Sample Category Title

Weekly Focus: Inflation Figures in Abundance

Market movers ahead

- In the US, we estimate core CPI inflation stood at 1.7 in December.

- In the euro area, the minutes from the ECB's December meeting are the highlight next week. We intend to look primarily for nuances in the assessment of the new staff projections, in particular on inflation.

- We estimate Chinese CPI inflation rose to 1.9% y/y in December.

- In the Nordic countries, inflation is in focus and we are set to get December figures for Denmark, Sweden and Norway.

- In Sweden, we also get the Riksbank Minutes from the previous meeting, which we hope will reveal a discussion on property prices and the importance that Board members attach to recent developments.

Global macro and market themes

- 'Reflation' beliefs have been spurred anew by a continued strong global cyclical stance, the enactment of the US tax reform and commodity-price rises. However, we doubt that 2018 will be the year when the global economy 'reflates', despite what looks like a benign growth environment near term.

- Central bank pricing appears increasingly aggressive in our view and we see potential for eventually fading 'reflation' hopes to postpone expectations for a first ECB hike, while the case for a Fed March hike could stay alive for now. This should send EUR/USD firmly below 1.20 in Q1.

Job Gains Slow to End 2017 Amid Solid 2018 Growth Start

Hiring slowed to 148,000 jobs in December, with the unemployment rate steady at 4.1 percent. Demand for labor remains strong, but sustaining 3 percent GDP growth will be difficult due to labor supply challenges.

Slower Hiring in December, But Trend Still Strong

Nonfarm payrolls came in a bit softer than expected for December, with employers adding 148,000 jobs over the month (top graph). Over the past three months, job gains averaged 203,700, which looks consistent with the 2.5-3.0 percent growth we expect to see in the first half of 2018. We continue to expect the FOMC to raise the fed funds rate again in March.

The weaker outturn in December can be traced to the service sector. Notably, retail employment fell by 20,000 jobs in December as the industry continues to adjust to changing buying patterns both on a seasonal and long-term basis. Hiring also slowed in transportation & warehousing, professional & business services and education & health relative to November. Hiring in the goods-producing sector held up better, rising by 55,000 amid solid gains in construction and manufacturing.

Beyond Nominal Wages: The Real Consumer Income

To get closer to 3 percent GDP growth, the demand side of the economy will need to be sustained by real income and thereby consumer spending. Average hourly earnings rose 0.3 percent in December. That pushed the 12-month gain up to 2.5 percent. For 2017 as whole, average hourly earnings grew 2.6 percent, the same as in 2016.

Moderate inflation has helped to generate real gains in average hourly earnings over the past few years, supporting household income and spending. When combined with aggregate hours worked (which takes into account payroll gains), real labor income looks to have picked up to about a 3.5 percent annual rate over the past three months.

We do not believe that recent months' weakness in hourly earnings suggests wage growth is stalling out. Broader compensation gains, including one-off bonuses or more generous benefits, have led a clearer uptrend in the Employment Cost Index over the past year (middle graph). Average hourly earnings can be somewhat noisy, but demand for workers remains strong and should generate some upward pressure on wages in the current year.

Will Labor Force Participation Rates Rise to Support 3 Percent?

Supply may be the bigger challenge for the coming year. The unemployment rate held steady at 4.1 percent, the third month in a row it has done so. However, we expect the rate to trend downward to 3.8 percent by the end of the year as total employment outpaces growth in the labor force. In 2017, 1.79 million jobs were added, while the civilian labor force increased by just 861,000 – we expect these tightening dynamics to continue.

Digging a little deeper, it is clear that structural issues persist. For example, while the labor force participation for men is higher than for women, growth in the prime age participation rate has only been experienced by women (bottom graph). These growth dynamics, or lack thereof, will pose a challenge to achieving sustained 3 percent growth.

Widening Trade Deficit Will Exert Drag on GDP Growth in Q4

The trade deficit widened markedly in the last two months of 2017. Consequently, real net exports likely exerted a significant drag on overall GDP growth in the fourth quarter.

Deficit Widens as Imports Jump More than Exports

The U.S. trade deficit widened to $50.5 billion in November from $48.9 billion in October (top chart). Not only was the outturn a bit higher than most analysts had expected, but it was the first time that the deficit has exceeded $50 billion since March 2012. Although exports of goods and services jumped by 2.3 percent in November, imports were up 2.5 percent.

There was broad-based strength on the export side of the ledger. The $2.5 billion increase in the export of capital goods was flattered by the $1.2 billion jump in exports of civilian aircraft, which can be volatile on a monthly basis. This sizeable increase in overall capital goods exports in November may reflect, at least in part, some statistical payback for weakness during the previous two months. Smoothing through the monthly volatility shows that overall exports clearly have rebounded in 2017 after their weakness in 2016. The value of American exports was up 6.0 percent in the September-November period relative to the same period in 2016 (middle chart).

There was also broad-based strength on the import side of the ledger. The value of imported petroleum products was up $1.5 billion in November. This increase in the value of petroleum imports largely reflects the trend increase in oil prices that occurred during the autumn. The volume of petroleum imports edged higher in November, but they remain well off their peak of a decade ago. Imports of cell phones jumped about $1.1 billion, which likely reflects the introduction of the Apple iPhone X. These one-off factors notwithstanding, import growth also strengthened over the course of 2017. Some of the increase in import values reflects higher commodity prices (e.g., oil), but growth in import volumes has strengthened as growth in domestic demand has picked up.

Net Exports Probably Exerted Headwinds on GDP Growth in Q4

In real (i.e., price adjusted) terms, the trade deficit widened by $1.1 billion in November. The real trade deficit is important because it enters directly into calculations of real GDP growth. Real net exports of goods and services provided modest positive contributions to overall GDP growth in the first three quarters of 2017, but it appears that the string will end in the last quarter of the year because real net exports of goods deteriorated significantly in October and again in November (bottom chart). If real exports and real imports in December remain at their respective November levels, then real net exports would slice more than one percentage point off of the topline GDP growth rate in Q4. Although we do not expect that the overall drag will be quite that large, real net exports likely exerted significant headwinds on overall GDP growth in Q4. Moreover, we look for a modest drag from trade to continue for the next few quarters.

Sunset Market Commentary

Global core bonds traded sideways going into the US payrolls report. Mixed EMU price data were ignored and oil & equity markets gave diverging impetus for bond trading. Brent crude corrected lower towards $67/barrel while the stock market party continued. US payrolls missed consensus by a wide margin, but earnings rose in line with expectations. US Treasuries spiked higher, while the Bund was unmoved. We don't expect the uptick to last as markets mainly focus on price instead of activity data. Changes on the German and US yield curves remain limited between -1 bp and +1 bp at the moment. The 2yr/10yr US yield differential narrowed to 50 bps, the lowest level since 2007. On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between +1 bp (Portugal) and -3 bps (Spain) with Greece outperforming (-8 bps).

Trading in the major USD cross rates also focused on the US payrolls. Yesterday, the dollar was in the defensive, but investors apparently found themselves positioned a bit too much USD short going into the US payrolls. Soft EMU inflation data had hardly any impact on the euro. EUR/USD traded in the mid 1.20 area just before the publication of the payrolls. Employment growth disappointed, but the key wage data were in line with consensus. The dollar spiked briefly lower upon the publication. EUR/USD jumped to the 1.2080 area, but the 1.2092 range top was again left intact. Even more, the dollar soon reversed post-payrolls losses. EUR/USD trades currently even below the pre-payrolls' level (1.2030 area). USD/JPY trades marginally below the pre-payrolls' level (currently 113.20 area). To conclude, payrolls disappointed, but the report caused hardly any damage for the dollar as price data are more important than activity data. The jury is still out, but the 1.2092 resistance again proves not that easy to break.

Risk sentiment on European stock markets remains ebullient with the German Dax posting another >1% gain, putting the YTD balance already at +3%. The Intel chip flaws can't spoil sentiment. US stock markets opened around 0.25% higher.

News Headlines

December EMU headline inflation declined in line with expectation from 1.5% Y/Y to 1.4% Y/Y, mainly due to negative energy base effects. Core CPI stabilized at 0.9% Y/Y, below 1% Y/Y consensus. Higher-than-expected November PPI readings (0.6% M/M & 2.8% Y/Y) balanced the core CPI miss from a market point-of-view. Higher producer prices might filter more rapidly through to consumer prices in a context of strong growth.

The December payrolls report disappointed. Net job growth amounted to 148k, below 190k forecasts. Taking into account revisions to the previous two months' figures results in a combined 51k miss. Bad weather wasn't to blame with less than average employees remaining home due to poor weather conditions. The unemployment rate stabilized as expected at 4.1%. Average hourly earnings, key to markets, printed as well bang in line with consensus (0.3% M/M & 2.5% Y/Y), but November data faced slight downward revisions.

The US non-manufacturing ISM disappointed in December, declining from 57.4 to 55.9 (vs 57.6 consensus).

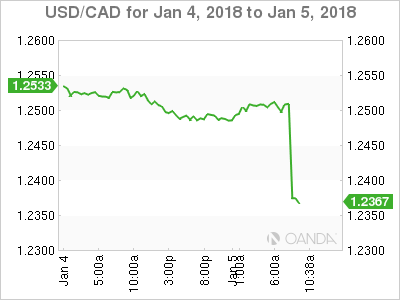

The Canadian job market is firing on all cylinders. The number of jobs rose by 78 600 (vs 2 200 consensus) in December, bringing the full-year employment gain to 422 500. That's the best annual increase since 2002. Canada's unemployment rate unexpectedly declined from 6% to 5.7%, the lowest level in more than 40 years. Average hourly earnings climbed by 2.7% Y/Y, down from 2.8% Y/Y in November. Canadian yields shot up to 9 bps higher with the 2-yr yield now at 1.7%, the highest since 2011. The loonie profited as well. USD/CAD dropped from around 1.25 to 1.2350. The market implied probability of a January rate hike from 1% to 1.25% increased from 41% to 73%.

USDCAD Falls Over 150 Pips on Weak US and Upbeat Canada Jobs Data

USDCAD fell to the lowest levels since late Sep 2017, on over 150-pips bearish acceleration after US / Canada jobs data. The greenback came under pressure on US NFP data miss while upbeat Canada employment figures (78.6K new jobs created in December vs 1K f/c) strongly boosted the loonie. Fresh bearish acceleration today is seen as extension of bear-leg from triple-top at 1.2915 zone, which broke below significant support at 1.2387 (Fibo 61.8% of 1.2061/1.2916 ascend and is expected to confirm strong bearish signal on daily close below 1.2387. Extension of bear-leg from 1.2915 lower platform below 1.2387 pivot would open way for full retracement of 1.2061/1.2916 corrective phase in the coming sessions. Meanwhile, bears may take a breather on oversold daily studies, with extended corrective upticks expected to stay capped under daily cloud base (currently at 1.2555).

Res: 1.2432; 1.2488; 1.2513; 1.2555

Sup: 1.2355; 1.2300; 1.2263; 1.2194

Canada Adds an Impressive 79K Jobs for a 13th Straight Monthly Gain

The Canadian labour market extended its gain in December, adding an impressive 78.6k net positions. Despite more Canadians being drawn to labour markets in December, the gains were enough to push the unemployment rate to 5.7% - the lowest rate since 1974.

Part time employment led the way again, adding 54.9k net positions, but full-time employment also rose, up 23.7k for a fourth straight monthly increase and a healthy 2.7% year-on-year gain.

Jobs were mainly among employees (as opposed to the self-employed) with 50.4k added in December. These positions skewed slightly towards the private sector (+28.2k), with the public sector adding 22.1k positions. Self-employment rose 28.2k on net.

By industry, the services side of the economy led the way, adding 72.6k positions. Notable standouts were finance, insurance, and real estate (+25.0k), educational services (+11.2k) and other services (+12.6k). The goods-producing side of the economy saw a more modest 6.0k net positions added as gains in construction and natural resources offset modest weakness in agriculture and manufacturing.

Among the provinces, all saw net hiring in December, but Quebec (+26.9k) and Alberta (+26.3k) topped the leader board. December's reports were impressive for both provinces: Quebec's unemployment rate, at 4.9%, reached another record low despite a climb in the participation rate, while Alberta recorded the strongest monthly job growth since 2011.

The hourly wage rate accelerated again, reaching 2.9% on a year-on-year basis. Strength could also be seen in the hours worked, which were up 3.1% year-on-year basis, helped by a robust month-on-month gain.

Key Implications

Unbelievable. We can now chalk up 13 straight months of job gains (a post-crisis record). What's more, nearly all details of the report were solid: despite more Canadians looking for work, job growth was enough to push the unemployment rate to 5.7%, its lowest level since 1974. It seems that Canadian job markets have been going from strength to strength of late.

The strength of the labour market is perhaps best reflected in further gains in wages, where growth has been robust – the 2.9% yearly climb is a far cry from the lows seen earlier in 2017. A solid climb in hours worked also bodes well for overall economic output in December.

For Bank of Canada governor Stephen Poloz, today's data should act as a further sign that despite hiccups in some areas of the economy, the underlying trend remains healthy. While risks to the outlook remain and may temper the overall pace of rate hikes, another policy interest rate hike in the near term now seems almost certain.

Canada’s Trade Deficit Narrowed Significantly in October

Canada's trade deficit widened to $2.5 billion in November (previously $1.6 billion) as the 5.8% rise in imports outpaced the 3.7% gain in exports. In real terms, the picture was worse, with import volumes up 5.0% and export volumes rising 0.6%.

The rise in imports was widespread, with nearly all industries reporting gains. Leading the way was metal ores and non-metallic minerals (+28%), aircraft and other transportation equipment and parts (+19%) and electronic and electrical equipment and parts (+11%). The only industry in which imports declined during the month was energy products (-3.6%).

Export gains were also fairly broad based, led by a rebound in motor vehicle and parts (+15%) which had fallen in the previous four months. Consumer goods (+7%) also had a strong showing in November, rising to the highest level seen in nearly a year. However, in volume terms, exports excluding autos were soft, falling 1.4%.

Canada's trade surplus with the U.S. slid to $3.3 billion in November (previously $3.5 billion), as the rise in exports (+5.4%) trailed that of imports (+6.5%). Canada's trade deficit with the rest of the world widened to $5.9 billion (previously $5.0 billion) as imports were up 4.4% and exports were down 1.4%.

Key Implications

This was a disappointing report, but unlikely the start of a trend. The strength in imports is suggestive of a return to normality in previously disrupted sectors such as autos. Still, the outperformance of imports versus exports means that net trade will act as a drag on growth during the month, and the decline in export volumes ex-autos is not very encouraging.

Going forward, the outlook for Canada's trade picture remains bright. A healthy US economy and a loonie sitting at around the 80 US cent level should keep demand for Canadian exports propped up, helping net trade support overall growth in the coming months. The biggest risk facing exporters is the ongoing NAFTA renegotiations, which have yet to make much progress.

The Bank of Canada may be disappointed in this report, but it is more than offset by this morning's spectacular employment report, which points to a labour market with little slack. As such, after this morning's releases, the Bank will be inclined to move interest rates higher sooner rather than later.

U.S. Economy Creates 148K Jobs in December and 2.2 Million in 2017 as a Whole

U.S. payrolls rose by 148k in December, disappointing survey expectations for 190k. Private-sector hiring expanded by 146k, below the consensus for 193k. Government payrolls edged up by 2k.

Goods-producing employment rose strongly in December, up 55k and led by a 30k gain in construction employment. Manufacturing employment also did well, rising by 25k. Services employment, on the other hand, decelerated to 91k from 176k in November.

Revisions were relatively minor, subtracting 9k from payrolls in November and October on net. However, the pattern of growth was reversed with November revised up (to 252k from 228k) and October revised down (to 211k from 244k).

The unemployment rate was unchanged at 4.1% in November. Household survey employment rose 104k, while the labor force expanded by 64k.

Average hourly earnings were up a relatively strong 0.3% in December and accelerated to 2.5% year-over-year (from a downwardly revised 2.4% in November).

For 2017 as a whole, the U.S. economy created just under 2.2 million jobs (December to December) slightly above its 2016 performance of 2.1 million. The unemployment rate fell 0.6 percentage points (from 4.7% last December), double the pace of decline in 2016.

Key Implications

The headline may have disappointed, but 148k jobs is a respectable rate of job growth for an economy at this stage of the cycle. As the labor market approaches full employment, analysts will have to adjust down the rate of job growth the economy can achieve. Maintaining a pace of 150k jobs a month would still be sufficient to put downward pressure on the unemployment rate.

Indeed, the challenge in 2018 will be how to continue to add jobs when there are fewer people looking for them. The low unemployment rate should mean faster wage growth as employers offer higher compensation in order to attract and retain talent. They will have more room to do so with the cut in the corporate tax rate.

Still, the rise in pay for those joining and staying in the labor force may not be immediately apparent in aggregate wage data, offset in part by slower wage growth among older worker and the replacement of retiring workers at the top of the pay scale with those joining at lower entry level wages. Ultimately, this may keep the focus on the underlying consumer inflation rate. Should it remain stubborn, the Fed is likely to continue to let the labor market run hot.

U.S Job Growth Slows While Canada Job Numbers Explode

US Job Growth Slows in December

- The U.S economy added +148k in December, almost all of them in the private sector (Previous +239k vs. +193k e).

- The U.S service sector deeply hit.

- Well below the 2017 monthly average of +171k jobs added but is enough to keep up with population growth and chip away at unemployment.

- The labor-force participation didn't budge in 2017 despite the +2m jobs added. Participation rate stands at +62.7% in December.

- The average hourly paycheck for private sector workers grew +2.5% in 2017. That suggests the labor market still has some slack despite the low unemployment.

- Hourly wages grew +9c , or +0.34%, in December from a month earlier.

- U.S yield curve 2/10 see a 'bull' flatter being priced in at +49 bps

Market reaction sell the USD (€1.2059, £1.3564, ¥113.34) and buy U.S treasuries.

Canadian Job Numbers explode

This morning's strong data would likely increasing pressure on the Bank of Canada (BoC) to hike interest rates much sooner than the market has being calculating. Odd's for a Jan hike next week are currently trading at +50%.

The CAD is up +0.88% at C$1.2369

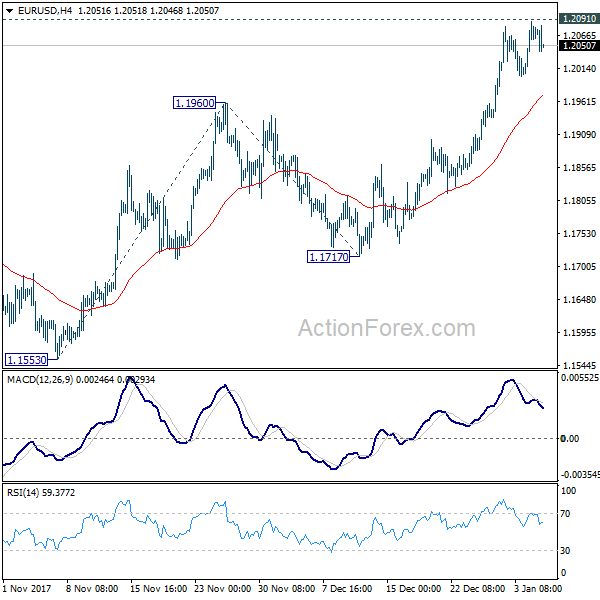

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2018; (P) 1.2053 (R1) 1.2102; More....

Intraday bias in EUR/USD remains neutral at this point. Further rise is expected as long as 4 hour 55 EMA (now at 1.1969) holds. Firm break of 1.2091 will confirm medium term rally resumption and target next key fibonacci level at 1.2494/2516. However, sustained break of 4 hour 55 EMA will extend the consolidation pattern from 1.2091 with with another decline through 1.1717 support.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.