Sample Category Title

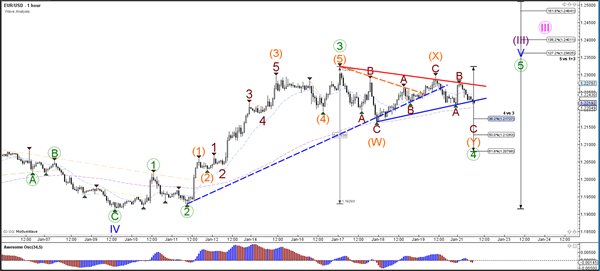

Daily Wave Analysis: EUR/USD, GBP/USD Build Triangle Chart Patterns In Uptrend

Currency pair EUR/USD

The EUR/USD is building a sideways retracement and the triangle chart pattern is probably just a correction within the uptrend. A bullish breakout above the resistance trend line (dotted red) could indicate the uptrend continuation towards the Fibonacci targets of wave 5 (blue).

The EUR/USD could expand the correction via a bearish ABC (brown) zigzag if price breaks below the support trend line (blue).

Currency pair GBP/USD

The GBP/USD is challenging the support line of the bullish channel. A break below the channel could see price test the Fibonacci support levels of wave 4 (green).

The GBP/USD is building a potential wave ABC (blue) correction which could take price towards the Fib levels. A bullish break above the round level of 1.40 could indicate a continuation of the uptrend.

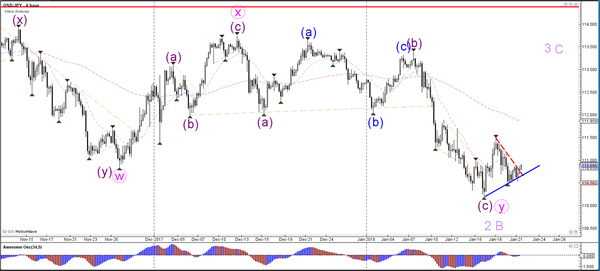

Currency pair USD/JPY

The USD/JPY failed to break the previous bottom and could be using it to bolster a new bullish rally.

The USD/JPY could be completing wave 2 (purple) and starting a wave 3 (purple) bullish momentum.

Forex Analysis: U.S. Government Shuts Down, German SPD Votes For Coalition Talks With Merkel

The U.S. government shutdown over the weekend as the Senate failed to pass a bill to keep the funds flowing late on Friday. The Democrats are making an issue of protections for young undocumented immigrants. President Trump has responded saying he will not negotiate on the issue until democrats vote to end the shutdown and reopen the government. How markets will react is still uncertain but risk has increased as a result of this political brinksmanship.

The German SPD party has voted to begin formal coalition talks with Chancellor Merkel’s Conservatives in an attempt to break the deadlock of the last few months and form a Government for the leading economy in Europe. Party delegates voted 362 to 279 in favour, with one abstention, for negotiations. The leaders had agreed on a blueprint for the coalition earlier this month but once a deal is struck from these negotiations the party will again have to vote to approve any subsequent Coalition before entering government. This vote was only the first step in the process that is expected to be difficult, as leading conservatives earlier rejected SPD demands for major concessions.

On Friday, German Producer Price Index (MoM) (Dec) was released and came in as expected at 0.2%, from 0.1% prior. The Producer Price Index (YoY) (Dec) was also as expected ta 2.3%, from 2.5% previously. EURUSD moved from 1.22447 to 1.22697 after the data release

The U.S. government shutdown over the weekend as the Senate failed to pass a bill to keep the funds flowing late on Friday. The Democrats are making an issue of protections for young undocumented immigrants. President Trump has responded saying he will not negotiate on the issue until democrats vote to end the shutdown and reopen the government. How markets will react is still uncertain but risk has increased as a result of this political brinksmanship.

The German SPD party has voted to begin formal coalition talks with Chancellor Merkel’s Conservatives in an attempt to break the deadlock of the last few months and form a Government for the leading economy in Europe. Party delegates voted 362 to 279 in favour, with one abstention, for negotiations. The leaders had agreed on a blueprint for the coalition earlier this month but once a deal is struck from these negotiations the party will again have to vote to approve any subsequent Coalition before entering government. This vote was only the first step in the process that is expected to be difficult, as leading conservatives earlier rejected SPD demands for major concessions.

On Friday, German Producer Price Index (MoM) (Dec) was released and came in as expected at 0.2%, from 0.1% prior. The Producer Price Index (YoY) (Dec) was also as expected ta 2.3%, from 2.5% previously. EURUSD moved from 1.22447 to 1.22697 after the data release

US Baker Hughes Rig Count was released at 747. The previously published number was 752. The Fed’s Quarles spoke at the Banking Law Committee Meeting in D.C. saying he intends to ease the burden of FED stress tests. He said that leverage ratio proposals are coming ‘relatively soon’ and that he wants to dial back the burden of living wills.

EURUSD is up 0.07% overnight, trading around 1.22230.

USDJPY is up 0.05% in early session trading at around 110.870.

GBPUSD is up 0.15% to trade around 1.38680.

USDCAD is down -0.11%, trading around 1.24819.

Gold is down -0.07% in early morning trading at around $1,330.10.

WTI is down -0.14% this morning, trading around $63.37.

Major data releases for today:

At 13:30 GMT, US Chicago Fed National Activity Index (Dec) will be released. The consensus is for 0.44 from 0.15 previously. USD crosses could be impacted by these data releases.

Major data releases for the week ahead:

On Tuesday at 04:00 GMT, Bank of Japan Interest Rate Decision and Policy Statement, Press conference to follow.

On Thursday at 12:45 GMT, Eurozone ECB Interest Rate Decision with Policy Statement and Press Conference to follow at 13:30 GMT.

At 13:30 GMT, Canadian Retail Sales (MoM) (Nov) and Retail Sales Ex-Autos (MoM) (Nov) will be released.

On Friday at 13:30 GMT, US Gross Domestic Product Annualized (Q4) will be released.

Investors Unmoved By The U.S. Government Shutdown

The U.S. government entered its third day of shutdown after U.S. Congress failed to arrive at a short-term budget deal. Although the story has been a major talking point among media, investors don’t seem too worried about the impact on their investments. Price action in most asset classes suggests that financial markets are growing increasingly immune to America’s political drama.

Although a shutdown will likely have a modest impact on growth due to lower spending, it largely depends on the duration to see a meaningful impact on GDP. According to Standard & Poor’s, the last time the government shutdown in 2013 for 16 days, the U.S. economy took a $24 billion hit. This suggests Q1 GDP may be dragged down 0.3% on average, for every week the government is shutdown.

Asian equities traded slightly lower on Monday, but given that the Japanese Yen and gold are flat at the time of writing, traders feel that the drama will be over soon. It remains to be seen whether the Democrats and Republicans will pass a short-term bill later today to keep the government running.

In Germany the government seems getting closer to forming a coalition after the Social Democrats voted in favor of entering formal coalition talks. The Euro gapped higher at the beginning of today’s session but gave up most of the gains few hours later. Given that only 56% of the SPD’s voted in favor of the talks, the rejection of a final coalition deal remains a risk that’s likely to keep the Euro capped for now.

The most interesting move seen in markets today was the U.S. 10-year treasury yields which broke above 2.67% for the first time since July 2014. This took U.S. – German 10-year yields to 208 basis points after it declined to 198 basis points on 16 January. I believe that the dollar should start benefiting from higher spreads especially if the European Central Bank manages to drag yields on European bonds when they meet on Thursday.

The Bank of Japan is also due to meet this week. Neither Banks are expected to change policy. BoJ will leave its policy rate unchanged at -0.1% and 10-year JGB at 0%, and the ECB will keep the benchmark, marginal lending and deposit rate unchanged at 0%, 0.25% and -0.4% respectively. Although the most recent minutes from the ECB suggested that policymakers are looking to tweak guidance in early 2018, I think the strong Euro performance will concern them. Thus, expect Mario Draghi to reiterate that interest rates won’t go higher until well beyond the end of the asset purchase program

Currencies: USD Withstands US Government Shutdown

Sunrise Market Commentary

- Rates: Cautiousness ahead of key events?

Today's trading might be paralyzed with key event risk looming. The US Senate has a vote scheduled after European trading to end the government shutdown. A positive outcome could push US yield through key resistance levels. Tomorrow morning's BoJ meeting and Thursday's ECB gathering are this week's other highlights. - Currencies: USD withstands US government shutdown

The dollar struggled to prevent further losses, but sentiment seems to be changing since the end last week and this morning. The greenback suffered no further damage from the political uncertainty due the US government shutdown. Will USD finally profit from rising interest rate support once the shutdown is 'solved'?

The Sunrise Headlines

- US stock markets ended 0.2% to 0.5% higher on Friday despite the looming vote to avoid a government shutdown. Asian stock markets trade with similar gains this morning with Japan and Korea underperforming.

- Germany took a big step towards forming a new government when the SPD voted in favour of formal coalition talks that could give Merkel a fourth term in office and break a four-month political deadlock.

- A US government shutdown will enter its third day as Senate negotiators failed to reach agreement to restore federal spending authority and deal with demands from Democrats that young "Dreamers" be protected from deportation. A new vote is set for today at 6pm CET.

- The Fed should continue to raise rates at a gradual pace during 2018 ('3 rate hikes is good starting point'), SF Fed President Williams said, saying he expects the recent tax cuts and other tailwinds to boost economic growth this year.

- OPEC and Russia reaffirmed their oil-cut alliance may endure past 2018. Russia is prepared to continue cooperating with the cartel and Saudi Arabia even after the deal expires, Energy Minister Novak said.

- Greece's sovereign credit rating was raised one level by S&P to B (positive outlook). EMU FM's meet today to assess the country's compliance with bailout terms and could sign off on loan disbursements of about €6.7 bn.

- Spain's credit rating was raised one level at Fitch, from BBB+ to A- (stable outlook), which said the country's 'buoyant' economic growth has helped reduce the government's general deficit.

Currencies: USD Withstands US Government Shutdown

USD withstands US government shutdown

The US government shutdown debate dominated the headlines on Friday, but there was no risk-aversion. US yields, equities and the dollar even traded with a upward bias as the US session proceeded. US bond yields tested resistance levels. The dollar held up well even as the political stalemate persisted. EUR/USD finished the session at 1.2222 (from 1.2238). USD/JPY closed the day slightly lower at 110.77.

The US Senate didn't agree on a spending bill. There was a slight retracement on Friday's reflation trade at the start in Asia this morning, but the move didn't went far. US yields decline slightly but the test of key technical levels is ongoing. The dollar opened slightly softer, but EUR/USD and USD/JPY soon rebounded back to Friday's closing levels.

The eco calendar is empty today. European news is constructive with the German SPD members giving green light for coalition talks. Spain and Greece enjoyed a rate upgrade on Friday. For now, this doesn't help the euro much. Markets will look out for a new vote on a temporary spending bill scheduled for CET 18.00. USD trading might remain erratic and driven by the news flow from Washington. That said, USD sentiment doesn't look too bad this morning. Is the US currency finally receiving some support from higher US yields?

Global Picture: the dollar was in the defensive of late as markets prepare for a change in policy from central banks outside the US. This propelled EUR/USD despite a huge interest rate differential in favour of the dollar. The USD decline slowed last week, but any 'rebound' remained unconvincing. A return below previous resistance at 1.2092 is needed to call off the ST alert for the dollar. EUR/USD 1.2598 (62% retracement) is next important resistance on the charts.

Disappointing UK retail sales mitigated sterling's positive momentum last week, but the damage for the UK currency was limited. EUR/GBP gradually returned to intermediate support in the low 0.88 area (probably inspired by the intraday EUR/USD price trend. Later this week, the UK CBI order data (Tuesday), labour data (Wednesday) and the first Q4 GDP estimate will be published. Of late, UK eco data were mostly only of intraday significance for sterling trading. Even so, a break below the 0.8800/10 area, might open the way for a retracement toward the 0.87 support, which we still consider a tough resistance

EUR/USD: stays away from recent top despite US political uncertainty

Market Update – Asian Session: Dollar Slightly Weaker, Markets Stall On US Govt Shutdown

Headlines/Economic Data

General Trend: Asian markets trade mixed as US government shutdown approaches 3rd day

US dollar (USD) trades broadly weaker following start of US government shutdown

South Korea 10-year bond yield rises over 5bps amid debt sale and gov’t considering issuance of 50-year bond; MSCI said the previously proposed capital gains tax on foreigners may hurt the South Korean equity market

Japan

Nikkei 225 opened -0.7%; closed %

TOPIX Securities +1%; Iron & Steel -1.2%

Nippon Paint +10% [4612.JP]: Largest shareholder Wuthelam Group is seeking more seats on board

Toshiba [6502.JP]: +3%: Considering IPO of memory chip business if sale falls through or fails to get regulatory approval by the end of March – FT

Kawasaki Heavy [7012.JP]: +1% (Expected to win a large order for subway cars in NYC – Nikkei)

Tokyo Steel [5423.JP] -1.3%: To raise Feb H-beam prices to ¥89K/t from ¥87K, hot-rolled oil price to ¥74K/ton from ¥73K

Nippon Steel [5401.JP] President: Want to raise steel prices again this year to reflect rising costs of raw materials and transportation

Looking Ahead: Bank of Japan (BoJ) decision and quarterly outlook report due for release on Tuesday

Tokyo Steel to report FY results after close on Tuesday

Korea

Kospi opened -0.2%

Chipmakers decline: Samsung Electronics -2%, Hynix -2.2%

Steelmakers trade weaker: Posco -3.5%, Hyundai Steel -0.5%

Banks trade generally weaker: Hana Financial -1.9%, Industrial Bank of Korea -1%, Woori Bank -1.1%,

Lotte Chemical [011170.KR]: +4.5% (positive broker commentary)

(KR) South Korea Dec PPI M/M: 0.1% v -0.1% prior; Y/Y: 2.3% v 3.1% prior

(KR) South Korea Jan 20-day Exports y/y: 9.2% v 16.4% prior; Imports y/y: 14.1% v 19.5% prior

(KR) South Korea Govt to mandate banks and exchanges to keep records of cryptocurrency transactions, in a potential move to impose taxes on the largely covert deals, financial authorities

(KR) South Korea Financial Services Commission: will tighten capital regulations on high-risk household lending

(KR) South Korea Finance Ministry: 'Positively' considering issuance of 50-year government bond

China/Hong Kong

Hang Seng opened +0.1%, Shanghai Composite -0.3%

Hang Seng Services Index +1.6% (strength in airlines and gaming firms), Materials +1.3%, Property/Construction +0.6%; Telecom -0.2%

HSBC -0.5% (~10.3% weighting of Hang Seng Index)

Units of China conglomerate HNA Group trade lower: HNA Infrastructure and HNA Innovation each decline by over 9%

Pou Sheng International [3813.HK] +27% (received takeover offer from Taiwan based parent company)

(CN) PBOC Adviser: Reiterates there is no need for PBoC to raise benchmark interest rates – China Daily

(CN) China PBOC OMO: Injects CNY110B v CNY230B injected in 7,14 and 63-day reverse repos prior: Net injection CNY20B v CNY80B injected prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.4112 v 6.4169 PRIOR (strongest CNY fix since Dec 8, 2015)

(CN) China Energy Administration: 2017 power consumption 6,307.7B KwH. +6.6% y/y

(CN) China forex market-making banks have voluntarily changed the counter-cyclical adjustment factor to the neutral stance in the pricing mechanism of the yuan's central parity rate in response to weakened yuan depreciation prospects.

(CN) China NDRC Spokesperson: Reiterates confident economy will maintain steady and good momentum in 2018; End 2017 outstanding corporate bonds CNY4.9T

Australia/New Zealand

ASX 200 opened +0.1%; closed -0.2%

ASX 200 REIT Index -0.5%, Financials -0.4%, Energy -0.4%

Commonwealth Bank [CBA.AU] -1.3% (cautious broker commentary)

SDL.AU To sell 51% stake in Cam Iron to Tidfore under MOU, no terms disclosed yet; +67%

YAL.AU Reports Q4 saleable coal production 8.65Mt, +92% y/y; +10%

DHG.AU Guides H1 digital revenue growth +22% y/y; total revenue growth +13% y/y; CEO Anthony Catalano to resign -12%

(AU) Australia PM Turnbull affirms next election won’t be held until 2019 - AFR

(AU) ANZ sees RBA raising rates in May this year as inflation picks up - local press

Other Asia

(TW) Taiwan may include Bitcoin in anti-money laundering rules - local press

Taiwan Dollar (TWD) gains 0.6% (highest level since Jan 2013)

(TH) Thailand Dec Customs Trade Balance: -$280M v $1.1Be (1st deficit since July 2017)

North America

US government shutdown: On Sunday, the US government shutdown entered its second day

(US) Senator Majority Leader Mcconnell (R): Set next Senate procedural vote on 3-week stopgap spending bill for noon EST Monday (vs prior reports that a vote could occur at 1 am EST on Monday); If DACA is not resolved by Feb 8th and government is open, he would allow a vote.

(US) Senator Flake (R-AZ):; Bipartisan meeting to be held on Monday at 10 am EST to discuss continuing resolution (CR)

(US) US Senate minority leader Schumer (D): Yet to reach agreement on path forward

Xerox [XRX]: Shareholders Icahn and Deason said to call for possible sale of the company - US financial media

Bioverativ [BIVV]: Sanofi said to be near deal to acquire the company for more than $11.5B; shareholders could receive $105/share (~64% premium) - US financial press

Looking ahead: Corporate earnings are expected from companies including Haliburton, Netflix, Steel Dynamics, TD Ameritrade

Europe

(DE) Today Germany Social Democrats (SPD, center-left) in a part conference agreed to support the opening of formal coalition talks with Chancellor Merkel’s conservative bloc

(ES) Fitch raises Spain sovereign rating one notch to A- from BBB+; outlook to Stable from Positive (from Jan 19th)

(GR) S&P raises Greece sovereign rating one notch to B from B-; maintains outlook Positive (from Jan 19th)

Barclays: Tiger Global has built more than a $1.0B stake in Barclays - FT

Looking Ahead: World Economic Forum due to be held in Davos, Switzerland from Jan 23-26th

Corporate earnings are expected from companies including UBS

Levels as of 01:00ET

Nikkei225 0%, Hang Seng +0.3%; Shanghai Composite +0.0%; ASX200 -0.2%, Kospi -0.9%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax +0.0%; FTSE100 -0.2%

EUR 1.2274-1.2214; JPY 110.89-110.53; AUD 0.8003-0.7978;NZD 0.7289-0.7268

Feb Gold -0.1% at $1,331/oz; Mar Crude Oil +0.2% at $63.41/brl; Mar Copper +0.6% at $3.20/lb

Asian Markets Are Mixed This Morning

Market movers today

We have a fairly quiet start to the week, which will be dominated by the Bank of Japan meeting (decision due to be announced tomorrow morning) and the ECB meeting on Thursday. See our expectations in our respective previews: BoJ preview, 17 January, and ECB preview, 19 January. On the BoJ meeting, we expect it to keep its 'QQE with yield curve control' policy unchanged, while Governor Haruhiko Kuroda should downplay the significance of daily market operations and repeat the BoJ's commitment to the current yield curve control. Looking ahead, we think it will keep its policy unchanged in 2018, assuming Kuroda is reappointed when his term ends in April.

Given the few data releases today, investor focus will be on the political developments in the US and Germany. In the US, investors will focus on the implications of a shutdown of the US government on Friday, as the US senate failed to pass a short -term funding measure (see here).

In the Germany, investors are likely to price in an increased likelihood of a grand coalition following SPD members yesterday giving their support for the party leadership to open formal coalition talks with the CDU/CSU on forming a new government .

Market movers today

Asian markets are mixed this morning with China slightly up while Japanese shares are down. This follows a weekend of significant political developments on both sides of the At lantic. In the US, members of congress have sought to break the stalemate that followed the failure to pass the short -term funding measure to keep the US government open. It is difficult to predict how long the US government shutdown will last, al though our base case is that it will find a solution fairly quickly. This should limit the economic damage: During the last closure of government in Q4 13 (more precisely from 1-17 October that year), GDP growth was lowered by about 0.3 percentage points, as federal workers were sent home, according to a BEA analysis. The USD was little affected over the weekend by the government shutdown.

In Germany yesterday, the Social Democrats (SPD) voted `yes' to pursue coalition talks with Angela Merkel's conservatives , moving one step closer to a stable government after months of political uncertainty. SPD delegates voted by 362 to 279 to move ahead with negotiations after the centre-left party's leaders agreed a preliminary coalition blueprint with Merkel's conservative bloc earlier this month. There was one abstention. Her party is due to recommend the resumption of coalition talks as soon as today.

Over the weekend, Spain was upgraded to ‘A-' by Fitch due to the improved growth and debt out look, as Catalonia was not seen to have had a big economic impact so far. We expect that Spain will launch a new 10y benchmark next week and look out for a strong demand and tight price.

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.8002 on Friday.

LME Copper prices rose 0.5% or $32.0/MT to $7079.0/MT. Aluminium prices rose 1.4% or $31.0/MT to $2256.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7995, with the AUD trading 0.09% lower against the USD from Friday’s close.

The pair is expected to find support at 0.7970, and a fall through could take it to the next support level of 0.7944. The pair is expected to find its first resistance at 0.8030, and a rise through could take it to the next resistance level of 0.8064.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Euro-Zone’s Current Account Surplus Increased In November

For the 24 hours to 23:00 GMT, the EUR declined 0.1% against the USD and closed at 1.2232 on Friday.

In economic news, the Euro-zone's seasonally adjusted current account surplus widened to €32.5 billion in November, after dropping for two straight months and compared to a revised surplus of €30.3 billion in the previous month.

Separately, Germany's producer price index (PPI) rose 2.3% on an annual basis in December, at par with market expectations. In the prior month, the PPI had climbed 2.5%.

The greenback advanced against most of its major counterparts on Friday, as investors shrugged off worries over a possible US government shutdown.

Macroeconomic data released in the US indicated that the flash Reuters/Michigan consumer sentiment index unexpectedly dropped to a level of 94.4 in January, dipping to its lowest level since July 2017, as consumers turned less optimistic about the current economic conditions. The index had registered a level of 95.9 in the previous month, while markets had expected for a rise to a level of 97.0.

In the Asian session, at GMT0400, the pair is trading at 1.2228, with the EUR trading a tad lower against the USD from Friday's close.

Meanwhile, the US government could not avert a shutdown, after members of the Senate failed to reach an agreement to fund government operations before the Friday's deadline.

The pair is expected to find support at 1.2200, and a fall through could take it to the next support level of 1.2171. The pair is expected to find its first resistance at 1.2276, and a rise through could take it to the next resistance level of 1.2323.

Amid a lack of macroeconomic releases in the Euro-zone today, investors would focus on the US Chicago Fed national activity index for December, scheduled to release later in the day.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average

Britain’s Retail Sales Plunged To An 18-Month Low Level In December

For the 24 hours to 23:00 GMT, the GBP declined 0.19% against the USD and closed at 1.3870 on Friday, after data showed that UK's retail sales came in worse-than-expected in December.

Britain's retail sales slid 1.5% on a monthly basis in December, declining by the most since the Brexit vote in 2016 and offering further evidence that rising price pressures and stubbornly weak wage growth would continue to erode the nation's consumer spending. Retail sales had registered a revised gain of 1.0% in the prior month, while markets were anticipating for a fall of 1.0%.

In the Asian session, at GMT0400, the pair is trading at 1.387, with the GBP trading flat against the USD from Friday's close.

The pair is expected to find support at 1.3824, and a fall through could take it to the next support level of 1.3779. The pair is expected to find its first resistance at 1.393, and a rise through could take it to the next resistance level of 1.3991.

In absence of any major macroeconomic releases in the UK today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.39% against the JPY and closed at 110.60 on Friday.

In the Asian session, at GMT0400, the pair is trading at 110.79, with the USD trading 0.17% higher against the JPY from Friday’s close.

The pair is expected to find support at 110.51, and a fall through could take it to the next support level of 110.23. The pair is expected to find its first resistance at 111.05, and a rise through could take it to the next resistance level of 111.31.

Going forward, investors would be paying close attention to the Bank of Japan’s (BoJ) interest rate decision, due in the early hours of tomorrow.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.