Sample Category Title

EURUSD Still Intraday Bullish Above 1.1713 Level

The euro has found dip buying demand from the key 1.1713 technical level against the U.S dollar in early Tuesday trading. Since the EURUSD hit 1.1807 on Monday morning, the pair had gradually started to slip lower to test towards the key 2015 price-high, found at 1.1713. The fundamental principle of the euro's fall this week remains intact, with the specter of uncertainty in German politics hanging over the euro currency, with no clear resolution in-sight.

The EURUSD pair remains technically bullish while trading above the 1.1713 technical level. Further intraday upside towards the 1.1755 and 1.1807 level appears possible.

Should the EURUSD pair start to slip below the 1.1713 technical level, further aggressive selling towards the 1.1664 level seems possible.

CAC Rally Continues

The CAC continues to gain ground this week. Currently, the CAC is at 5,376.95, up 0.68% on the day. For a second straight day, there are no French or eurozone indicators on the schedule. On Wednesday, the eurozone releases consumer confidence and the Federal Reserve will publish the minutes of the November policy meeting.

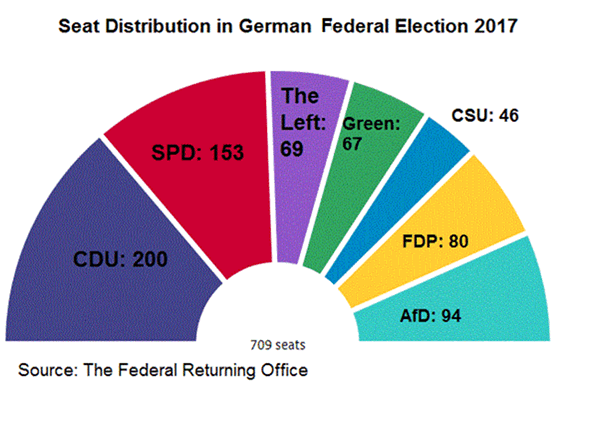

When Germany sneezes, the eurozone is likely to get a cold. Germany is currently facing one of its biggest political crises in decades, as President Angela Merkel has been unable to form a coalition. Talks to form a government have been ongoing for a month, but the Free Democratic Party (FDP) pulled the plug on Sunday, saying there was no "basis of trust" to enter a government with Angela Merkel's CDU-CSU alliance and the Greens. The parties have been holding negotiations for a month, but have failed to bridge the gaps on issues such as immigration. Merkel has said she is not interested in running a minority government, whereby the opposition could topple the government at any time. President Frank-Walter Steinmeier has urged the parties to redouble their efforts in order to reach an agreement, warning that another election would cause uncertainty in German as well as Europe.

ECB head Mario Draghi spoke before a European Parliament Committee on Monday, and sounded optimistic about the eurozone economy. Draghi said that the ECB continues to see signs that the recovery is continuing. Economic growth continues to point upwards, and employment is at a record high. As for inflation, Draghi was optimistic, saying he was confident that wage growth will increase and drive underlying inflation. Still, Draghi acknowledged that inflation has "yet to show convincing signs of a self-sustained upward trend."

DAX Ignores Political Crisis, Rally Continues

The DAX index has started the week with strong gains. In the Tuesday session, the DAX is at 13,126.00, up 0.52% on the day. The index has jumped 1.4% this week. There are no German or eurozone indicators on the schedule. On Wednesday, the eurozone releases consumer confidence and the Federal Reserve will publish the minutes of the November policy meeting.

Germany is facing one of its biggest political crises in decades, as President Angela Merkel has been unable to form a coalition. Talks to form a government have been ongoing for a month, but the Free Democratic Party (FDP) pulled the plug on Sunday, saying there was no "basis of trust" to enter a government with Angela Merkel's CDU-CSU alliance and the Greens. The parties have been holding negotiations for a month, but have failed to bridge the gaps on issues such as immigration. Merkel has said she is not interested in running a minority government, whereby the opposition could topple the government at any time. President Frank-Walter Steinmeier has urged the parties to redouble their efforts in order to reach an agreement, warning that another election would cause uncertainty in German as well as Europe.

ECB head Mario Draghi spoke before a European Parliament Committee on Monday, and sounded optimistic about the eurozone economy. Draghi said that the ECB continues to see signs that the recovery is continuing. Economic growth continues to point upwards, and employment is at a record high. As for inflation, Draghi was optimistic, saying he was confident that wage growth will increase and drive underlying inflation. Still, Draghi acknowledged that inflation has "yet to show convincing signs of a self-sustained upward trend."

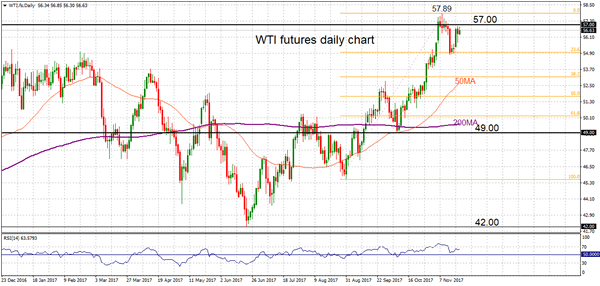

WTI Oil Futures Pause Rally And Shifts To Neutral, Room For Further Strength

WTI oil futures have been rising steadily and closing above the 200-day moving averages since mid-September. The bullish technical picture was confirmed by the crossover of the 50-day MA above the 200-day MA but the rally lost steam at 57.89 and subsequently, the near-term trend has shifted to neutral.

The market is now trapped between the key round figure of 57.00 and the 23.6% Fibonacci retracement level (54.96) of the latest rise from 45.56 to 57.89. These levels will act as support and resistance in the near term as the market is expected to remain in a consolidation phase. The RSI has turned flat and upside momentum has been exhausted after the market reached overbought levels when RSI rose above 70.

There is room for further strength since the 50-MA is rising. A break above 57.00 would open the way for a re-test of 57.89 and from there, there is scope to resume the uptrend. A fall back into the 53.00 handle (break below 38.2% Fibonacci) would indicate the short-term uptrend has ended.

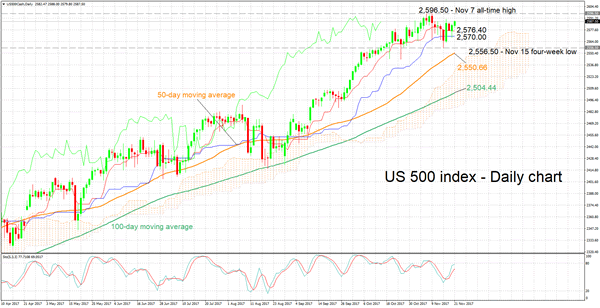

US 500 Index Looking Bullish In The Short- And Medium-Term, Trades Not Far Below All-Time High

The US 500 index has been rising over the last two days and currently trades not far below the all-time high of 2,596.50 recorded on November 7.

The positive alignment with the Tenkan-sen line being above the Kijun-sen line is painting a bullish picture in the short-term. Notice though that both lines are flat at the moment. This could be an indication of positive momentum losing steam. The very-short term picture though remains positive as indicated by the stochastics: the %K line is above the slow %D line with both lines currently heading higher.

Should the index continue gaining, resistance might come around early November’s all-time high of 2,596.50 with the area around this level also encapsulating 2,600, a potential psychological mark.

On the downside, support might come around the current levels of the Tenkan- and Kijun-sen lines at 2,576.40 and 2,570.00 respectively. The area around these levels was also fairly congested recently. Further below, the range around November 15’s four-week low of 2,556.50 could provide additional support.

The medium-term picture is clearly bullish: the 50- and 100-day moving averages (MAs) are positively sloped with the price being above both MAs. In addition, the index is trading above the Ichimoku cloud.

Overall, both the short- and medium-term are currently looking bullish though it should be mentioned that there is a sign that positive short-term momentum might be losing steam.

German Political Stalemate: Four Options on Table, None An Easy Way

Although the selloff the euro as a result of a breakdown of Germany's coalition talks appeared short-lived, political instability in the country and the EU would remain in play for some time. We see four possibilities are present in the aftermath of FDP's walkout from the 4-week exploratory talks: 1 New election, 2. Grand coalition (a CDU/CSU+SPD Government), 3. Restart of the Jamaica talks (CDU/CSU + FDP+ Greens) or 4. Formation of a minority government by CDU/CSU with either the Greens or FDP. It appears that none of the above options is easier to be achieved as each has its own limitations and constraints. This report would analyze each of the four scenarios. Yet, assessing the likelihood of the scenarios at this stage appears premature as the developments remain fluid.

While the market had anticipated a Jamaica coalition government would likely be formed after the federal election in September, the negotiations collapsed with FDP walking out from the exploratory talks on Sunday night. The parties involved (CDU/CSU + FDP+ Greens) failed to agree on migration and energy policies, as well as other controversial issues. The FDP leader, Christian Lindner, explaining the walkout, indicated that there are 'irreconcilable differences' amongst the parties which 'have no common vision for modernization of the country or common basis of trust'. Executive Chancellor Angela Merkel described FDP's walkout as 'regrettable' and noted that it's 'a day of deep reflection on how to go forward in Germany'. She added that, 'as chancellor, I will do everything to ensure that this country is well managed in the difficult weeks to come'.

Resumption of Jamaican Talks: German President Frank-Walter Steinmeier, a SPD member and the former foreign minister, has called for the leaders to reconsider returning to negotiation table. He is scheduled to meet with the Greens and FDP on Thursday. We see the resumption of the Jamaican talks is challenging, if not impossible. Indeed, in our previous reports, we have mentioned that while CDU/CSU had preferred to work with FDP given the similarities in ideologies and policy platforms, FDP and Green are traditional rivalries. The two parties have very different views on various issues, ranging from labor and social policy, to immigration policy; from fiscal policy to EU integration. There is limited cooperation between the two parties in local level, let alone federal level. Concluding of the 4-week talks with a walkout has clearly explained the divergence and conflict.

Minority Government: If the FDP refuses to return to the negotiation table eventually, Merkel might consider forming a minority government, either with the Greens or FDP. Yet, Merkel has already indicated she would rather have another election than forming a minority government. A CDU/CSU + Greens minority government would miss 42 seats to reach the majority in the parliament while a CDU/CSU + FDP one would miss 29. In either case, one or two more parties would be needed to provide the 'supply-and-confidence' support to the government. It appears that no feasible candidate is identified for now to sign the 'supply-and-confidence' agreement due to the divergent views on critical political and economic issues. What Merkel is more concerned is that the arrangement might end up giving the far-right AfD more power in the parliament.

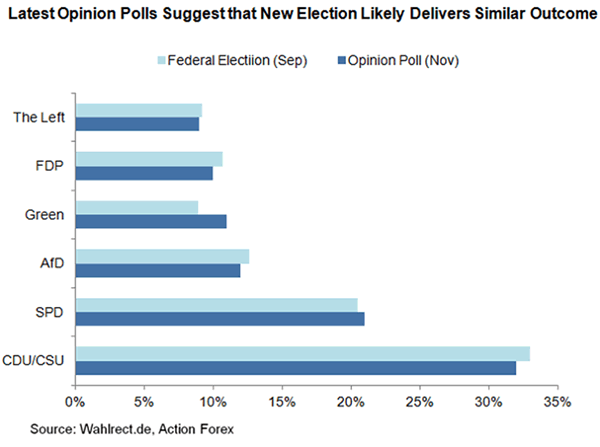

New Election: While Merkel noted her preference of a snap election to a minority government, recent survey suggests that the outcome would not make much difference. Germany would again end up with two choices- Grand Coalition or Jamaican Coalition. The latest poll of polls shows that CDU/CSU has still secured one-third of support, followed by 21% and 12% for SPD and AfD, respectively.

Grand Coalition: Upon receiving its biggest defeat since WWII, the SPD has pledged after the September election that it would be the biggest opposition. The SPD has attributed the loss of popularity and support to being a coalition partner of the CDU/CSU in the past term. SPD's leader Schulz reiterated that his party would not join Merkel after the collapse news. Yet, he noted that 'in such a situation, the sovereign, that is the voters, must reassess what is going on', adding that the party is not 'shy away from a new election'. The SPD would be meeting the President on Wednesday.

The situation remains fluid and it is difficult for now to assess which scenario has higher chance to materialize. What can be certain now is that political instability in Germany would continue for some time. the situation would also make it more difficult to implement significant reforms, both in domestic policies and EU integration.

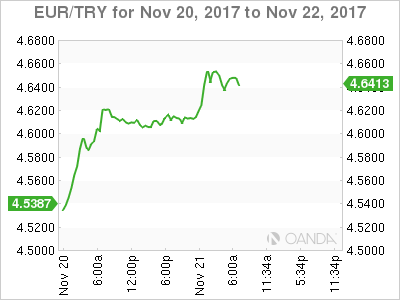

Turkey’s Central Bank Lends Lira Support

Tuesday November 21: Five things the markets are talking about

Both U.S and German politics dominate capital market moves.

Despite the holiday-shortened trading week, the progress of the U.S tax reform legislation through congress continues to be closely watched. While in Germany, it remains unclear whether Chancellor Merkel will attempt to govern with a minority administration or that another early election in the spring will prove necessary.

In the U.K, ‘dovish' comments from BoE rate setter Dave Ramsden, who voted against the recent interest rate hike, seems to have had little impact on the pound (£1.3235). Investors seem to be more focused on Brexit negotiations.

Stateside, existing home sales (10:00 am EDT) are expected to rise for a second consecutive month, while Fed Chair Yellen, who yesterday confirmed that she will leave the Fed when her term ends, is scheduled to speak in New York (06:00 pm EDT). Markets will be looking for clues as to whether the Fed will hike rates next month.

Be prepared, Ms. Yellen may be asked her views on future Fed policy without her at the helm.

1. Stocks pare gains as German political impasse hits Europe

In Japan, stocks rallied overnight after large cap stocks such as automakers and manufacturers of factory automation equipment rallied, while North Korean tensions supported defence-related shares. The benchmark Nikkei ended +0.7% higher, while the broader Topix added +0.7%.

Down-under, the MSCI Asia Pacific Index jumped +0.9% to the highest in more than a week.

In Hong Kong, stocks had their best day in seven-weeks on Tuesday. The Hang Seng index was up +1.91%, while the Hang Seng China Enterprises index rose +2.91%.

In China, the blue-chip index ended at a fresh 28-month high overnight, bolstered by robust gains in brokerage firms. At the close, the Shanghai Composite index was up +0.6%, while the blue-chip CSI300 index was up +1.8%.

In Europe, regional indices trade slightly higher across the board recovering from earlier weakness, in relatively quiet trade.

U.S stocks are set to open in the ‘black (+0.1%).

Indices: Stoxx600 +0.1% at 386.7, FTSE flat at 7392, DAX +0.2% at 13080, CAC-40 +0.20% at 5351, IBEX-35 +0.2% at 10040, FTSE MIB +0.3% at 22251, SMI +0.2% at 9318, S&P 500 Futures +0.1%

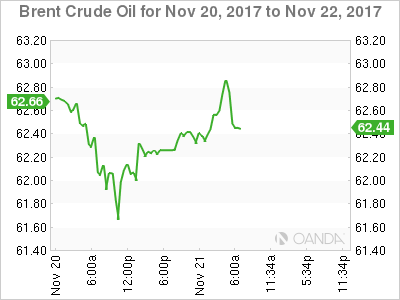

2. Oil rises ahead of OPEC meeting, gold prices steady

Oil prices remain better bid as traders look to next weeks OPEC meeting (Nov. 30) at which major crude exporters are expected to extend production cuts, though rising U.S. output continues to cap some of these gains.

Brent crude oil is up +47c at +$62.69 a barrel, while U.S light crude (WTI) is at +$56.74, up +32c.

OPEC, together with a number of non-OPEC producers led by Russia, has been restraining output this year in an effort to end a global supply overhang and support prices.

OPEC is expected to extend cuts, as storage levels remain high despite recent drawdowns, although there are doubts about the willingness of some participants to keep restricting production.

However, the biggest headache for OPEC has been a rise in U.S drilling, led by shale oil producers, which in turn is capping price gains.

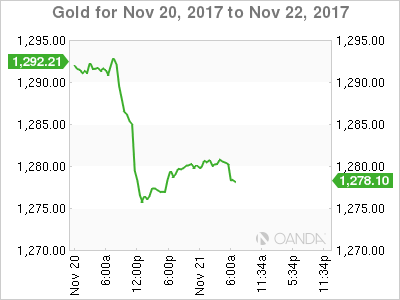

Gold prices have inched higher ahead of the U.S open; with investors waiting for tomorrow's Fed minutes for clues on the outlook for potential rate rises. Spot gold is up +0.3% per ounce. The metal fell about -1.4% yesterday in its biggest one-day percentage drop since Sept. 11.

3. U.S yield curve flattest in a decade

The U.S Treasury yield curve has flattened to +59 bps for the first time in over a decade and is on track for its biggest monthly flattening since February 2016.

The gap between 2/10-years has narrowed -20 bps so far this month, and is at its tightest level since October 2007. The yield on 10-year Treasuries declined -1 bps to +2.35%.

In Germany, the 10-year Bund yield has fallen -2 bps to +0.35%, the lowest in almost two weeks on political uneasiness.

In the U.K, the 10-year Gilt yield has decreased -4 bps to +1.252%, the lowest in almost two-weeks, while in Japan, the 10-year JGB yield has dipped -1 bps to +0.033%, the lowest in more than a week.

Elsewhere, Turkey's 10-year government bond yields have jumped to a multi-year high of +12.35%, the highest in five-years. The 2-year bond also has rallied to +13.53%, a higher level than the 10-year bond, creating an “inverted” yield curve, which points to the perception of elevated near-term risks.

>

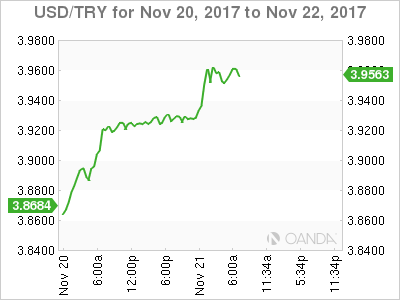

4. Turkey's central bank lends lira support

In emerging markets, the Turkish lira (TRY) has hit an all-time low of $3.9780 outright, as recent pressure on the central bank (CBRT) from its own government and ongoing tensions with the U.S continues to pressure the currency.

Note: TRY is down some -17% against the dollar since Sept.

The central bank said it would end its interbank money-market facility for overnight transactions from tomorrow and instead fund banks via its late liquidity overnight lending rate. The move will raise average funding costs by 0.25 bps to +12.25%.

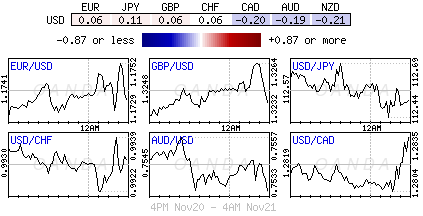

The EUR is +0.2% up against the U.S dollar at €1.1753 as improving eurozone growth takes precedent before political issues in Germany. Chancellor Merkel said she would rather have another election than form a minority government.

In the U.K, GBP/USD rises to its highest in nearly three weeks at £1.3268 – up +0.25% on the day – on reports that PM Theresa May is preparing to double her offer for a Brexit “divorce” settlement. Although this offer would still be below what the EU has demanded, it raises some optimism among investors that Brexit talks may be able to progress toward discussing a trade deal.

5. Reserve Bank of Australia (RBA) monetary policy minutes

The minutes of the last Reserve Bank of Australia (RBA) policy meeting pointed to hopes that economic growth was strengthening, but also “considerable uncertainty” over how quickly wage growth might pick up.

RBA Gov. Lowe hardly sounded ‘hawkish' in signalling there's little reason for now to think about higher interest rates, the Aussie dollar nonetheless took the opportunity to rebound after weeks of declines. The currency has moved back to A$0.7560 an intraday high.

Officials continue to fret anew about the country's lack of notable wage growth – Gov. Lowe speech did not sound that hopeful of a near-term uptick in inflation.

EUR/USD – German Political Woes Weighing on Euro

After starting the week with losses, the euro has settled down in the Tuesday session. Currently, EUR/USD is trading at 1.1734, down 0.00% on the day. In economic news, there are no eurozone indicators on the calendar. The US will release Existing Home Sales, with an estimate of 5.42 million. As well, Fed Chair Janet Yellen will speak at an event in New York City. Wednesday is busy, as the US releases employment, durable goods and consumer confidence reports. Also, the Federal Reserve releases the minutes of its November policy meeting.

Germany is facing one of its biggest political crises in decades, as President Angela Merkel has been unable to form a coalition. Talks to form a government have been ongoing for a month, but the Free Democratic Party (FDP) pulled the plug on Sunday, saying there was no “basis of trust” to enter a government with Angela Merkel's CDU-CSU alliance and the Greens. The parties have been holding negotiations for a month, but have failed to bridge the gaps on issues such as immigration. Merkel has said she is not interested in running a minority government, whereby the opposition could topple the government at any time. President Frank-Walter Steinmeier has urged the parties to redouble their efforts in order to reach an agreement, warning that another election would cause uncertainty in German as well as Europe.

Will we see a triple sweep from US housing indicators? The markets are forecasting that Existing Home Sales will improve in October, following sharp housing data on Friday. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Start also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter, which is good news for the US economy.

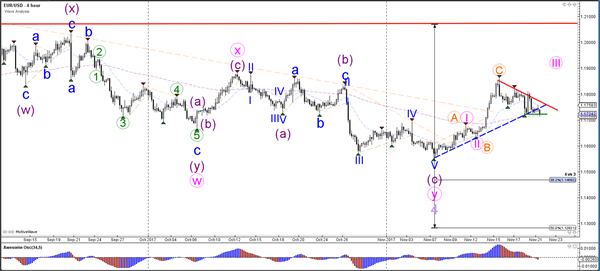

Daily Wave Analysis: EURUSD Fails To Break Above 1.18 And Retests 1.17 Support

Currency pair EUR/USD

EUR/USD is retesting key support trend lines (blue/green). A break below the support could indicate a failure to continue the uptrend and makes an ABC (orange) more likely than a 123 (pink) pattern, which in turn could mean that the wave 4 (light purple) is still active

The EUR/USD potential breakout aboveresistance (red) could indicate a continuation of the uptrend within a wave 5 (purple) of wave 3 (pink). A push below the 61.8% Fib makes a wave 4 less likely and could indicate a bearish continuation towards the targets of wave Y (blue).

Currency pair USD/JPY

The USD/JPY bounced at the 38.2% Fibonacci support level and retraced back to the resistance trend line (red) of the bearish channel. A bullish break above that resistance could see price challenge the 38.2, 50% Fibs or shallower trend line (orange) whereas a bearish continuation could target the 50% Fib.

The USD/JPY could expand the wave X (pink) via an ABC zigzag (blue), although this scenario becomes less likely if price breaks below the support trend lines (blue).

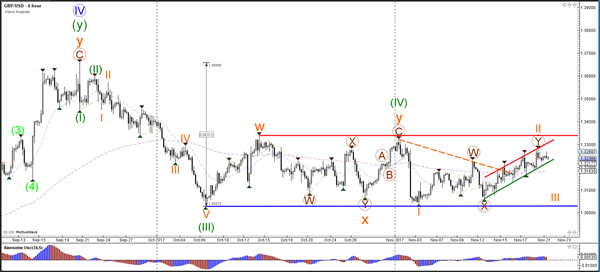

Currency pair GBP/USD

The GBP/USD remains in the bullish channel (red/green) within the larger sideways range (red/blue). A breakout above the higher resistance (red) or below the support (blue) is needed before a new trend can be expected.

The GBP/USD seems to have completed a new ABC pattern (blue), which in turn could have completed waves Y (green/brown).A break below the channel support (green) could indicate a potential breakout towards the bottom of the range (blue).

NZD/USD Continuation Bearish SHS Pattern

The NZD/USD is in a strong monthly downtrend. If we zoom in to H4/H1 time frame, we are also able to see a downtrend but also a retracement that is happening now. The POC zone 0.6833-45 (D H4, EMA89, 61.8, ATR top) once hit, could reject the price. At the top of that we also see a continuation Bearish SHS pattern (cont Bearish SHS) that happens in a downtrend, close to supports. Targets are 0.6793, 0.6781 and 0.6760 as long as 0.6670 holds.

L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)