Sample Category Title

EURGBP Hits 5-Week Low; Sharp Sell-off Continues

EURGBP edged sharply lower over the last hours and recorded a fresh 5-week low of 0.8710. When looking at the bigger picture the pair has been trading within a downward sloping channel since October 2017. The short-term technical indicators are bearish and point to more weakness in the market.

Looking at the 4-hour chart, prices are looking capped by the 20 and 40 simple moving averages which are negatively aligned after a bearish crossover that took place on January 18. Furthermore, the RSI indicator has entered the negative zone, whilst the MACD oscillator is ready to post a downward cross with its trigger line in the bearish territory.

Further losses could see the December 8 low of 0.8690 acting as a major support. A drop below the aforementioned obstacle would reinforce the bearish structure in the short-term and open the way towards the next key support level of 0.8635, which is near with the lower band of the downward sloping channel.

In the event of an upside reversal, the 0.8760 level could act as a strong barrier before being able to re-challenge the 0.8800 handle.

Sterling Shines above $1.41; New Zealand Reports on Inflation

Here are the latest developments in global markets:

FOREX: Better than expected employment readings and growing hopes of a softer Brexit pushed pound/dollar to 1.4151 (+1.04%) during early European trading hours and led euro/pound down to a 5-week low of 0.8746 (-0.75%). Euro/dollar edged up to fresh 3-year highs at 1.2355 (+0.28%) after Eurozone's Markit composite PMI surprisingly hit a new all-time high. On the other hand, dollar/yen extended losses towards a 4 ½-month low of 109.36 and the dollar index touched a 3-year trough at 89.70 following comments by the US Secretary Steven Mnuchin who said that a weaker dollar is attractive for trade purposes. Aussie/dollar and kiwi dollar were among the best performers, trading at 4-month highs, while Swedish krona/dollar gained ground after the Swedish central bank, the Riksbank, said that it might start raising interest rates before the ECB.

STOCKS: A drag in utilities and techs erased part of gains in energy stocks. However, European indices continued to trade at 2 ½-year highs amid optimism on the region's economic expansion and continuing earnings growth. The pan-European STOXX 600 lost speed, trading slightly up by 0.03% at 1045 GMT after the Bank of Merrill Lynch downgraded the French waste and water group Suez to underperform from neutral, while JP Morgan cut its ratingS for AMS – Apple's supplier – to neutral. The blue-chip Euro STOXX 50 was up by 0.23%, whereas the German DAX 30 and the UK FTSE 100 were steady. The Swiss SWI 20 jumped by 0.53%, underpinned by rising healthcare equities.

COMMODITIES: Oil prices were mixed. WTI crude climbed by 0.34% on the day to $64.66 per barrel and Brent was slightly down by 0.10% at $69.89. Gold surged by 0.64% on the back of a weaker dollar, last seen at $1,349.50 per ounce.

Day ahead: New Zealand release CPI figures; Trump heads to Davos

Later in the day, the economic calendar features the Markit flash manufacturing PMI, existing home sales and data on oil inventories out of the US, while New Zealand will report on Q4 consumer prices.

At 1445 GMT, the US manufacturing PMI for the month of January is expected to inch down from 55.1 in December to 55.0 according to IHS Markit, whilst existing home sales due at 1500 GMT are said to decline by 2.2% m/m in December for the first time after rising for three consecutive months. In November, the measure hit a 1 ½-year high at 5.6%.

A few minutes later(1530 GMT), the Energy information administration will release its weekly report on the US oil inventories, with forecasts suggesting crude oil and distillate stocks falling by a smaller amount in the week ending January 19. Gasoline inventories, though, are anticipated to continue rising at a slower pace.

New Zealand Q4 CPI figures will follow at 2145 GMT with the potential to shake the kiwi. Expectations are for inflation to slow down to 0.4% q/q compared to 0.5% in the previous quarter, while on a yearly basis the index is projected to remain flat at 1.9%, within the RBNZ's target of 1-3.0%.

In Davos, Switzerland, the global elite continues discussions on world topics at the annual World Economic Forum for the third day. Trump administration officials are also on the way to attend the event after the US Senators on Monday managed to end the government shutdown until February 8. Investors will be eager to hear any comments by the US President as he has shown opposition to many areas of discussions including trade issues in his first year of presidency. Moreover, his first legislative achievement involving massive tax cuts for businesses and individuals has attracted global interest as the US business environment might be more profitable for foreign companies.

US Data Eyed After Positive UK and Euro Releases

GBPUSD Above 1.40 After Encouraging UK Employment Data

It's been a relatively busy start to trading on Wednesday, with data from the UK and eurozone dominating so far and giving investors there cause for optimism.

The pound is flying against the dollar again, aided by some more encouraging labour market data out of the UK. Unemployment remained at 4.3% in the three months to November, with overall employment rising by more than 100,000 as the economy continues to shrug off Brexit-related headwinds even against the backdrop of lower growth. There was also encouraging news on earnings, with basic wage growth edging up to 2.4%, although this is still well below inflation meaning consumers continue to experience negative real growth.

UK Unemployment Rate

Once again this leaves the Bank of England in a difficult position because the labour market is clearly tightening and wages are improving which would typically warrant higher interest rates but this is being accompanied by decelerating growth and huge economic uncertainty, not the ideal environment in which to hike. The central bank may have raised rates last year but this was when inflation was at its peak and it's not expected to go higher. There may have also been a desire to remove the post-Brexit stimulus as the economy proved more resilient than expected. Policy makers may adopt a more cautious approach this year.

GBPUSD Weekly Chart

Eurozone PMIs Lift EURUSD to Three Year Highs

The euro is also making solid gains against a flagging dollar, with the pair now trading at more than three year highs, which has been aided by another batch of encouraging flash PMIs from the eurozone for January. The flash composite PMI rose to a 139-month high this month, with both the manufacturing and services sectors signalling strong optimism, providing further evidence that the region is going from strength to strength.

Eurozone Composite PMI

The region has benefited from the improved global economic environment and a weaker euro and the latter could be a challenge for it over the course of this year. The ECB is going to be very aware of this but will also be under pressure to remove further monetary support even as it brings an end to new bond purchases later this year. Traders are clearly already anticipating further tightening measures including at least one rate hike in 2019, which may be much earlier than many expected a year or two ago.

EURUSD Weekly Chart

USD Looking For a Lift From US PMIs and Housing Data

The gains we're seeing in the pound and euro isn't helping European stocks this morning, with the FTSE off around half a percent and the DAX down a few points. US equity markets are eyeing a positive start to trading on Wednesday, with more data on the agenda including manufacturing and services PMIs as well as existing home sales and crude inventories.

Canadian Dollar Improves as Greenback Struggles

USD/CAD has posted strong gains on Wednesday. Currently, the pair is trading at 1.2333, down 0.71% on the day. On the release front, there are no Canadian events. In the US, today's key event is Existing Home Sales, which is expected to dip to 5.72 million. On Thursday, Canada releases retail sales reports. The US will publish unemployment claims and New Home Sales.

Will NAFTA survive? The free trade agreement is critical for the Canadian economy, so threats by US President Trump to blow up the agreement are causing genuine concern for the Bank of Canada. Negotiations between Canada, Mexico and the US have not yielded much progress, and a sixth round of negotiations start on Tuesday. Trump has repeatedly said he is unhappy with the deal, and an advisory council to Canadian Foreign Minister Chrystia Freeland sounded pessimistic about a new trilateral deal being reached. Still, Trump is unpredictable, and there are also many US companies that benefit from the current deal and are opposed to the US pulling the plug. If NAFTA is terminated, it's likely the Canadian dollar will take a tumble.

The US government shutdown made the headlines for several days, but turned out to be little more than a nuisance, as the shutdown affected only one working day. On Monday, the Senate voted 266-150 to extend government funding until February 8. This stopgap measure will enable the government to provide services during that time, but the lawmakers will need to hammer out a longer-term agreement, as these short extensions are just band aid solutions. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

CAC Ticks Lower as French Manufacturing PMI Dips

The CAC index is showing little movement in the Wednesday session. Currently, the index is at 5528.80, down 0.12% on the day. On the release front, France and the eurozone released manufacturing and services PMIs. Eurozone PMIs were a mix, as Flash Manufacturing PMI dipped to 59.6, missing the estimate of 60.4 points. Flash Services PMI improved to 57.6, missing the forecast of 56.5 points. The trend was similar with French releases. Manufacturing PMI slowed to 58.1, missing the forecast of 58.7 points. There was better news from the Services PMI, as the reading of 59.3 beat the estimate of 58.9 points. On Thursday, the ECB is expected to maintain interest rates at 0.00%.

ECB policymakers meet on Thursday for the first policy meeting of 2018. We're unlikely to see any dramatics, as the ECB is likely to retain its pledge to continue buying bonds under its asset-purchase program (QE). The ECB has trimmed QE from EUR 60 billion to 3o billion/mth, but is likely to maintain interest rates for 3-6 months after that. Still, ECB policymakers have hinted that the Bank could wind up QE in September, and this has pushed the euro higher in recent weeks. ECB President Mario Draghi will speak after the statement, and if he hints that QE will not be extended, European stock markets could respond with gains. However, Draghi may prefer to keep a low profile until March, when policymakers will have had a chance to review updated economic forecasts.

With Britain on its way out of the European Union, France is hoping to pick up more spoils as foreign banks close shop in London and thousands of employees move to the continent. In November, Paris won the right to host the European Banking Authority, which is currently based in London. France is hoping to convince bankers to choose Paris, and is providing exemptions from state -pension payments and has opened additional spots at bilingual schools. There is plenty of competition for financial sector jobs which will leave the UK, with Frankfurt, Dublin and Amsterdam all in the bidding to pick up the slack caused by Brexit.

GBPUSD Gains Likely to Extend above 1.4000

The British pound has raced higher against the greenback in early Wednesday trading, climbing to 1.4118, following broad-based selling in U.S dollar index. Better than expected employment figures from the United Kingdom economy today, have helped to boost the GBPUSD pair to a new 19-month trading high. Price-action is currently hovering around the 1.4100 region, with the markets attention firmly focused on the falling value of U.S dollar, as it trades well below the key 90.00 level.

The GBPUSD pair is likely to extend gains while trading above the 1.4000 level, further upside towards 1.4160 and 1.4210 remains possible.

Should price-action on the GBPUSD pair start to move below the 1.4000 level, a correction towards the 1.3940 and 1.3880 levels may ensue.

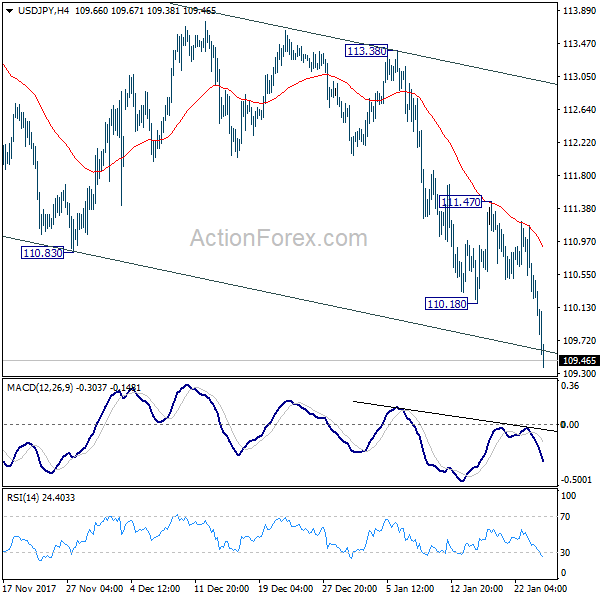

USDJPY Weakness to Accelerate Below 109.50

The U.S dollar has moved to lowest trading level against the Japanese yen since September 2017, hitting 109.40, following dollar negative comments from the U.S Treasury Secretary. Speaking at the World Economic Forum in Davos, Switzerland, U.S Treasury Secretary Steve Mnuchin said that a weaker U.S dollar is good for the American economy, immediately causing the USDJPY pair to break lower. Traders now look to Manufacturing data from the U.S economy, and the fastening depreciation in the value of the U.S dollar.

The USDJPY pair is likely to see further selling while trading below the 109.50 level, further losses towards 108.98 and 108.60 now appear likely.

Should the USDJPY pair start to trade back above the 109.50 level, a correction towards 109.80 and 110.18 remains possible.

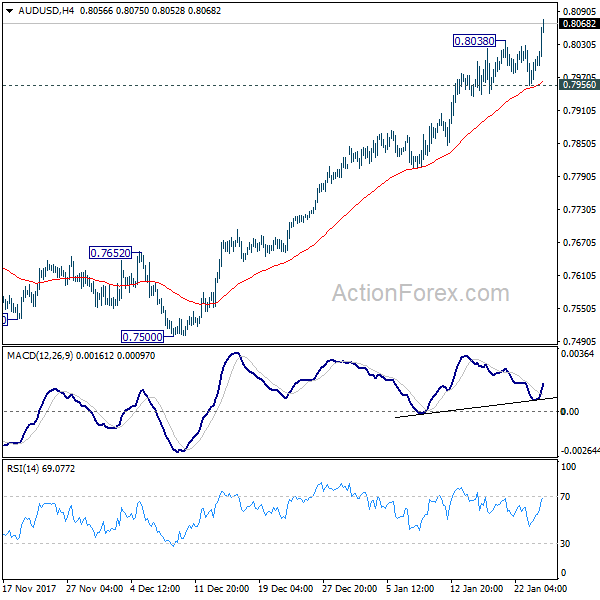

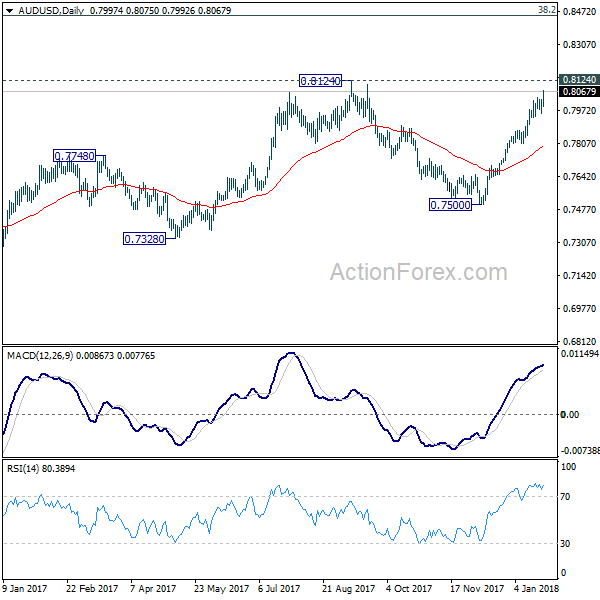

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7960; (P) 0.7995; (R1) 0.8033; More...

AUD/USD's break of 0.8038 indicates resumption of rise from 0.7500. Intraday bias is back on the upside for 0.8124 resistance. Break there will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451. On the downside, break of 0.7956 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside and bring reversal.

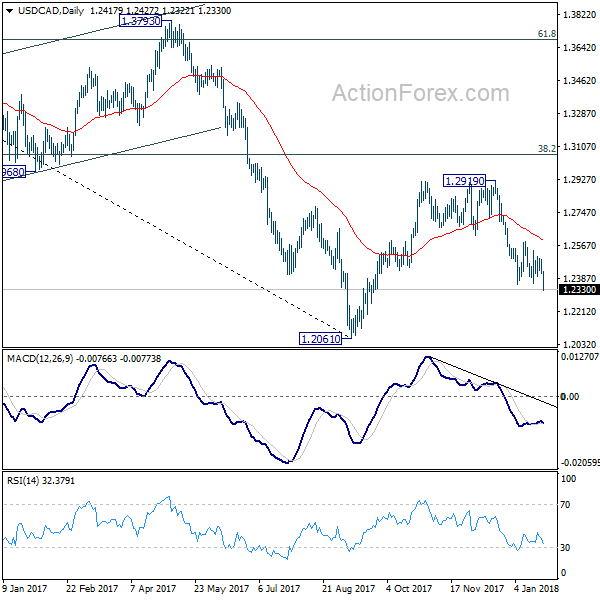

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2395; (P) 1.2442; (R1) 1.2467; More...

USD/CAD drops to as low as 1.2322 so far. Break of 1.2354 indicates resumption of fall from 1.2919. Intraday bias is back on the downside for retesting 1.2061 low. On the upside, break of 1.290 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, rebound from 1.2061 is likely completed completed at 1.2919, rejected by 55 week EMA (now at 1.2850) and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.96; (P) 110.57; (R1) 110.88; More...

USD/JPY's decline continues to as low as 109.38 so far. Break of lower channel support suggests downside acceleration. Intraday bias remains on the downside for 107.31 low. On the upside, break of 110.18 support turned resistance will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.