Sample Category Title

Market Update – European Session: Focus Remains On German Politcal Situation

Notes/Observations

Downplaying political risks out of the euro area; Germany seems to be heading towards a Merkel-led minority government or towards early spring new elections

Overnight

Asia:

RBA Nov Minutes: pass-through to inflation could be delayed by many factors including retail competition. Saw considerable uncertainty on how rapidly wages might pick up and add to inflation

Japan Finance Min Aso stated that the Extra budget was not a response to economic downturn. Tax changes need to consider work reform and an aging society; one time depreciation is a big encouraging investment. BoJ's JGB purchases are not aimed at debt monetization

President Trump: US to designate North Korea as a state sponsor of terrorism

Europe:

German Chancellor Merkel: new elections would be better than a minority govt; goal was still to form a stable govt. wiling to be Chancellor for another 4 year term, not afraid of new elections. conservatives were now united on the migration issue

BOE's Dep Gov Ramsden (dissenter): UK economy in a weaker growth period for some time to come; domestic CPI is below the rate consistent with 2% goal. Markets had been pricing in another bank rate hike by the end of next year, consistent with yield curve that was the base for BOE's Nov outlook

UK panel reportedly considering move to £40B (€45B) Brexit financial settlement offer

ECB expected to make small, incremental changes next year in discussing QE exit. More likely to make only small adjustments through 2018 rather than a major language change on QE policy. Governing Council had not yet formally taken up the issue of how to handle announcements on ending QE

European Banking Authority (EU bank regulator) to relocate to Paris from London post-Brexit

Americas:

Janet Yellen to resign from Fed Board of Governors, effective upon the swearing in of her successor as Chair

S&P affirmed Canada sovereign ratings at AAA; outlook Stable

Economic Data:

(CH) Swiss Oct Trade Balance (CHF): 2.3B v 2.9B prior; Real Exports M/M: -1.8% v -1.1% prior; Real Imports M/M: -1.1% v -3.1% prior

(NL) Netherlands Oct House Price Index M/M: 0.7 v 0.3% prior; Y/Y: 8.2 v 7.3% prior

(FI) Finland Oct Unemployment Rate: 7.3% v 8.0% prior

(ZA) South Africa Sept Leading Indicator: 98.4 v 97.2 prior

(NO) Norway Petroleum Directorate (NPD): Oct Oil production at 1.54M bpd v 1.44M prior

(HK) Hong Kong Oct CPI Composite Y/Y: 1.5% v 1.7%e

UK Oct Public Finances (PSNCR): -£3.8B v +£11.4B prior; Public Sector Net Borrowing: £7.5B v £6.5Be, Central Government NCR: -£6.7B v +£19.3B prior, PSNB ex Banking Groups: £8.0B v £7.1Be

(BR) Brazil Nov IGP-M Inflation (2nd Preview): 0.4% v 0.3%e

Fixed Income Issuance:

(ID) Indonesia sold total IDR5.95 in 6-month Islamic Bills and 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

(PL) Poland sold €300M in 2-year notes via private placement; pricing at +45bps to 3-month Euribor

(ES) Spain Debt Agency (Tesoro) sold total €4.23B vs. €3.5-4.5B indicate range in 3-month and 9-month Bills

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2030, 2040, 2044 and 2048 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.1% at 386.7, FTSE flat at 7392, DAX +0.2% at 13080, CAC-40 +0.20% at 5351, IBEX-35 +0.2% at 10040, FTSE MIB +0.3% at 22251, SMI +0.2% at 9318, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European Indices trade slightly higher across the board recovering from earlier weakness, in relatively quiet trade. Low cost airline carrier Easyjet reported a slight Rev beat, with a positive start to Q1 with shares up over 5%. Elsewhere Compass and Aggreko trades lower in the UK after earnings. Recent IPO Vapiano trades 7% higher on strong y/y earnings growth. Looking ahead notable earners include retailers Dollar Tree and ChicoFas, as well as engineering firm Jacobs and Lowes.

Equities

Consumer discretionary [Easyjet [EZJ.UK] +5.6% (Earnings), Kingfisher [KGF.UK] -1.2% (Earnings), Aggreko [AGK.UK] -9.1% (earnings), Vapiano [VAO.DE] +8.1% (Earnings)]

Consumer Staples [Compass Group [CPG.UK] -3.5% (Earnings)]

Industrials: [Babcock (BAB.UK] -2.3% (Earnings)]

Speakers

BOE members Cunliffe, McCafferty, Saunders and Vlieghe testified at Treasury Select Committee on recent quarterly inflation report

MPC member Cunliffe (dissenter) noted that inflation to peak in Q4. Had a cautious stance on wage outlook. Possible to wait before tightening

MPC member Vlieghe: stated that inflation to peak around this time if oil prices and GBP currently stayed steady. Outlook consistent with modest tightening

MPC member Saunders: CPI to stay above the 2% target for some time

MPC member McCafferty: Equilibrium unemployment rate might be below 4.5%

Italy Stats Agency (Istat) updated its Economic forecasts which raised 2017 GDP growth from 1.0% to 1.5% while cutting 2018 GDP growth from 1.5% to 1.4%

Italy Fin Min Padoan: Domestic economy showing signs of improvement with employment, production and exports rising

Italy PM Gentiloni: Budget law aimed at creating jobs

German Parliamentary leader Schaeuble (former Fin Min): Urges political parties to try to form a stable govt

German FDP official Theurer: New elections is not the next step, only last option. Too early to say if new coalition effort might succeed

Spain Fin Min de Guindos: Catalan region suffering from severe slowdown in Q4

Turkey Central Bank statement: Cuts banks borrowing rate limits at interbank overnight ops to zero (nil). To make all funding from late liquidity

RBA Gov Lowe: No strong case for near-term adjustment in policy. Competition to constraint inflation for a while. More likely that the next move in interest rates would be higher

Currencies

EUR/USD retested the weekly lows of 1.1722 and trying to downplay the political risks out of the euro area. German politics remained n focus following breakdown of Merkel's coalition talks. Merkel stated that she preferred new elections to a minority government

GBP/USD was higher in the mid 1.32 area on renewed hopes of progress in Brexit talks. The GBP was firmer for the 6th straight session for its best winning streak since June.

Analysts noted that Fed Chair Yellen to leave the Fed when her successor Powell takes her seat in February, increasing Fed vacancies. With so many replacements needed within its FOMC dealers noted that markets could turn increasingly uncertain about Fed policy

USD/TRY began the session with the Lira at fresh record low against the dollar 3.98 area. Dealers cited that lira-settled forward foreign-exchange sale auctions failed to ease the currency's selloff. Some stabilization did occur

Fixed Income

Bund futures trade 163.14 up 25 ticks, as a political deadlock in Germany continued to weigh on investors' confidence. Continued upside sees 163.40 then 163.63. A reversal targets 162.50 then 162.38.

Gilt futures trade at 125.23 up 43 ticks as Gilts break the 125.00 handle. Continued upside eyeing 125.675 then 126.47. Downside targets include 124.90 then 124.24.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.841T from €1.849T. Use of the marginal lending facility climbed to €273M from €214M prior.

Looking Ahead

(AR) Argentina Oct Budget Balance (ARS): No est v -31.4B prior

(AR) Argentina Central Bank Interest Rate Decision

(NG) Nigeria Central Bank Interest Rate Decision: Expected to leave Interest Rate unchanged at 14.0%

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (UK) DMO to sell 0.125 Mar 2026 I/L Gilts;

06:00 (UK) Nov CBI Industrial Trends Total Orders: +3e v -2 prior; Selling Prices: No est v 18 prior

06:00 (FI) Finland to sell €1.0B in 0.50% Sept 2027 RFGB bond

06:00 (TR) Turkey to sell 10.7% 2022 Bonds

06:30 (EU) ESM to sell €1.5B in 6-month bills

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (HU) Hungary Central Bank (NBH) Rate Decision: Expected to leave Base Rate unchanged at 0.90%

08:05 (UK) Baltic Dry Bulk Index - 08:00 (NZ) Fonterra Global Dairy Trade Auction

08:30 (US) Oct Chicago Fed National Activity Index: 0.20e v 0.17 prior

08:30 (CA) Canada Sept Wholesale Trade Sales M/M: 0.6%e v 0.5% prior

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:00 (BE) Belgium Nov Consumer Confidence: No est v 4 prior

09:00 (HU) Hungary Central Bank Gov Matolcsy post rate decision statement

09:05 (SE) Sweden Central Bank (Riksbank) Dep Gov Jochnick speech in Copenhagen

10:00 (FR) ECB's Coeure on panel in Frankfurt

10:00 (US) Oct Existing Home Sales: 5.40Me v 5.39M prior

11:30 (US) Treasury to sell 4-Week Bills

13:00 (US) Treasury to sell $13B in 2-year Floating Rate Notes (FRN)

15:00 (MX) Mexico Citibanamex Survey of Economists

16:30 (US) Weekly API Oil Inventories

16:45 (NZ) New Zealand Oct Net Migration: No est v 5.2K prior

18:00 US) Fed Chair Yellen speaks at Stern Business School

CRUDE OIL Bullish Pressures Continues

Crude oil has finished its consolidation and is now ready to challenge again its 1-year high. Expected to show further short-term bullish increase. Indeed the technical structure has a history of decent consolidation phase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

Rumors Make the Oil Go Up

The oil market has another reason to recover. At the beginning of last week, they were selling oil because there were rumors that Russia had no interest to extend the OPEC+ agreement, but at the end of it the price movement direction changed to the opposite. Saudi Arabia announced that Russia would support the OPEC+ agreement extension after March 2018.

The closer November 30th is, when the OPEC is going to have a meeting in Vienna, the more doubts investors have about future announcements and actions. Saudis say that the decision on the agreement will be announced during the meeting in Austria. "Oil bulls" like this possibility, but mostly because of hopelessness and lack of options: everybody knows that the organization has no plan "B".

The latest statistics from Baker Hughes published last Friday shows that by November 17th the Rig Count has increased by 8 and now equals 915 units. All 8 are gas rigs; the number of oil rigs hasn't changed. It turns out that the shale oil sector is still in stagnation phase. It's very unlikely that shale oil producers are afraid of the current commodity prices, because they look quite balanced and help to keep the production profitable. Financing may be a problem, because shale deposits can't be suspended. If a deposit is stopped, all operations will have to start anew.

A factor that may slow down "bulls" this week will be the updated API weekly crude oil stock report. The previous readings showed increase in stocks, which is reasonable as far as both seasonal factor and oil demand/supply balance are concerned.

From the technical point of view, the short-term trend for Brent is bearish, but the dominating one is still bullish. The short-term decline may move towards 60.30, because this area is a support level for both short- and long-term tendencies. If the price rebounds from this level, it may start a new rising impulse with the targets near the current high at 64.75 and the upside border of the long-term rising channel at 66.50.

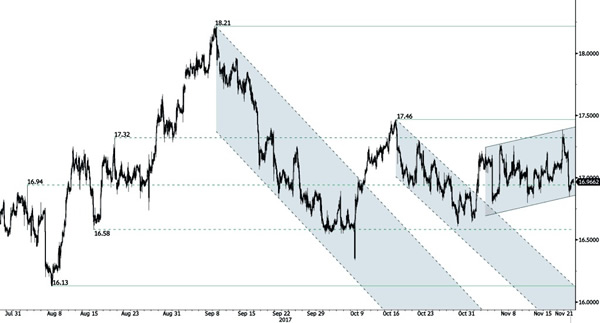

SILVER Increasing Slightly

Silver is heading higher. Hourly support can be found at 16.60 (27/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

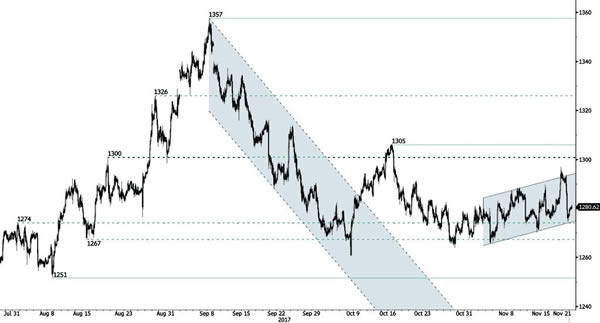

GOLD Bouncing On Rising Trendline Support

Gold is pushing higher. The technical structure confirms the end of the consolidation phase. Support lies at a distance at 1251 (08/08/2017 high). Resistance is located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN $10’000 Very Soon

Bitcoin has broken the $8000. The technical structure shows a tremendous positive shortterm momentum. Hourly support is located at 5605 (13/11/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the shortterm, the digital currency should continue rising.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Strengthening

EUR/CHF has broken key resistance at 1.1711 before bouncing back. Support is given at 1.1610 (27/10/2017 low). Expected to show continued bullish strengthening.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Wide-Open For Further Downside

EUR/GBP was rejected from rising trendline showing an aggressive reversal. Hourly support is given at a distance at 0.8733 (01/11/2017 low). Next resistance is located at 0.9014 (27/10/2017 high). Expected to go lower.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Break Of Key Support

AUD/USD is ready to go even lower showing that downside pressures are still lively. Hourly resistance is given at a distance at 0.7897 (13/10/2017 high). Expected to show renewed pressures towards key support at 0.7535 (22/06/2017 low).

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Short-Term Bullish

USD/CAD has failed to clear resistance indicating downside risk. Resistance at 1.2820 (07/11/2017 high) has been broken. Hourly support lies at 1.2667 (10/11/2017 low). Expected to show continued upside pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.