Sample Category Title

EUR/NZD 4H Chart: Going Down

The large scale situation on the EUR/NZD pair has not changed. However, there has been one notable development, as the pair has formed a new medium term channel down pattern.

The channel has guided the pair down to touch the 1.68 mark, and the decline is likely going to continue. The reason for that is the fact that the pair has passed a strong support cluster from the 1.6930 to 1.6870 levels.

As that cluster has been passed, the next notable support level is located below the 1.67 mark, where a long term 61.80% Fibonacci retracement level is located at.

EUR/GBP 4H Chart: Breaks Support

The situation on the EUR/GBP has not changed. There is no real need to change the already drawn medium and large scale patterns. Although, there is a reason why a review is done.

The currency exchange rate has broken the support of a long term channel up pattern. The passing of the support was already expected, as the pair had bounced off the resistance of a more dominant channel down pattern.

Meanwhile, in regards to the short term one can observe that the pair is being kept flat by the weekly PP and will likely remain so until the resistance of the medium scale channel down pattern will force it

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 31 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 25 Aug 2017

• Trend bias: Near term up

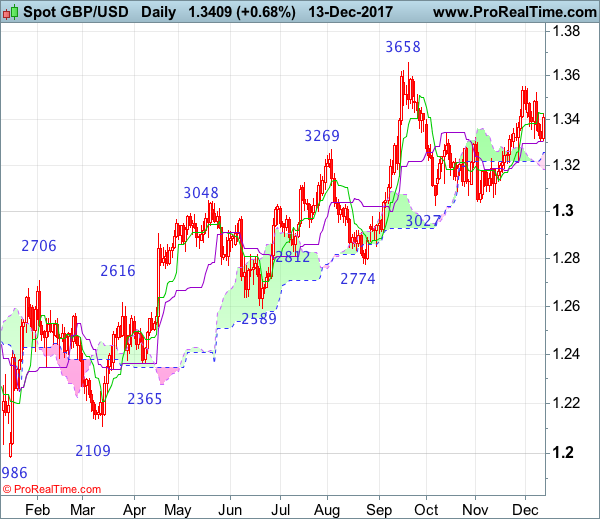

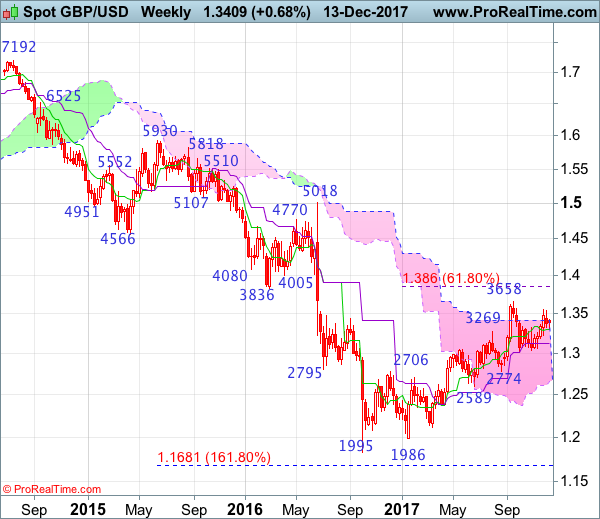

GBP/USD – 1.3445

Although the British pound found support at 1.3303 and has staged a strong rebound, if our view that a temporary top formed at 1.3550 is correct, upside would be limited to 1.3490-00 and price should falter well below said recent high, bring another retreat, below 1.3340-45 would bring retest of 1.3303 but break there is needed to add credence to this view and extend the corrective fall from 1.3550 for weakness to 1.3260-70, having said that,only a daily close below indicated support at 1.3221 retain bearishness, bring further fall to 1.3185-90 and later towards 1.3130 but sharp fall below there should not be repeated and price should stay above previous support at 1.3062.

On the upside, whilst initial marginal gain from here cannot be ruled out, reckon upside would be limited to 1.3500 and said resistance at 1.3550 should remain intact. Only a break above this recent high would abort and signal the rise from 1.3027 has resumed instead, bring further subsequent headway to resistance at 1.3596, however, still reckon upside would be limited and price should falter below another previous chart resistance at 1.3658 (this year’s high).

Recommendation: Hold short entered at 1.3460 for 1.3260 with stop above 1.3560.

On the weekly chart, although sterling slipped initially this week to 1.3303, as cable continued finding good support just above the Tenkan-Sen (now at 1.3295), suggesting further consolidation would be seen, however, still reckon upside would be limited to 1.3500 and price should falter below recent high at 1.3550, bring another retreat later, below said support at 1.3303 would add credence to our view that top has possibly been formed, bring further fall to support at 1.3221, once this level is penetrated, this would add credence to this view, bring further fall to 1.3130 and later towards strong support at 1.3062. Looking ahead, only a drop below 1.3027 support would revive bearishness and signal top has indeed been formed at 1.3658, bring a stronger correction of early rise to 1.3000, then towards support at 1.2909.

On the upside, expect recovery to be limited and 1.3500 should hold, bring another retreat later. Above recent high at 1.3550 would shift risk back to the upside and extend the rise from 1.3027 to 1.3600, then test of last month’s high at 1.3658, break there would confirm medium term rise from 1.1986 low has resumed for headway to 1.3750-60 and 1.3800 but anticipated overbought condition should prevent sharp move beyond 1.3860 (61.8% Fibonacci retracement of 1.5018-1.1986).

Technical Outlook: AUDUSD Extends Post-Fed Rally After Upbeat Australian Jobs Data

The Aussie dollar extended strong recovery rally from 0.7500 base into fourth straight day on Thursday and broke above key near-term barrier at 0.7653 (05 Dec high).

Fresh bullish extension was triggered by better than expected Australian jobs data (61.6K new jobs added vs 19.2K f/c) while unemployment rate remained unchanged at 5.4%., adding to strong bullish sentiment after Fed disappointment sent US dollar lower across the board.

Bulls are looking for next barriers at 0.7683/90 (55/200SMA’s which formed bear-cross), with break here expected to open way for extension of corrective leg from 0.7500 towards key short-term barriers at 0.7719/29 (base of falling daily cloud / 02 Nov high).

Session low at 0.7626 marks initial support, with dips expected to hold above 0.7600 (30SMA / daily Kijun-sen).

Res: 0.7675, 0.7719, 0.7729, 0.7800

Sup: 0.7641, 0.7626, 0.7600, 0.7587

Technical Outlook: GBPUSD Extends Post-Fed Rally, Eyes Retail Sales / BOE

Cable remains firm on Thursday and extends strong post-Fed rally, breaking above 10SMA (1.3416) which capped Wednesday's rally and generating bullish signal.

Fresh bullish acceleration pressures barrier at 1.3455 (Fibo 61.8% of 1.3549/1.3302 downleg) and break hear would further encourage bulls for probes above 1.3500 and possible extension towards 1.3549 (01 Dec peak).

Daily studies are entering full bullish mode and being supportive for further advance, with downside being supported by 4-hr cloud (spanned between 1.3415 and 1.3385).

UK retail sales and BOE policy decision are key events for sterling today.

Retail sales are forecasted to rise in November (benchmark m/m 0.4% f/c vs 0.3% in Oct, core 0.5% f/c vs 0.1% in Nov), with release upbeat release expected to further boost pound.

Conversely, sterling could be deflated on retail sales miss.

The Bank of England is going to announce its first policy decision after raising rates last month for the first time in more than a decade.

Wide expectations are for unchanged policy on today's meeting, with much slower pace of tightening expected from BOE, compared to US Federal Reserve.

Investors will be also looking for BOE's stance about Brexit, which is mostly expected to stay neutral.

Res: 1.3455, 1.3491, 1.3520, 1.3549

Sup: 1.3415, 1.3385, 1.3368, 1.3305

Technical Outlook: EURUSD Probes Above Daily Cloud In Extension Of Post-Fed Rally, ECB In Focus Today

The Euro probes above daily cloud top (1.1823) in early Thursday's trading, in attempts to extend previous day's strong rally (the biggest one-day gains since Nov 24) after Fed disappointed investors. The US central bank increased interest rates by quarter point to 1.5% as expected, but left the outlook for 2018 unchanged. Investors had strong expectations for Fed's more aggressive approach to the monetary policy in 2018 but the central bank opted for the initial decision which includes three rate hikes next year. The dollar was sold-off after the announcement, boosting its major counterparts. The EURUSD pair cracked key near-term barrier, provided by cloud top, reinforcing bullish signal generated on daily close above 1.1810/21 (Fibo 38.2% retracement of 1.1961/ 1.1717 downleg/20SMA). Fresh bulls show hesitation at cloud top which could result in extended consolidation, before resuming higher as are firmly bullish and daily techs turning into full bullish setup. Sustained break above daily cloud will be firm bullish signal for extension of recovery leg from 1.1717 towards targets at1.1867/78 (Fibo 61.8%/lower tops of 04/05 Dec), with stronger acceleration to probe above 1.1900. Double-bottom which formed on daily chart (1.1712/17, 21 Nov / 12 Dec lows) underpins the advance. Today's focus turns towards the ECB's policy meeting. The European central bank is expected to point at improving economic growth but will likely stick to its ultra-low rates and asset-buying program for some more time, in order to lift stubbornly low inflation.

Res: 1.1843, 1.1867, 1.1878, 1.1903

Sup: 1.1823, 1.1810, 1.1797, 1.1773

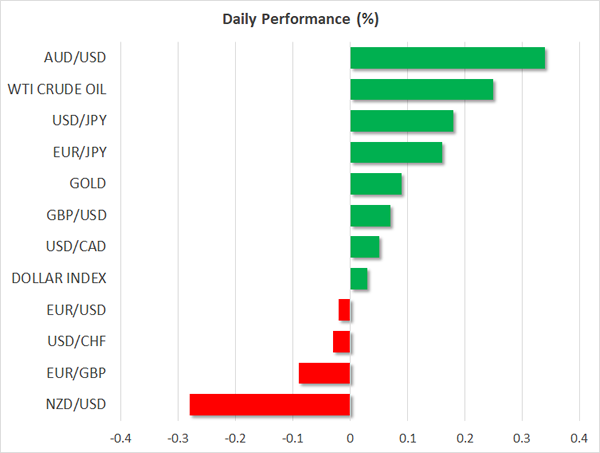

Jobs Report Lifts Aussie, ECB And BoE Eyed

Here are the latest developments in global markets:

FOREX: The dollar index was little changed after recording sharp losses the previous day as investors expected a more hawkish rate outlook by the Federal Reserve. The aussie was on a positive footing versus the greenback after better-than-anticipated employment figures.

STOCKS: The Nikkei 225 finished lower by 0.3% and the Hang Seng was last down by 0.3%; most major Asian benchmarks headed lower though losses were limited. Euro Stoxx 50 futures traded lower by 0.3% at 0713 GMT, with contracts on the Dow, S&P 500 and Nasdaq 100 all being up 0.1%.

COMMODITIES: WTI and Brent crude traded higher by 0.3% and 0.6%, at $56.76 and $62.79 a barrel respectively. Yesterday’s weekly EIA report showed a bigger-than-anticipated drawdown in US crude oil inventories. Gold was slightly higher at $1,256.80 an ounce. The precious metal gained on the back of dollar weakness yesterday, adding 1.0% on the day.

Major movers: Dollar consolidates losses; aussie maintains positive momentum after upbeat employment figures

The dollar’s index against a basket of currencies was marginally higher as European traders were about to get on their desks to begin their trading day. Still, the gauge was not far above 93.33, a one-week low tracked earlier. The US currency suffered losses as the Fed maintained its projections for three more interest rate increases in 2018 and 2019; market participants were anticipating a more hawkish stance. The 25 bps interest rate hike that was expected was of course delivered to drive the fed funds rate to a range of 1.25-1.50%.

Core inflation figures coming in below expectations yesterday also acted as a drag on the greenback, casting additional doubts on whether inflation would soon rise to the Fed’s target of 2% – it should be mentioned that the US central bank though uses the core PCE measure as its gauge for inflation. Not everything was negative for the dollar though, as Congressional Republicans arrived at a deal on final tax legislation on Wednesday, with a vote expected next week.

Dollar/yen was higher by 0.2% at 112.73. Yesterday the pair lost 0.9%. Euro/dollar and pound/dollar were not much changed, consolidating yesterday’s gains that saw the pairs move above the 1.18 and 1.34 handles respectively. Earlier in the day, euro/dollar touched a one-week high of 1.1843.

Aussie/dollar was up by 0.3%, trading not far below 0.7674, the one-month high it hit earlier on the day. Australia’s currency was supported by positive data on employment released during the Asian session. Unlike the aussie, the New Zealand dollar didn’t manage to maintain momentum from previous days. Kiwi/dollar was down by 0.3% at 0.7000, though it still traded relatively close to its highest since late October tracked yesterday.

Besides the Fed, the Chinese central bank also slightly raised rates for its reverse repos and medium-term lending facility, though reaction in the markets to the decision was fairly limited.

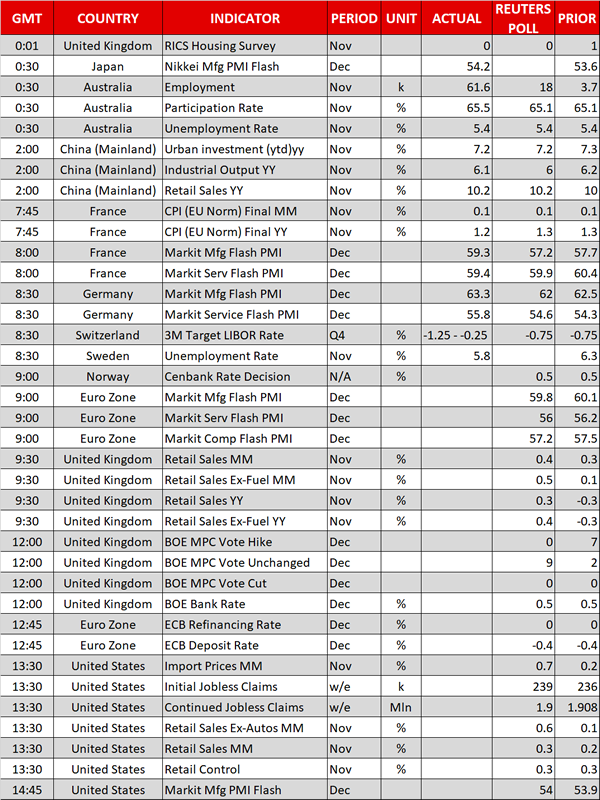

Day ahead: European central banks decide on rates; US & UK retail sales attract attention

Traders are expected to have a relatively busy day at the office on Thursday as several economic reports out of the US, the UK and the EU will be published, while central bank events would be in the spotlight, with the Bank of England, the European Central Bank, the Norges Bank and the Swiss National Bank making announcements on interest rates and publishing their economic projections.

The Bank of England will be the first in line among its European peers to reveal its rate decision at 1200 GMT. Despite inflation crossing far above the BOE’s target of 2.0%, expectations are for rates to remain flat at 0.50%. However, the markets will be looking forward to the monetary policy statement to identify any updates on the BoE’s plans to tighten monetary stimulus in the coming years.

At 1245 GMT the European Central Bank is anticipated to hold benchmark interest rates unchanged and confirm its decision to halve its asset purchases starting next year. As this is widely expected, investors’ focus would turn to the central bank’s macroeconomic projections on economic growth and inflation. The ECB will likely revise up its growth forecasts, while it will also deliver initial 2020 estimates. Following the decision, the ECB chief Mario Draghi will be holding a press conference at 1330 GMT.

The Swiss National Bank and Norway’s central bank are also completing their meetings on monetary policy today.

In terms of data, Eurozone flash Markit PMI readings for the month of December due at 0900 GMT are forecasted to appear slightly weaker than in November, with the composite index sliding by 0.3 points to 57.2. In contrast, first estimates on the US manufacturing and service PMIs are expected to inch up (1445 GMT).

British and US retail sales are expected to surprise to the upside. Particularly, consumers’ spending in the UK due at 0930 GMT is anticipated to rise by 0.3% y/y in November after falling for the first time in four years, while the monthly US gauge is projected to climb by an equivalent percentage.

In addition, initial jobless claims out of the US will be available at 1330 GMT, with analysts projecting the number of people claiming unemployment benefits to increase moderately by 3,000 in the week ending December 8 to 239,000.

Elsewhere, the Bank of Canada’s chief Stephen Poloz will give a speech at the Canadian Club of Toronto at 1740 GMT. A press conference would follow.

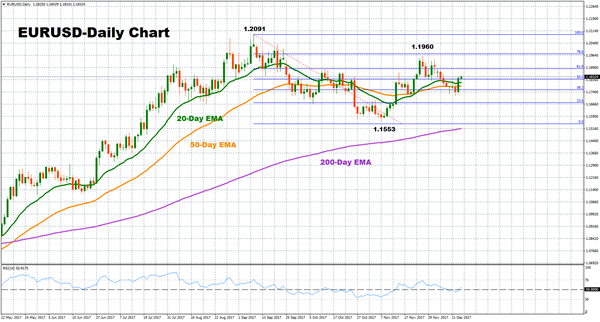

Technical Analysis: EURUSD consolidates gains but short-term risks tilted to the upside

EURUSD is currently neutral as it has been ranging around the 1.1800 key-level over the last four days. However, the bullish cross between the 20 and the 50-day exponential moving average lines as well as the RSI starting to slope upwards may signal that upside movements could emerge in the near-term.

Should the pair head up, immediate resistance could be found at 1.1882, this being the 61.8% Fibonacci mark of the downleg from 1.2091 to 1.1553. Further increases could also target a previous peak at 1.1960. However, if the ECB delivers a dovish message on the eurozone’s economic outlook, prices could decline. In this case, the area around the current level of the 20-day EMA 1.1799 could provide support – notice that price action is currently taking place not far above this level.

(SNB) Swiss National Bank Leaves Expansionary Monetary Policy Unchanged

The Swiss National Bank (SNB) is maintaining its expansionary monetary policy, with the aim of stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB is to remain at –0.75% and the target range for the three-month Libor is unchanged at between –1.25% and –0.25%. The SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration.

Since the last monetary policy assessment, the Swiss franc has weakened further against the euro and, more recently, has also depreciated against the US dollar. The overvaluation has thus continued to decrease, yet the franc remains highly valued. The depreciation of the Swiss franc reflects the fact that safe havens are currently less sought after. However, this development is still fragile. Therefore, despite the easing of the situation, the negative interest rate and the SNB's willingness to intervene in the foreign exchange market as necessary remain essential. These measures keep the attractiveness of Swiss franc investments low and thus ease pressure on the currency. A renewed appreciation would still be a threat to price and economic developments.

The new conditional inflation forecast for the coming quarters is higher than it was in September. This is mainly due to increased oil prices and the further weakening of the Swiss franc. The longer-term inflation forecast is virtually unchanged. For the current year, it has risen marginally to 0.5%, from 0.4% in the previous quarter. For 2018, the SNB anticipates an inflation rate of 0.7%, compared to 0.4% last quarter. For 2019, it continues to expect inflation of 1.1%. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon.

The past few months have seen further improvements in the international environment. The global economy exhibited strong, broad-based growth in the third quarter. The SNB expects it to continue developing favourably in the quarters ahead. The growth forecasts for the euro area and the US have been revised upwards slightly compared to the previous baseline scenario. While the normalisation of monetary policy gradually continues in the US, monetary policy in the euro area and Japan remains highly expansionary. In Switzerland, GDP grew in the third quarter at an annualised 2.5%. Growth was primarily driven by manufacturing, which benefited from dynamic economic developments abroad and the weaker Swiss franc. In the wake of this development, capacity utilisation in the economy as a whole increased further. The unemployment rate declined again slightly through to November.

Given the supportive global environment and favourable monetary conditions, the recovery in the Swiss economy looks set to continue in the coming months. For 2018, the SNB expects GDP growth of around 2%, compared to 1% in the current year.

Imbalances on the mortgage and real estate markets persist. While growth in mortgage lending remained relatively low in 2017, residential property prices rose again slightly. In the residential investment property segment, the strong price growth continued. The SNB will continue to monitor developments on these markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.

USDJPY Under Increased Downside Pressure After Drop Below 50-Day MA

USDJPY has come under increased downside pressure after sharply reversing a recent rally from the 111 to 113 handle.

Near-term momentum has stalled as can be seen by the RSI which did not fall to far below the 50 line. USDJPY has consequently stabilized near the mid-112 handle. But additional weakness cannot be ruled out since the pair dropped below the 50-day moving average.

The odds for a further decline are not that high for now as long as momentum has stalled but unless USDJPY can reclaim the 113 handle soon then there is scope for prices to move lower and target the area between the 200-day MA (111.66) and the key 111 level.

The level at 111 is a major one and is expected to offer strong support but if it fails to hold then a deeper move down would set USDJPY on the path toward the 108-area at the lower end of the longer-term range that the market has been trading in during the past nine months.

Overall, risk is tilted to the downside in the near term. Only a break above key resistance at 113 would ease immediate downside pressure and shift the focus back to 114.

GBPUSD Now Bullish Above 1.3400 Level

The British pound has broken back above the 1.3400 level against the U.S dollar, after the FOMC monetary policy decision. The U.S dollar dropped across the board, after it was revealed that FOMC voting Members Neil Kashkari and Charles Evans dissented against hiking U.S rates in December. The GBPUSD pair now trades around the 1.3430 mark, after breaking back above the key 1.3400 level. Traders now await the release of UK Retail Sales, and the Bank of England interest rate decision and monetary policy statement.

The GBPUSD pair remains intraday bullish while trading above the 1.3400 technical level, upside resistance is now found at the 1.3470 and 1.3520 levels.

Should price-action on the GBPUSD pair fall below the 1.3400 technical level, downside support is seen towards the 1.3380 and 1.3340 levels.