Sample Category Title

USD Slips As Fed Hikes Rates

The much anticipated FOMC meeting concluded yesterday with the Federal Reserve hiking interest rates by 25 basis points. At the meeting, the central bank's projection for rate hikes next year was in line with market expectations. The Fed projected three rate hikes for 2018 and two rate hikes for 2019. The rate hike yesterday saw two dissenting votes from Evans and Kashkari.

In the UK, the monthly labor market data showed that the UK's unemployment rate was unchanged at 4.1% but wage growth continued to remain weak in comparison to the the inflation.

Looking ahead, a busy day on the economic calendar is marked by central bank meetings from the Swiss National Bank, European Central Bank and the Bank of England. No monetary policy changes are expected from either of the central bank meetings making the forward guidance key in anticipation of future policy actions.

In the U.S. the monthly retail sales numbers will be released with forecasts pointing to a strong rebound in retail sales. The flash manufacturing and services PMI numbers are also expected today followed by BoC Gov. Poloz's speech.

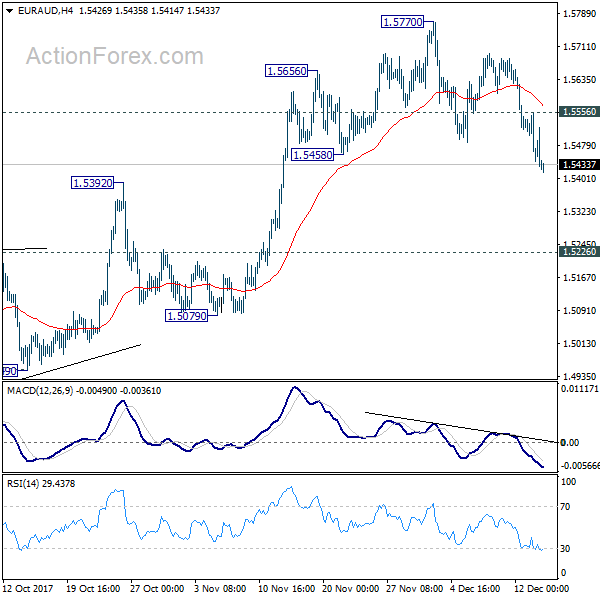

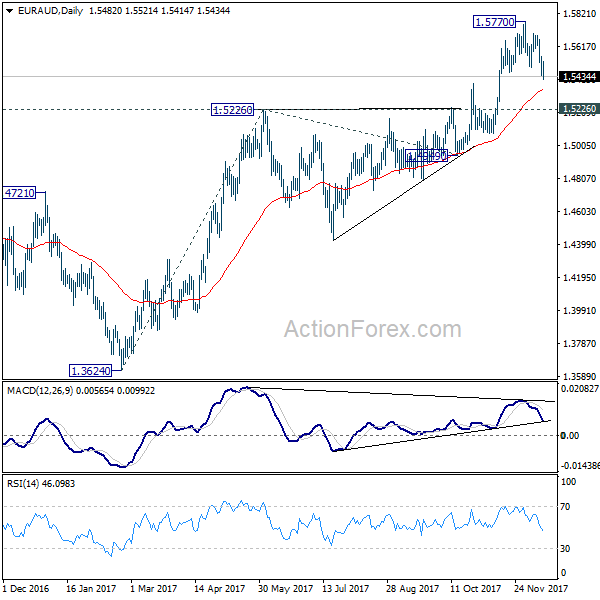

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5430; (P) 1.5493; (R1) 1.5546; More....

EUR/AUD's correction from 1.5770 is still in progress and would extend lower. But at this point, we'd still expect downside to be contained above 1.5226 key support to bring rally resumption. Above 1.5556 minor resistance will turn bias to the upside for 1.5770. Break there will resume the medium term rise and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, sustained break of 1.5226 will carry larger bearish implications and turn outlook bearish.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

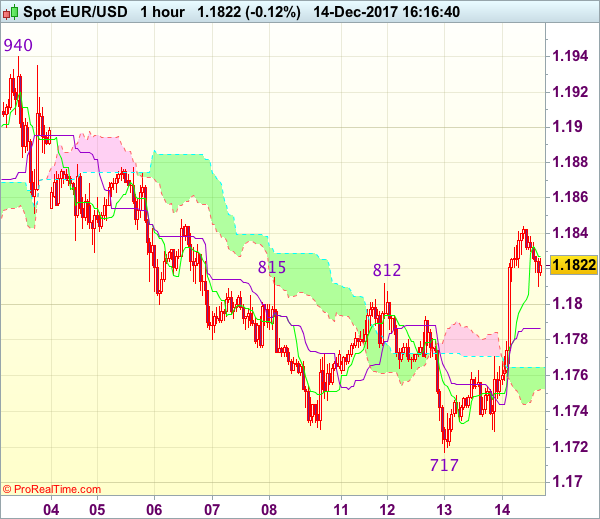

Trade Idea : EUR/USD – Exit short entered at 1.1835

EUR/USD - 1.1720

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1827

Kijun-Sen level : 1.1787

Ichimoku cloud top : 1.1765

Ichimoku cloud bottom : 1.1752

Original strategy :

Sold at 1.1835, Target: 1.1735, Stop: 1.1870

Position : - Short at 1.1835

Target : - 1.1735

Stop : - 1.1870

New strategy :

Exit short entered at 1.1835,

Position : - Short at 1.1835

Target : -

Stop : -

The overnight strong rebound due to dollar’s broad-based weakness after Fed suggests a temporary low has been formed at 1.1717, hence consolidation with mild upside bias is seen and gain to 1.1860, then 1.1880 cannot be ruled out, however, near term overbought condition should prevent sharp move beyond 1.1900 and price should falter well below resistance at 1.1940, bring retreat later.

In view of this, would be prudent to exit short entered at 1.1835 and stand aside in the meantime. Below the Kijun-Sen (now at 1.1787) would suggest an intra-day top is formed instead, bring weakness to 1.1750 but break of 1.1735-40 is needed to revive bearishness and signal the rebound from 1.1717 has ended, bring retest of this level.

Currencies: Dollar Declines Even As Fed Continues Policy Normalization

Sunrise Market Commentary

- Rates: Sell-on-upticks in Bund and US Note future

Today's eco calendar heats up with EMU PMI's, US retail sales and the ECB meeting. We expect data to remain strong, while upward GDP/CPI projections by the ECB could draw investors' attention. Those factors are negative for core bonds. Especially when taking into account yesterday's Fed message. The Fed is willing to continue its tightening cycle unabatedly. - Currencies: Dollar declines even as Fed continues policy normalization

A soft US core CPI and a Fed decision in line with expectations caused a reposition (decline) in US yields and weighed on the dollar. Positive Fed forecasts and decent US retail sales shouldn't be that bad for the dollar, but the ECB forecasts are a wild card.

The Sunrise Headlines

- US stock markets lost some (Nasdaq) to all (S&P) intraday gains going into the close. Asian risk sentiment is mixed overnight with China and Japan underperforming. China's central bank nudged up money market rates.

- The Fed showed continued optimism about the US economy in voting to raise short-term interest rates for the third time this year (to 1.25%-1.5%), and signalling it would stay on a similar path next year amid a leadership transition.

- Theresa May suffered her first major legislative defeat, after pro-European Conservatives backed a move insisting that parliament has a full vote on any Brexit deal before ministers begin implementing it.

- The highest-earning Americans will get a lower tax rate and corporations will pay slightly more than in previous plans under a deal House and Senate Republicans reached on the party's competing tax-overhaul bills.

- Banks are pushing for an eleventh-hour reprieve for a key part of new European markets rules (Mifid II) because about a fifth of their clients do not have the vital tag they will need to continue trading.

- China's retail sales (10.2% Y/Y) and investment growth (7.2% Y/Y) held basically steady in November as a slight uptick in state-led spending continued to help prop up overall investment heading into the close of 2017.

- Today's eco calendar contains the preliminary reading of the EMU December PMI's, the US retails sales, import prices and jobless claims. The UK retail sales are also scheduled for release. Several central Banks will decide on Monetary policy including the ECB, the Bank of England, the Norges Bank and the Swiss National Bank

Currencies: Dollar Declines Even As Fed Continues Policy Normalization

Fed holds course, but dollar declines

USD sentiment deteriorated in US dealings yesterday. Core CPI came out slightly softer than expected and US yields declined, wrong-footing USD longs. The Fed as expected raised its policy rate by 25 bps. Yellen and Co turned more optimistic on the economy. The inflation forecast and median dots on the expected rate path were little changed, but the Fed acknowledged that inflation stays low currently. US yields declined another 4/5 bps after the Fed decision, causing additional intraday USD losses. EUR/USD finished the day at 1.1826 (from 1.1742). USD/JPY closed the session at 112.54 (from 113.55).

Asian equities opened mixed overnight, but gradually ceded ground. Chinese retail sales (10.2% Y/Y), fixed assets sales (7.2%) and industrial production (6.1% Y/Y) all printed very close to expectations. The PBOC raised the rate for some reverserepurchases, confirming its intention to curb (excessive) leverage. The dollar stabilizes after yesterday's setback. EUR/USD trades in the 1.1825 area. USD/JPY is changing hands in the 112.60 area. It is too early to call a USD bottoming, but the US currency isn't losing any further ground. Australian November labour market data were strong. AUD/USD jumped to the mid 0.76 area, reaching the highest level in more than a month.

Today's eco calendar is well filled. Preliminary EMU PMI's are expected to have eased slightly, but will indicate ongoing strong growth. The ECB will leave its policy unchanged. The updated growth and inflation forecasts will dominate the market reaction. Growth forecasts will probably be revised higher. Markets will also keep a close eye at the inflation forecast at the end of the forecasting period. How close will the inflation forecast come to the 2.0% target? If the target is seen within reach, it might cause a repositioning on EMU interest rate markets and support the euro. US data are interesting too. Headline retail sales are expected at 0.3% M/M, the control group sales are forecast at 0.4 % M/M. We don't have much reason to take a different view from consensus. Yesterday, the dollar made a step backward on slightly softer US core CPI. The Fed maintaining its normalisation path was not enough to support the dollar. We assume that the decline in US yields and in the dollar was mostly profit-taking/a squeeze in a market that was positioned short US bonds and that raised USD longs in the run-up to the Fed. Given yesterday's Fed forecasts, we don't see a big case for a significant further USD decline from here

However, the ECB forecasts are a wildcard for euro trading. An upward revision of the growth forecast and inflation nearing the 2% target at the end of the forecast period could propel EMU rates and the euro. So, the EUR/USD rebound might still go a bit further. For now, we assume that the pair will not return to the recent high (1.1961 area). We will reconsider to add EUR/USD shorts once the ECB meeting is out of the way.

Technical picture. EUR/USD set a post-ECB low mid-November, but the USD's momentum wasn't strong enough. EUR/USD settled in a directionless consolidation pattern in the 1.17/19 area. A return below 1.1713 would signal an improvement in the ST USD momentum. Next support comes in at 1.1554 (November low). USD/JPY's momentum deteriorated early November, dropping below the 111.65 neckline. No aggressive follow-through selling occurred though. Over the previous two weeks, the pair rebounded, calling off the downside alert and returning to the 110.84/114.73 range. We amended our ST bias from negative to neutral. We maintain the view that a sustained break north of 115 won't be easy

EUR/USD: USD declines on soft CPI. Fed doesn't help

EUR/GBP

EUR/GBP holds sideways consolidation pattern

EUR/GBP initially hovered in the 0.8810/20 area. The EU Parliament finally approved a Brexit resolution. Sterling gained a few ticks during the morning session. The UK labour data were mixed. UK employment dropped a bigger than expected 56k in the 3 months to October. At the same time, UK wage growth was marginally higher than expected (2.3% ex bonuses). Sterling hardly reacted as the report contained little news for the BoE to change its assessment. Further sterling gains were blocked as UK PM faced more headwinds in the parliamentary vote of the UK Brexit bill. Finally, the UK PM had to concede a bigger role of Parliament in the Brexit process. However, the approval of the amendment had only a limited impact on sterling. EUR/GBP closed the session little changed at 0.8812. Cable rebounded north of 1.3420 on USD weakness.

Today, the UK retail sales are expected to rise a modest 0.4% M/M and 0.3% Y/Y. The BoE will announce its policy decision. We expect them to keep its policy unchanged. Markets will look out whether Carney and Co will strike a slightly more hawkish tone after the recent rise in inflation. We see little room for the BoE to tighten policy as long as real wages remain low/negative. We don't expect the BoE's announcement to provide a lasting support for sterling. Brexit headlines remain a wildcard, but we don't expect any high profile negative news short-term

Recent developments pushed EUR/GBP lower in the 0.8690/0.9033 consolidation pattern. EUR/GBP tested 0.8693 support (62% retracement) on Friday, but the test was rejected. Next support comes in at 0.8653. We assume that the 0.8653/90 area won't be easy to break short-term. We hold a neutral bias on EUR/GBP short-term. We consider a return to the bottom of this range as an opportunity to reduce sterling long exposure against the euro.

EUR/GBP rebounds in the established trading range despite Brexit deal

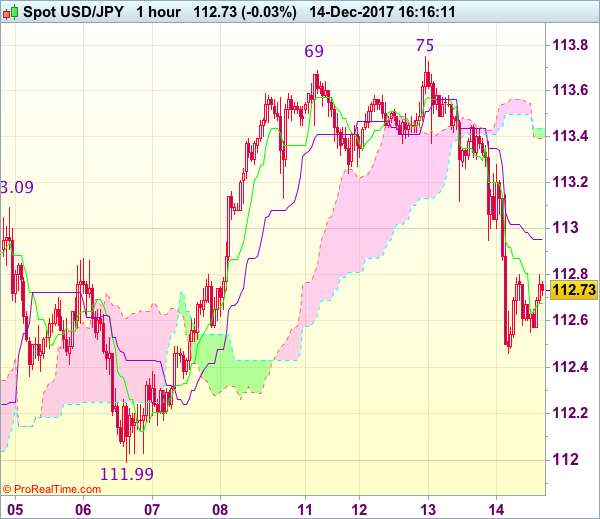

Trade Idea : USD/JPY – Exit long entered at 112.60

USD/JPY - 112.75

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.68

Kijun-Sen level : 112.96

Ichimoku cloud top : 113.44

Ichimoku cloud bottom : 113.39

Original strategy :

Bought at 112.60, Target: 113.70, Stop: 112.25

Position : - Long at 112.60

Target : - 113.70

Stop : - 112.25

New strategy :

Exit long entered at 112.60,

Position : - Long at 112.60

Target : -

Stop : -

Although the greenback recovered after finding support at 112.46, yesterday’s selloff suggests top has been formed at 113.75, hence upside would be limited to the Kijun-Sen (now at 112.96) and downside risk remains for the retreat from 113.75 to extend weakness to 112.30-35, however, near term oversold condition should limit downside and support at 111.99 should remain intact.

In view of this, would be prudent to exit long entered at 112.60 and stand aside in the meantime. Above previous support at 113.12 (now resistance) would suggest low is possibly formed, bring a stronger rebound to 113.40-45 but price should falter below resistance at 113.75 and bring another decline later.

Less Hawkish Fed Drags The Dollar, ECB BoE Next

Fed's decision key takeaways

The Federal Reserve raised its benchmark interest rate by 25 basis points on Wednesday to a target range of 1.25%-1.5%. The central bank also expects higher economic growth from 2018 to 2020 compared to September's projections. They now expect GDP to grow 2.5% in 2018 from 2.1% forecast in September, and 2.1% in 2019 from 2.0%. However, longer term growth expectations were left unchanged at 1.8%, suggesting that tax reforms will only have limited impact on the economy. On another positive note, the Fed expects the unemployment rate to fall to 3.9% in 2018 and 2019, from an earlier forecast of 4.1%.

Despite the interest rate hike and the upgraded economic growth projections, the dollar fell instead of rising. Here's why:

The Fed remained concerned about inflation which continued to undershoot its target. This led to two policymakers Charles Evans and Neel Kashkari dissenting against the decision to tighten policy.

Many economists expected that tax reforms would lead to higher interest rates in 2018, and 2019. However,the Fed's Dot Plot remained unchanged- projecting three rate hikes for 2018 and two for 2019.

The sharp fall in Treasury bond yields suggests that investors were expecting more hawkishness from the Fed, particularly in terms of interest rates projections for 2018.

Given that Charles Evans and Neel Kashkari, the current voting members, will be replaced by Loretta Mester and John Williams next year, we are likely to see a more hawkish Fed. However, it won't be until March 2018 that we get additional guidance from the Federal Reserve which will be led by the new Chair Jerome Powell.

ECB & BOE

The European Central Bank and Bank of England are due to announce their last monetary decisions for 2017 later today. While no significant changes are expected in terms of interest rates or asset purchases, marketscould still move with the publishing of ECB's new economic forecast.

Given that the ECB cut its asset purchase program in October to €30 billion from €60 billion, I don't expect anything new on this front. However, the Eurozone's economy has seen broad improvement in many key economic indicators. GDP growth, employment, retails sales, consumer confidence, manufacturing and services PMI, & core consumer prices, all improved from the last meeting. This should be reflected in the staff's forecast on GDP growth and probably inflation. Draghi's tone however, will be the key driver for the single currency. Despite the improvement in data, his tone has remained dovish for the past couple of meetings. Any hawkish surprise will lead to strength in the Euro, as it signals a shift in policy for 2018.

The BoE will continue to be overshadowed or influenced by Brexit talks. Theresa May's defeat yesterday, in a key vote which gave the Parliament a legal guarantee to vote on the final Brexit deal with Brussels, will likely complicate the BoE's view on Brexit. However, the improvement in economic data and a surge in inflation above 3% might pressure the central bank to tighten policy further in 2018. Any hints of rate hikes next year will boost Sterling, although I expect more information will be provided in February 2018 when the BoE updates its economic forecast.

Fed Raises Rates, Maintains Normalization Path

- Fed raises the fed fund target range by 25 bps to 1.25%/1.50% as expected

- The Fed expects the economy to expand at a moderate pace and labor market conditions to remain strong

- Governors expect stronger growth and lower unemployment in 2018/19

- Inflation expectations and the path of expected rate hikes are little changed

- US yields and the dollar cede ground after the Fed's policy announcement

- US equities stay close to record levels.

Fed 2018/19 rate path unchanged

The FOMC, as expected, raised its Fed funds target range by 25 basis points to 1.25%-1.50%. Two Fed members (Evans and Kashkari) dissented, preferring unchanged rates at this Fed meeting. The run-off of the Fed's balance sheet will continue as set out in the September policy decision. For now this process develops in the background, as the Fed intended it to be.

The Policy assessment on the economy was little changed from the November statement. The Fed repeated that despite hurricane-related fluctuations, job gains have been solid and that the unemployment rate declined further. Household spending is expanding at a moderate pace. Growth in business fixed investment has picked up in recent quarters. The Fed couldn't but acknowledge that overall inflation and inflation other than food and energy have declined this year and are running below 2%.

The median forecast of the FOMC showed a mixed picture. Expectations for economic growth were revised higher and the unemployment rate is expected to decline more than previously anticipated. The projections for inflation and the median value for the Fed fund target rate were little changed compared to the September forecast.

Median forecasts for the unemployment rate were revised further downward from 4.1% to 3.9% for 2018 and 2019. The median forecast for growth was revised slightly higher in particular for next year. The median Fed forecast for 2017 was raised to 2.5% (from 2.4%), for 2018 to 2.5% (from 2.1%) and for 2019 to 2.1% (from 2.0%). Fed governors still see the long run growth rate at 1.8%. So, the Fed sees a good chance for the current economic cycle to last a bit longer than anticipated earlier.

Fed chairwoman Yellen said at the press conference that the impact of the tax reform was highly uncertain. She said it could raise aggregate demand and have a (moderately?) positive impact on supply. However the Fed chair also aired some concerns on rising debt levels. On financial stability, she said she didn't see a worrisome build-up in credit or leverage. Noting is flashing red or orange on financial stability.

Yellen gave an ‘interpretation' on the recent flattening of the yield curve. The Fed Chair doesn't see this flattening of the curve as a precursor of a recession. In the past, an inverted yield curve was the result of short-term rates rising well above average expected rates over the longer term, meaning that monetary policy had become restrictive. This is currently not the case. This time, the flattening of the yield curve is due to the time premium of LT yields to remain stubbornly negative as investors don't see any upcoming risks that would push yields higher.

Changes in the median inflation forecast and the forecast of the expected rate path were less pronounced than for growth and, to a lesser extent, unemployment. The expected path for the (core) PCE deflators was unchanged from September with inflation expected to rise to 1.9% in 2018 and to 2% in 2019 and 2020.

Despite a divergent picture on activity indictors on the one hand and price indicators on the other hand, the Fed governors basically left expectations for the Fed rate path unchanged. The median forecast for the Fed fund rate target still stands at three rate hikes in 2018 and two rate hikes in 2019. The median forecast for 2020 was slightly upwardly revised, indicating at least one additional rate hike in 2020 (median 3.1%) bringing the Fed rate at time well above the LT equilibrium rate (2.75%).

Conclusion: the Fed expects the economic recovery to stay well on course in 2018 and to decelerate more slowly in 2019. Even at that time growth remains above the LT trend. At the same time inflation remains modest, but the Fed still maintains the view that mainly transitory factors are holding inflation low. Over time, growth and a further decline in unemployment will contribute to inflation returning to target

Markets react soft to Fed decision

The market reaction to the Fed rate decision and the new Fed forecasts was modest. On bond markets, the repositioning that started after the publication of the November CPI data, yesterday afternoon, continued. US government bond yields declined another 4 to 5 bps with the belly of the curve slightly outperforming. The implied market probability of a March Fed rate hike declined from about 65% to 56%.

The loss of interest rate support weighed on the dollar. EUR/USD rebounded further from the 1.1775 area to close the session at 1.1826. USD/JPY broke below the 113 handle. US equities tried to extend gains immediately after the Fed decision. The S&P almost exactly touched the intraday record peak, but a sustained new upleg/break failed. US indices closed the session little changed (S&P) to modestly higher (Dow and Nasdaq).

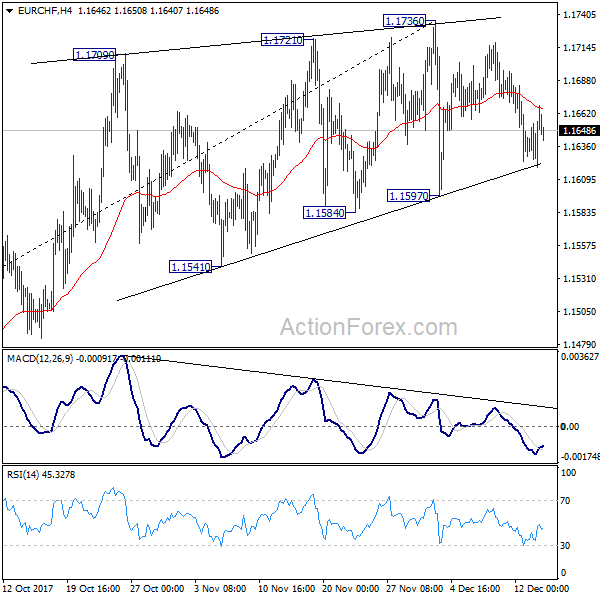

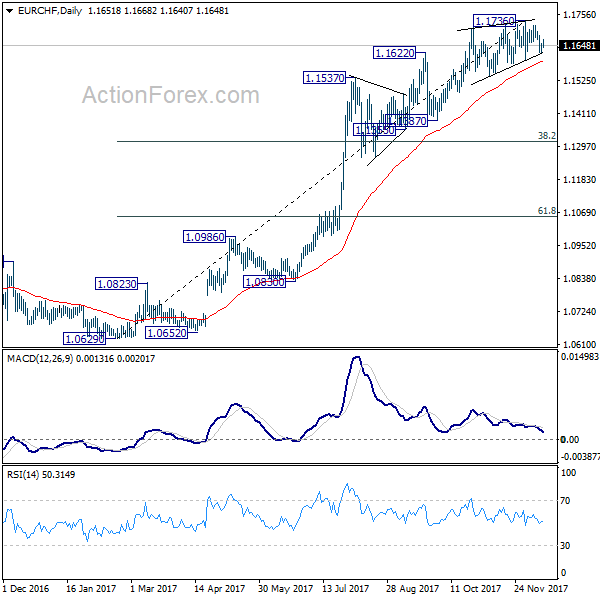

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1625; (P) 1.1641; (R1) 1.1668; More...

Intraday bias in EUR/CHF remains neutral first. We maintained the view that EUR/CHF is close to topping, if not formed. This is supported by persistent bearish divergence condition in 4 hour MACD, and rising wedge like structure. On the downside, break of 1.1597 support will will be a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

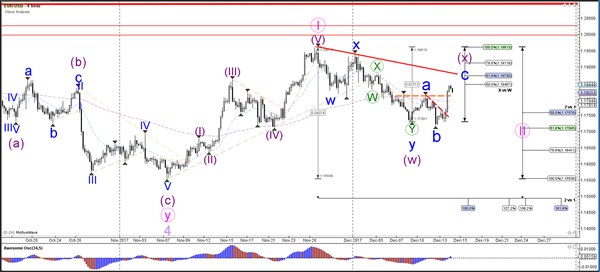

Daily Wave Analysis: EUR/USD Bullish Wave 4-5 Could Test 1.19 Resistance

Currency pair EUR/USD

The EUR/USD broke above the resistance trend lines (dotted) as expected in yesterday's analysis as price expands a potential wave C (blue) within wave X (purple). A bearish bounce at the resistance trend line (red) could indicate an expansion of wave 2 (pink) whereas a bullish breakout could indicate that wave 2 is completed. Today's EUR interest rate could impact price action, volatility, and the direction of the currency pair.

Today's EUR interest rate could impact price action, volatility, and the direction of the currency pair.

Currency pair GBP/USD

The GBP/USD also bounced at support and broke above resistance trend line (dotted orange), which could be part of a wave 4 (brown).

Today's GBP interest rate could impact price action, volatility, and the direction of the currency pair.

Currency pair USD/JPY

The USD/JPY broke below the support trend line which makes a bullish wave pattern unlikely at this point. A bearish variation has bee added which shows a wave WXY (pink) within a larger wave 2/B (light purple).

The USD/JPY could be building a wave A (purple). A break above the 61.8% Fib invalidates a wave 4 (blue).

Last Night’s Fed Meeting Turned Out Rather Uneventful

Market movers today

We do not expect the ECB to make any changes to its policy stance or forward guidance at the meeting today. Focus will therefore be on news regarding QE composition after the scale down and the updated ECB growth and inflation projections, where we expect the new 2020 forecast to show headline inflation close to the target at 1.8% target , in line with the Governing Council's growing urge t o move on wit h monetary policy normalisation.

Euro area PMIs for December are also released due to be today and we look for a small decline in manufacturing and services PMI to 59.5 and 55.7, respectively, in line with a decline in the leading order-inventory balance.

We also have the Bank of England (BoE) meeting today, where we expect the BoE to stay on hold. It is one of the small meetings without updated project ions or a press conference; focus will hence be on the statement and minutes for any hints on the beginning of a hiking cycle.

The two-day EU summit starts today, where EU leaders will have to decide whether sufficient progress has been made to enter phase 2 of the Brexit negotiations. This seems likely given the deal st ruck between the EU and UK government last week.

In Scandinavia, we also have a busy schedule with November housing data in Sweden and Norges Bank meeting (see next page).

Selected market news

Last night's Fed meeting turned out rather uneventful. As expected, the Fed hiked the target range to 1.25-1.50% and kept the dot signal broadly unchanged. While two of the dovish FOMC members dissented (Evans and Kashkari), they are losing their voting rights next year. There were also no major changes in the statement. We think the Fed meeting was on the soft side. While most FOMC participants have incorporated some fiscal stimuli from tax reforms into their forecasts, the dots plot were broadly unchanged, as inflation continues to disappoint the Fed. For more details, please see FOMC review: Broadly unchanged Fed signal, 13 December.

Yields lower, dollar weaker. Taking its cue from the slightly soft outcome of the Fed meeting, as well as core CPI figures that showed a decline to 1.7% y/y (from 1.8%), the yield on 10-year US Treasuries fell by 6bp during the day to 2.34%. Meanwhile, the EUR/USD rose some 0.7% to levels above 1.18.

In the UK, the UK government lost an important vote last night in the House of Commons. Tory rebels backed an amendment , which promised the MP s a ‘meaningful vote' on the final Brexit deal as suggested by the opposition. While the amendment in itself does not mean much in our view (as it is difficult to say what a ‘meaningful vote' even means in this situation), it is a reminder t hat t he minority government is weak and PM Theresa May's posit ion has weakened.