Sample Category Title

Markets in Risk-On Mode but Currency Trading Subdued

Markets are generally back in risk seeking mode. Major US indices ended in record highs as DOW gained 0.69% to 23590.83, S&P 500 up 0.65% to 2599.03 and NASDAQ rose 1.06% to 6862.48. Asian markets follow with Nikkei gaining 200 pts in initial trading. Trading in currency markets is relatively subdued in Asian session. For the week, Sterling remains the strongest one follow by commodity currencies. Euro remains the weakest one on political uncertainties in Germany, but loss is, again, limited. Dollar is trading mixed as markets await FOMC minutes. Expectation on the minutes is rather low as they shouldn't reveal anything that alter the chance of a December Fed hike.

Fed Yellen: New normal is really different

Fed Chair Janet Yellen said that inflation staying below the 2% is one of the "biggest challenge". She added that "the issue facing monetary policy at the moment is how to craft a monetary policy that maintains a strong labor market, but also moves inflation back up to our 2% objective." And the so called "new normal" was "really different". Yellen noted that "we have been revising down our estimates [of the neutral rate], and market participants have been doing the same." However, under the new norm, Fed would have left with few tools to respond to another crisis and that is "very dangerous state of affairs."

NAFTA talks ended in frustrations

US Trade Representative Robert Lighthizer expressed his frustration after the fifth round of North American Free Trade Agreement (NAFTA) renegotiation talk with Canada and Mexico. Lighthizer said that he "remain concerned about the lack of headway", and "we have seen no evidence that Canada or Mexico are willing to seriously engage on provisions that will lead to a rebalanced agreement." He warned that "absent rebalancing, we will not reach a satisfactory result." On the other hand, Canadian Foreign Minister Chrystia Freeland said the U.S. put forward "extreme proposals" that "we simply cannot agree to." Freeland warned that "some of the proposals that we have heard would not only be harmful for Canada but would be harmful for the U.S. as well." Mexican Economy Minister Ildefonso Guajardo said "we're prepared to work towards that (rebalancing) goal, provided it doesn't limit Mexico's ability to produce and export."

Near 50% German prefers new election

In Germany, a new poll by INSA for Bild daily showed that 49.9% of German preferred new election, after coalition talks between Chancellor Angela Merkel's CDU/CSU, FDP and Greens collapsed earlier this week. 28% blamed FDP for the failure of talks, but that was closely followed by 27% who blamed Merkel. And, only four out of 10 said Merkel should run again as chancellor in new election. 24% prefer another someone else from CDU. A big question is on whether a new election could change the current deadlock. The poll showed that support of CDU at 30%, SPD at 21%, GDP on 10% and Greens on 11%. That is, the deadlock would remain a deadlock unless the parties adjust their stances.

ECB Coeure: Link between asset purchase and inflation would change

ECB Executive Board member Benoit Coeure said in an interview that "European recovery is the strongest for the last decade, and the broadest for the last two decades." But inflation "remains weak" even through there are "some signs" of picking up. And even in in Germany, "inflationary pressures are surprisingly subdued". And therefore monetary policy needs to "remain accommodative". The end data of the asset purchase program in September 2018 "is still far away" according to Coeure. But the link between asset purchases and inflation would change "at some point between now and September 2018".

On the data front

Australia Westpac leading index rose 0.1% mom in October, construction work done rose 15.7% in Q3. Economic calendar is busy in the US today, with jobless claims, durable goods, and FOMC minutes featured.

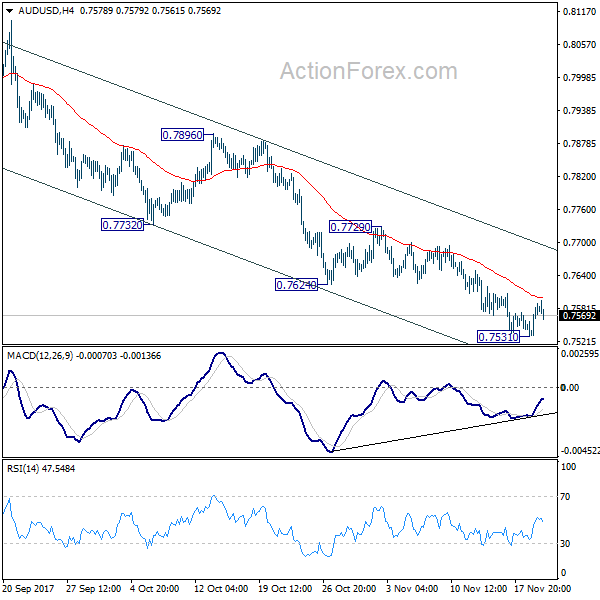

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7543; (P) 0.7566; (R1) 0.7601; More...

A temporary low is in place at 0.7531 in AUD/USD and intraday bias is turned neutral for consolidation. Upside of recovery should be limited below 0.7729 resistance and bring another decline. Break of 0.7531 will resume the whole fall from 0.8124 and turn bias to the downside for next key cluster level at 0.7322/8. However, considering bullish divergence condition in 4 hour MACD, break of 0.7729 will indicate near term reversal and bring stronger rebound back to 0.7896 resistance and above.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8049). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Oct | 0.10% | 0.10% | ||

| 0:30 | AUD | Construction Work Done Q3 | 15.70% | -2.30% | 9.30% | 9.80% |

| 12:30 | GBP | U.K. Chancellor Presents Budget to Parliament | ||||

| 13:30 | USD | Initial Jobless Claims (NOV 18) | 241K | 249K | ||

| 13:30 | USD | Durable Goods Orders Oct P | 0.30% | 2.00% | ||

| 13:30 | USD | Durables Ex Transportation Oct P | 0.40% | 0.70% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Nov A | -0.9 | -1 | ||

| 15:00 | USD | U. of Mich. Sentiment Nov F | 98 | 97.8 | ||

| 15:30 | USD | Crude Oil Inventories | 1.9M | |||

| 17:00 | USD | Natural Gas Storage | -18B | |||

| 19:00 | USD | FOMC Meeting Minutes Nov |

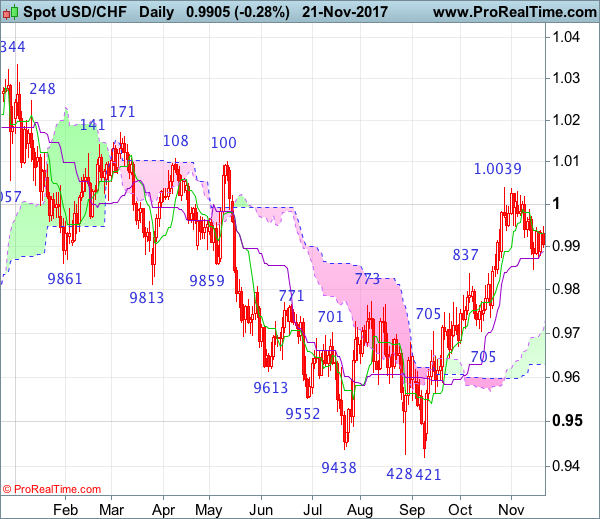

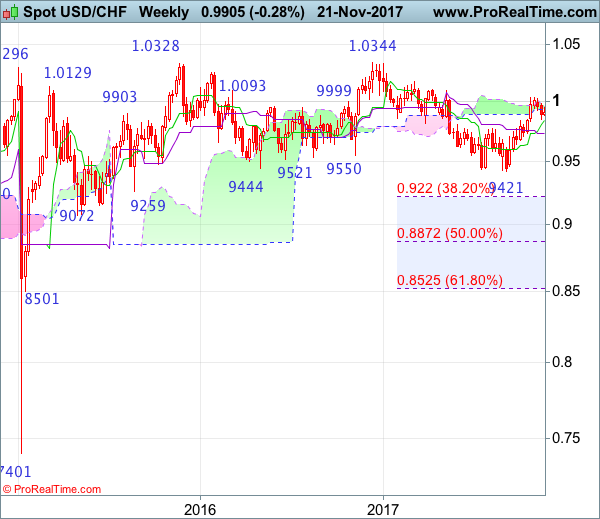

USD/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 7 Mar 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 9 May 2017

• Trend bias: Near term up

USD/CHF – 0.9907

Although the greenback found renewed buying interest at 0.9846 and recovered, reckon upside would be limited to 0.9985-90 and near term downside risk remains for the retreat from 1.0039 temporary top to bring another corrective decline, below said support at 0.9846 would extend weakness to 0.9800-05, however, reckon support at 0.9737 would hold and bring rebound later. Above 0.9950-55 would bring test of 0.9985-90 but break of indicated resistance at 1.0018 is needed to signal the pullback from 1.0039 has ended, bring retest of this level first.

On the downside, whilst initial weakness to 0.9800-05 cannot be ruled out, as long as support at 0.9737 holds, prospect of another rise to 1.0039 remains. A daily close below said support at 0.9737 would signal a temporary top has been formed instead, bring test of previous support at 0.9700, below there would confirm and bring retracement of recent upmove from 0.9421 to minor support at 0.9670, then 0.9642 (another support) but reckon downside would be limited to 0.9590-00 and support at 0.9565 should remain intact.

Recommendation: Buy at 0.9770 for 0.9970 with stop below 0.9670.

On the weekly chart, the greenback slipped last week and a black candlestick was formed, retaining our view that further consolidation below recent high at 1.0039 would be seen and pullback to the Tenkan-Sen (now at 0.9841) is likely, however, reckon downside would be limited to 0.9770 and bring another rise later, above last week’s high at 0.9987 would suggest the pullback from 1.0039 has ended, bring retest of this level, break there would extend the rebound from 0.9421 low to previous resistance at 1.0100-08, having said that, near term overbought condition should prevent sharp move beyond previous resistance at 1.0171 and 1.0200-10 should hold from here.

On the downside, although initial pullback to the Tenkan-Sen (now at 0.9841), then 0.9800 is likely, reckon 0.9770 would limit downside and bring another rise later. Below 0.9730-37 (current level of the Kijun-Sen and previous support) would defer and signal top is formed instead, this also suggest first leg of rebound from 0.9737 has ended and bring weakness to 0.9690-00, however, reckon support at 0.9642 would limit downside and price should stay above support at 0.9565 and the greenback shall stage another strong rebound next month.

Market Morning Briefing: The Aussie Is Trading Above The Weekly Support At 0.75

STOCKS

Almost all the major equity indices are marginally up today and look bullish for the near term.

Dow (23590.83, +0.69%) has risen exactly as expected to levels near 23600. While there is more room on the upside towards 24000 and higher on the weekly candles, the 3-day and daily charts suggest little room on the upside with resistances coming up near 23750-23800 region. Note that the earlier resistance mentioned near 23600 has now risen by 150-200points. Near term looks bullish.

Dax (13167.54, +0.83%) has moved up above 13100 contrary to our expectation of a narrow sideways consolidation. While above 13100, index looks bullish towards 13200-13300 or even higher in the coming sessions. The horizontal support on the daily candles and the 21-MA support on the 3-day line charts seem to be holding well for now.

Nikkei (22590.27, +0.78%) is slowly inching up towards 22800 which could act as a decent resistance in the near term. Only a break above 22800, would we focus on testing higher levels of 23200-23400 in the medium term. Important to keep an eye on the US-Japan 10yr yield and Dollar Yen for further directional cues. Although important and long term resistances are hovering not much higher than current levels for Dollar Yen and Nikkei, a sharp rejection to indicate a reversal is not visible yet. Till then immediate view continues to remain bullish.

Shanghai (3435.41, +0.73%) has also been sharply moving up in the past 2 sessions. While the upward momentum continues, the rise could continue towards 3440-3460 in the next few sessions.

Nifty (10326.90, +0.27%) has risen decently yesterday and as mentioned yesterday, could be headed towards 10400-10500 levels with some interim dips.

COMMODITIES

Gold (1279.25) is almost stable with no major movement visible. Price is stuck within 1300-1270 region and could be trapped in the sideways consolidation for some more time before eventually trying to move up.

Brent (63.07) looks bullish and could move up towards 64.00-64.60 again in the coming sessions. WTI (57.65) is also trading higher and could test 58-59 in the next couple of sessions before pausing in the near term. Levels near 59 would be an important resistance for WTI as seen on the 3-day candles. A break above that is needed to turn bullish for the longer term.

The Brent-WTI Spread (5.42) has been coming down sharply from resistance near 7 and could test 5.00-4.50 before again bouncing back towards 6.

Copper (3.1255) has moved above immediate resistance at 3.10 and the price could now well test 3.15-3.20 before pausing again.

FOREX

Dollar Index (93.94) is stuck along the support levels of 93.50 but has not seen a sharp bounce yet. While both Euro and Dollar Index has immediate supports, the one on the Dollar Index looks more likely to hold. Else the index could see some more of sideways consolidation in the near term.

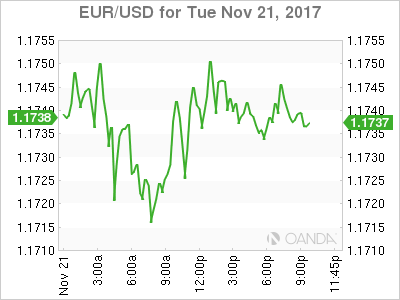

EURO (1.1735) is trading near earlier resistance turned support of 1.17 and while it holds a decent bounce back towards 1.1800-1.1850 is possible. Else a break below 1.17 could turn bearish for Euro in the near term.

Dollar-Yen (112.28) is stuck near 112.30 for the past 3-sessions. Support is visible on the daily candles near 112 which if holds can push back the price towards 113.0-113.5 in the near term; else a break below 112 is needed to see a sharp fall towards 111-110 in the longer run. An immediate bounce if seen could take up Nikkei also in the near term.

The Pound (1.3250) is almost stable near previous levels. Immediate resistance is visible near 1.33 from where a rejection is likely.

The Aussie (0.7565) is trading above the weekly support at 0.75 and while that holds, Aussie could move up towards 0.76-0.77 soon.

It would be crucial to watch if Dollar-Rupee (64.8850) bounces back towards 65.0-65.1 or moves lower to test 64.80. A bounce would be preferred just now while there could be scope of 64.60 if 64.80 breaks on the downside.

The Chinese Yuan (6.6311) is trading slightly weak against the US Dollar and could test 6.64 before again strengthening towards 6.62.

INTEREST RATES

The US yields are trading just near support levels and could possibly see a bounce in the near term. The 5Yr (2.10%), 10Yr (2.35%) and the 30YR (2.75%) are all up by 1bps and may move higher in the coming sessions.

The US yield differentials have all fallen sharply. The 10-5Yr (0.26%) is down from 0.34% within a week’s time while the 30-10Yr (0.40%) and the 30-5Yr (0.66%) are also trading at much lower levels. A faster bounce in the 5Yr and 10Yr compared to the 30Yr could lead to some recovery in the yield differentials.

The US-Japan 10Yr (2.33%) is yet to test resistance near 2.36% which now looks possible by the weekend. A rejection from there would be necessary to see some Yen strength in the near term.

The German-US 10Yr (-2%) is stable could test medium term support near -2.05%.

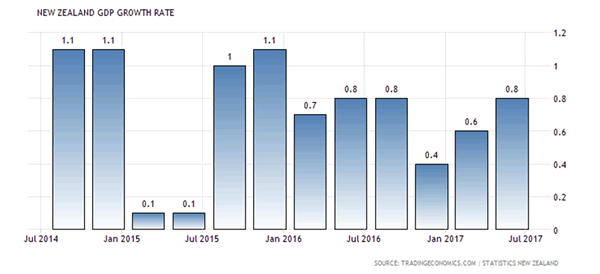

Is New Zealand Facing A Recession In The Near Term?

Key Points:

- Forbes's article claims New Zealand Facing a Recession in the coming year.

- Labour Government pitched as the prime driver of a recessionary cycle.

- Reality suggests it will take a global shock, not political policy, to induce a recession.

The past few days have seen a range of media outlets repeating claims from Forbes opinion piece that suggested that New Zealand could be facing a recession under Jacinda Ardern's Labour Party. Now as easy as it is to point the finger of discontent at the new incumbents the truth, as always, lays somewhere in between.

The thing is that most economists have been wondering when the next global down turn will appear for the past few years. The lack of inflation, along with any recessionary pressures, has been the subject of plenty of navel gazing from those of us within the profession. So given that economies typically run on cycles it isn't out of the question that we could see a recession in New Zealand over the next few years.

In fact, the chances of rising global risks and additional economic headwinds is actually quite likely over the next few years but to suggest that a recession on the way is pure speculation and not based on any current modelling, at least that I've seen. Sure, we are likely to shave some GDP growth in the coming years given the anti-immigration, anti-foreign property mantra from Labour. However, this could be largely balanced out by increased government spending in a variety of social areas. Subsequently, it would be a brave person that would predict a recession totally based on the prospects of a social/left wing dominated government.

In reality, New Zealand's next recession is likely to come from abroad and represent a significant global shock. Will it be the collapse of the debt fuelled, credit driven Chinese economy? Will the bubble pop around the dearth of mounting bad debts in the U.S. student loan market? Or potentially it could be a collapsing global car industry which has also been fuelled by easy credit terms.

The thing is economists are often the worst people in the world at predicting recessions given the role that human behaviour and expectations play in their formation. In fact, central bank's typically raise rates into recessionary cycles given that their data is typically backward looking. So use some caution when reading claims that the Labour Government will pitch us into a recession especially when even the experts are unsure of when and where the next one will come from

A Bit Of The Merry -Go- Round Syndrome In Currency Markets

A bit of the Merry -go- Round syndrome in currency markets

More of the same overnight as Forex Asset classes ebb and flow on yield curve speculation as 2's vs 10s continue to flatten with 2-year yields gravitating towards 1.77 %. There's no real news to report other than the fact the momentum play suggests the curve continues to flatten in the absence of any discernible US inflation to influence the long end.

The market is starting to look towards FOMC minutes as the next possible dollar driver given most do want to hear the Fed's view on the state of the flattening yield curve if nothing else Is the flattening momentum driven by EU bond markets, or does it signal the market's pricing in a slower trajectory for US growth. And of course, traders want to capture the Feds frame of mind towards inflation and extraordinary accommodation which will be key drivers for a number of currency pairs that are in G-10 dealers portfolios.

Overnight, US stock markets hit record highs on Tech Gains as investors do not want to fall behind this raging bull.But only time will tell if they're following false prophets or about to bank real profits.

Looking at a few of those key currencies this morning :

The Australian Dollar

There was a significant build-up of short Aussie positions hoping for a move lower post-RBA monetary policy minutes. But even with the relatively dovish RBA tack highlighted by considerable uncertainty over depressed wages, the market could only muster 20 pips downside test as the 2-way risk was always part of the equation ahead of Governor Lowe speech and the Governor didn't support the markets overly-dovish expectations. In fact, when he suggested the next move in rates would likely be up, it triggered a wave of short covering given that negative positioning was relatively heavy. And of course, the boisterous China equity markets sentiment helped lift the Aussie off the mat. Again as is so often the case, it's tough being the Aussie bear when testing the bottom of near-term ranges.

But with the Federal Reserve Board the only major central bank who are persistently sending a hawkish message (despite the flattening of the US yield curve), the outlook for the Aussie remains negative. The Feds are on the move to end the decade of extraordinary accommodation for no other reason than to provide themselves with buffer to adjust policy when the next economic downturn occurs. But on any hint of US inflation, especially the wage growth variety, look for an aggressive repricing of the US rates curve which will all but vaporise any forward Aussie premium. I suspect traders will be reloading shorts if the Fed minutes wax hawkish.

The Japanese Yen

Given the waves of political risk aversion the past fortnight, short-term traders have probably built up a considerable short position and correctly so as the markets remain in a constantly edgy state

.But the more extended the 112 support level holds he more susceptible these trading positions become to a significant near-term squeeze, even more so on positive US tax reform news. But given the US political newsflow has slowed to a drip with legislators in Washington on Thanksgiving holiday's, the USDJPY will continue to trade at the mercy of US Treasury yields. But even then, given that traders are gearing down for the year-end holiday season unless there's an unexpected or definitive shift in Fed policy, I think the 113-114.25 area is about as good as its going to get for the dollar bulls heading into year-end.

Since we're nearing Tax Reform crunch time, how the US dollar benefits from US tax reform remains a bit of a puzzle. Of course, tax reform will be a boon to equity markets but will equity inflows alone be enough to hold the USD bears at bay. While tax reform should be a meaningful positive, the US dollars medium-term fortunes are down to a quicker pace of tightening from the Fed and little more.

The Euro

The market continues to downplay the political risks out of the eurozone but none the less German politics remained in focus following the breakdown of Merkel's coalition talks.And given her options, Merkel stated that she preferred new elections to a minority government. Angela Merkel is a cunning political warhorse, and while her tenure at the helm appears a bit wobbly at this stage, the market should not discount her political savvy for one minute.

The last two days have been a microcosm for trading the Euro throughout 2017. A surprising shift in news flow creates new positions which are faded over the course of the next 12 hours only to have the original trading positions then gradually reentered over the subsequent 24hrs. It's been a merry-go-round to say the least and its unlikely to stop anytime soon

The Pound

Let's be clear no one likes trading the pound and given just how badly the Brexit negotiations are going there is few compelling reason to own any UK assets. And with the BOE roosting with the doves, there are even fewer plausible reason to buy Cable. So why isn't sterling trading lower. Two possible reasons 1) longer-term positioning is entrenched 2) The outside chance the Brexit goes through, and Sterling rallies 5-7 big figures.

Given this less than comforting risk rewards scenario, short-term speculators have pretty much given up the Sterling storyline.

Energy Markets

Oil prices rise after the API reports a significant draw in crude inventories.But all eyes remain focused on the OPEC's flux and reflux heading to Vienna as the meeting's outcome will ultimately determine oil prices near-term fate, but the API data does not go unnoticed as US production and inventories data have a tendency to act as a foil to OPEC production cuts.Both WTI and Brent were trending higher during Tuesdays NY session prior to the API release reflecting OPEC anticipation for the November 30 meeting. But at the NYMEX close, WTI failed to make any meaningful breakout perhaps influenced still by last weeks bearish demand revision from the IEA

Asia FX

Asian Stock exchanges soared as the Dragon breathed fire into Asian equity markets hitting ten-year highs with Chinese and HK stocks outperforming. In what could be a sign of things to come capital inflow is surging into the crucial mainland, and HK tech and financial sectors as investors look for undervalued opportunities. Whatever reservations investors may have had about booking profits into year end have been temporarily put on the back burner for fear of falling behind the raging global equity bull market run.

Regional currencies have made substantial gains and there remains a bias to sell USD regionally despite the broader G-10 space handcuffed by political woes and consolidating into a holiday-shortened week.

Oil prices are being watched closely by the local (ASEAN)currency basket traders as its thought that a top side price break could complicate the landscape for some while simplifying the outlook for other. On our regional highlight currency below MYR should benefit in a higher oil-price scenario, while INR and PHP are likely to suffer froma terms-of -trade basis.

The Malaysian Ringgit

But the $MYR has been unfettered by the EU political noise or the recent bid in USD across the broader markets. In fact, the Ringgit continues to march to the beat of its own drummer as the market remains exceptionally bullish after the massive bounce in GDP data released last week.Also, the BNM remains unwavering in their hawkish language. In fact, this week Governor Ibrahim all but suggested the central bank has a preference for a stronger currency. The BNM would prefer the stronger Ringgit to take the edge off rising prices given their latest forecast suggest inflation be at the upper end of the forecast range. If Oil prices do break out it will certainly complicate the matter for the BNM from an inflation standpoint. As it stands a January rate hike looks all but certain and the robust 3Q GDP does suggest one an additional rate hike for 2018 suggesting the MYR has ways to go before the currency runs out of gas.

The Philippine Peso

Similarly, the Philippine Peso which was written as the local whipping boy only last month continues to firm in a similar fashion to regional peers. The Peso is being supported by bullish sentiment related to the country's Macro prospects as momentum builds to close out the year on a blistering GDP print. Also, the Peso is trading in a much higher correlation with other regional currencies lately and reaping the benefits of local currency momentum.

The bottom line is it's hard to escape the local reflationary storyline.

The Indian Rupee

The Indian Rupee continues to gain traction, and if oil prices remain subdued given the bravado in local markets, we should expect we could see USDINR retest the post-Moody's-upgrade lows of 17 Nov (64.62-64.65 zone) sooner rather than later.

US Dollar Falls Ahead Of Federal Reserve Minutes

US durable goods and Fed minute to guide greenback

The USD has fallen across the board with commodity currencies the biggest movers against the greenback. The Aussie 0.40 percent, the kiwi 0.34 percent and the loonie 0.31 percent. US yields are the flattest since 2007. The distance between the 2 year and 10 year bonds has narrowed by 20 basis points. The durable goods orders could have a bigger impact that the Fed minutes released on Wednesday, given that the market has already priced into the greenback a rate hike when the central bank meets in December.

The US Census Bureau will release the durable goods orders data on Wednesday, November 22 at 8:30 am EST. Economists are forecasting a gain of 0.4 percent for the core durable goods (excluding transportation) and the same increase for durable goods after the big gain of 2.0 percent in last month’s report.

Oil prices are higher on USD weakness and with tomorrow’s release of the Energy Information Administration weekly crude inventories at 10:30 am EST the price is subject to change. The price of oil has been sensitive to fluctuations in supply as the Organization of the Petroleum Exporting Countries (OPEC) and other major producers seek stability through a production cut agreement that expires in March of 2018.

The U.S. Federal Reserve will publish the minutes form its November meeting on Wednesday, November 22 at 2:00 pm EST. There will be more clues on where certain policy makers stand regarding inflation, but the market is still pricing in a 99 percent probability of a US rate hike in December. The monetary policy statement on November 1 did little to confirm a rate hike, but given the rise of the US economy and the Fed’s removal of the use of the “moderately” language.

The EUR/USD gained 0.10 percent on Tuesday. The single currency is trading at 1.1744 after US bond yields have fallen. The negative on the EUR of the German coalition failure seems to have been priced out despite positive housing data in the US. Over the weekend the attempt by German Chancellor Angela Merkel to form a coalition was not successful after the Free Democratic Party pulled out. Given the loss of votes to the two major parties the last partner of Merkel’s party declined to join her coalition and instead set its sights on the opposition. The uncertainty in German leadership could be a huge blow for Brexit negotiations. Despite the lack of clarity in the face of elections in the new year, the market still prices the EUR to outperform the USD in 2018. German growth will be a big component as the other EU nations show signs of recovery.

Kenny Fisher, MarketPulse analyst, outlined the improving housing conditions in the US. [http://www.marketpulse.com/20171121/gold-posts-gains-fed-minutes-ahead/]

US housing indicators continue to beat expectations. On Monday, it was the turn of Existing Home Sales, which climbed to a 4-month high. On Friday, Building Permits and Housing Starts impressed the markets. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Starts also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

The USD has fallen more than 11 percent versus the EUR in 2017. The victory of Trump and his following pledge to introduce tax reforms and incur in higher infrastructure spending gave the US currency a boost, but as those promises have yet to come to life the buck is under pressure. The actions of the Fed have been priced into the currency pair, but as the European Central Bank (ECB) starts tapering its massive QE program and a potential rate hike in 2018 the single currency has risen as there is more upside seen by investors compared to the dollar.

The U.S. Federal Reserve has telegraphed its intentions in 2017 and will round up the year with an interest rate hike before a change in leadership takes place in February sees the rise of Jerome Powell to the chair position while Yellen has said that she will retire despite still holding a governor position.

Market events to watch this week:

Wednesday, November 22

8:30 am USD Core Durable Goods Orders m/m

8:30 am USD Unemployment Claims

10:30 am USD Crude Oil Inventories

2:00 pm USD FOMC Meeting Minutes

4:45 pm NZD Retail Sales q/q

Thursday, November 23

4:30 am GBP Second Estimate GDP q/q

8:30 am CAD Core Retail Sales m/m

11:30 am CHF SNB Chairman Jordan Speaks

Gold Posts Gains

Gold has posted sharp losses in the Monday session. In North American trading, the spot price for an ounce of gold is $1282.39, up 0.43% on the day. On the release front, Existing Home Sales improved to 5.48 million, beating the forecast of 5.42 million. Later in the day, Fed Chair Janet Yellen will speak at an event in New York City. Wednesday will be busy, as the US releases employment, durable goods and consumer confidence reports. Also, the Federal Reserve releases the minutes of its November policy meeting.

US housing indicators continue to beat expectations. On Monday, it was the turn of Existing Home Sales, which climbed to a 4-month high. On Friday, Building Permits and Housing Starts impressed the markets. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Starts also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

As President Trump's tax reform bill winds it way through Congress, gold prices have been fluctuating. On Monday, gold prices jumped 1.4%, erasing the losses seen on Friday. President Trump won a major legislative victory on Thursday, as the House of Representatives passed its version of the tax bill, by a vote of 227-205. However, with the vote largely based on party lines, Republicans will have a tougher battle passing the Senate version of the bill, as the Republicans have a slim majority of 52-48. The tax legislation provides major tax relief and cut corporate taxes from 35% to 20%, and if Congress does enact a new tax code, the US dollar could make strong gains, at the expense of gold.

Pound Yawns as Mfg. Order Expectations Surge

The British pound is showing limited movement in the Tuesday session. In North American trade, GBP/USD is trading at 1.3240, up 0.05% on the day. In the UK, Public Sector Net Borrowing climbed to GBP 7.5 billion, above the forecast of GBP 6.6 billion. This marked the highest deficit since April. There was much better news from CBI Industrial Order Expectations, which jumped to 17, crushing the estimate of 3 points. As well, BoE Governor Mark Carney testified about inflation before a parliamentary committee. In the US, Existing Home Sales improved to 5.48 million, beating the forecast of 5.42 million. Later in the day, Fed Chair Janet Yellen will speak at an event in New York City. Wednesday is busy, as the US releases employment, durable goods and consumer confidence reports. Also, the Federal Reserve releases the minutes of its November policy meeting. In the UK, the government will present the Autumn Forecast Statement.

There was positive news from British CBI Industrial Order Expectations, an important barometer of the manufacturing sector. The indicator surged to 17 points in October, rebounding from the September release of -2 points. Manufacturing indicators continue to point upwards, boosted by strong global demand and a weak British pound. Export order books are at their highest levels since 1995, and the markets are predicting that the export and manufacturing sectors will continue to shine in the fourth quarter.

US construction numbers continue to beat expectations. On Monday, it was the turn of Existing Home Sales, which climbed to a 4-month high. On Friday, Building Permits and Housing Starts impressed the markets. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Starts also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

Euro Weighed by German Political Uncertainty, Looks to Eurozone Flash PMIs for Support

The euro is once again dogged by political risks as the collapse of the coalition talks in Germany has raised the prospect of months of uncertainty in the Eurozone's biggest economy. The announcement on Monday of the collapse of the three-way coalition talks between Chancellor Angela Merkel's party, the CDU/CSU, the pro-business Free Democratic Party (FDP) and the Green party, has driven the euro to a one-week low of $1.1712, shifting the near-term risks for the currency back to the downside.

The failure to form a coalition is a serious blow for Merkel, whose party had its worst election performance in September since 1949. Germany's president, Frank-Walter Steinmeier, is urging all parties to resume talks but there are few hopes of any deal being struck. It is thought it is unlikely for the FDP to return to the negotiating table after unexpectedly pulling out of the talks. The Greens have accused the FDP of trying to oust Merkel as Chancellor.

Merkel could now try to form a minority government, with the possible backing of the Greens. However, Merkel has already hinted that she would prefer to have fresh elections, with the aim of achieving a strong and stable government, than to run a minority government. But with the President reluctant to call new elections, the possibility of some sort of a compromise between the parties cannot be dismissed. The FDP's withdrawal from the coalition talks may now put pressure on the Social Democrats (SPD) to reconsider reviving their 'grand coalition' with the CDU/CSU.

Although the SPD leader, Martin Schulz yesterday ruled out entering another coalition and voiced his support for snap elections, the threat of voter punishment for forcing new elections could yet see the party find itself being lured into a new grand coalition, especially if Merkel was to offer significant concessions to secure a deal. The same can be said for the FDP.

The most probable outcome however, is a fresh election. Under German law, the process of calling a snap election could take weeks, suggesting the current political stalemate is unlikely to be resolved before the end of the year. This could weigh on the euro and deepen the currency's downward correction from the 32-month high of 1.2092 set in September. A re-test of November's 3½-month low of $1.1552 would become highly likely under such a scenario.

However, strengthening economic fundamentals for Germany and the Eurozone, mean downside moves are likely to be limited. Eurozone PMI data due on Thursday should serve as a reminder of that. The region's composite PMI is expected to stay unchanged at 56.0 in November's flash reading. The index hit a six-year high of 56.8 in April and May and combined activity in services and manufacturing has held near those highs since.

The euro could also find support from Friday's Ifo business survey out of Germany. The Ifo business climate index hit an all-time high of 116.7 in October and is only forecast to fall marginally to 116.6 in November.

While the euro area's improving economic landscape does not appear to be at risk from developments in Germany, any early sign that the political situation is starting to dent business confidence in the country could put a damper on wider investor sentiment in the region. This could prove a catalyst for a sharper sell-off in the euro. But for now, the single currency has underlying support from expectations of a gradual removal of monetary stimulus by the European Central Bank over the coming year.

Aussie Bounces after RBA Lowe Says Next Rate Move is Up; Turkish Lira Hits Record Low

The aussie overperformed its peers during the European session, posting a strong rebound after the RBA governor ruled out the possibility of expanding stimulus monetary policy. On the other hand, the Turkish lira hit a record low against the greenback after the Turkish president threatened to take control of the Central Bank of the Republic of Turkey (CBRT).

Speaking at a dinner event in Sydney, the RBA governor underlined that "there is not a strong case for a near-term adjustment in monetary policy", explaining that the labour market has more space to grow, while the RBA expects inflation to rise gradually and remain below the central bank's target level for some time. However, he mentioned that "the next move in interest rates will be up, rather than down" if the economy performs in line with expectations, foreseeing that employers will invest in the workforce and therefore accelerate consumers spending. Early on Tuesday, the minutes of the RBA's meeting in October revealed concerns on subdued wage growth, pushing the aussie down to a five-month low of $0.7532. But after Lowe's speech, the aussie erased this week's losses, jumping to $0.7583 and gaining 0.30% on the day.

Its New Zealand cousin rose by 0.34% to $0.6831 despite global dairy prices falling by 3.4% in this month's second Global Trade Dairy Auction. In the previous auction, dairy prices declined by 3.5%.

The greenback was in a range against its counterparts, with the index slipping back to 94.08 after reaching a fresh one-week high at 94.16 in the first hours of the session. Investors will be eager to hear any developments in the tax story but only after Senators return from a week off due to Thanksgiving holiday on Thursday. Moreover, their bets on next year's interest rate trajectory might shift as four new members are said to join the Fed board. The current Fed chair, Janet Yellen confirmed yesterday that she would step down from the board after her successor, Jerome Powel takes over as chair, creating a fourth vacancy. Minutes from October's FOMC meeting due on Wednesday will also gather attention.

Data on the US existing home sales released before the session-end appeared better than expected, adding some gains to the dollar.

Dollar/yen was last trading 0.40% lower at 112.20.

The loonie gained 0.40% on the day on the back of higher oil prices, although readings on wholesale sales in September came in disappointing. Dollar/loonie was last seen at 1.2767.

In other news, the Turkish president, Tayyip Erdogan, criticized monetary policy, spreading fears of a potential government intervention in monetary decisions. This emerged after the CBRT decided to tighten liquidity by raising borrowing costs, ignoring Erdogan's desire to lower interest rates. The dollar topped at an all-time high of 3,9768 versus the Turkish lira in the face of Erdogan's threats.

The euro was mainly steady at one-week low levels of $1.1740, unable to recover as investors were closely watching political developments in Germany. Reports that the ECB will only be making minor adjustments to its monetary policy guidance next year rather than a major shift to its language as its current quantitative program expires in December did not bring any significant volatility to the market.

Four BOE members including Michael Saunders, Jon Cunliffe, Ian McCafferty and Gertjan Vlieghe testified in front of the British Parliament early in the session, backing a forward guidance on monetary policy dependent on economic developments. Moreover, they supported that the central bank would not make conclusions on Brexit, retaining its assumption of a smooth exit from the bloc, unless business and consumer surveys show otherwise. Pound/dollar rose by 0.11% to 1.3241, while euro/pound hit a 1 ½-week low of 0.8841 before inching up to 0.8856.

In commodities, gold surged by 0.48% to trade at $1,282.43 per ounce and energy prices extended their uptrend ahead of the API weekly report on US oil inventories. WTI crude increased by 1.12% to $57.05 per barrel and Brent jumped by 0.80% to $62.71.