Sample Category Title

Elliott Wave View: Dow Future Intra-Day

Dow Future Short Term Elliott Wave view suggests that the decline to 23205 ended Intermediate wave (4). Intermediate wave (5) is in progress as an Ending Diagonal Elliott Wave structure where Minor wave 1 ended at 24536 and Minor wave 2 ended at 24073. The Index has broken above Minor wave 1 at 24536 which suggests the next leg higher has started.

Near term, rally from 24071 low remains active as 5 waves impulse Elliott Wave Structure and expect a little more upside before Minute wave ((i)) ends. Afterwards, Index should pullback in Minute wave ((ii)) in 3, 7, or 11 swing to correct cycle from 12/7 low (24071) before the rally resumes. We don’t like selling the pullback and expect Index to find buyers in Minute wave ((ii)) pullback in 3, 7, or 11 swing as far as pivot at 24071 low stays intact.

YM_F Dow Future 1 Hour Elliott Wave Chart

FOMC Hikes Rate For Third Time, With Two Dissents

The greenback got dumped, as a result of a series events happened over the past day. Defeat of GOP Roy Moore in the Alabama Senate race and the miss of the core CPI were followed by a final version of tax bill. The day culminated in the conclusion of the FOMC announcement, which saw a 25 bps rate hike as expected, but with two dissents. US dollar fell against major currencies with the DXY index losing -0.71% for the day. Treasuries firmed, sending yields higher with the 2-year and 10-year yields dropping -4 points and -5 points respectively.

Alabama Senate Race

Democrat Doug Jones surprising won the Alamaba special election with 671 151 votes (49.9%), defeating GOP Roy Moore with just about 20K votes. This is the first time that Republican lost the seat in the state in 25 years. The outcome has further shrunk the Republican’s slim majority in the Senate to only two votes. The Democrat has urged the Senate majority leader to delay the vote of tax bill until after Jones has worn in.

Final Tax Bill

On the other hand, the House and Senate leaders have eventually agreed on the final version of the tax plan. It is reported that the controversial corporate tax rate would be lowered to 21%, compared with 20% preliminarily proposed. Yet, the reduction would take effect in 2018, compared with Senate’s proposal of 2019. Meanwhile, the top income tax rate would fall to 35% from 39.5%. It is unlikely that the Republican would agree to delay the vote as the Democrat requested. The final bill would be voted in the House and Senate next week.

Core CPI Missed Expectations

Headline CPI steadied at +2.2% y/y in November. While this came in line with expectations, the core reading surprisingly missed consensus (of +1.8%) and eased to +1.7% y/y, from +1.8% in October. Inflation outlook remained positive, though with both a three-month and six-month rate at +1.9%.

FOMC Announcement

The November inflation data did not affect the Fed’s monetary decision. Policymakers, as expected, hiked to policy rate, by +25 bps, to the 1.25-1.5% range in December. However, the decision was made with Neel Kashkari and Charles Evans (both are doves) dissenting. The fed also upgraded the economic outlook, raising GDP growth forecasts and lowering the unemployment rate for the next year. Inflation would likely stay below the +2% target for the coming year. Note that the Fed has incorporated the impacts of the tax reform bill in its forecasts. Meanwhile the median dot plot continued to project three rate hikes next year but just over two in 2019.

There were a few changes in the accompanying statement. For instance, policymakers reiterated that core inflation'declined this year' and 'running below 2%', but removed the language of 'remained soft'. On the job market, they noted that it would remain 'strong', compared with previous description of 'some further strengthening' in the labor market condition. This might imply reduced need for tightening.

On the updated economic projections, GDP growth was revised higher to +2.5% in 2017, +2.5% in 2018 and +2.1% in 2019, from +2.4%, +2.1% and +2% respectively. The longer-term forecast stayed unchanged at +1.8%. Unemployment rate was revised lower to 4.1% in 2017, 3.9% in 2018 and 2019, and 4% in 2020, from 4.3%, 4.1% and 4.2%, respectively. The longer-term unemployment rate stayed unchanged at 4.6%. On inflation, the PCE inflation stayed unchanged all over the Fed’s forecast horizon, at 1.9%, 2%, 2% and 2% in 2018, 2019, 2020 and the longer run respectively.

The decision to raise the policy rate was again not unanimous. Kashkari’s dissent was expected as he also dissented against a rate hike in June. Evans, however, was not used to dissenting despite his usual dovish stance. Yet, both voted for the last time as the regional Presidents rotate next year. The new composition of the FOMC voting members remains uncertain. This is certainly something that one should pay attention to.

On the monetary policy outlook, the median dot plot projects three rate hikes next year and just over two in 2019. The 2020 projection edged higher by almost 1 more increase, while most participants forecast the terminal rate to exceed the neutral rate.

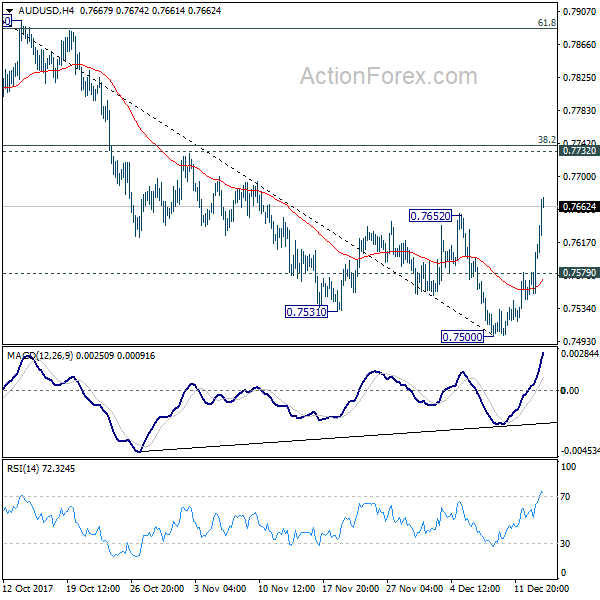

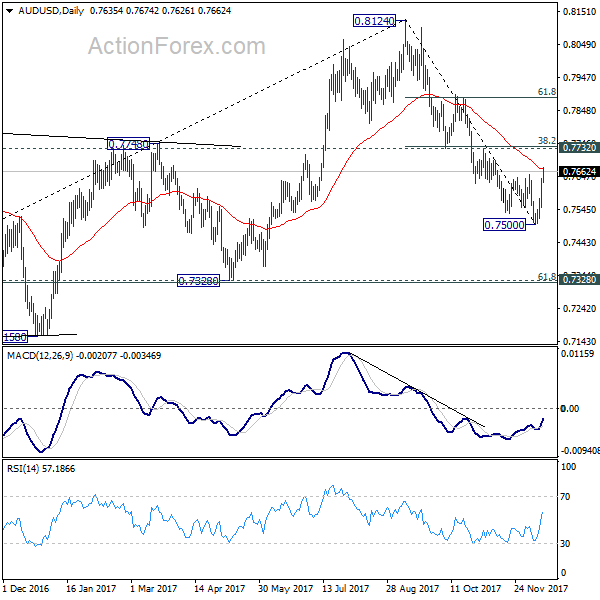

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7579; (P) 0.7609; (R1) 0.7666; More...

AUD/USD's strong rebound and break of 0.7652 indicates short term bottoming at 0.7500, on bullish convergence condition in 4 hour MACD. Intraday bias is now on the upside for further rise. However, we'd expect strong resistance from 0.7732 cluster resistance (38.2% retracement of 0.8124 to 0.7500 at 0.77385) to limit upside to bring fall resumption. Below 0.7579 minor support will turn bias to the downside for 0.7500 and believe. However, sustained break of 0.7732 should invalidate our bearish view and bring stronger rise through 61.8% retracement at 0.7886.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8029). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

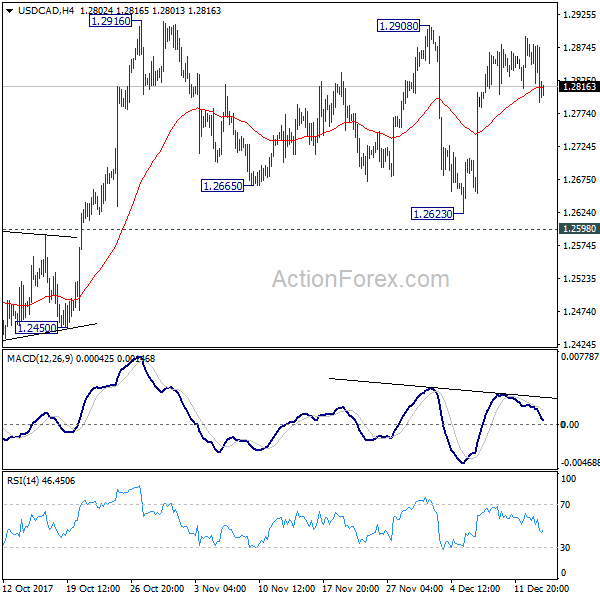

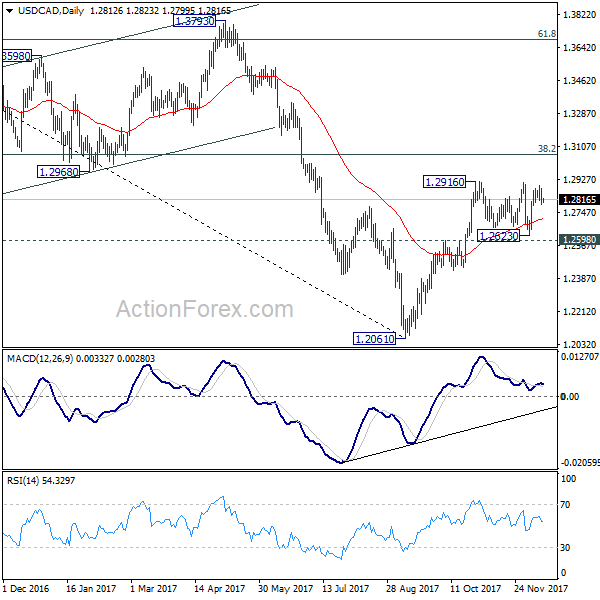

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2776; (P) 1.2828; (R1) 1.2865; More....

USD/CAD is staying in range below 1.2916 and intraday bias remains neutral first. On the upside, firm break of 1.2916 will resume whole rally from 1.2061 and target 1.3065 medium term fibonacci level next. In case of another fall, we'd expect strong support from 1.2598 to contain downside and bring rebound. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2888). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

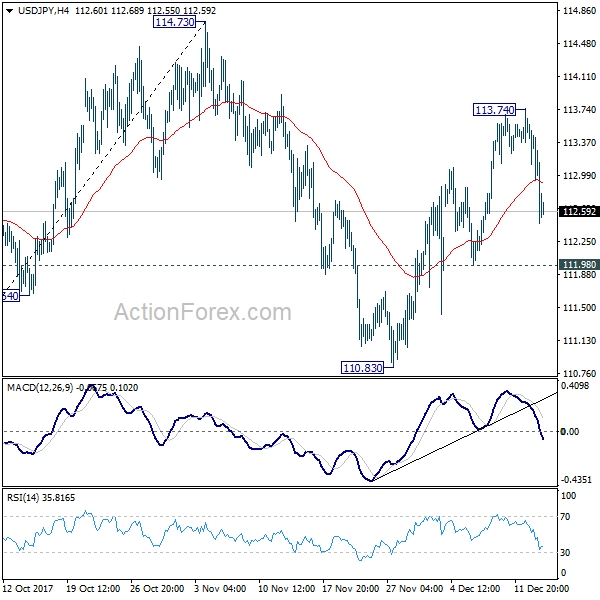

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.13; (P) 112.85; (R1) 113.25; More...

USD/JPY's pull back from 113.74 extended lower but it's kept well above 111.98 minor support. Intraday bias remains neutral and such decline is still seen as a correction. As noted before, as long as 111.98 support holds, further rally is expected in the pair. On the upside, above 113.68 will extend the rise from 110.83 to 114.73 resistance first. Decisive break there will resume whole rise from 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

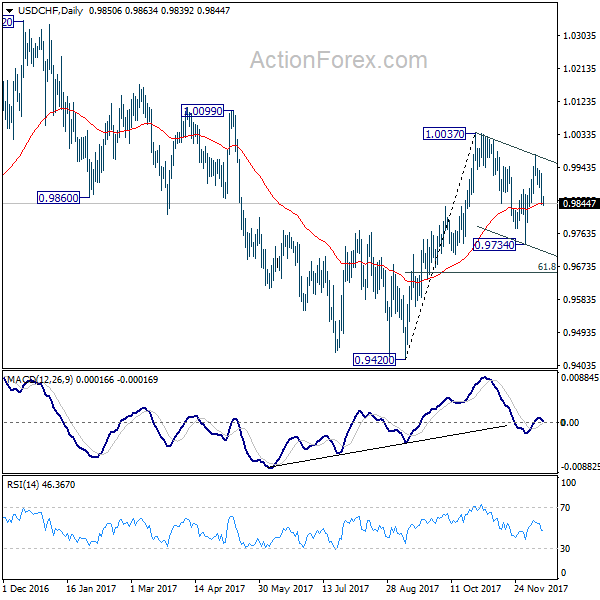

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9821; (P) 0.9874; (R1) 0.9908; More....

Strong break of 0.9981 support suggests that USD/CHF's rebound from 0.9734 has completed at 0.9977 already. Intraday bias is back on the downside for 0.9734 and below to extend the correction from 1.0037. We'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound On the upside, above 0.9895 minor resistance will turn bias back to the upside for 0.9977 instead.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

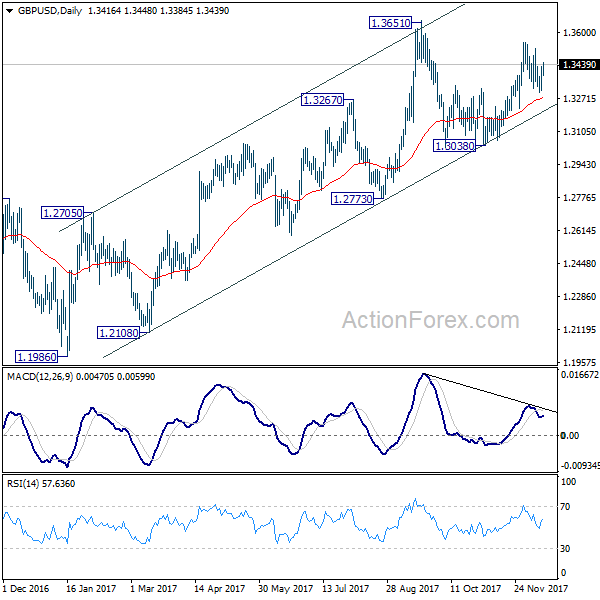

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3342; (P) 1.3384; (R1) 1.3458; More....

GBP/USD recovers on dollar weakness but stays below 1.3549, intraday bias remains neutral first. As long as 1.3220 support holds, we'd continue to favor another rise. On the upside, break of 1.3549 will target 1.3651 high next. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

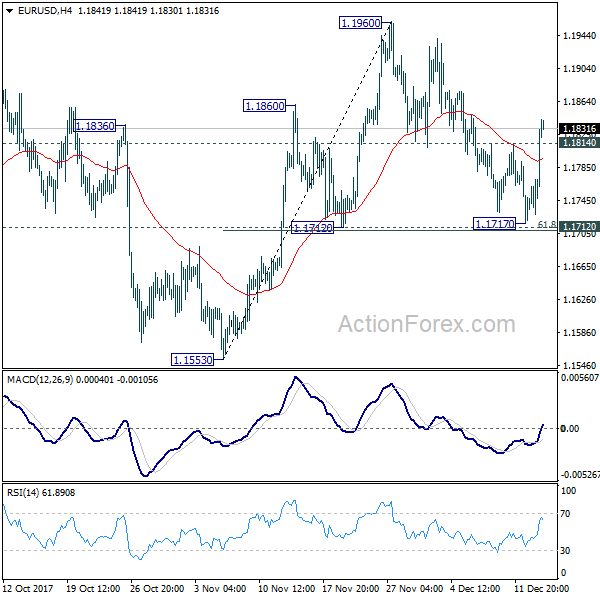

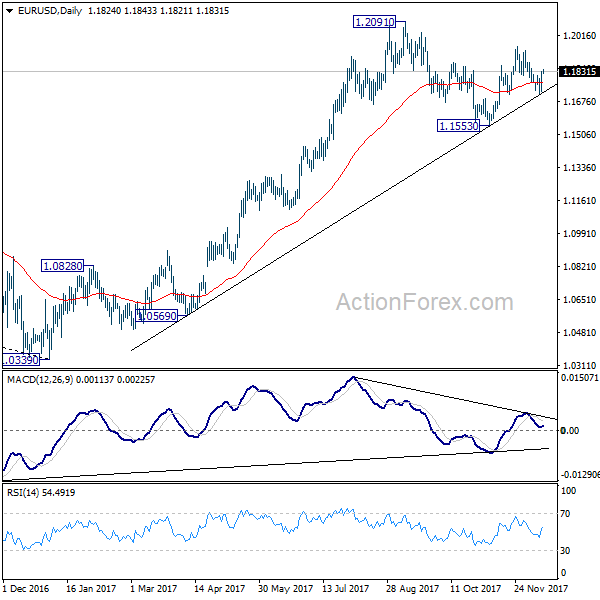

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1759; (P) 1.1795 (R1) 1.1861; More....

EUR/USD's strong break of 1.1814 resistance suggest that corrective pull back from 1.1960 has completed at 1.1717 already. Also, as the pair defended 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708), near term bullish outlook is retained. Intraday bias is back on the upside for 1.1960 first. Break will target 1.2029 high next. And even in case of retreat, outlook will remain bullish as long as 1.1708/12 cluster support holds.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Dollar Stays Weak Despite Fed Hike and Tax Bill, EUR/USD Now Targeting 1.2

Dollar tumbled broadly after FOMC rate hike as most likely an extended selloff after core CPI miss. News on the progress in Republican's tax bill provided little support to the Dollar. Technically, Dollar index should have confirmed the rejection from 94.16 resistance. Equivalently, EUR/USD has defended 1.1712 key near term support. more downside is now likely in the greenback in near term with EUR/USD heading back to 1.1960 and possibly have a go at 1.2 handle before year end. Staying in the currency markets, Aussie is propelled higher by a stunning job report. European majors are generally firm too, ahead of SNB, BoE and ECB rate announcement.

Fed announcement wasn't dovish at all

Fed's announcement overnight wasn't exactly a dovish one. Federal funds rate was raised by 25bps to 1.25% to 1.50% as widely expected. In the new economic projections, GDP forecast for 2018 was raised to 2.5%, up from 2.1%. For 2019, GDP forecast was raised to 2.1%, up from 2.0%. Unemployment rate projections for 2018 and 2019 were lowered to 3.9%, down from 4.1%. Inflation forecasts were kept unchanged. That is, PCE is projected to be at 1.9% at 2018 and 2.0 at 2019. Core PCE is projected to be at 1.9% in 2018 and 2.0% at 2019.

Mostly importantly, federal funds rate projections were also kept unchanged. That is, to be at 2.1% at 2018 and 2.7% at 2019. That's equivalent to more than three more hikes in both 2018 and two to three hikes in 2019. Indeed, for 2020, rate is now projected to be at 3.1%, revised up from September's forecast of 2.9%.

Updated Fed projections

The negative reaction in Dollar was probably firstly due to one more dissenter to the hike. But dissenters Minneapolis Fed President Neel Kashkari and Chicago Fed President Charles Evans are two known doves. And Evans has already hinted in his recent comments that he'd vote "no". So that shouldn't be a surprise to anyone who followed closely. Secondly, there were speculations that Fed could accelerate the path next year to have four hikes. And people were disappointed by the lack of hints for that. Again, given the lack of inflationary pressure, there is little chance for Fed to hit the brake harder than it should be. Three hikes will remain the base case scenario unless there is a clear pick up in inflation. Thirdly, the more probably reason, Dollar was just extending the post CPI selloff as Fed event risks were cleared.

Republicans agreed on 21% corporate tax rate, starts in 2018

Republicans were making important progresses on the tax bill. One of the most sticky topic of corporate tax cut should have been solved. House and Senate Republicans have agreed to cut corporate tax rate from 35% to 21% (instead of 20%), and starts in 2018 (Senate originally wanted it in 2019). Top individual rate is lowered to 38% for the highest earners (down from House 39.6% and Senate 38.5%). The so-called Corporate Alternative Minimum Tax will be repealed (Senate wanted to maintain). Obamacare individual mandate will also be repealed. There could be some more minor issues to resolve. But the bill should be ready for vote before Christmas.

Aussie surges on stunning job data

Australian Dollar surges broadly today after a stunning employment report. The job market grew 61.6k in November, more than triple of expectation of 19.2k. Full time jobs grew 41.9k while part time jobs grew 19.7k. Unemployment rate was unchanged at 5.4% as participation rate jumped from 65.2% to 65.5%. Nonetheless, there is no change in the general view that RBA will stand pat throughout 2018, unless there is a pickup in wage growth. Also from Australia consumer inflation expectation rose 3.7% in December.

Release from China, retail sales rose 10.2% yoy in November, below expectation of 10.3% yoy. Fixed assets investments rose 7.2% yoy, in line with consensus, industrial production rose 6.1% yoy, below expectation of 6.2% yoy.

Busy calendar ahead

The economic calendar is extremely busy today. SNB, BoE and ECB rate decision will be the main focuses. Nonetheless, no change in monetary policy is expected from all of the three. And, BoE has just hiked last month. ECB will start tapering in January. There is little chance of any surprise today. So, these three announcement could be non-events.

On the data front, Eurozone PMIs will be the main focuses while UK will release retail sales. US will release jobless claims, retail sales import price and PMIs later today. Canada will release new housing price index.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1759; (P) 1.1795 (R1) 1.1861; More....

EUR/USD's strong break of 1.1814 resistance suggest that corrective pull back from 1.1960 has completed at 1.1717 already. Also, as the pair defended 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708), near term bullish outlook is retained. Intraday bias is back on the upside for 1.1960 first. Break will target 1.2029 high next. And even in case of retreat, outlook will remain bullish as long as 1.1708/12 cluster support holds.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | Consumer Inflation Expectation Dec | 3.70% | 3.70% | ||

| 0:01 | GBP | RICS House Price Balance Nov | 0% | 0% | 1% | |

| 0:30 | AUD | Employment Change Nov | 61.6K | 19.2K | 3.7K | 7.8K |

| 0:30 | AUD | Unemployment Rate Nov | 5.40% | 5.40% | 5.40% | |

| 2:00 | CNY | Retail Sales Y/Y Nov | 10.20% | 10.30% | 10.00% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Nov | 7.20% | 7.20% | 7.30% | |

| 2:00 | CNY | Industrial Production Y/Y Nov | 6.10% | 6.20% | 6.20% | |

| 4:30 | JPY | Industrial Production M/M Oct F | 0.50% | 0.50% | ||

| 8:00 | EUR | France Manufacturing PMI Dec P | 57.2 | 57.7 | ||

| 8:00 | EUR | France Services PMI Dec P | 59.9 | 60.4 | ||

| 8:15 | CHF | Producer & Import Prices M/M Nov | 0.30% | 0.50% | ||

| 8:15 | CHF | Producer & Import Prices Y/Y Nov | 1.20% | |||

| 8:30 | CHF | SNB Sight Deposit Interest Rate | -0.75% | -0.75% | ||

| 8:30 | CHF | SNB 3-Month Libor Upper Target Range | -0.25% | -0.25% | ||

| 8:30 | CHF | SNB 3-Month Libor Lower Target Range | -1.25% | -1.25% | ||

| 8:30 | EUR | Germany Manufacturing PMI Dec P | 62 | 62.5 | ||

| 8:30 | EUR | Germany Services PMI Dec P | 54.6 | 54.3 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Dec P | 59.7 | 60.1 | ||

| 9:00 | EUR | Eurozone Services PMI Dec P | 56 | 56.2 | ||

| 9:30 | GBP | Retail Sales M/M Nov | 0.40% | 0.30% | ||

| 12:00 | GBP | BoE Bank Rate | 0.50% | 0.50% | ||

| 12:00 | GBP | BOE Asset Purchase Target Dec | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--0--9 | 7--0--2 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0--0--9 | 0--0--9 | ||

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.20% | 0.20% | ||

| 13:30 | USD | Initial Jobless Claims (DEC 09) | 239K | 236K | ||

| 13:30 | USD | Retail Sales Advance M/M Nov | 0.30% | 0.20% | ||

| 13:30 | USD | Retail Sales Ex Auto M/M Nov | 0.70% | 0.10% | ||

| 13:30 | USD | Import Price Index M/M Nov | 0.80% | 0.20% | ||

| 14:45 | USD | US Manufacturing PMI Dec P | 54.2 | 53.9 | ||

| 14:45 | USD | US Services PMI Dec P | 54.6 | 54.5 | ||

| 15:00 | USD | Business Inventories Oct | -0.10% | 0.00% | ||

| 15:30 | USD | Natural Gas Storage | 2B |

Market Morning Briefing: Euro Bounced From Support Near 1.1717

STOCKS

FED hiked interest rates by 25bps as expected. But that has not impacted the Dow much. Dow (24585.43, +0.33%) inched up to test 24666 before closing at slightly lower levels yesterday. We continue to look at important resistance near 24800 and while that holds, Dow could come off sharply from there or trade sideways in the 24800-24000 region in the coming sessions.

13200 seems to be a decent resistance on the Dax (13125.64, -0.44%) for the near term and while that holds, Dax is likely to trade sideways in the 13200-12900 region. Dax is likely to come down below 13100 in the next few sessions. For any further upside, the Dax will have to break above 13200 and sustain in the near term.

Nikkei (22726.76, -0.14%) is trading below resistance near 23000. Note that the index is range-bound within 22200-23000 region and is likely to continue in the same region for a few more sessions. Near term preference would tilt on the downside if the fall in Dollar Yen (112.64) continues in the near term towards 112 or lower.

Shanghai (3292.71, -0.31%) looks bearish for the near term. While immediate support near 3260-3280 holds, we could see some trade within 3260-3320 region in the next few sessions.

Nifty (10192.95, -0.46%) and Sensex (33053.04, -0.53%) are headed downwards and are in the correction phase just now. While Nifty could target 10100, Sensex could move down towards 32750-32500 in the coming sessions.

COMMODITIES

Gold (1256.67) has risen sharply from support levels of 1240 and could be stalled near 1260 for sometime before again rising back towards 1280/90 levels. A pause and probably a corrective dip is possible from levels near 1260.

Silver (16.08) has risen in line with our expectations and could move up towards 16.40-16.60 soon.

Brent (62.81) has come down surprisingly contrary to our view of a rise towards 68. As mentioned earlier, it could find some support in the 61.00-62.00 region from where a bounce back towards 65-66 or higher is possible.

WTI (56.77) has come off sharply too and could test support near 55.50-56.00 before attempting a rise from there. A break below 55, if seen could turn the bulls down and initiate some corrective dips going forward. But before giving any priority to that view, we would wait for any confirmed move below 55.

Copper (3.0575) could face immediate resistance just below 3.10 and while that holds, Copper could come off towards 3 again in the medium term.

FOREX

Dollar-Index (93.387) has retreated from resistance near 94 on the 3 day candles after the expected 25 bp rate hike by the Fed. As mentioned yesterday, the rate hike seems to have been factored in by the market already, which was reflected in the recent uptrend of the Dollar Index towards 94. With the next rate hike expected to happen only in the March FOMC meeting, we might be looking at a period of bearishness in the Dollar. US Retail Sales data (to be out later today) would need to exceed Market expectations of 4.81 % y-o-y growth to provide some strength to the dollar.

Euro (1.1835) bounced from support near 1.1717, with corresponding dip of the Dollar Index (from 94) and can now be expected to embark on a rally in the medium term. In the near term, immediate resistance can be seen near 1.19 which had been tested earlier this month. Euro’s rally could however see it rise past this resistance and move towards higher resistance near 1.25 on the weekly line chart. The ECB meeting today could provide further strength to Euro.

Dollar-Yen (112.62) has fallen in line with the Dollar Index and can now be expected to move towards 112 in the near term with a gradual move towards support at 110 on the weekly candles by next month.

Pound (1.3435) along with the Euro & Yen has seen a rise after the rate hike yesterday. However, we would need to watch the pound in the next couple of sessions to get more directional clarity (whether it will move back down on its downtrend towards support at 1.32-1.3225 on the daily, 3 day and weekly charts, or whether it will test resistance near 1.355-1.3575 on the weekly candles before dipping again.

Rupee (64.30) has opened lower compared to its close at 64.4375 yesterday and with a rally in the Euro & dip in Dollar strength, might well test previously mentioned support near 64.20.

INTEREST RATES

Fed has hiked by 25bp as expected. Now the expected number of increases in 2018 is 3.There were 2 votes against a rate hike and apparently Yellen said that relatively low/ steady inflation is here for some more time. No action is expected in the Jan FOMC meeting. The next one after that is in March, which will be chaired by Powell.

Keep an eye on the ECB meet today. In case Draghi states anything on the EUR-USD view, we could see an impact on the currency pair in the near term.

The US yields are trading low after the FOMC statement. The 5Yr (2.12%), 10Yr (2.36%) and the 30Yr (2.74%) are down from previous levels of 2.17%, 2.40% and 2.78% respectively. The yields could move down for another sessions before bouncing back from supports visible below current levels.

The US-Japan 10Yr (2.31%) came off from resistance but we will have to see if the yield spread is able to come off below 2.28% or continue to trade along the channel resistance for some more time. Only on a sustained break below 2.28%, we would get some fall in Nikkei and Dollar Yen in the near to medium term.

The German-US 10YR (-2.04%) bounced back sharply from -2.09% as expected and could test resistance above current levels soon. Thereafter, another leg of fall could be expected towards -2.10% or lower. All eyes on the ECB meeting today.