pullback Cracks Key 0.80 Support, Threatening For Deeper Correction

The Australian dollar holds in red for the fourth straight day and extends pullback from new high at 0.8135 (26 Jan). Today's bearish acceleration broke below 10SMA (0.8044) and cracked next pivot at 0.80 zone (0.8010 - Fibo 38.2% of 0.7807/0.8135 upleg/0.80 – psychological support). Fresh weakness is generating bearish signal and showing strong threats for broader uptrend as close below 0.80 would signal deeper correction and larger bulls on hold for some time. Further easing would face support at 0.7975 (rising 20SMA) and could extend towards next key support at 0.7892 (Fibo 38.2% of entire 0.7500/0.8135, 11 Dec/26 Jan rally). Stronger dollar on hawkish Fed and south-heading indicators on daily chart support the notion. Conversely, return and close above 10SMA is needed to sideline rising bearish threats.

Res: 0.8044, 0.8067, 0.8100, 0.8135

Sup: 0.8000, 0.7975, 0.7936, 0.7892

Technical Outlook: USDJPY – Extended Recovery Seen On Firm Break Above Falling 10SMA

The pair rallies on Thursday as dollar was inflated by hawkish stance from Fed, signaling stronger recovery from 2018 low at 108.28.

Fresh strength broke above three-day consolidation top and cracked important barriers at 109.50/57 (Fibo 38.2% of 111.48/108.28 bear-leg / falling 10SMA, generating bullish signal.

Close above here is needed to confirm and open barriers at 109.88 (Fibo 50%) and 110.25 (Fibo 61.8% of 111.48/108.28 downleg).

Daily RSI is heading north after reversing from oversold territory and showing space for further advance, with momentum building and underpinning the rally.

Alternatively, failure to clear 109.50/57 pivots and close below, would signal that bulls are losing traction and would keep the downside vulnerable.

Overall picture remains bearish and current rally is seen as correction and positioning for fresh downside.

Res: 109.88, 110.25, 110.58, 110.72

Sup: 109.50, 109.03, 108.50, 108.28

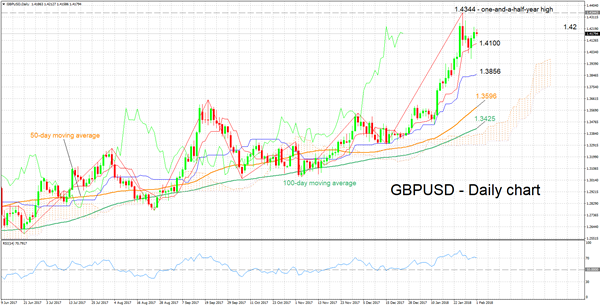

Technical Outlook: GBPUSD – Recovery Acceleration Eyes Key Barrier At 1.4344

Cable holds firm bullish tone on Thursday and extends strong recovery rally of past two days from 30 Jan spike low at 1.3979.

Today's rally broke above 1.4258 (Fibo 76.4% of 1.4344/1.3979 pullback) opening way towards psychological 1.4300 barrier and key barrier at 1.4344 (post Brexit vote recovery high).

Eventual break here would open way for extension of recovery phase from 1.1930 (07 Oct 2016 post-Brexit fall low) towards projected levels at 1.4431 (Fibo 123.6%) and 1.4484 (Fibo 138.2% projection).

Rising 10 SMA / daily Tenkan-sen continue track the advance, offering solid supports at 1.4102/00 which guards key near-term support at 1.40 zone.

Near-term action is also underpinned by thick 4-hr cloud (spanned between 1.4157 and 1.4043).

Sterling showed impressive rally in January, rallying 5.2% for the month, in its biggest monthly rally since May 2009.

Res: 1.4286, 1.4344, 1.4400, 1.4431

Sup: 1.4232, 1.4200, 1.4157, 1.4135

GBPUSD Buyers In Control Above 1.4200

The British pound has recovered upside momentum against the U.S dollar, following the Federal Reserve's decision to leave the U.S interest rate unchanged. The GBPUSD pair is now testing back towards the 1.4200 handle in early Thursday trading, after dropping to 1.4122 on Wednesday, after EU officials rejected the City of London's Brexit blueprint. Manufacturing data is now the focus of financial markets, as traders await the release of the UK Manufacturing PMI for January and the U.S ISM Manufacturing report.

The GBPUSD pair is likely to encounter further gains while trading above the 1.4200 level, key upside resistance is found at 1.4234 and 1.4284.

Should the GBPUSD pair struggle to gain traction above the 1.4200 handle, a decline back towards 1.4154 and 1.4122 seems likely.

EURUSD Dirextion Defined By Range Break

The euro continues to trade in range-bound conditions against the U.S dollar, following the FOMC policy decision, with price-action currently searching for a directional bias between the 1.2385 and 1.2432 levels. The EURUSD pair is still well supported above the 1.2400 level in early Thursday trading, despite a better than expected U.S ADP Job Report and the Federal Reserve striking a positive tone in yesterday’s policy statement release. Moving into the European session, EURUSD traders await a clear range-break and a raft of January Manufacturing PMI data being released from across the eurozone.

The EURUSD pair remains strong bullish above the 1.2432 level, further upside towards 1.2470 and 1.2538 would then seem possible.

Should the EURUSD pair fall below the 1.2385 level, sellers will likely try to test towards the 1.2355 and 1.2280 support levels.

BITCOIN Falls As Problems With Bitfinex Continue

Bitcoin's price is down a quarter of a percent after Bloomberg broke the news about Bitfinex.

According to the report, the Commodities and Futures Trading Commission (CFTC) had subpoenaed the people behind Bitfinex. Bitfinex is one of the largest cryptocurrencies exchange in the world.

According to the CFTC, the people behind Bitfinex created a token called tether, which was pegged to the dollar. Each token represented one dollar. However, on close inspection, the company did not have the dollars it claimed to have.

On Wednesday, after Bloomberg published the report, the New York Times followed it up with an article that suggested Bitfinex was propping up the price of bitcoin. According to the report, the company artificially increased and decreased the price of bitcoin instead of letting the market set the price. If this is true, there are limited chances that the company will exist for long.

The implications of a Bitfinex failure would be severe to the cryptocurrency industry because of its size. Some have compared it to the Goldman Sachs of cryptocurrencies.

The concerns about Bitfinex will continue to cloud many cryptocurrencies and bitcoin in particular. Traders will wonder whether other exchanges could be compromised as well thus lead to a sell off. As shown below, in the past couple of days, the price of bitcoin has been in consolidation mode with the price not moving as much as it did before. It has also struggled to recover from last month's highs.

Spotlight On US Data Continues

Attention will remain on US economic data in the latter half of the week, with Thursday’s reports focused on jobs and manufacturing.

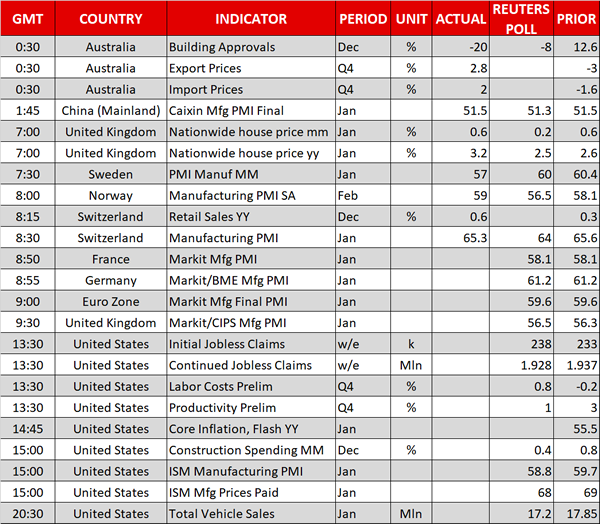

Investors can expect a somewhat active European session on Thursday, with IHS Markit reporting on manufacturing PMI for the UK, Germany, France, Italy, Greece and the broader euro area. The Eurozone manufacturing PMI is forecast to hold steady at 59.6 on a scale of 1-100 where 50 separates expansion from contraction.

The start of US trading will feature the weekly initial jobless claims report courtesy of the Department of Labor. The number of Americans filing for first-time unemployment benefits is forecast to rise by 5,000 to a seasonally adjusted 238,000. On Wednesday, payrolls processor ADP said US private sector employers added 234,000 workers last month, a figure that was well above forecasts.

Later in the morning, IHS Markit and the Institute for Supply Management (ISM) will each report on US manufacturing PMI. The ISM report, which is more closely followed by the financial market, is forecast to show a half point drop to 58.8.

Finally, the Department of Commerce will report on construction spending at 15:00 GMT. The December report is forecast to show expansion of 0.4%.

Earlier in the day, Caixin China reported a slightly better than expected reading of manufacturing PMI for the world’s second largest economy. The manufacturing purchasing managers’ index came in at 51.5 in January, unchanged from the previous month.

The report indicated: “The manufacturing industry had a good start to 2018. Going forward, we should keep a close eye on the stability of the demand side.”

EUR/USD

Europe’s common currency has been rangebound all week long, as the prolonged dollar slide finally found a short-term bottom. The EUR/USD exchange rate was last seen trading at 1.2419 for a gain of 0.1%. The pair peaked at 1.2475 on Wednesday before reversing back down to the low 1.2400 range. EUR/USD faces immediate resistance at 1.2470, followed by 1.2500. On the downside, immediate support is located at 1.2390, followed by 1.2355.

GBP/USD

Pound sterling is holding steady against the dollar, with cable trading around 1.4200. The pair was kept in check by an assertive US Federal Reserve, which indicated on Wednesday that interest rates may soon rise in response to faster inflation. The GBP/USD exchange rate faces near term support at 1.4120, the intraday low, with resistance up ahead at 1.4232.

USD/CAD

The USD/CAD continues to hold steady above 1.2300 following a series of protracted drops in previous weeks. The pair remains highly sensitive to economic data and monetary policy, with the Canadian dollar gaining more competitive advantage thanks to a robust domestic economy. The US nonfarm payrolls report on Friday could be the pair’s next major trading catalyst.

Optimistic Fed Message Does Little For The Dollar, Major Economies’ Manufacturing PMI Data Due

Here are the latest developments in global markets:

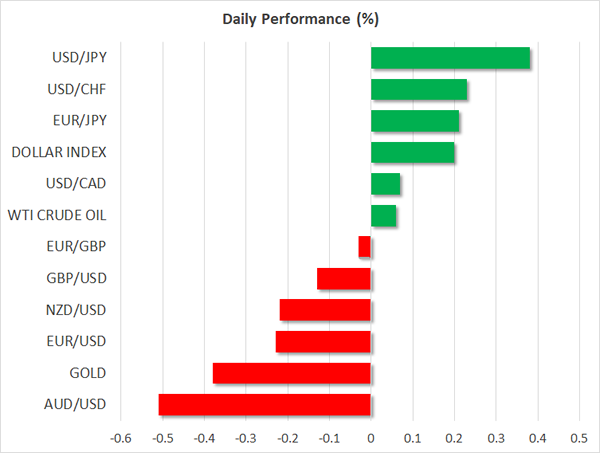

FOREX: The dollar index traded 0.2% higher on Thursday, recovering some of its recent losses, buoyed by the Fed's slightly more hawkish tone on the US economic outlook upon completion of its two-day meeting on monetary policy.

STOCKS: Japanese markets skyrocketed, with the Nikkei 225 moving 1.7% higher and the Topix surging by 1.8%, both indices regaining some of the ground they lost in recent days. In Hong Kong, the Hang Seng was down by 0.4%, while in Europe, futures tracking the Euro STOXX 50 are 0.6% higher. Turning to the US, the S&P 500, Dow Jones and Nasdaq Composite all finished higher yesterday, albeit not by much. The Dow gained the most out of the three, advancing by less than 0.3%. The relatively muted performance of these indices is being attributed to the surge in US Treasury yields, with the 10-year benchmark briefly topping 2.75% overnight, its highest level since April 2014.

COMMODITIES: Gold was nearly 0.4% lower, last trading near $1340 per ounce, as the modest rebound in the greenback weighed on the dollar-denominated precious metal. Oil prices were little changed, with both WTI and Brent crude rising by less than 0.1%. Interestingly enough, both oil benchmarks finished the day higher yesterday, even despite the weekly EIA inventory data showing a much higher build in stockpiles than what was anticipated

Major movers: FOMC upgrades inflation outlook, paves the way for March hike

The Fed kept its policy unchanged yesterday via a unanimous vote, as was widely anticipated. The statement accompanying the decision had a more optimistic tone compared to previously, upgrading the Committee's assessment of inflation. Inflation is now anticipated “to move up this year” and to stabilize around 2%, from previously being expected to remain somewhat below 2%. Policymakers also appeared upbeat on the broader economy, noting that gains in employment, household spending, and business investment have been solid.

The dollar spiked up on the news, but quickly gave back all of its winnings to trade virtually unchanged in the following hours, before assuming a direction during the Asian trading session Thursday and moving a little higher. The relatively indecisive price action in the USD, at least initially, may reflect the fact that many investors already anticipated a slightly more hawkish bias by the Committee, given the economy's solid performance. Markets have fully priced in a March rate increase, while another two quarter-point hikes by the end of the year are almost fully factored in, according to the Fed funds futures.

The greenback gained the most against the aussie, which suffered a little overnight after Australia's building approvals for December came in significantly lower than projected.

Day ahead: Major economies on the receiving end of PMI data; US jobless claims also on the horizon

The eurozone will see the final release of Markit's manufacturing PMI for the month of January at 0900 GMT. The reading is expected to be confirmed at 59.6, reflecting a decrease from December's 60.6, though still pointing to robust sectoral growth by comfortably exceeding the 50 mark that separates expansion from contraction. Germany and France, the eurozone's two largest economies, will see the release of their manufacturing PMI figures for the first month of the year a few minutes earlier (at 0855 GMT and 0850 GMT respectively).

The UK will also be on the receiving end of manufacturing PMI data. The January Markit/CIPS manufacturing PMI will be made public at 0930 GMT. The measure is anticipated to tick slightly higher relative to December, remaining well above 50. Unlike the eurozone that sees the release of a flash estimate as well, the UK only receives a single release; this may render sterling more “susceptible” to greater market movement upon release of the data and in case of a surprise.

Over in the US, of most interest are likely to be data on weekly initial and continued jobless claims due at 1330 GMT, as well as the ISM's January manufacturing PMI scheduled for release at 1500 GMT. First-time jobless claims applicants are expected to have increased during the week ending January 27, though not by much and to still remain well below the 300k threshold that's associated with a healthy labor market. The ISM's survey on manufacturing activity is projected to reflect a reduction compared to December, though at 58.8 – should expectations materialize – it would still constitute a robust number.

Other releases that might draw some attention out of the US are Q4 2017 preliminary data on labor costs and productivity (1330 GMT), Markit's final reading on January manufacturing PMI (1445 GMT), December construction spending figures (1500 GMT) and January's total vehicle sales (2030 GMT).

ECB executive board member and chief economist Peter Praet will be giving a speech at the luncheon conference of Cercle de Lorraine at 1115 GMT.

On the equities front, corporate giants Alibaba, Amazon, Apple and Google parent Alphabet will be among companies releasing quarterly earnings reports on Thursday.

Technical Analysis: GBPUSD bullish bias could be under threat as RSI halts advance

GBPUSD is trading roughly 150 pips below the one-and-a-half-year high of 1.4344 hit on January 25. The Tenkan-sen line remains above the Kijun-sen line and the RSI indicator is in bullish territory above 50. The aforementioned are supporting the view for a bullish short-term bias. Notice though that the RSI has halted its advance after rising well above the 70 overbought level last week. This could be an indication of changing dynamics in the short-term.

A stronger manufacturing PMI out of the UK during early European trading hours – or weaker releases out of the US later on Thursday – could see the pair gaining ground. The area around the 1.42 handle – a level of potential psychological significance – might be acting as immediate resistance at the moment. An upside breakup would turn the focus to the range around last week's one-and-a-half-year high of 1.4344 as an additional barrier to stronger bullish movement.

Weaker UK data, or equivalently more robust figures out of the US, on the other hand, might see the pair heading lower. In this case, the area around the current level of the Tenkan-sen at 1.41, which coincides with a point of potential psychological importance, might offer support