Sample Category Title

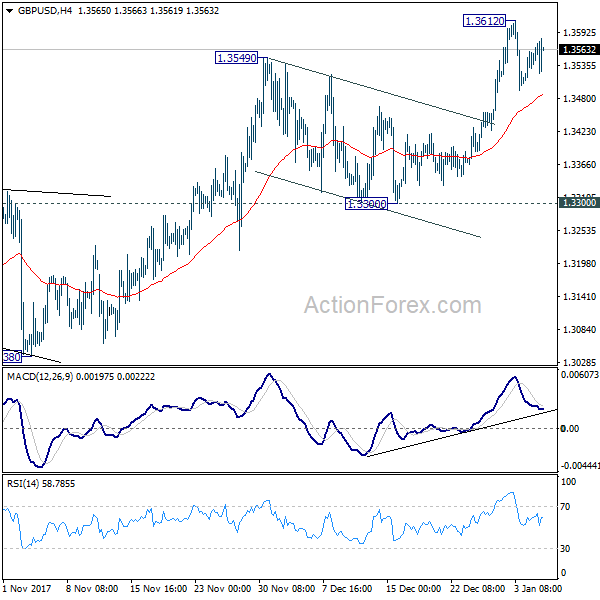

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3518; (P) 1.3538; (R1) 1.3572; More.....

Intraday bias in GBP/USD remains neutral for consolidation below 1.3612 temporary top. As long as 4 hour 55 EMA (now at 1.3488) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support.

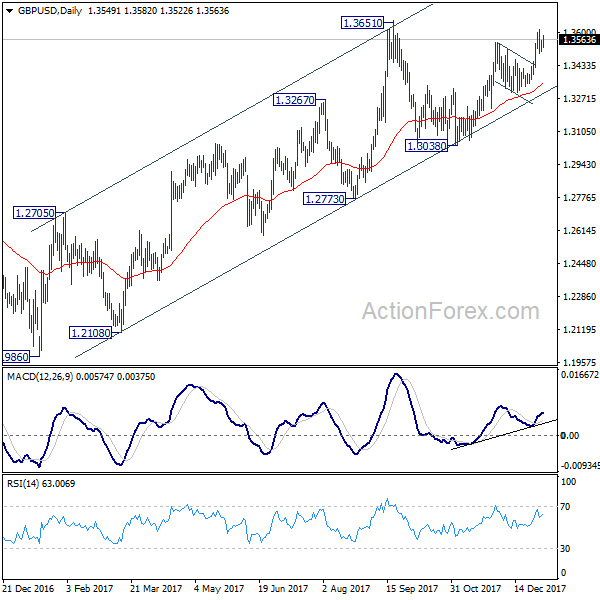

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

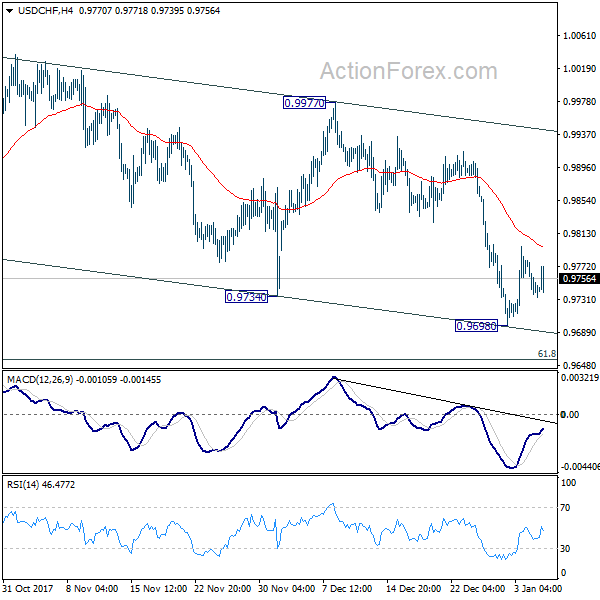

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9729; (P) 0.9755; (R1) 0.9772; More....

USD/CHF is staying in corrective trading above 0.9698 temporary low and intraday bias remains neutral. As long as 4 hour 55 EMA (now at 0.9795) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

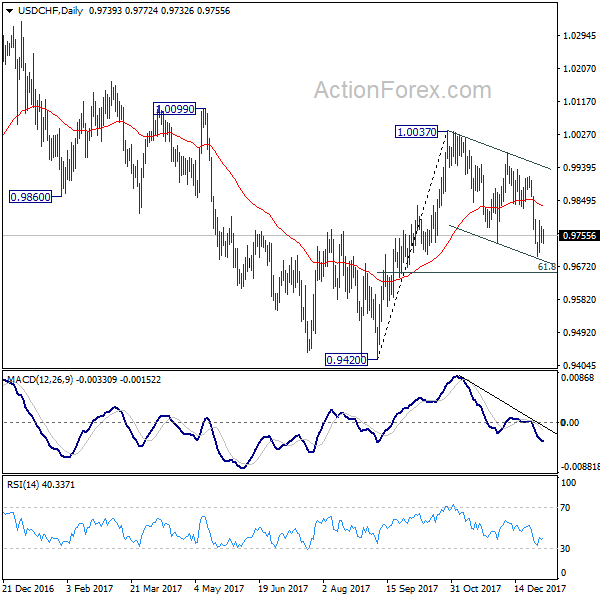

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

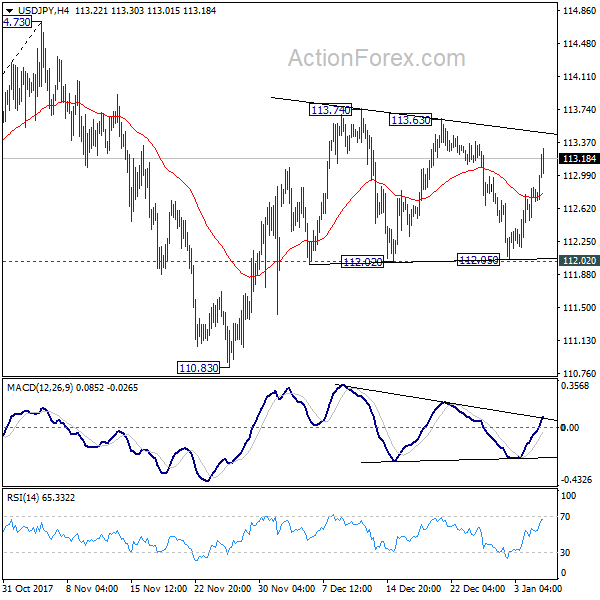

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.51; (P) 112.68; (R1) 112.92; More...

Despite the strong rebound from 112.05, USD/JPY is staying in range of 112.02/113.74 and intraday bias remains neutral first. Near term outlook stays bullish as long as 112.02 support holds and further rise is expected. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

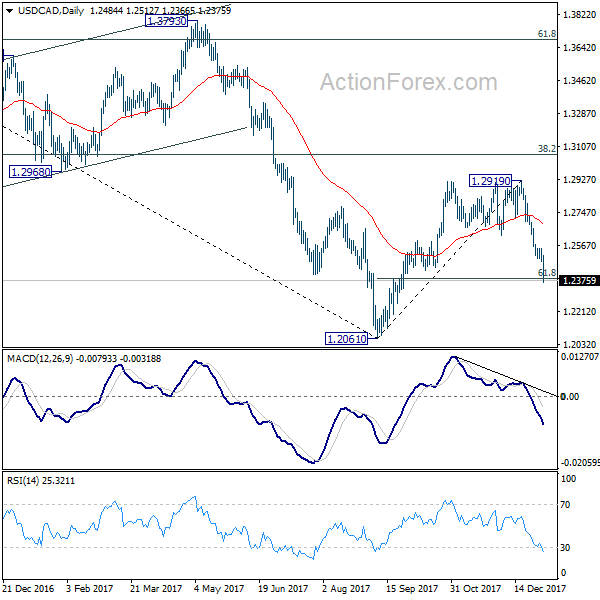

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2462; (P) 1.2508; (R1) 1.2534; More....

Dollar's fall accelerates to as low as 1.2366 so far and breaks 61.8% retracement of 1.2061 to 1.2919 at 1.2389. Based on current momentum, it's getting more likely that fall from 1.2919 is resuming larger down trend. Intraday bias stays on the downside as long as 1.2480 minor resistance holds. Sustained trading below 1.2389 will pave the way to 1.2061 low. On the upside, above 1.2480 will turn intraday bias neutral first.

In the bigger picture, current near term downside acceleration argues that USD/CAD was rejected by 55 week EMA (now at 1.2850. And the rebound from 1.2061 is possibly completed at 1.2919. More importantly, larger fall from 1.4689 (2016 high) could be resuming. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. Nonetheless, break of 1.2623 will revive the original case of bullish reversal and would resume the rebound from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

Canadian Dollar Surges on Another Stellar Job Report, Dollar Struggles after Mixed NFP

Canadian dollar soars in early US session after another month of stellar job data. The employment market grew and impressive 78.6k in December, just slightly smaller than prior month's 79.5k. It's also well above expectation of 0k growth. Unemployment ate, dropped to 5.7%, down from 5.9% and was way below expectation of 6.0%. That's also the lowest level in more than four decades, since the series began in 1976. The strength in job market is sealing the deal for BoC to hike again in Q1. And there could be more speculations for a January hike ahead. USD/CAD dives through 1.2380 handle, comparing to 1.2500 just an hour ago. Also from Canada, trade deficit came in larger than expected at CAD -2.5b in November.

Dollar, on the other hand, is trading a touch softer after mixed job data. Non-farm payrolls report showed 148k job growth in December, well below expectation of 189k. But prior month's figure was revised up from 228k to 252k. Unemployment rate was unchanged at 4.1% as expected. The positive part is that average hourly earnings grew 0.3% mom, meeting expectation. While the set of NFP data still indicates very healthy job market in the US, it's not doing much to solidify three Fed hikes this year. Also from US, trade deficit widened to USD -50.5b in November.

Technically, EUR/USD is still holding below 1.2091 resistance. USD/CHF is kept well above 0.9698 temporary low. USD/JPY is in range of 112.02/112.05. With the exception of USD/CAD, there is no clear sign of post-data direction in other Dollar pairs.

Released earlier today, Eurozone CPI slowed to 1.4% yoy in December, in line with consensus. But core CPI was unchanged at 0.9% yoy, missing expectation of 1.0% yoy. PPI jumped to 2.8% yoy in November, though. Eurozone retail PMI rose to 53 in December. German retail sales was strong and grew 2.3% mom in November. From Australia, trade balance unexpectedly turn into AUD -0.63b deficit in November, much worse than expectation of AUD 0.55b surplus. Japan monetary base rose 11.2% yoy in December. UK BRC shop price index dropped -0.6% yoy in December.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2462; (P) 1.2508; (R1) 1.2534; More....

Dollar's fall accelerates to as low as 1.2366 so far and breaks 61.8% retracement of 1.2061 to 1.2919 at 1.2389. Based on current momentum, it's getting more likely that fall from 1.2919 is resuming larger down trend. Intraday bias stays on the downside as long as 1.2480 minor resistance holds. Sustained trading below 1.2389 will pave the way to 1.2061 low. On the upside, above 1.2480 will turn intraday bias neutral first.

In the bigger picture, current near term downside acceleration argues that USD/CAD was rejected by 55 week EMA (now at 1.2850. And the rebound from 1.2061 is possibly completed at 1.2919. More importantly, larger fall from 1.4689 (2016 high) could be resuming. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. Nonetheless, break of 1.2623 will revive the original case of bullish reversal and would resume the rebound from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Dec | 11.20% | 13.20% | ||

| 00:01 | GBP | BRC Shop Price Index Y/Y Dec | -0.60% | -0.10% | ||

| 00:30 | AUD | Trade Balance (AUD) Nov | -0.63B | 0.55B | 0.11B | -0.30B |

| 07:00 | EUR | German Retail Sales M/M Nov | 2.30% | 1.00% | -1.20% | |

| 09:10 | EUR | Eurozone Retail PMI Dec | 53 | 52.4 | ||

| 10:00 | EUR | Eurozone PPI M/M Nov | 0.60% | 0.30% | 0.40% | |

| 10:00 | EUR | Eurozone PPI Y/Y Nov | 2.80% | 2.50% | 2.50% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec A | 0.90% | 1.00% | 0.90% | |

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Dec | 1.40% | 1.40% | 1.50% | |

| 13:30 | CAD | International Merchandise Trade (CAD) Nov | -2.5B | -1.3B | -1.5B | -1.6B |

| 13:30 | CAD | Net Change in Employment Dec | 78.6K | 0.0K | 79.5K | |

| 13:30 | CAD | Unemployment Rate Dec | 5.70% | 6.00% | 5.90% | |

| 13:30 | USD | Change in Non-farm Payrolls Dec | 148K | 189K | 228K | 252K |

| 13:30 | USD | Unemployment Rate Dec | 4.10% | 4.10% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Dec | 0.30% | 0.30% | 0.20% | |

| 13:30 | USD | Trade Balance Nov | -50.5B | -48.1B | -48.7B | -48.9B |

| 15:00 | CAD | Ivey PMI Dec | 62.2 | 63 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Dec | 57.6 | 57.4 | ||

| 15:00 | USD | Factory Orders Nov | 1.40% | -0.10% |

Global Equity Bulls Unstoppable, NFP in Focus

Another day, another record high for world stocks, as a growing sense of optimism over the global economy boosts risk sentiment.

Asian shares ventured higher during early trading on Friday, while European markets opened on a positive note amid the risk-on environment. With the Dow Jones Industrial Average surpassing 25,000 for the first time ever on Thursday, U.S equity bulls are clearly back in town and as such, we could see further gains on Wall Street this afternoon.

Dollar steady ahead of NFP

It is interesting how the Dollar remained stuck near a four-month low during early trading on Friday, despite the stronger than expected data in the US boosting expectations of a Fed rate hike in March.

The U.S ADP employment report smashed market expectations, as U.S private employers added 250,000 jobs in December, an encouraging sign from the U.S labour markets. The fact that the Dollar still depreciated following the economic release suggests that investors may be diverting their attention elsewhere, namely the upcoming U.S tax reforms. One of the biggest risks the Dollar could face this year, is the impact of Trump's sweeping tax overhaul falling below market expectations.

Today's main event risk for the Dollar will be the non-farm payroll report, which should offer fresh insight into the health of the U.S. job market. With the ADP results steamrolling over market expectations, investors will be paying attention to see if NFP headline figures produce a similarly positive pattern. Although Dollar bulls have entered the year simply missing in action, today's NFP report could provide a welcome boost. A solid headline NFP figure, coupled with signs of rising wage growth, may offer an opportunity for Dollar bulls to make a late Friday appearance. Alternatively, a disappointing U.S jobs report would likely result in further downside.

Taking a look at the technical picture, the Dollar Index remains bearish on the daily charts, with sustained weakness below 91.80 opening a path towards 91.55. For bulls to have any chance of charging back into the game, prices needed to break above 92.33 and 92.65, respectively.

Commodity spotlight - Gold

Gold edged lower trading on Friday, ahead of the anticipated U.S non-farm payroll data release, but remained on track for a fourth consecutive week of gains.

This has been a positive trading week for Gold, with a vulnerable U.S Dollar and geopolitical tensions in Iran likely factors behind the metal's appreciation. Gold bulls could be instilled with fresh inspiration to elevate prices higher, if the NFP report disappoints this afternoon. On the other hand, a solid report could spell further declines in the short term, with $1310 acting as a level of interest. Taking a look at the technical picture, Gold remains bullish on the daily charts above $1300. Bulls need to conquer $1320 for the metal to witness further upside towards $1333.

Dollar Stronger ahead of NFP Report; European Stocks Drift Higher

Here are the latest developments in global markets:

FOREX: December's preliminary inflation figures out of the Eurozone offered little to the euro as the price measures came in line with expectations on a yearly basis and slightly weaker relative to the month before. However, the region's producer prices surprised to the upside, providing some support to the common currency, which consolidated near four-week highs versus the greenback. Euro/dollar parked at 1.2048 (-0.16%), while euro/yen climbed to a two-year high of 136.51 (+0.30%). Pound/dollar reversed gains from earlier in the day, retreating to 1.3540, with investors looking forward to fresh Brexit news before taking positions. The dollar index broke above the 92 key-level (+0.20%) ahead of the all-important NFP report, while against the yen it stretched towards 113.25 (+0.44%) amid risk-on sentiment. Dollar/loonie inched up to 1.2510.

STOCKS: European stocks climbed higher on Friday, with eurozone shares being on track to post the best weekly performance since May as recent economic data strengthened investors optimism on the region's economic outlook. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.56% and 0.61% on the day respectively at 1015 GMT with healthcare and consumer cyclicals leading the gains. The Swiss SMI jumped to an all-time high (+0.41%), while the British FTSE 100 posted another record high (+0.28%). The German DAX 30 extended its uptrend for the third day, surging by 1.0% on the back of rising auto and healthcare stocks. Futures on the main US indices were pointing to a positive open.

COMMODITIES: Oil prices slipped even further during the European session as traders doubted whether the market will retain its bullish run given the threat from higher US production. WTI crude was trading 0.90% lower at $61.46 per barrel and Brent declined by 0.80% to $67.52. In other energy news, Saudi Arabia converted its giant oil company Aramco into a joint-stock company as of January 1, a key step to go through an initial public offering in 2018 in the domestic stock exchange. However, an international listing is also considered. Gold was down by 0.40% at $1,317.50 per ounce.

Day ahead: US & Canada report employment numbers

Looking ahead to the remainder of the day, the US will publish another patch of economic data that have the potential to shake the dollar.

Among the releases, the US government's monthly nonfarm payrolls report, which tracks labor stats for both the private and public sectors, will be in focus. According to analysts, the report due at 1330 GMT is expected to show a job gain of 190,000 in December compared to 228,000 seen in the previous month, whilst the unemployment rate is forecasted to remain unchanged at a 17-year low of 4.1%. However, these numbers might come second in priority as the markets are eagerly awaiting for wage growth to pick up instead and therefore push up the slow-moving inflation towards the Fed's 2.0% target. In November, average hourly earnings grew by 0.2% m/m and are anticipated to continue rising in December at the slightly faster pace of 0.3%. However, on a yearly basis wage growth is projected to stand flat at 2.5%.

Meanwhile, the Bureau of Economic analysis will give an update on trade balance figures, with the monthly trade deficit estimated to widen in November. At 1500 GMT factory orders and durable goods will come into view.

Traders will keep a close eye on the loonie as well, as Canadian labor data will be available along with the US employment report. Unlike the unemployment rate in the US, the Canadian one is anticipated to inch up by 0.1 percentage points to 6.0% in December. Regarding the number of job positions, those are anticipated to increase by 1,000, far below the previous mark of 79,500. Data on the trade balance and Ivey PMI readings will also gather some attention out of Canada.

In terms of policymakers' appearances, Philadelphia Fed President Patrick Harker will be speaking on the US economic outlook at 1515 GMT and Cleveland Fed President Loretta Mester will be participating in a panel discussion titled "Coordinating Conventional and Unconventional Monetary Policies for Macroeconomic Stability" at 1730 GMT. Bank of England chief economist Andy Haldane will be chairing panel discussions at the Allied Social Sciences Association Annual Meeting; the relevant event begins at 1930 GMT.

In oil markets, the US Baker Hughes oil rig count due at 1800 GMT will be in focus.

Canadian Dollar Steady as Investors Eye Employment Data

The Canadian dollar has ticked lower in the Friday session. Currently, the pair is trading at 1.2500, up 0.10%. On the release front, there are a host of key events on both sides of the border. In the US, wage growth is expected to gain 0.3%, but the markets are braced for a slowdown in Nonfarm Payrolls, with an estimate of 190 thousand. We'll also get a look at ISM Non-Manufacturing PMI, which is expected to edge up to 57.6 points. In Canada, Employment Change is expected to post a soft gain of 1.8 thousand, after a sparkling gain of 79.5 thousand in November. Canada will also release Ivey PMI and Trade Balance. Traders should be prepared for some movement from USD/CAD during Friday's North American session.

The Canadian dollar climbed 2.5% in December, and continues to move higher early in the New Year. Much of the loonie's climb can be attributed to the rise in oil, which has jumped 6.8% since mid-December. Geopolitical tensions have boosted oil prices, in particular tensions with North Korea and the recent civil unrest in Iran. There is pressure on the Bank of Canada to raise its benchmark rate of 1.0%, which is lagging behind the Federal Reserve rate of between 1.25-1.50%. With the Fed widely expected raise rates in January, the Canadian dollar could lose ground if the BoC fails to respond with a rate hike of its own on January 17. However, the BoC may hold back, as it concerns continue over US threats to dismantle the free trade agreement.

As expected, the Federal Reserve minutes from December were positive in tone. At that meeting, the Fed raised interest rates for a third time in 2017. Policymakers noted in the minutes that economic activity was expanding at a "solid pace", buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

USDJPY Strongly Bullish Above 113.10 Level

The U.S dollar has continued to firm against the Japanese yen in early Friday trading, with price-action now trading well above the key 113.10 technical level. The USDJPY pair is currently trading around the 113.25 region, as daily buying momentum accelerates as the U.S dollar index recovers lost ground. Going forward, the 113.60 resistance zone is the next major technical barrier for medium and long-term USDJPY bulls. The upcoming U.S Non-farm payrolls job report will impact the pair also, with expectations high for a solid headline number.

Buyers retain control of the pair while price-action trades above the key 113.10 level, upside targets for the USDJPY pair are located at 113.60 and 114.40.

Should the USDJPY pair decline below the 113.10 technical level, well-defined daily support is found at 112.70 and 112.30.

EURUSD Direction Defined by 1.2050 Level

The euro has moved marginally lower against the U.S dollar during the European trading session, falling to a session low around the 1.2040 region. The EURUSD slipped back despite a round of positive economic data points from the eurozone, which showed rising monthly inflation in the euro trading block and positive German Retail Sales figures. Moving into the U.S session, buyers will look to breach the 1.2089 weekly price- high, while sellers will be focused on the psychological 1.2000 support region.

The EURUSD pair remains bullish while trading above the 1.2050 level, a break of the 1.2089 weekly-high should expose further upside towards 1.2150 and 1.2200.

If sellers can contain the EURUSD below the 1.2050 level, sellers will try to move price-action back below the 1.2030 and 1.2000 levels.