Sample Category Title

Dollar Collapses After Mnuchin Weak Currency Comments

USD Softer Ahead of ECB Monetary Policy Meeting

Trump Administration Endorses Dollar Weakness and gets tough on trade

The USD tumbled against all majors on Wednesday. The US Secretary of the Treasury issued comments in support of a weaker dollar. The combination of a lower currency and a tough stance on trade has sparked concerns that a global trade war could ignite. The US dollar has lacked traction in 2018 as domestic political uncertainty and economic recovery abroad continue to put downward pressure on the greenback. The highlight for the market on Thursday will be the press conference from European Central Bank (ECB) President Mario Draghi.

- The ECB minutes from December diverged form what Draghi said.

- The World Economic Forum in Davos continues in Switzerland

- US Commerce Secretary talked up hardline approach to trade

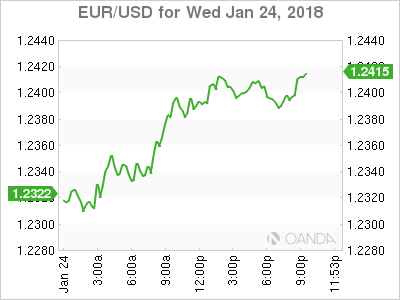

The EUR/USD gained 0.82 percent on Wednesday. The single currency is trading at 1.24 after some comments from US officials showed the current administration has diverged from the past in seeking a strong dollar policy and in fact could be ramping up for a trade war. US Secretary of the Treasury Steven Mnuchin said he welcomed the weakness in the US given the positive impact on trade. The words from the Secretary were shocking given his predecessors comments on a strong currency. Trade has been at the forefront after the US has imposed tariffs on certain products with President Donald Trump scheduled to talk at Davos on Friday. The US leader is anticipated to continue to paradox of highlighting stronger growth, which should value the currency higher, while at the same time seeking trade advantages in his America first strategy.

The European Central Bank (ECB) will publish its minimum bid rate on Thursday, January 25 at 7:45 am EST. There is no change expected with the attention of the market focused on the words of ECB President Mario Draghi who will host a press conference at 8:30 am EST.

The EUR touched a three year high versus the USD and given the minutes showed a more hawkish ECB, Draghi could go even deeper into neutral territory and talk down both the currency by highlighting the still low European inflation. Given that most of this EUR move was sparked by US dollar weakness Mr Draghi is facing an uphill battle.

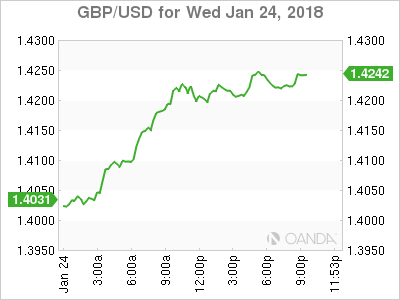

The GBP/USD gained 1.53 percent in the last 24 hours. The currency pair is trading at 1.4210 and reached levels not seen since the aftermath of the Brexit referendum. The higher chances of a softer exit and the weakness of the US dollar left the pound in current levels with the assumption that the ECB is close to announcing an end of QE this year with a small possibility of higher rates before the end of 2018. Mario Draghi has tried to shied away from saying that in so many words, with his actual statements remaining neutral despite evidence that there is a strong economic recovery underway, particularly by looking at Germany. That the engine of the European recovery is Germany will not be a surprise but this time it seems the there are multiple signs of optimism in the EU.

The GBP was the strongest performer on Thursday against the dollar, but similar to the EUR move it was based more on USD weakness than any particular British indicator. The political uncertainty which ended in a 1 day shutdown of the Federal Government was not the perfect start for for Washington taking into consideration the primaries in the fall.

Market events to watch this week:

Thursday, January 25

7:45am EUR Minimum Bid Rate

8:30 am CAD Core Retail Sales m/m

8:30 am EUR ECB Press Conference

Friday, January 26

4:30 am GBP Prelim GDP q/q

8:30 am CAD CPI m/m

8:30 am USD Advance GDP q/q

8:30 am USD Core Durable Goods Orders m/m

Gold Climbs Against Battered US Dollar, Hits 16-Week High

Gold has posted strong gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $13523.90, up 0.94% on the day. On the release front, Existing Home Sales disappointed, slowing to 5.57 million. This missed the forecast of 5.72 million. On Thursday, the US releases unemployment claims and New Home Sales.

The broad selloff of the US dollar continues, as major rivals such as the euro, pound and yen have posted strong gains on Wednesday. Gold has also jumped on the bandwagon, and has climbed 3.7% in the month of January. Gold has benefited from weaker appetite for risk, as global equity markets are lower. We could see more movement from gold later during the week, with the release on Friday of Advance GDP for the fourth quarter of 2016, as well as durable goods reports.

The US government shutdown lasted just three days, and only affected one working day. Still, the positive news didn’t boost the struggling US dollar. The funding agreement that Congress approved is little more than a band-aid solution, as it extends funding only until February 8. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration. If the bipartisan efforts to reform immigration implodes, the government will again find itself without funds come next month. With many members of Congress up for re-election in November, lawmakers will be trying to avoid angering voters with a second shutdown next month.

Pound Soars Despite Soft British Jobless Data

The British pound has posted strong gains in the Wednesday session. In North American trade, GBP/USD is trading at 1.4207, up 1.48% on the day. In economic news, the UK released key employment numbers. Wage growth remained unchanged at 2.5%, matching the forecast. Jobless claims climbed to 8.6 thousand, well above 2.3 thousand. There was no change to the unemployment rate, which held at 4.3%. This matched the estimate. In the US, Existing Home Sales disappointed, slowing to 5.57 million. This missed the forecast of 5.72 million. On Thursday, the US releases unemployment claims and New Home Sales.

The pound continues to impress, and is currently at its highest level since June 2016. GBP/USD has climbed 5.3% in January, as the US dollar has been battered by its major rivals. On Tuesday, the pair pushed above the symbolic 1.40 level, and with sentiment waning over the dollar, the pound rally could continue this week. The markets are keeping a close eye on Preliminary GDP for Q4, which will be released on Friday.

The US government shutdown turned out to be little more than a nuisance, with only one working day lost. On Monday, the Senate voted 266-150 to extend government funding until February 8. This stopgap measure will enable the government to provide services during that time, but the lawmakers will need to hammer out a longer-term agreement, as these short extensions are just band aid solutions. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

Dollar Dam Breaks

US dollar technical support levels crumbled Wednesday in a rout on the dollar that's been building for weeks. The pound was the top performer while the US dollar lagged. New Zealand CPI missed estimates early in Asia-Pacific trade. A new USD trade has been posted to subscribers. Below is the Premium video, highlighting the reasons behind the trade and positioning ahead of Thursday's ECB press conference.

It's gone from bad to worse for USD as the combination of talk from Mnuchin, worries about trade and better prospects elsewhere undermine the currency. The dollar lost more than a full cent against the euro, yen and pound Wednesday. Gold soared to its highest level since summer 2016.

USD/JPY fell to the lowest since September; EUR/USD rose to the best level in three years and the pound climbed 250 pips to the highest since the Brexit vote.

Along with that, commodities priced in US dollar soared with gold and oil hitting multi-year highs.

The trigger was a comment from Mnuchin. As Ashraf pointed out, it was something he had said before, but at the moment every USD-negative tidbit is amplified and the momentum is running away.

Quietly, US economic data has softened as well. Yesterday, the Richmond Fed manufacturing index slipped to 14 compared to 19 expected in January. Today FHFA house price data and existing home sales were both on the soft side.

The big question for central bankers this year will be inflation and Q4 data from New Zealand raised some questions. Prices rose just 1.6% y/y compared to 1.9% expected. The kiwi fell a full cent to 0.7335 on the headlines. Moves in commodity and FX prices will further cloud the global inflation picture.

One person who will desperately try to restrain his currency in the day ahead is Draghi but he faces a tough task. Any hint of less-dovish policy will send the euro skyward.

US GDP Could Give the Battered Dollar Some Reprieve

US economic growth is expected to have slowed a little in the final quarter of 2017, but to still remain in healthy territory. However, according to Fed models, there is the prospect for a slightly better reading than what is anticipated. With the implied probability for a Fed hike in March resting at 73%, a positive surprise in GDP could seal the deal for such an action, and perhaps help the dollar to regain some poise.

The first estimate of US GDP for the fourth quarter will be released on Friday at 1330 GMT, and expectations are for economic growth to have slowed to 3.0% on an annualized basis, from 3.2% in the previous quarter. Besides growth figures, this data set will also contain numbers on consumer prices for the quarter, though in this regard, investors may pay more attention to the core PCE price index for December that will be released on Monday.

What do gauges of the economy suggest? The Atlanta Fed GDPNow model currently anticipates Q4 growth at 3.4%, while the New York Fed's Nowcast model forecasts a print of 3.9%. Therefore, the risks surrounding the official forecast of 3.0% may be tilted to the upside, perhaps for a slightly stronger-than-anticipated GDP print.

Even though the Fed is widely expected to stand pat at its upcoming policy meeting next week, the same cannot be said for the March gathering. At the time of writing, the implied probability for a rate hike in March stands at 73% according to the Fed funds futures, and a positive surprise in the GDP data could push that percentage even higher. Strengthening expectations could help the dollar to claw back some of its recent losses, at least on the news. Dollar/yen could spike up and target the 109.80 barrier, where an upside break could set the stage for extensions towards the next resistance threshold at 110.20.

On the flipside, in case these data disappoint relative to expectations, the dollar could come under renewed selling interest. Dollar/yen could fall below its recent lows of 109.40, potentially targeting the 108.70 support area. If the bears prove strong enough to overcome that hurdle, the next level that could come into play is the round figure of 108.00.

Finally, it should be noted that the US will also publish durable goods orders for December at the same time as the GDP figures, implying that any market reaction in the dollar at the release may be influenced by those prints too, especially in case of a notable surprise.

Sunset Market Commentary

Markets:

US and European bonds came again under modest pressure today. Strong EMU PMI's suggest that the economic expansion continued at the start of 2018, weighing on European bonds. At the same time the 10-yr Note future also drifted back south after yesterday's rebound. There was no high profile US economic news. However, fear for a protectionist battle between the US and its trading partners might have been a negative for Treasuries. US Treasury Secretary Mnuchin applauding the decline of the dollar and Commerce Secretary Wilbur Ross indicating more action to protect American exporters raised the odds for a confrontation between the US and its main trading partners, including China. The jury is still out, but growing tensions between the US and China might question the PBOC's preparedness to hold the current huge portfolio of US Treasuries. US bond yields rise between 2.7 bps (2-y) and 4.4 bps. German yields increase between 0.1 bp (2-y) and 2.7 bps (10-y).

The USD decline accelerated today. Recent protectionist actions/rhetoric of the Trump administration are an additional negative for the US currency. In this respect, US Treasury Secretary Mnuchin further undermined confidence in the dollar as he indicated that the decline of the dollar was good for US trade. Mnuchin formally repeated the US mantra of a strong dollar in line with economic fundamentals over time. However, this sounds ever less credible. EUR/USD jumped to the 1.2350 area and remained under upward pressure later in the session. The EMU January PMI's were again very strong, but hardly impacted FX trading. Dollar weakness prevailed. Initially, intraday declines in the likes of EUR/GBP, EUR/AUD, EUR/JPY even suggested that the euro should not per se be the forerunner to profit from current USD decline (admittedly the moves were largely reversed later). Whatever, protectionist action from the US is becoming an ever bigger source of USD nervousness. Trump's speech in Davos on Friday might be at least as important for the fate of the dollar (and EUR/USD) than tomorrow's ECB meeting. EUR/USD trades in the 1.2375 area. USD/JPY is drifting lower in the 109 big figure (currently109.40).

Sterling was an outperformer against an overall weak dollar. Cable already filled offers in the high 1.42 area. The rise of sterling was supported by a good UK labour market report. Job growth in the 3 months to November was again strong, easing concerns after a poor figure last month. At the same time, sterling was supported by relatively soft comments from Brexit Minister Davis. He told UK lawmakers that the UK might initially stay closely aligned to the EU's regulatory framework. EUR/GBP is trading in the 0.8725 area. So the key 0.8690 support is coming within reach.

European equities show modest losses of the order of 0.25%/0.50% as the sharp decline of the dollar weighs on the region's exporters. US equities open again with modest gains of 0.2% to 0.4% . This time the Dow outperforms.

News Headlines:

"A weaker dollar is good for us as it is related to trade and opportunities," US Treasury Secretary Mnuchin told reporters at the World Economic Forum in Davos.

EMU businesses had a much better start to 2018 than expected, ramping up activity at the fastest rate since the middle of 2006, the composite PMI showed. The EMU index jumped to 58.6 this month from 58.1. The upturn was driven by a strong performance in the bloc's dominant service industry, where new business flooded in at a rate not seen in over a decade.

The British Office for National Statistics said the number of people in work rose by 102k in the 3 months to Nov. taking employment to a record 32.2 mn. The figures went some way to alleviating worries that Britain's labour market was running out of steam. Earnings, ex. bonuses, rose by 2.4% Y/Y, the biggest increase since Dec 2016.

USDCHF: Fresh Bearish Extension Eyes Key M/T Supports at 0.9438/20

The pair slumped on Wednesday as the greenback came under increased pressure. Fresh weakness after consolidation phase in previous few sessions extends into second day and probes below 0.9500 support, last traded in early Sep 2017.

Larger downtrend from 1.0037 (01 Nov high) is currently riding on the third wave and eyes its 161.8% Fibonacci expansion at 0.9472. The wave can travel further down for test of key med-term supports at 0.9438/20 (21 July/08 Sep double-bottom).

Break here will be strong bearish signal for extension of downtrend from 1.0343 which would also confirm weekly double-top at 1.0325 (Nov 2015) and 1.0343 (Dec 2016) peaks.

Meanwhile, bears could show stronger signs of hesitation on approach to key 0.9438/20 supports, but firm bearish setup favors limited upside before bears resume.

Falling 10 SMA (currently at 0.9621) should limit corrective upticks.

Res: 0.9554; 0.9621; 0.9666; 0.9704

Sup: 0.9482; 0.9438; 0.9420; 0.9362

COPPER: Strong Recovery Rally on Weaker Dollar Sidelines Downside Threats

Copper price bounced from five-week low at $3.1065 on Wednesday, inflated by sharp fall of US dollar that offsets negative impact from strong rise in copper inventories.

Fresh rally so far retraced the largest part of Tuesday's strong fall (the biggest one-day loss since 05 Dec), sidelining immediate downside threats, after corrective leg from $3.3200 high was contained by 100SMA at $3.1065.

Recovery rally dented Fibo 38.2% of entire $3.3200/$3.1065 downleg and could extend further as slow stochastic is heading north after emerging from oversold territory and shoeing a plenty of space upside.

Immediate barrier lies at $3.2028 (converged 10/30 SMA's), followed by $3.2293 (20SMA).

Break here and through $3.2384 (Fibo 61.8% of $3.3200/$3.1065) would generate strong bullish signal and neutralize near-term bears.

Res: 3.2028; 3.2132; 3.2293; 3.2384

Sup: 3.1881; 3.1569; 3.1416; 3.1065

Sterling Boosted by UK Jobs Report, Dollar Sobs

Investors who were itching for another opportunity to propel Sterling higher were given the green light on Wednesday after UK employment data came in stronger than market expectations.

The number of people in work unexpectedly jumped in the three months to November, while wage growth offered a pleasant surprise by rising 2.4% - the highest in almost a year. Although the number of jobless claims rose by 8.6k during the months of December, the unemployment rate held steady at 4.3%. While Sterling could continue benefiting from the positive labor report in the near term, it must be kept in mind that UK inflation still remains above wage growth. With wage growth still lagging behind inflation, it is likely to squeeze household incomes which would consequently put the standard of living under pressure. Sentiment over the UK economy could take another hit if consumers' spending power continues to deteriorate amid the high inflation and tepid wage growth environment.

Taking a look at the technical picture, the GBPUSD is unquestionably bullish on the daily charts, mostly due to a weakening US Dollar. A growing sense of optimism over a soft Brexit outcome has also played a role in the currency's incredibly appreciation, with prices trading around 1.4170 as of writing. The combination of Dollar weakness and Brexit related optimism has the ability to elevate the GBPUSD towards 1.4200 and 1.4230. Technical lagging indicators such as the MACD and 50 Moving Averages both go in line with the bullish sentiment on the daily charts. If bears want to jump back into the game, the GBPUSD needs to break below 1.3850 which is over 300 pips away from current prices.

Dollar under renewed selling pressure

The battered Dollar extended losses against a basket of major currencies on Wednesday, after US Treasury Secretary Mnuchin said a weaker Dollar is "good" for trade.

It has certainly been a rough trading week for the Dollar amid political uncertainty in Washington, with recent comments from Mnuchin fueling the downside. The Dollar is clearly in trouble, with further losses on the cards as the prospects of other major central banks gradually tightening monetary policy, erode buying sentiment further. From a technical standpoint, the Dollar Index is heavily bearish on the daily charts. The breakdown below 90.00 could invite a further decline towards 89.60 and 89.00, respectively.

Currency spotlight - EURUSD

The EURUSD sprinted to a fresh three year high above 1.2350 during Wednesday's trading session amid a softening US Dollar.

With the bullish sentiment towards the European economy stimulating investor appetite for the Euro, and Dollar weakness still a recurrent market theme, the EURUSD remains heavily supported. A hawkish ECB meeting on Thursday has the ability to push the EURUSD much higher. From a technical standpoint, the currency pair is firmly bullish on the daily charts. A solid breakout and daily close above 1.2320 could encourage a further incline towards 1.2400 and 1.2440, respectively.

Bitcoin hovers around $11,000

Bitcoin displayed weak and vulnerable characteristics this week as the cryptocurrency struggled to hold ground above $11,000.

There is anxiety in the air over South Korea banning anonymous cryptocurrency trading, while China's cryptocurrency crackdown has somewhat impacted appetite for Bitcoin. Taking a look at the technical standpoint, Bitcoin remains in a bearish trend on the daily charts. Sustained weakness below $11,000 could invite a decline towards $10,000. Alternatively, a break above $12,000 could trigger a further incline towards the $13,000 lower high.

EURUSD: Resumes Medium Term Uptrend, Faces More Upside Pressure

EURUSD: The pair has resumes its medium term uptrend leaving risk of more strength on the cards. On the upside, resistance comes in at 1.2400 level with a cut through here opening the door for more upside towards the 1.2450 level. Further up, resistance lies at the 1.2500 level where a break will expose the 1.2550 level. Its daily RSI is bullish and pointing higher suggesting more strength. Conversely, support lies at the 1.2300 level where a violation will aim at the 1.2250 level. A break of here will aim at the 1.2200 level. Below here will open the door for more weakness towards the 1.2150. All in all, EURUSD faces further upside move on bullish offensive.