Sample Category Title

USD/CAD Canadian Dollar Lower Ahead Of Bank Of Canada

Bank of Canada expected to stand pat on Wednesday

The US dollar is trading higher against most major pairs. The EUR is the outlier as the USD is down against the single currency ahead of the European Central Bank (ECB) monetary policy announcement on Thursday. The Bank of Canada (BoC) is up first with the Canadian central bank set to releases its benchmark rate statement on Wednesday, October 25 at 10:00 am EDT. The central bank is anticipated to keep rates unchanged after an earlier unexpected rate hike in September that put the benchmark rate at 1.00 percent. A press conference by Governor Stephen Poloz will take place at 11:15 am EDT. Canadian data has underperformed and the loonie is on the back foot against the dollar following the optimism surrounding the Fed Chair announcement and US tax reforms.

US President Donald Trump is set to announce his pick to Chair the U.S. Federal Reserve before November 3. In an informal straw poll during a lunch with Republican Senate leadership Stanford economist John Taylor was the preferred choice. Markets still have Fed Governor Jerome Powell in the lead. Taylor’s approach to monetary policy is said to be more rule based versus Yellen’s data driven approach.

The USD/CAD gained 0.27 percent on Tuesday. The currency pair is trading at 1.2677 ahead of the monetary policy statement from the Bank of Canada (BoC). Investors are not expecting a change in the benchmark interest rate and will focus instead on the monetary policy report and the press conference by BoC governor Stephen Poloz. The Canadian economy surprised with impressive growth in the first half of the year. The pace of recovery prompted the central bank to remove the stimulus it had added in 2015. Restoring the benchmark interest rate to 1.00 percent with two rate hikes in 2017. The market is not pricing in another rate hike this year as the economy is showing signs of slowing down and there are uncertainties about NAFTA negotiations.

Canadian real estate prices have been cooled by the two rate lifts as well as newly announced mortgage rules will come into effect. Household debt has worried the government and the BoC which could leave rates at current level beyond the end of 2017. The U.S. Federal Reserve is not forecasted to keep rising rates beyond 2017 with the December meeting almost at 100 percent probability of a rate hike. Until a new Fed Chair is announced there will be uncertainty on what to expect from the central bank.

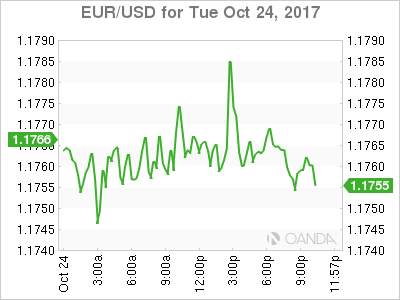

The EUR/USD gained 0.24 percent in the last 24 hours. The single currency pair is trading at 1.1779 after positive flash purchasing managers indices in manufacturing and services. The manufacturing PMI came in at 54.5 beating expectations as well as the services PMI that recorded a 55.9 reading. As the monetary policy decision announcement by the European Central Bank (ECB) approaches the EUR is beginning to rise as the market anticipates the reduction of the monthly bond purchases. The ECB is expected to taper its QE program from 60 billion euros, but at the same time extend the duration of the program to avoid putting the recovery of the eurozone in jeopardy.

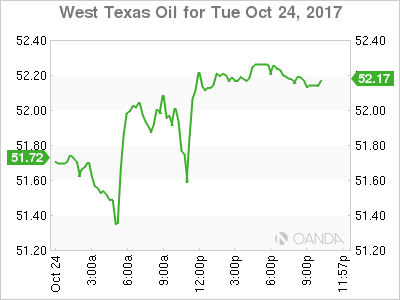

West Texas Intermediate is trading at $52.15 after Saudi Arabia once again is pleading to rebalance the energy market. An extension of the crude output deal involving the Organization of the Petroleum Exporting Countries (OPEC) and other major producers continues to makes the rounds. The current deal expires at the end of the first quarter of 2018, but talk of an extension could push it back until the end of the year.

The Energy Information Administration (EIA) will release the weekly US inventory data on Wednesday, October 25 at 10:30 am EDT. A 2.6 million drawdown is forecasted for US crude stocks.

Disruptions to the supply chain in Iraq are also keeping prices above the $52 price level. The fallout of the independence movement in Northern Iraq has resulted in the army moving into oil rich areas and supply has been restricted by about 200,000 daily barrels. The impact to global energy inventories is not massive as Southern Iraq houses the majority of production, but oil prices are sensitive to news about reduced supply.

Market events to watch this week:

Wednesday, October 25

4:30 am GBP Prelim GDP q/q

8:30 am USD Core Durable Goods Orders m/m

10:00 am CAD BOC Monetary Policy Report

10:00 am CAD BOC Rate Statement

10:00 am CAD Overnight Rate

10:30 am USD Crude Oil Inventories

11:15 am CAD BOC Press Conference

Thursday, October 26

7:45 am EUR Minimum Bid Rate

8:30 am EUR ECB Press Conference

8:30 am USD Unemployment Claims

Friday, October 27

8:30 am USD Advance GDP q/q

Gold Under Pressure Over Fed Chair Uncertainty

Gold has lost ground in the Tuesday session. In the North American session, the spot price for an ounce of gold is $1275.72, down 0.48% on the day. On the release front, Richmond Manufacturing Index slowed to 12 points, well off the forecast of 19 points. This marked its weakest gain since June. In the US, there are two key events – Core Durable Goods Orders and New Home Sales.

Gold prices have steadied this week, after the metal slipped 1.9 percent last week. Investor risk appetite increased as the US posted strong numbers last week, as employment, manufacturing and housing data beat their estimates. As well, the growing possibility that John Taylor could become the next head of the Federal Chair has hurt gold, as Taylor is considered a strong proponent of higher interest rate levels.

Who will take over at the Federal Reserve? The markets are keeping close tabs on the central bank, as Janet Yellen’s 3-year term expires in February. President Trump has said he will nominate a new Fed head in the coming days, and the front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen’s monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump’s choice for the new Fed chair could have an effect on monetary policy and the strength of the US dollar. Still, most economists are of the view that monetary policy will be largely driven by the performance of the US economy. Inflation levels remain weak and may not reach Fed’s target of 2 percent before 2020, but that has not dampened expectations of a December rate hike. According to CME FedWatch, the odds of a raise in December stand at 96 percent.

BOC To Back Off, Big Day Ahead

The 2nd half of the week is underway, featuring non-stop news including Wednesday's Bank of Canada decision. On Tuesday, the euro was the top performer while the New Zealand dollar lagged as the swoon continued. Bad news on the tax reform plan and chatter of a Taylor nomination (see standing in image below) confounded USD traders. Australian CPI, UK GDP and the BOC decision are up next.

USD/CAD touched the highest since mid-August on Tuesday in a sign that the market is less-worried about a hawkish Bank of Canada. USD/CAD broke the 100-day moving average and neared 1.27 as the +200 pip gain since Friday's soft retail sales reported extended.

That data point is a big reason why few expect another hike from Poloz. However the market is pricing in a 18% chance of higher rates because of the central bank's unpredictable recent history. If the BOC decides to remain on the sidelines, signals about the December meeting and beyond will be closely watched. The market is pricing in a 46% chance of a hike on Dec 6 and that rises to 72% for the January meeting. If the BOC moves to a clear neutral stance, expect a sharp rally in USD/CAD.

The other side of that trade is also dangerous. US 10-year yields broke above 2.40% Tuesday in a move that Bill Gross said could signal the end of the generational bond bull market. That helped to push USD/JPY briefly above 114.00.

At the same time, politics remains a dominant theme. USD fell on talk that Trump's tax cut plan doesn't have enough votes in the Senate. Competing with that was a report that John Taylor won an informal Senate Republican poll to be the next Fed Chair.

Aside from the BOC and Fed, look for big moves in the Australian and UK currencies. At 0030 GMT, the Q3 Australian CPI report is due and expected to show a 0.8% q/q rise. The trimmed mean is forecast at +0.5% q/q and a miss there will be a market driver.

At 0830 GMT, pound traders will be locked into the first look at UK Q3 GDP. The consensus is for a +0.3% reading and a miss in either direction will have major implications for GBP.

Pound Loses Ground, UK Preliminary GDP Next

The British pound has posted losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3123, down 0.55% on the day. On the release front, there are no British releases on the schedule. In the US, the Richmond Manufacturing Index softened to 12 points, well off the forecast of 19 points. This marked its weakest gain since June. Wednesday will be busy. The UK releases Preliminary GDP, with an estimate of 0.3%. In the US, there are two key events – Core Durable Goods Orders and New Home Sales.

Britain's manufacturing sector continues to expand, but the data is pointing to slower growth in the third quarter. CBI Industrial Order Expectations, which surveys sentiment among manufacturers, showed a decline for the first time in over a year. Earlier in October, two key manufacturing indicators softened. Manufacturing Production dipped to 0.4% in August, down from 0.5% a month earlier. Still, this beat the estimate of 0.2%. As well, Manufacturing PMI slowed to 55.9 in September, compared to 56.9 in August. Brexit is a constant concern for investors, and any signs of weakness in the economy could trigger the sell-off of British pounds in favor of safe-haven assets, such as gold and the Japanese yen.

Who will take over at the Federal Reserve? The markets are keeping close tabs on the central bank, as Janet Yellen's 3-year term expires in February. President Trump has said he will nominate a new Fed head in the coming days, and the front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have an effect on monetary policy and the strength of the US dollar. Still, most economists are of the view that monetary policy will be largely driven by the performance of the US economy. Inflation levels remain weak and may not reach Fed's target of 2 percent before 2020, but that has not dampened expectations of a December rate hike. According to CME FedWatch, the odds of a raise in December stand at 96 percent.

UK Pound Falls Amid Doubts Over Next Interest Rate Increase

The EUR/USD is consolidating within a narrow range as it waits for new drivers to encourage volatility. Mixed data from the Eurozone has not helped investors to pick a market direction. The preliminary report on flash manufacturing PMI showed growth of the indicator to 58.6 in October, which is 0.5 more than expected. On the other hand, preliminary data on flash services PMI showed a decline to 54.9 compared to 55.8 in September. Investors are waiting on ECB President Mario Draghi's speech on Thursday in search of a direction. Tomorrow the focus will be on the housing market report and durable goods orders in the US that may trigger sharp moves.

The sterling declined amid uncertainty around the possibility of an interest rate hike by the Bank of England. Investors are also skeptical about the outcome of negotiations between the UK and European Union, despite the progress that has been seen recently. Tomorrow the preliminary statistics on the country's GDP growth for the third quarter will be published. The GBP/USD was also under pressure from positive news on the growth of flash services PMI in the US for October, which grew to 55.9 against 55.3 in September.

Traders attention will turn to the consumer price index report in Australia early tomorrow morning at 00:30 GMT. If we see a growth in inflation, the Reserve Bank of Australia may look to tighten monetary policy despite earlier statements that the current interest rate level is reasonable.

EUR/USD

The single currency quotes are moving in a narrow range and after the end of the current consolidation we are likely to see a sharp movement in either direction. Breaking through the support at 1.1730 may become a trigger for the bears to pull the pair down to 1.1620 or even 1.1550. At the same time, we do not exclude growth resuming and in case of opening long positions with potential targets at 1.1825 and 1.1925, the stop should be set under 1.1730.

GBP/USD

The British pound is testing an important support level at 1.3150, breaking through it may be a stimulus for further drops with the next objectives at 1.3050 and 1.2950. We should note that currently the RSI on the 15-minute chart is close to the oversold zone, which indicates a potential rebound. An increase is likely to be limited by the inclined resistance line at the 1.3250 mark.

AUD/USD

The fall of aussie quotes has slowed and the price is consolidating at the moment. Previously the price broke the important 0.7800 level, which was the basis for further price declines to the target levels at 0.7740 and 0.7700. The MACD signal line is approaching zero and its crossing may point to a potential upward movement with correction to the SMA100 on the 15-minute chart and 0.7800 resistance line.

Trade Idea Wrap-up: USD/CHF – Buy at 0.9840

USD/CHF - 0.9892

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9877

Kijun-Sen level : 0.9870

Ichimoku cloud top : 0.9854

Ichimoku cloud bottom : 0.9810

Original strategy :

Buy at 0.9795, Target: 0.9895, Stop: 0.9760

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9795, Target: 0.9895, Stop: 0.9760

Position : -

Target : -

Stop : -

As the greenback has surged again after finding renewed buying interest at 0.9838, suggesting recent rise from 0.9421 low is still in progress and bullishness remains for this move to extend further gain to 0.9910-15, then towards 0.9940-50, having said that, near term overbought condition should limit upside and price should falter well below psychological resistance at 1.0000, bring retreat later.

In view of this, we are looking to buy dollar again on pullback as said support at 0.9838 should limit downside and bring another rise. Below the lower Kumo (now at 0.9810) would defer and risk test of support at 0.9796 but only break of latter level would add credence to this view, bring retracement of recent rise to 0.9775-80, however, support at 0.973037 should remain intact.

Trade Idea Wrap-up: GBP/USD – Sell at 1.3170

GBP/USD - 1.3120

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3163

Kijun-Sen level : 1.3171

Ichimoku cloud top : 1.3193

Ichimoku cloud bottom : 1.3158

Original strategy :

Sell at 1.3285, Target: 1.3155, Stop: 1.3320

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3170, Target: 1.3060, Stop: 1.3205

Position : -

Target : -

Stop : -

As cable met renewed selling interest at 1.3228 earlier today and has retreated sharply, suggesting the rebound from 1.3088 has ended there and bearishness remains for another test o said support, break there would extend the fall from 1.3338 to 1.3050, then towards recent low at 1.3027 which is likely to hold from here due to near term oversold condition, bring rebound later.

In view of this, wee are looking to sell cable on minor recovery as the Kijun-Sen (now at 1.3171) should limit upside and bring another decline. Above 1.3200-05 would risk another test of 1.3228, break there would bring a stronger rebound to 1.3240-45 (61.8% Fibonacci retracement of 1.3338-1.3088) but still reckon resistance at 1.3287 would cap upside.

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1763

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1760

Kijun-Sen level : 1.1751

Ichimoku cloud top : 1.1796

Ichimoku cloud bottom : 1.1762

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency broke below previous support at 1.1730, lac of follow through selling and the subsequent rebound from 1.1725 suggest further consolidation would take place and recovery to 1.1780-90 cannot be ruled out, however, still reckon upside would be limited to 1.1820-25 and price should falter well below resistance at 1.1858, bring further choppy trading later.

On the downside, below said support at 1.1725 would extend the fall from 1.1880 top to 1.1700 and possibly towards indicated previous support at 1.1669 but break of latter level is needed to retain bearishness and extend further subsequent decline to 1.1640-45 first. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

Trade Idea : USD/JPY – Buy at 113.40

USD/JPY - 113.95

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.78

Kijun-Sen level : 113.62

Ichimoku cloud top : 113.74

Ichimoku cloud bottom : 113.20

Original strategy :

Buy at 113.00, Target: 114.00, Stop: 112.65

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.40, Target: 114.40, Stop: 113.05

Position : -

Target : -

Stop : -

As the greenback found renewed buying interest at 113.24 and has staged a strong rebound, suggesting the pullback from 114.10 has ended and break of this level would confirm recent rise from 111.65 has resumed for headway to 114.45-50 (50% projection of 111.65-114.10 measuring from 113.24) but reckon upside would be limited to 114.75-80 (61.8% projection) and 115.00 would hold from here.

In view of this, we are looking to buy dollar again on pullback as 113.30-40 should hold, bring another rise. Below 113.20-24 (50% Fibonacci retracement of 112.30-114.10 and said support) would defer and bring correction to 112.95-00 (61.8% Fibonacci retracement) but reckon 112.60-70 and bring another rise later.

Yen Dips on Soft Japanese Manufacturing Report

USD/JPY has posted gains in the Tuesday session, erasing the losses at the start of the week. In North American trade, USD/JPY is trading at 113.95, up 0.45% on the day. On the release front, there are no major events on the schedule. Japanese Flash Manufacturing PMI came in at 52.5, missing the estimate of 53.1 points. In the US, the Richmond Manufacturing Index softened to 12 points, well off the forecast of 19 points. This marked its weakest gain since June. On Wednesday, the US will release Core Durable Goods Orders and New Home Sales.

Japanese voters went to the polls on Tuesday, and there were no surprises as Prime Minister Shinzo Abe cruised to an easy victory. Abe's Liberal Democratic Party and a small junior coalition party won a convincing victory, winning at least 312 seats out of 465 seats in the lower house of parliament. The result gives Abe a two-third majority in both seats of parliament, which will allow him to continue his policies. We can expect to see the ultra-loose monetary policy continue until inflation moves closer to the Bank of Japan's target of around 2 percent. Although Abe won a decisive victory, his popularity remains low. The LDP took full advantage of a divided opposition which failed to provide the Japanese voter with a credible alternative. The Tokyo stock markets posted gains after the election, but the Japanese yen responded with slight losses.

The guessing game at the Federal Reserve continues, as investors await the next choice for Federal Reserve chair. Janet Yellen's 3-year term expires in February, and President Trump has said he will nominate a new Fed head in the coming days. The front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have have an effect on monetary policy and the strength of the US dollar. Still, most economists are of the view that monetary policy will be largely driven by the performance of the US economy. Inflation levels remain weak and may not reach Fed's target of 2 percent before 2020, but that has not dampened expectations of a December rate hike. According to CME FedWatch, the odds of a raise in December stand at 96 percent.