Sample Category Title

Forex Markets Staying in Consolidation Mode, Aussie Got No Lift from Strong Job Data

Trading in the forex markets remain rather dull today. Dollar's recovery overnight again lack conviction. Nonetheless, USD/JPY does seem to have bottomed out, but that's mainly thanks to Yen's weakness. Canadian Dollar is bounded in range after the highly anticipated BoC rate hike. Traders are holding their bet on the Loonie after cautious tone of BoC. Sterling spiked higher through 1.3835 key resistance but there was no follow through buying. It'll take a little more time to see if that's bull trap. Australian Dollar doesn't get any lift by strong job data and is staying in consolidation.

Canadian Dollar range bound after BoC rate hike

BOC raised the policy rate by 25 bps to 1.25% yesterday, as "recent data have been strong, inflation is close to target, and the economy is operating roughly at capacity". The move had been widely anticipated. As such, we observed the instant "sell the news" move in USDCAD after the announcement. Canadian dollar's retreat was pared later in the day, though, as the market has priced in another rate hike by May. Policymakers remained cautious over future rate hikes and cited the uncertainty in the NAFTA renegotiations as a risk. Yet, the market appeared to have shrugged off these comments.

The central bank also released its latest Monetary Policy Report (MPR), providing updated economic projections. The staff projected GDP growth to average at 3% in 2017, followed by 2.2% in 2018 (up from 2.1% in October's estimate). Growth should ease further to 1.6% in 2019 (up from October's 1.5% forecast). A major risk facing Canadian economy is the uncertainty around NAFTA negotiations which is "clouding the economic outlook". As such, the latest economic projections have incorporated "additional negative judgment on business investment and trade" of NAFTA uncertainty.

More in BOC Raises Policy Rate, Market Prices In Another Hike Before May

Fed Beige Book: Modest to moderate gains in activity

The latest Beige Book prepared by the Atlanta Fed continued to depict an upbeat economic environment. All Districts surveyed reported "modest to moderate gains" in economic activity while Dallas reported a "robust" increase. The outlook for this year remains optimistic. On the employment situation, most Districts noted a tight labour market. Some suggested that the situation is constraining growth. Despite this, wages in most Districts only grew at a "modest" pace.

Focus shifting to BoJ meeting next week

With BoC decisions now passed, focuses are gradually shifting to BoJ meeting next week. According to a Reuters poll, the majority of economists surveyed expected BoJ to stand pat on interest rate throughout 2018. But it should also be noted that there is no overwhelming consensus on what would happen in the second half. It's noted that the outlook in the latter part of 2018 will very much depend on the future of Governor Haruhiko Kuroda. That is, whether Prime Minister Shinzo Abe would offer him another term.

Yet, for the near term, there is little chance for a change in BoJ's policies. According to Bloomberg's report, the summary of opinions of December meeting noted discussion on the possibility of raising rates. But that's just a small shift in sentiments, and it's not even a majority of view. The document noted that "when it is expected that economic activity and prices will continue to improve going forward, the situation may occur where the Bank will need to consider whether adjustments in the level of interest rates will be necessary," as one member said.

Australia job growth extends record streak

Australian job growth remained strong with 34.7k expansion in December. That's more than double of market expectation of 15.2k. That's the 15th straight month of expansion, the longest streak since 1993. And the more encouraging part is that full time jobs rose by 322k since December 2016, making up the majority of the 393k growth. Unemployment rate rose to 5.5% but that's due to a jump in participation rate at 65.7%. For the moment, markets are only pricing in 50/50 chance of an RBA rate hike by August. Also from Australia, consumer inflation expectation rose 3.7% in January.

Elsewhere

A batch of key Chinese data will be the focus today, including GDP. US will release housing starts, Philly Fed survey and jobless claims.

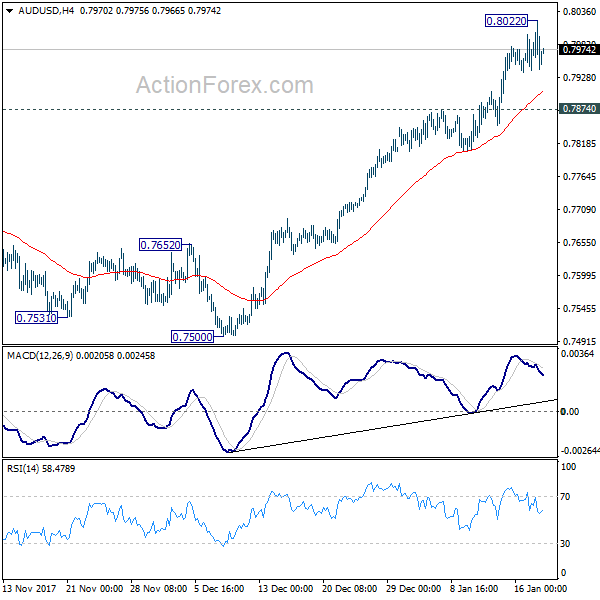

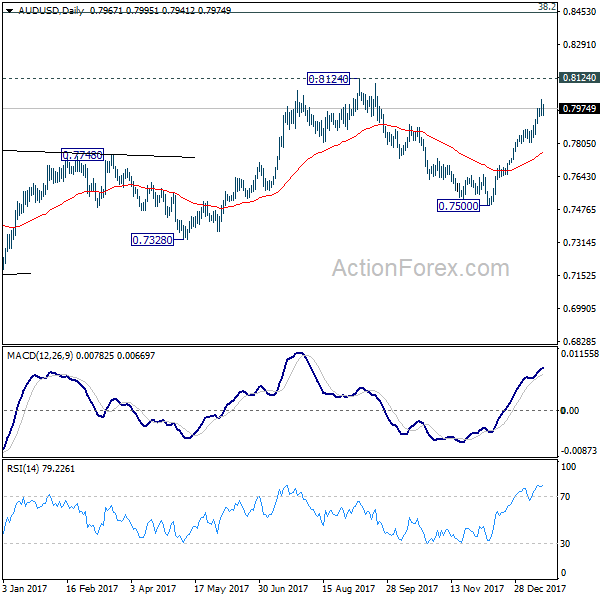

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7932; (P) 0.7977; (R1) 0.8014; More...

AUD/USD lost some upside momentum after hitting 0.8022 and intraday bias is turned neutral for consolidations first. Further rally is expected as long as 0.7874 support holds. Above 0.8022 will extend the rise from 0.7500 to 0.8124 high. there will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451. On the downside, break of 0.7874 will indicate short term topping and turn bias to the downside for 55 day EMA (now at 0.7764).

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | Consumer Inflation Expectation Jan | 3.70% | 3.70% | ||

| 0:01 | GBP | RICS House Price Balance Dec | 0.00% | -1.00% | 0.00% | |

| 0:30 | AUD | Employment Change Dec | 34.7K | 15.2K | 61.6K | 63.6K |

| 0:30 | AUD | Unemployment Rate Dec | 5.50% | 5.40% | 5.40% | |

| 4:30 | JPY | Industrial Production M/M Nov F | 0.60% | 0.60% | ||

| 7:00 | CNY | GDP Y/Y Q4 | 6.70% | 6.80% | ||

| 7:00 | CNY | Retail Sales Y/Y Dec | 10.20% | 10.20% | ||

| 7:00 | CNY | Industrial Production Y/Y Dec | 6.10% | 6.10% | ||

| 7:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Dec | 7.10% | 7.20% | ||

| 13:30 | CAD | ADP Employment Dec | 59.2K | |||

| 13:30 | USD | Housing Starts Dec | 1.27M | 1.30M | ||

| 13:30 | USD | Building Permits Dec | 1.29M | 1.30M | ||

| 13:30 | USD | Philadelphia Fed Business Outlook Jan | 24 | 26.2 | ||

| 13:30 | USD | Initial Jobless Claims (JAN 13) | 251K | 261K | ||

| 15:30 | USD | Natural Gas Storage | -359B | |||

| 16:00 | USD | Crude Oil Inventories | -4.9M |

Fed: Beige Book Indicates Solid Economic Activity Through the End of 2017

Today's Beige Book indicated that economic activity across all twelve Federal Reserve Districts continued to expand from late-November through the end of 2017. The Dallas District reported a robust increase in activity while the remaining Districts noted modest to moderate gains over this period of time. Sentiment remains positive and should be amplified this year as the impact of tax reform begin to take effect.

Retailers reported expansion in non-auto purchases, with the holiday season rewarding some more than anticipated. On the other hand, vehicle purchases were mixed across Districts as the boost from hurricane replacement needs dwindled. Increasingly, retailers are implementing technology upgrades and expanding their e-commerce channels in order to remain competitive.

Price pressures largely intensified relative to the previous report, with inputs to manufacturing, construction and transportation experiencing notable cost increases. Some of these increases in non-labor input costs were passed onto consumers by way of selling prices. Retail price increases were modest in comparison, while building material prices remained elevated.

Residential real estate inventories remained tight, leading to consistent growth in home prices. However, the lack of homes for sale restrained home transactions, which were largely flat as buyers were disappointed by the lack of options on the market. At the same time, a scarcity of labor also limited construction activity, with contacts reporting little relief in the near future. Non-residential activity continued to increase, supported by favorable business conditions.

Employment growth continued at a modest pace relative to the prior report, with hiring becoming increasingly complicated by a shortage of qualified workers. Notably, manufacturing and construction workers were in short supply. This led employers to increase wages, with a widening array of industries raising wages since the prior report. Additionally, several firms intend to continue raising wages in the coming months.

Manufacturers largely reported modest growth in business conditions, with capital expenditures increasing for many producers. Transportation activity also rose alongside production. Some auto assembly plants experienced delays in activity as they re-tooled their shops in order to shift focus away from small passenger car production towards SUVs. Importantly, several manufacturers intend to ramp up investment in 2018 as order volumes are expected to rise.

Key Implications

This Beige Book confirms that the economy rounded out 2017 on solid footing. Inflation pressures continued to build, with steady increases in labor and non-labor input costs suggesting that selling prices will edge higher over 2018. Strong demand led several manufacturers to invest in additions to capacity, with this trend set to continue through the year as the effects of tax reform begin to be felt. Specifically, the slashing of the corporate tax rate, along with the immediate expensing of equipment should support investment. Additionally, heightened global economic growth expectations will further add to this positive sentiment. At the same time, the renegotiation of NAFTA is still a lingering uncertainty, and may thwart some investment until a resolution is in sight.

Consumer incomes will continue to reap the benefits of a tightening labor market, with personal income tax cuts further supporting disposable income gains. On the housing side, inventory of homes for sale will likely remain constrained, as the pipeline of new properties is hindered by labor shortages in the construction industry, with price pressures remaining in place. This will continue to stretch affordability and, together with the implementation of the $10,000 cap on state and local tax deductions (which includes property taxes), will also raise the cost of homeownership. Taken together with the lower cap on the mortgage interest deduction (down from $1M to $750k), this is slated to weigh on home price growth in high-priced markets including those in New York and the District of Columbia.

This report suggested that businesses are increasingly passing on increases in their own input costs to consumers. As such, these should show up in headline inflation figures in the near future. Together with a healthy labor market, the pick-up in inflation should enable the Fed to implement three hikes this year, with the first of these likely to take place in March.

Gold Price Testing Crucial Support At $1320

Key Highlights

- Gold price is in a major uptrend and it recently broke the $1300-1320 resistance zone against the US Dollar.

- There are two key bullish trend lines forming with support at $1325 and $1320 on the 4-hours chart of XAU/USD.

- The price remains in an uptrend as long as it is above the $1320 level.

- The US Industrial Production in Dec 2017 increased by 0.9%, more than the forecast of +0.4%.

Gold Price Technical Analysis

There were heavy upsides noted in Gold price from the $1250 support against the US Dollar. The price climbed above the $1280, $1300 and $1320 resistances to place itself in the bullish zone.

Looking at the 4-hours chart of XAU/USD, there is a clear uptrend in place above $1300. The price recently traded as high as $1344.37 and is currently correcting lower.

There are two key bullish trend lines forming with support at $1325 and $1320 on the same chart. An intermediate support was broken at the 38.2% Fib retracement level of the last leg from the $1308 low to $1344 high.

A key support and buy zone is around $1320-25 since it is near the 50% Fib retracement level of the last leg from the $1308 low to $1344 high. Clearly, there are many supports on the way down starting with $1325 up to $1320.

Should there be a close below $1320, the price may move into a short-term bearish trend for a test of the $1300 and $1280 support levels.

On the flip side, an initial resistance is at $1345. A successful close above $1345 could open the doors for further gains toward the $1380 level.

Recently, the US saw the release of the Industrial Production for Dec 2017. The market was looking for an increase of 0.4% in Dec 2017 compared with the previous month. The actual result exceeded the forecast as there was an increase of 0.9%.

Initially, there was no major help for the greenback after the release since major pairs such as EUR/USD and GBP/USD were seen trading higher. Later, both pairs moved down and trimmed gains. Moreover, USD/JPY started an upside recovery and traded above 111.00.

Australia’s Unemployment Rate Unexpectedly Advanced In December

For the 24 hours to 23:00 GMT, the AUD traded flat against the USD and closed at 0.7958.

LME Copper prices rose 0.3% or $24.0/MT to $7047.0/MT. Aluminium prices rose 0.7% or $15.0/MT to $2187.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7956, with the AUD trading slightly lower against the USD from yesterday's close.

Overnight data indicated that Australia's seasonally adjusted unemployment rate surprisingly rose to 5.5% in December, while market participants had envisaged the unemployment rate to remain steady at 5.4%. On the contrary, the number of people employed in Australia rose more-than-expected by 34.7K in December, following a revised increase of 63.6K in the previous month.

Meanwhile, the nation's consumer inflation expectations remained unchanged at 3.7% in January.

The pair is expected to find support at 0.7924, and a fall through could take it to the next support level of 0.7891. The pair is expected to find its first resistance at 0.8006, and a rise through could take it to the next resistance level of 0.8055.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average

Euro-Zone’s Annual Inflation Slowed As Expected In December

For the 24 hours to 23:00 GMT, the EUR declined 0.73% against the USD and closed at 1.2170, after a couple of officials from the European Central Bank (ECB) voiced worries over the common currency's sharp rally.

On the macro front, data showed that the Euro-zone's final consumer price index (CPI) climbed 1.4% on an annual basis in December, confirming the flash estimates and compared to a rise of 1.5% in the prior month. Also, the region's seasonally adjusted construction output rebounded 0.5% on a monthly basis in November, after recording a revised drop of 0.3% in the prior month.

Macroeconomic data released in the US showed that industrial production climbed 0.9% MoM in in December, beating market expectations for an advance of 0.5%, buoyed by robust gains in utility output. In the prior month, industrial production had recorded a revised fall of 0.1%. Moreover, the nation's manufacturing production climbed 0.1% on a monthly basis in December, falling short of market consensus for a gain of 0.3%. Manufacturing production had risen by a revised 0.3% in the preceding month.

On the other hand, the nation's NAHB housing market index eased to a level of 72.0 in January, in line with market expectations. In the prior month, the index had registered a more than 18-year high level of 74.0. Other data revealed that the nation's MBA mortgage applications rose 4.1% in the week ended 12 January, compared to an increase of 8.3% in the previous week.

Separately, the Federal Reserve's (Fed) Beige Book report indicated that the US economy and inflation expanded at a modest-to-moderate pace from late November through the end of December 2017, while most districts reported modest increase in wages and tighter labour market conditions. Further, it revealed that the outlook for 2018 remains optimistic for a majority of contacts across the country.

In the Asian session, at GMT0400, the pair is trading at 1.2181, with the EUR trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2135, and a fall through could take it to the next support level of 1.2088. The pair is expected to find its first resistance at 1.2258, and a rise through could take it to the next resistance level of 1.2334.

Amid a lack of macroeconomic releases in the Euro-zone today, investors would look forward to the US housing starts and building permits data for December, followed by initial jobless claims figures, all slated to release later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s Pay Growth Would Accelerate And Jobless Rate Set To Fall To Fresh Lows: BoE’s Saunders

For the 24 hours to 23:00 GMT, the GBP rose 0.14% against the USD and closed at 1.3809, after an external MPC member of the Bank of England (BoE), Michael Saunders, stated that interest rates will likely have to rise faster-than-anticipated this year as he expects Britain's labour market to tighten further, pushing wage growth to its fastest rate since the financial crisis.

In the Asian session, at GMT0400, the pair is trading at 1.3807, with the GBP trading slightly lower against the USD from yesterday's close.

Overnight data indicated that UK's RICS house price balance registered an unexpected rise to 8.0% in December, compared to a flat reading in the prior month. Markets had anticipated for house price balance to fall to 1.0%.

The pair is expected to find support at 1.3729, and a fall through could take it to the next support level of 1.3650. The pair is expected to find its first resistance at 1.3914, and a rise through could take it to the next resistance level of 1.4020.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Industrial Production Revised Lower In November

For the 24 hours to 23:00 GMT, the USD rose 0.87% against the JPY and closed at 111.34.

In the Asian session, at GMT0400, the pair is trading at 111.44, with the USD trading 0.09% higher against the JPY from yesterday’s close.

Overnight data showed that Japan’s final industrial production advanced 0.5% MoM in November, less than a rise of 0.6% indicated in the preliminary print. Industrial production had registered a similar rise in the previous month.

The pair is expected to find support at 110.84, and a fall through could take it to the next support level of 110.24. The pair is expected to find its first resistance at 111.76, and a rise through could take it to the next resistance level of 112.08.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Losses This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.68% against the CHF and closed at 0.9661.

In the Asian session, at GMT0400, the pair is trading at 0.9653, with the USD trading 0.08% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9595, and a fall through could take it to the next support level of 0.9538. The pair is expected to find its first resistance at 0.9689, and a rise through could take it to the next resistance level of 0.9726.

Amid no macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic events.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoC Lifted The Benchmark Interest Rate, Warned On NAFTA Risk

For the 24 hours to 23:00 GMT, the USD rose 0.18% against the CAD and closed at 1.2456.

The Canadian Dollar lost ground against the USD, after the Bank of Canada (BoC), at its latest monetary policy meeting, cautioned that uncertainty linked to the future of NAFTA is clouding the economic outlook.

The BoC, as widely anticipated, raised the key interest rate by a quarter percentage point to 1.25%, on the backdrop of a recovery in inflation and a sustained growth in the economic activity. In a post-meeting statement, the central bank stated that while higher interest rates would be warranted over time, some continued monetary policy accommodation will likely be needed to support growth and inflation. However, the central bank also highlighted that the economic outlook remains marred by the future of North American Free Trade Agreement (NAFTA), as its uncertainty was causing investments to be postponed or diverted.

In the Asian session, at GMT0400, the pair is trading at 1.2456, with the USD trading flat against the CAD from yesterday’s close.

The pair is expected to find support at 1.2378, and a fall through could take it to the next support level of 1.2301. The pair is expected to find its first resistance at 1.2527, and a rise through could take it to the next resistance level of 1.2599.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BOC Raises Policy Rate, Market Prices In Another Hike Before May

BOC raised the policy rate by +25 bps to 1.25% in January, as 'recent data have been strong, inflation is close to target, and the economy is operating roughly at capacity'. The move had been widely anticipated. As such, we observed the instant 'sell the news' move in USDCAD after the announcement. Canadian dollar's retreat was pared later in the day, though, as the market has priced in another rate hike by May. Policymakers remained cautious over future rate hikes and cited the uncertainty in the NAFTA renegotiations as a risk. Yet, the market appeared to have shrugged off these comments.

At the press conference, Governor Poloz stressed that the monetary policy decision is 'data dependent', and 'there's no question that the data on balance since October have been stronger than our base case'. The central bank was upbeat over both global and domestic economic developments. The obviously hawkish note was its upgrades on the assessment of slack, suggesting that the 'economy is operating roughly at capacity'. In December, it remained focused on the 'continued absorption of economic slack'. The central bank also acknowledged that 'labor slack is being absorbed more quickly than anticipated'.

The central bank also released its latest Monetary Policy Report (MPR), providing updated economic projections. The staff projected GDP growth to average at +3% in 2017, followed by +2.2% in 2018 (up from +2.1% in October's estimate). Growth should ease further to +1.6% in 2019 (up from October's +1.5% forecast). A major risk facing Canadian economy is the uncertainty around NAFTA negotiations which is 'clouding the economic outlook'. As such, the latest economic projections have incorporated 'additional negative judgment on business investment and trade' of NAFTA uncertainty.

BOC acknowledged that inflation is moving close to target, but cautioned over fluctuation in the months ahead due to temporary factors. Revisions to the inflation forecast were modest and policymakers expect it to reach the +2% target in mid-2018, about a quarter earlier than projected in October.

On the monetary policy outlook, BOC admitted that 'the economic outlook is expected to warrant higher interest rates over time'. Yet, in order not to trigger excessive strength in the loonie which would be a drag the economic recovery, it affirmed that 'some continued monetary policy accommodation will likely be needed to keep the economy operating close to potential and inflation on target' and the 'Governing Council will remain cautious in considering future policy adjustments'.