Sample Category Title

Chinese Urban Investment, Industrial Output and Retail Sales in Focus; Aussie also Eyed

China will see the release of figures on November fixed asset investment, industrial production and retail sales on Thursday at 0200 GMT. The data are not just important for the world's second largest economy, but also Australia, which has China as its major exports destination.

The annual pace of growth for fixed asset investment in urban areas is expected to stand at 7.2%, reflecting a minor slowdown from October's respective rate of 7.3%. November's industrial output is anticipated to grow by 6.0% on an annual basis, slightly easing from the preceding month's 6.2%, while retail sales are projected to rise by 10.2% y/y, exceeding October's 10.0%.

Should fixed asset investment decline as expected, then this would mark the eighth consecutive month of declines for the measure. It should also be pointed though, that if projections materialize, the reading would still expand at a robust pace.

It should be kept in mind that the slowdown in certain readings in the latter part of the year is coming on the back of government efforts to reduce financial risks as well as curb pollution, with efforts on the latter possibly acting as a drag on industrial output. The reasoning behind such actions is that Chinese authorities are increasingly placing emphasis on the quality of growth rather than merely the quantity; more balanced growth was pledged during the five-yearly Communist Party Congress in October and the first steps to achieve that goal are seemingly being taken. This has the capacity to result in a weaker outlook for growth, but at the same time it would facilitate the sustainability of growth, reducing risks for extreme adverse conditions further ahead.

On the retail sales front, Alibaba's promotions during the so-called "Singles' Day" in November is likely to have acted as the catalyst for the forecasted increase in sales.

Besides movements in the yuan, Australia's strong economic ties with China would place the aussie in the spotlight as the above data become public – the Australian currency is considered a liquid proxy for China's economy.

An upside surprise in the figures could boost aussie/dollar. In such an event, the pair might meet resistance at around 0.7643, this being the 23.6% Fibonacci retracement level of the September 8 to December 8 downleg. Bear in mind, that the area around this mark also encapsulates the December 5 one-month high (0.7653), as well as the current levels of the 50- and 200-day moving averages (0.7671 and 0.7689 respectively).

If the data disappoint though, forex market participants could push the pair lower. In this case, aussie/dollar might find support around the six-month low of 0.7498 that was recorded on December 8.

It should be noted that Australian data on employment (and unemployment) for the month of November due earlier on Thursday (0030 GMT) are likely to act as market movers for the aussie as well.

Soft US CPI Wrong-Foots USD Longs ahead of Fed

- European equity markets lose slightly ground today. US equities futures traded in negative territory as Republicans saw their majority in the Senate reduced to the smallest margin. However sentiment improved again throughout the session. Major US indices opened with gains of 0.2% to 0.4%. S&P and Dow touch new all-time peaks.

- US inflation picked up in November thanks to a jump in energy prices (0.4% M/M & 2.2% Y/Y) yet unexpectedly cooled when excluding food and fuel costs (0.1% M/M & 1.7% Y/Y), which could factor into Federal Reserve discussions this week on how fast to raise interest rates.

- Italian newspaper Messagero reported that the parliamentary vote is scheduled on March 4 and President Mattarella is expected to dissolve parliament on Dec 28 or Dec 29. Based on current polls, the Five Star Movement has an edge over the Pd for first place, but a centre-right coalition could eclipse them both.

- Industrial production in the euro area grew by 3.7% in the year to October after a 0.2% rise on the month. Ireland led the pack for the year, with a rise of 13.4%, while the Netherlands bumped along the bottom with a decline of 0.4%.

- The number of people in work in Britain fell again (-56k), suggesting employers are turning more cautious as Brexit nears. Pay growth quickened slightly (2.3% Y/Y) but it remained lower than inflation. The unemployment rate stabilized at 4.3%.

- The European Parliament urged EU leaders to allow the next phase of EU negotiations to start, backing a motion that recognised that Brexit talks had made sufficient progress-. The motion also included a line criticising Britain's Brexit negotiator Davis.

Rates

Limited short covering after US core CPI miss

Global core bonds currently trade mixed with US Treasuries outperforming German Bunds. Both faced selling pressure at the start of European trading with the Bund being worst off. Technical factors might have been at play as the German 10-yr yield finally bounced off 0.3% support yesterday following an intense, multiday, test. A (small) negative surprise in US core inflation readings convinced some investors to do some last minute short covering ahead of tonight's Fed meeting and caused a U-turn in trading dynamics. US Treasuries record small daily gains at the moment, while the Bund is near opening levels. Stronger than expected, but outdated, EMU industrial production data left no traces.

At the time of writing, the US yield curve drops 1.6 bps (2-yr) to 2.2 bps (5-yr) lower. Changes on the German yield curve vary between -0.7 bps (2-yr) and +0.2 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany widen up to 4 bps with Italy (+7 bps) underperforming and Greece outperforming (-9 bps). The Italian underperformance could be partly due to the starting shot in the parliamentary campaign. Media reported that early parliamentary election will be held on March 4.

The Fed meets today and is expected to hike its policy rate a third time this year by 25 bps to 1.25%-1.5% which is completely discounted in markets. The new "dot plot" will receive most attention. We expect the central bank to stick to its intention to hike rates three times next year. Since September, (rate) markets for the first time this hiking cycle started aligning with the Fed's scenario. Past years, they were positioned much more dovish which proved right in 2015 and 2016. The market implied probability of a next rate hike (to 1.5%-1.75%) in March already stands at 60% with two hikes discounted for 2018. The median rate projection for 2019 has more potential to change. In September, it was 2.688% with 8 governors expecting higher rates and 8 governors expecting lower rates. A small upward shift is possible if governors start factoring in some positive effects from fiscal stimulus. The median growth forecast for next year (2.1%) could also be subject to an upward revision. The impressive sell-off at the front end of the yield curve suggests that some short term profit taking is possible while immediate losses at the longer end of the curve seem more likely given current positioning. In that case, we might see some corrective steepening short term.

Currencies

Soft US CPI wrong-foots USD longs ahead of Fed

The dollar was driven by alternating feelings throughout the day. Initially the greenback held op fairly well even as the Republican party saw its majority in the Senate reduced to the smallest margin. In US dealings, the core US CPI came out slightly softer than expected. US yields declined several basis points, wrong-footing USD longs. EUR/USD trades in the 1.1760 area. USD/JPY tries to hold north of 113. Will the Fed's message be able to change fortunes again in favour of the dollar?

Asian equities opened mixed, but found a better bid later. Most indices ex-Japan and India closed in positive territory. Japan core October machine orders were strong (5.0% M/M), but didn't help Japanese equities. They underperform as USD/JPY declined. The US currency was in the defensive as the Republican party lost the Senate vote in Alabama, reducing its majority in the Senate to a slim 51-49. USD/JPY spiked to the 113.15 area but returned to the 113.40 at the start in Europe. EUR/USD rebounded overnight, trading in the 1.1750/60 area at the European open.

European equities opened with slight losses, but tried to join the Asian positive momentum. However, there was no strong enough driver to support a clear directional move. European investors were maybe a bit uncertain on the consequences of the very narrow majority that the Trump administration will have to cope with going forward. Even so, core yields traded with a slight upward bias as investors counted down to the Fed's policy decision. The dollar remained well bid against the euro but struggled against the yen.

The US CPI report was slightly softer than expected. US November headline inflation rose 0.4% M/M and 2.2% Y/Y (from 2.0%) as expected, but core inflation unexpectedly softened from 1.8% to 1.7%. As such, the miss wasn't that big. However, over the previous days investors gradually adapted positions preparing for a rather hawkish Fed. This build-up became stretched/vulnerable after the softer core inflation. US yields declined up to 5 bps. USD longs were wrong-footed by this unexpected loss of interest rate support. EUR/USD jumped higher in the 1.17 big figure. The pair trades in the 1.1760 area. USD/JPY filled bids just below 113 (currently 113.05). Will the Fed still be able/try to convince markets not to give too much weight to ongoing mediocre inflation data?

Sterling going nowhere. Data give no clear signal

Sterling opened near yesterday's closing levels with EUR/GBP hovering in the 0.8810/20 area. During the morning session, EU's Barnier defended the recommendation to start the second phase of Brexit negotiations before the EU parliament. He warned that the UK should meets its promises, but the tone was less tough than was the case earlier this week. The EU Parliament finally approved a Brexit resolution. Sterling gained a few ticks during the morning session. The UK labour data were mixed. UK employment dropped a bigger than expected 56k in the 3 months to October. At the same time, UK wage growth was marginally higher than expected (2.3% ex bonuses). Sterling hardly reacted as the report contained little news for the BoE to change its assessment. However, the gains of sterling remained limited as the UK government continues to face headwinds in the parliamentary vote of the UK Brexit bill (also from conservatives PM's). EUR/GBP holds near the 0.88 pivot. Cable rebounded to the 1.3360 area, mostly on post-CPI USD weakness.

US: CPI Inflation Trending Higher

The CPI rose 0.4 percent in November as energy prices rebounded. Core inflation was noticeably softer at 0.1 percent, but was held down by weakness in more volatile components like airfare, lodging and apparel.

Firmer Headline Inflation

Consumer price inflation firmed in November with the consumer price index (CPI) rising 0.4 percent. That pushed the year-ago rate up to 2.2 percent compared to 1.7 percent last November.

Headline inflation was lifted by higher energy prices in November. Gasoline prices have typically fallen this time of year, but rose this November leading to a seasonally adjusted gain of 7.3 percent. Food prices, on the other hand, were unchanged. Grocery prices edged down amid lower prices for proteins, beverages and fruits & vegetables, which offset a 0.2 percent increase in the price of food away from home.

Core Inflation Softer on Lodging, Airfare and Apparel

While the headline gain was in line with expectations, the 0.1 percent rise in core inflation was weaker than anticipated. Core services rose 0.2 percent, which marked a slowdown from the previous month. The weaker outturn was in no small part driven by some of the more volatile components of core services, including lodging away from home (down 1.3 percent) and airline fares (down 2.4 percent). Another notable standout, however, was a 0.8 percent decline in physician services, which along with wireless services, was a major contributor to the slowdown in core inflation earlier this year.

After increasing in October, core goods prices fell 0.1 percent. The decline was largely traceable to a 1.3 percent drop in apparel prices - the largest monthly decline in nearly 20 years as holiday discounting looks to have gotten an earlier start this year. In contrast, prices for autos and prescription drugs rose in November.

Pickup in Core Inflation Supportive of More Fed Tightening

Fed officials have been concerned this year about the slowdown in core inflation that began last spring. Core inflation has been picking up on trend, with the three-month annualized rate coming in at 1.9 percent. That should push up the year-over-year rate, which edged back down to 1.7 percent last month. With much of the weakness in November core inflation coming from the more volatile components, we continue to expect inflation to trend higher in the coming months.

Today's FOMC meeting is almost certain to conclude with another 25 bps increase in the fed funds rate. Additional rate hikes in 2018, however, are likely to hinge on further gains in inflation. The Fed's preferred measure of core inflation, the PCE deflator, has reached or surpassed the Fed's 2.0 percent target in only five months of the current expansion, leaving a number of committee members worried about the persistent shortfall. As inflation should more clearly pick up in the coming months, we expect the FOMC will continue on with its gradual pace of tightening in the year ahead.

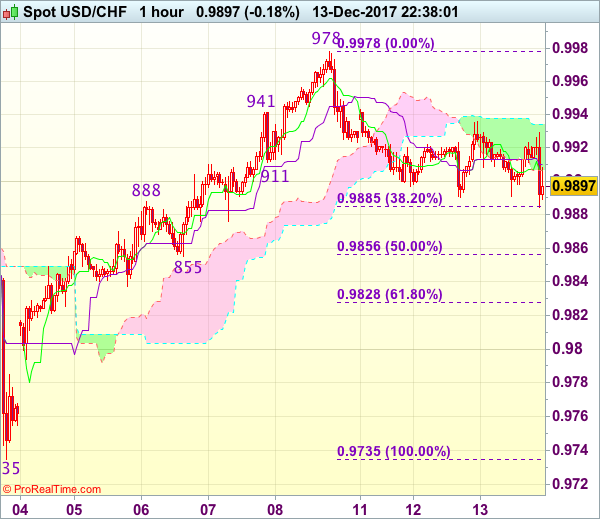

Trade Idea Wrap-up: USD/CHF – Buy at 0.9860

USD/CHF - 0.9902

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9907

Kijun-Sen level : 0.9910

Ichimoku cloud top : 0.9934

Ichimoku cloud bottom : 0.9907

Original strategy :

Buy at 0.9860, Target: 0.9970, Stop: 0.9825

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9860, Target: 0.9970, Stop: 0.9825

Position : -

Target : -

Stop : -

Although the greenback rebounded after holding above support at 0.9890, reckon upside would be limited to 0.9950 and risk remains for another corrective fall to bring retracement of recent rise, however, downside should be limited to 0.9855-60 (50% Fibonacci retracement of 0.9735-0.9978) and bring another rise later, above 0.9950 would suggest the retreat from 0.9978 has ended, bring retest of this level, break there would signal recent upmove has resumed and extend gain to 1.0000 but price should falter below recent high at 1.0038.

In view of this, would not chase this rise here and we are looking to buy dollar on subsequent pullback as 0.9855 support should contain downside. Only below 0.9825-30 (61.8% Fibonacci retracement of 0.9735-0.9978) would abort and signal top has been formed, bring further fall to 0.9800.

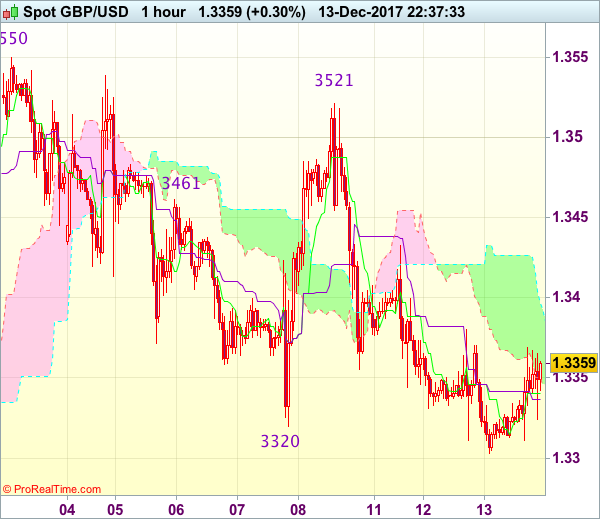

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3375

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.3344

Kijun-Sen level : 1.3340

Ichimoku cloud top : 1.3396

Ichimoku cloud bottom : 1.3350

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has rebounded after falling to 1.3303 yesterday, suggesting consolidation above this level would be seen and corrective bounce to 1.3400 is likely, however, break of indicated resistance at 1.3432 is needed to signal low has been formed there, bring a stronger rebound to 1.3475–80 but still reckon resistance at 1.3521 would hold from here.

In view of this, would not chase this rebound and would be prudent to stand aside for now. Below 1.3320-25 would bring retest of 1.3303, break there would extend the fall from 1.3550 top to 1.3280 and later 1.3250 but price should stay well above previous support at 1.3221.

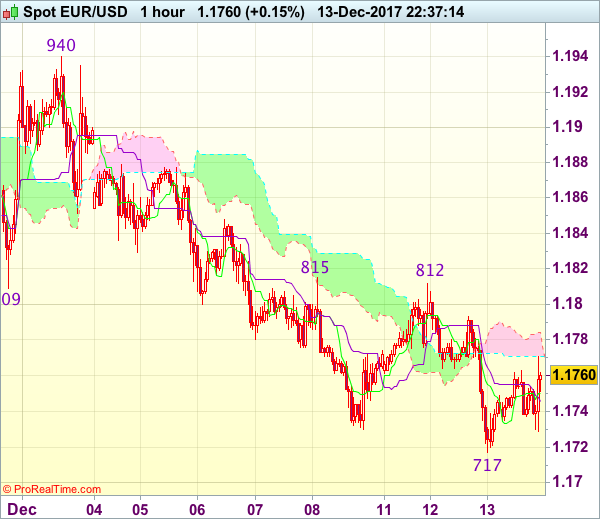

Trade Idea Wrap-up: EUR/USD – Sell at 1.1835

EUR/USD - 1.1754

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1750

Kijun-Sen level : 1.1746

Ichimoku cloud top : 1.1784

Ichimoku cloud bottom : 1.1771

Original strategy :

Sell at 1.1825, Target: 1.1720, Stop: 1.1860

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1835, Target: 1.1735, Stop: 1.1870

Position : -

Target : -

Stop : -

As the single currency rebounded after falling to 1.1717 yesterday, suggesting consolidation above indicated key support at 1.1713 would be seen and corrective bounce to the lower Kumo (now at 1.1771) is likely, however, reckon upside would be limited to resistance at 1.1812-15 and bring another decline later, below said support at 1.1713-17 would extend recent fall from 1.1961 top to 1.1695-00, then towards 1.1660-70.

In view of this, we are looking to sell euro on further subsequent recovery as said resistance at 1.1815 should limit upside and bring another decline. Above 1.1845-50 would defer and suggest low is formed, bring a stronger rebound to 1.1875-80 first.

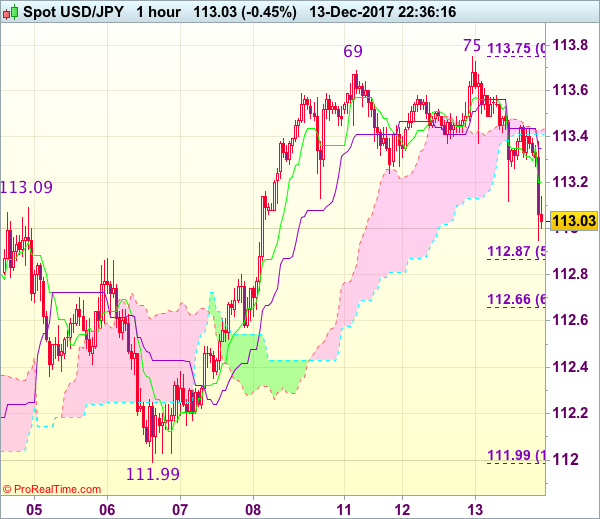

Trade Idea Wrap-up: USD/JPY – Buy at 112.60

USD/JPY - 113.04

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.20

Kijun-Sen level : 113.35

Ichimoku cloud top : 113.43

Ichimoku cloud bottom : 113.41

Original strategy :

Buy at 112.90, Target: 114.00, Stop: 112.55

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.60, Target: 113.70, Stop: 112.25

Position : -

Target : -

Stop : -

As the greenback has retreated after marginal rise to 113.75, suggesting consolidation below this level would be seen and pullback to 112.85-90 (50% Fibonacci retracement of 111.99-113.75 and previous resistance turned support) is likely, however, reckon 112.65-70 (61.8% Fibonacci retracement) would limit downside and bring another rise later, above said resistance at 113.75 would extend recent upmove from 110.84 low to resistance area at 113.91-114.07 but a sustained breach above this region is needed to signal early uptrend has resumed for headway towards 114.34.

In view of this, would be prudent to buy dollar again on further corrective fall as 112.66 (61.8% Fibonacci retracement of 111.99-113.75) would limit downside and bring another rise. Below 112.55-57 support would defer and suggest top has been formed instead, bring subsequent fall to 112.20-25.

US: Core Inflation Pressures Cool in November

Prices rose a healthy 0.4% in November as reported by the headline consumer price index (CPI), which helped to lift total inflation slightly to 2.2% year-on-year, from 2.0% in October.

Three quarters of the price increase was due to energy prices, which rose 3.9% on the month, boosted by a 7.3% jump in the price of gasoline. The overall food index was unchanged for the second straight month in November.

The disappointing part came in core inflation, which only rose 0.1% in November. The year-on-year pace of core inflation slipped a tick to 1.7% in November from 1.8% in October. A 1.3% drop in apparel prices - the largest decrease since 1998 - was a notable weight on core inflation. Airline fares also fell 2.4% on the month. Elsewhere in core inflation, the weighty shelter component rose 0.2% m/m, a tick lower than October as prices for lodging away from home fell 1.3% in November after rising the previous three months.

The slight loss of core inflation momentum was felt in both goods and services. Core goods prices were back in deflationary territory (-0.1% m/m) and are down 0.9% versus a year ago, slightly less negative than the prior month. Core services rose 0.2% m/m, and are up 2.5% versus a year ago. Prices for medical care services were soft in November (-0.1% m/m) after a string of hotter readings.

Key Implications

We remain confident that conditions are ripe for inflation to build in the months ahead, although the process is proving lengthy. No doubt November's inflation data is a setback. But, the sizeable decline in apparel prices is unlikely to be repeated next month, suggesting core inflation will firm once again in December. In an economy with unemployment at a 17-year low, and back-to-back quarters of 3% growth in real terms, conditions are ripe for increased pricing power. Adding to those healthy economic conditions, Congressional Republicans look set to pass a tax cut in the coming days. This will add further to inflationary pressures in 2018.

A rate hike at the FOMC meeting later today was essentially a lock, and November's data isn't weak enough to change that. However, it will provide some fodder for the doves on the FOMC to argue for a gradual pace of rate hikes in the coming quarters. As of the last meeting, the Fed expected to raise rates three times next year, but the "dots" will be watched closely later today to see if the Fed is tempering it's optimism on the pace of rate hikes going forward.

Trade Idea: EUR/GBP – Buy at 0.8755

EUR/GBP - 0.8806

Original strategy :

Buy at 0.8755, Target: 0.8855, Stop: 0.8720

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8755, Target: 0.8855, Stop: 0.8720

Position : -

Target : -

Stop : -

Although the single currency retreated from 0.8847, early strong rebound from last week’s low of 0.8690 suggests low has possibly been formed there and consolidation with mild upside bias is seen for a test of resistance at 0.8868, however, break above there is needed to add credence to our view that low has been made and suggest the decline from 0.9015 has ended, bring further gain to 0.8890-00 later.

In view of this, we are looking to turn long on dips as 0.8755-60 should limit downside and bring another rebound. Below 0.8720-25 would risk retest of 0.8690 but only break there would revive bearishness and signal the fall from 0.9015 is still in progress and may extend weakness to 0.8660-65 and then 0.8640-45.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

U.S. November CPI Rises though Core Inflation Moderates

Highlights:

- Headline CPI rose an expected 0.4% sending the annual rate up to 2.2% from 2.0% in October.

- A 7.3% monthly jump in gasoline prices provided a lion's share of the increase.

- Excluding food & energy prices, 'core' CPI rose 0.1% in the month and 1.7% over the year.

Our Take:

The year-over-year increase in core inflation dropped back down to 1.7% in October. After holding steady at 1.7% four five consecutive months, the rate moved up to 1.8% in October. The increase continues to be constrained by a large drop in telecommunications prices earlier this year and in apparel prices in November. The absence of inflation pressures has been a puzzle with respect to the U.S. economy. Indications, such as a low unemployment rate, are indicative of the economy operating close to capacity. Operating at capacity is usually associated with inflation pressures starting to build with businesses having increased difficulty responding to rising demand because of resource constraints and thus temper demand by raising prices. Today's report provides some confirmation of retailers responding in this expected manner with services prices up 2.6% over the past year. However, it is being offset by lower goods prices. Our expectation is that the growing capacity constraints will increasingly see the price performance of the former dominate with core inflation resuming an upward trend.