Sample Category Title

Elliott Wave View: FTSE Intra Day

FTSE Elliott Wave view suggests that Primary wave ((4)) ended with the decline to 7199.5. Up from there, rally is unfolding as an impulse Elliott Wave structure where Minor wave 1 ended at 7327.5 and Minor wave 2 ended at 7289.75. Rally to 7494.34 ended Minor wave 3, and pullback to 7473.12 ended Minor wave 4. The last leg Minor wave 5 ended at 7565.11 and this also ended Intermediate wave (A) of a zigzag Elliott Wave structure from 9/15 low (7199.5).

Intermediate wave (B) is currently in progress as a double three Elliott Wave structure. From 7565.11 high, Minor wave W ended at 7485.42 and Minor wave X bounce ended at 7560.04. Near term, while bounces stay below 7565.11, expect the Index to turn lower towards 7431 – 7481 area to complete Intermediate wave (B). Afterwards, Index should resume the rally to new high or at least bounce in 3 waves. We don’t like selling the proposed pullback.

FTSE 1 Hour Elliott Wave Analysis

Trade Idea: GBP/USD – Sell at 1.3175

GBP/USD – 1.3135

New strategy :

Sell at 1.3175, Target: 1.3005, Stop: 1.3235

Position: -

Target: -

Stop:-

As sterling met resistance at 1.3228 yesterday and has retreated quite sharply, suggesting the rebound from 1.3088 has ended and test of this level is likely, break there would extend weakness to recent low at 1.3027 but break there is needed to retain bearishness and confirm recent decline has resumed for test of psychological level at 1.3000 and later towards 1.2950-60 which is likely to hold from here due to near term oversold condition.

In view of this, we are looking to sell cable on recovery as 1.3170-75 should limit upside and bring another decline. Above said resistance at 1.3228 would abort and prolong consolidation, then the rebound from 1.3088 may extend gain to 1.3270-75 but as outlook remains consolidative, reckon upside would be limited to 1.3287 and price should falter well below resistance at 1.3338. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

Trade Idea: GBP/JPY – Hold long entered at 149.50

GBP/JPY - 149.40

Original strategy:

Bought at 149.50, Target: 151.50, Stop: 148.90

Position: - Long at 149.50

Target: - 151.50

Stop: - 148.90

New strategy :

Hold long entered at 149.50, Target: 151.50, Stop: 148.90

Position: - Long at 149.50

Target: - 151.50

Stop:- 148.90

Although sterling fell to as low as 149.15 yesterday, as the pound found support there and has rebounded, retaining our bullishness and gain to 150.10 is likely, however, break of resistance at 150.50 is needed to signal the erratic rise from 146.95 has resumed for a retracement of the fall from 152.85 towards 151.00 but still reckon upside would be limited to towards resistance at 151.60 which is likely to hold from here, bring retreat later.

In view of this, we are holding on to our long position entered at 149.50. Below 148.90-00 would defer and risk weakness to 148.55-60, break there would signal top is formed instead, then weakness to indicated support at 147.80 would follow. Once this level is penetrated, this would signal the rebound from 146.95 has ended, bring weakness to another previous support at 147.30, below would confirm the fall from 152.85 has resumed for retest of 146.95. Looking ahead, below there would extend the fall from 152.85 top for retracement of recent upmove to 146.60-65 and then 146.00 but previous support at 145.25 should remain intact.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Trade Idea: EUR/JPY – Hold long entered at 133.20

EUR/JPY - 133.83

Original strategy:

Bought at 133.20, Target: 135.20, Stop: 132.60

Position: - Long at 133.20

Target: - 135.20

Stop: - 132.60

New strategy :

Hold long entered at 133.20, Target: 135.20, Stop: 133.10

Position: - Long at 133.20

Target: - 135.20

Stop:- 133.10

As the single currency found support at 133.10 and has rebounded again, retaining our bullishness and upside bias remains for a retest of recent high at 134.41, however, above this resistance is needed to confirm early upmove has resumed and extend headway to 135.00-10 and later towards 135.50-60 which is likely to hold from here due to overbought condition.

In view of this, we are holding on to our long position entered at 133.20. Below said support at 133.10 would defer an risk correction to 132.70-75 but only break of indicated support at 132.47 would abort and prolong choppy trading, risk weakness to 132.00, having said that, strong support at 131.66 should remain intact, bring another rebound later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

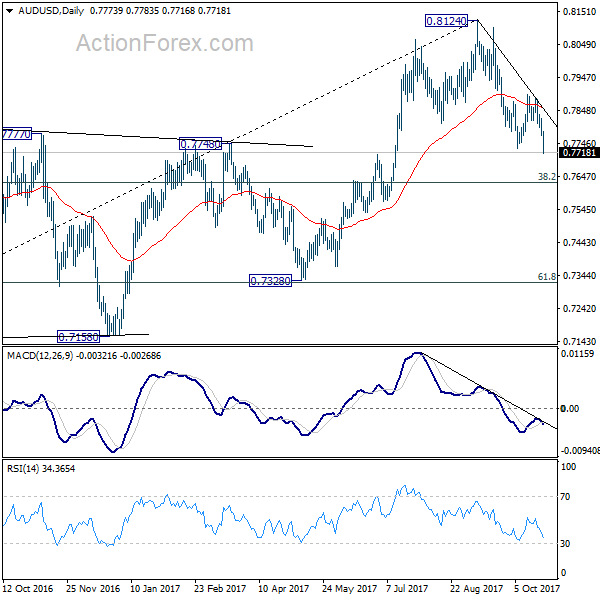

Trade Idea: AUD/USD – Hold short entered at 0.7875

AUD/USD – 0.7721

Original strategy:

Sold at 0.7875, Target: 0.7700, Stop: 0.7860

Position: - Short at 0.7875

Target: - 0.7700

Stop:- 0.7860

New strategy :

Hold short entered at 0.7875, Target: 0.7700, Stop: 0.7800

Position: - Short at 0.7875

Target: - 0.7700

Stop:- 0.7800

Aussie has dropped today and broke below previous support at 0.7733adding credence to our view that the decline from 0.8125 top has resumed, hence bearishness remains for this move to extend weakness to 0.7700 and later towards 0.7660-65, however, near term oversold condition should limit downside and reckon 0.7600 would hold from here.

In view of this, we are holding on to our short position entered at 0.7875. Above 0.7795-00 would defer and risk a stronger rebound to 0.7820-25 but Only break of latter level would defer and suggest a temporary low is formed instead, risk rebound to 0.7855-60 first, however, price should falter well below resistance at 0.7897.

On the 4-hour chart, recent upmove from 0.7329 is unfolding as an impulsive rise with wave 3 as well as smaller degree wave (iii) extending, only minor wave v of (iii) has ended at 0.8125, hence bullishness remains for this move to extend headway to 0.8200, then towards 0.8300, however, reckon upside would be limited to 0.8400 and the final wave 5 should falter below 0.8500, bring correction later.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7755; (P) 0.7790; (R1) 0.7809; More...

AUD/USD drops to as low as 0.7783 so far today. Break of 0.7732 support confirms resumption of decline from 0.8124. Intraday bias is back on the downside for medium term fibonacci level at 0.7628 first. Current development affirms the case of medium term reversal. Firm break of 0.7628 will pave the way to 0.7328 key support next. On the upside, above 0.7769 minor resistance will turn intraday bias neutral first. But outlook will remain cautiously bearish as long as 0.7896 resistance holds.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will affirm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Dollar and Yields Extended Rally on Tax Cut and Fed Chair Theme, Australian Dollar Plummets after CPI Miss

US equities surged to new record highs again while treasury yields jumped as tax plan and Fed chair position continued to be the theme that drove the markets. The developments also took Dollar generally higher. DOW closed up 167.80 pts or 0.72% at 23441.76, hitting all time high. S&P 500 and NASDAQ gained 0.16% and 0.18% too but lagged DOW in the record runs. 10 year yield jumped 0.030 to close at 2.406, above 2.396 key resistance, which is see as a bullish signal. TNX could now be heading to retest 2.621 high made back in December.

At this point, Dollar index is still limited below 94.14 key near term resistance. But that's mainly due to Euro's resilience, which is trading as the second strongest currency for the week, next to Dollar. The common currency is being supported by expectation of ECB tapering, to be announced tomorrow. Elsewhere in the currency markets, Australian Dollar tumbles sharply today after CPI miss. Aussie is even weaker than Kiwi, which is suffering from negative reactions to the policies of the new government.

For the day ahead, UK Q3 GDP will be a key to watch. While a BoE November hike is highly likely, that's not a done deal yet. Sterling could suffer if GDP growth misses expectations. German Ifo business climate is another focus in European session but that is unlikely to alter ECB's course. BoC rate decision is the main highlight in US session but that could be a non-event. US will release durable goods orders, house price index and new home sales.

Republicans united on tax plan, despite political rift with Trump

The feud between US President Donald Trump and some Republicans continued, including with Bob Corker and Jeff Flake. But recent developments suggest that while some Republicans would continue to heavily criticize Trump on political front, they are rather united regarding the tax plan. The rifts are not going to derail the push for completing the tax cuts by year end. It's reported that House Republicans are now prepared to take the Senate version of the tax plan in order to move forward swiftly, dropping some ideological demands. Reconciliation of the Senate and House version will be a big step forward.

Taylor got most "show of hands" in Fed chair race

Treasury yields are also supported by news that Stanford University economist John Taylor got the most "show of hands" in a closed-door lunch, where Trump asked the Republican senators who they prefer to be next Fed Chair. The White House noted that Trump is taking this decision seriously. While Taylor has been viewed as a hawk as the Taylor rule he created points to significant increase in the policy rate from the current level, his own monetary stance might not be so.

In his speech titled Rules Versus Discretion: Assessing the Debate Over the Conduct of Monetary Policy at the Boston Fed conference on October 13, Taylor noted that "one can easily adjust the equilibrium interest rate in the rule". He added that the most important suggested change in policy rules in recent years is probably to "adjust the intercept to accommodate the lower estimate of the equilibrium real interest rate (R*)". He appears content with the situation that the FOMC members have recently adjusted the average estimate of the neutral by "at least one percentage point lower" than the original 2%.

Aussie CPI miss suggests no RBA hike soon

Consumer inflation data from Australia surprised to the downside. Headline CPI rose 0.6% qoq in Q3, below expectation of 0.8% qoq. Annual rate slowed to 1.8% yoy, down from 1.9% yoy and missed expectation of 2.0% yoy. RBA trimmed mean CPI was unchanged at 1.8% yoy, missed expectation of 2.0% yoy. RBA weighted median CPI was unchanged at 1.9% yoy, below expectation of 2.0% yoy. The data suggested that it will be hard for RBA to considering raising interest rate any time soon.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7755; (P) 0.7790; (R1) 0.7809; More...

AUD/USD drops to as low as 0.7783 so far today. Break of 0.7732 support confirms resumption of decline from 0.8124. Intraday bias is back on the downside for medium term fibonacci level at 0.7628 first. Current development affirms the case of medium term reversal. Firm break of 0.7628 will pave the way to 0.7328 key support next. On the upside, above 0.7769 minor resistance will turn intraday bias neutral first. But outlook will remain cautiously bearish as long as 0.7896 resistance holds.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will affirm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | CPI Q/Q Q3 | 0.60% | 0.80% | 0.20% | |

| 0:30 | AUD | CPI Y/Y Q3 | 1.80% | 2.00% | 1.90% | |

| 0:30 | AUD | CPI RBA Trimmed Mean Q/Q Q3 | 0.40% | 0.50% | 0.50% | |

| 0:30 | AUD | CPI RBA Trimmed Mean Y/Y Q3 | 1.80% | 2.00% | 1.80% | |

| 0:30 | AUD | CPI RBA Weighted Median Q/Q Q3 | 0.30% | 0.50% | 0.50% | |

| 0:30 | AUD | CPI RBA Weighted Median Y/Y Q3 | 1.90% | 2.00% | 1.80% | 1.90% |

| 6:00 | CHF | UBS Consumption Indicator Sep | 1.53 | |||

| 8:00 | EUR | German IFO - Business Climate Oct | 115.1 | 115.2 | ||

| 8:00 | EUR | German IFO - Expectations Oct | 107.3 | 107.4 | ||

| 8:00 | EUR | German IFO - Current Assessment Oct | 123.5 | 123.6 | ||

| 8:30 | GBP | GDP Q/Q Q3 A | 0.30% | 0.30% | ||

| 8:30 | GBP | GDP Y/Y Q3 A | 1.50% | 1.50% | ||

| 8:30 | GBP | Index of Services 3M/3M Aug | 0.40% | 0.50% | ||

| 12:30 | USD | Durable Goods Orders Sep P | 1.00% | 2.00% | ||

| 12:30 | USD | Durables Ex Transportation Sep P | 0.50% | 0.50% | ||

| 13:00 | USD | House Price Index M/M Aug | 0.40% | 0.20% | ||

| 14:00 | CAD | BoC Rate Decision | 1.00% | 1.00% | ||

| 14:00 | USD | New Home Sales Sep | 556K | 560K | ||

| 14:30 | USD | Crude Oil Inventories | -5.7M |

Market Morning Briefing: Euro Rose To A High Of 1.1793 In The US Session Yesterday

STOCKS

Dow (23441.76, +0.72%) is back into the rally and yesterday's mentioned correction has not seen follow through to extend the dip further. Bulls continue to remain strong and may continue to dominate prices for the coming sessions. Test of 23500-24000 if seen would not be a surprise.

Dax (13013.19, +0.08%) is trading below immediate resistance near 13060-13100 and while that holds, the index could be trading within 13100-12900 region before deciding n further direction. For now 13100 seems to be an important resistance which could probably push the price to levels below 12900 in the medium term. Note a break above 13100, if seen would turn very bullish for Dax for the coming weeks.

Nikkei (21830.78, +0.12%) has some room on the upside on the weekly candles and could test levels near 22500 before facing some rejection from there back to levels near 22000-21500 in the coming weeks. For now, the uptrend remains intact with immediate target of 22000 and higher. Resistance on Dollar Yen (113.88) near 114.50 on the weekly would be crucial to keep an eye on. A sustained break above 114.50-115.00 if seen would invite fresh bulls and open up higher targets for the Dollar Yen.

Shanghai (3394.66, +0.19%) is open to test levels near 3410-3420 in the coming sessions. Near term looks bullish while the price trades above the 21-day MA clearly visible on the daily line charts.

Nifty (10207.70, +0.22%) has decent scope of testing 10400 on the upside in the near term. There is a possibility of the index opening with a gap up today trying to attempt higher levels of 10300-10320.

COMMODITIES

Gold (1274.06) seems to have broken below the immediate support on the daily candles and could test 1260-1250 levels while below 1280. Thereafter, a bounce back towards 1300 is likely.

Silver (16.88) could tets support near 16.60 before rising back towards 17 and higher.

Brent (58.38) has not been able to move above 58.60 in the past few sessions and could possibly come off today towards 57.50 or lower again. But on the longer term, we could see a rise towards 59.50-60.00. Near to medium term looks sideways to bullish.

WTI (52.43) would have to rise above 53 to turn bullish towards 54-55 levels in the medium term. But at the same time,there is resistance visible on the weekly candles that could possibly give some rejection near current levels or let the price rise towards 53-54 levels in the next couple of weeks.

Resistance on the 3-day candles on Copper (3.1950) is important and could keep the price range-bound for a few sessions before it starts to come off towards 3.10 and lower. Near term could be ranged sideways with longer term bearishness on the cards.

FOREX

Euro (1.1760) rose to a high of 1.1793 in the US session yesterday. The strength of the 1.1730-00 Support could be increasing a bit.

Dollar-Yen (113.90) rose again yesterday, negating the fall from 114.07 seen on Monday. This is a surprise and might signal a test of the long-term Resistance at 114.50. The Euro-Yen (133.88) has risen well alongwith the rise in Dollar-Yen and may be able to rise towards 135+ in coming days.

The Pound (1.3130) has proved our bearishness right after all, as the cited Resistance at 1.3250 has held well. Further sales from here could target 1.30 in the next few days from where a short-term bounce could be seen.

Contrary to expectation of Support at 0.7785, the Aussie (0.7727) has actually broken lower with some force, surprising us. However, some more Support may be available near 0.7700. Need to see if that holds/ breaks over today-tomorrow.

Dollar-Yuan (6.6419) trades further higher today and may well surpass the psychological 6.65%. Dollar-Rupee rose to 65.07 yesterday. Unsure of its possible movement today.

INTEREST RATES

Both the US 10Yr (2.42%) and German 10Yr (0.47%) have risen almost equally. The German-US 10yr Spread (-1.95%) has come down marginally.

Need to see if there is a good bounce from here or not. As mentioned yesterday, there is Support at 0.40% on the German 10Yr and Resistance in the 2.40-50% region on the US 10Yr.

In India, we need to see how the bond market reacts to the Bank Recapitalisation Plan announced yesterday. The 10yr GOI had come down a bit to 6.7820% yesterday.

The Aussie Dollar Plummets

The Aussie Dollar Plummets

The Aussie bulls are running for cover as the national CPI has missed the mark badly. The headline rose 0.6%QoQ versus 0.8% expected. The with the trim mean at 0.4%QoQ versus 0.5% both prior and consensus. Unrounded, the core came in at 0.37%, which is below the target band.

Implication along the AUD interest rate curve is significant as whatever glimmer of hope the RBA hawks had riding on the CPI print has quickly evaporated in a sea of red.

With the possible move to a more hawkish Fed policy still in play, the Aussie dollar bulls should remain sidelined. After the initial gap lower to .7745 an extension lower is in-game as the USD bulls clamour for downside AUD exposure.

And given the build-up of Long Aud versus its commonwealth peers AUDNZD and AUDCAD we should expect more AUD bloodletting as these positions head for the exits

The London open will be closely monitored as a test of .7700 looks more likely than not

There Is A Lot To Digest

There is a lot to digest

Investors are nearing a dizzying state of maximum overload given the sheer volumes of headlines, rumours and market whispers, they need to digest.

US politics dominated investor focus.President Trump visited Senate Republicans for lunch on Tuesday, and predictably traders took note of the market whispers surrounding Tax Reform and The Fed Chair.

The big news is that House of Republicans is now scheduled to release a full tax reform bill to the public next Wednesday, but Senate mutter tempered the mood as Republican Sens. Bob Corker, John McCain, Rand Paul may not support tax overhaul.

Trump canvassed Senators for their Fed Chair preference from the shortlisted Taylor Yellen and Powell. According to Senator Scott, Taylor “appeared to win.”.

The markets were unvoiced on the tax reform muckrake, but US 10 year yields popped higher on the Taylor straw poll victory which precipitated a break of the hugely significant 2.4% level. Breaching the 2.4 % level is tremendously convincing from both a psychological and technical perspective, as this barrier has acted as the principal benchmark for gauging both Fed and dollar sentiment.

USDJPY moved on both storylines: down 30pips on tax reform news approaching 113.50 then but then recovered to 113.958 on Taylor headline. There is no escaping these storylines and investors will have a lot on their plate absorbing these evolving narratives as uncertainty continues to reign.

There was a lot of jostling on the market overnight, but the sum of all parts points towards US equities, yields and USD higher. And while the USD in mainly bid in early APAC reversing Monday dollar swoon, positioning remains light in a very cautious market . Predictably so as currency moves have been lightning quick and unmediated at times.

Looking ahead

AUD CPI, where consensus is for +2.0% YoY. We have virtually nothing priced in for November, and the first full hike is only by November 2018.

And it should be a massive day for CNY as we’ll find out who the new Politburo Standing Committee consists of in a media rollout at 11:45 local time

The Euro

Trade continues to be somewhat lacklustre ahead of what is widely perceived as the ECB’s non-event of the year. None the less, the ECB will have to reduce its assets purchases to avoid breaching legal limits, but the consensus is the reduction will be relatively currency neutral. For the most part, traders are tuning in for the slim chance Draghi and Co will provide some definitive forward guidance.

The Euro continues to take its cue from USD sentiment.

The Japanese Yen

Buying any dips in USDJPY seems to be a no-brainer given recent political developments should mean Abe/Kuroda Redux in their never-ending quest to ensure a slightly weaker JPY. With Tokyo buying the 113.25 dip yesterday more than a few traders were burned chasing the dollar lower as the 113.20-30 held firm like a rock

USDJPY is back testing the rarified air around the 114.00 level waiting for some concrete news on tax reform and or Fed Chair. But with the market increasingly pricing in tax reform, it’s likely coming down the Fed Chair nomination to ignite the rocket engine and shoot USDJPY higher.

The Australian Dollar

The Aussie is suffering at the hands of US yields and as a result, we are back testing 2-week lows despite resounding commodity prices.

However, do not ignore today’s CPI print as higher than expected impression could lead to a notable shift in short-term interest rates sentiment and underpin the Aussie. But this too may only provide some temporary relief as the market looks to fade Aussie dollar strength.

The New Zealand Dollar

The Kiwi continues to wobble on political uncertainty. But when you throw in a dose of monetary policy uncertainty with the incoming Government poised to “review and reform ” the RBNZ, things get messy.

Asia EM FX

There is no escaping or avoiding the headline risk jitters. US bond yields are dictating the pace of play as local traders nervously bide their time. USDAsia will continue to track USDJPY as fast money rules with longer-term traders showing little appetite for risk.

Yuan

It will be interesting to gauge just how much of a “decisive role” the market will play in the economy into year end. So far these comments are following on deaf ear as its likely state-owned entities were keeping the market in check over the China summit to avoid any extreme awkwardness.

MYR

Its a big week for the Ringgit but with the Budget likely to target lower income groups the net effect should be stimulatory for the economy and support the local unit to a degree.

However, the market focus remains on the next Fed Chair and US tax reform. Recent tax reform headlines have proven positive for both US equity and the US dollar markets. Also, the prospect of a hawkish surprise on the Fed Chair has also underpinned USD sentiment. Asian FX is showing a robust correlation to the USD trend so we could be on the verge of a near-term crossroad that could see the broader USD push higher short-term and weaken the MYR towards 4.25 USDMYR support levels, more so on a hawkish Fed chair surprise.

While the MYR long-term outlook remains favourable, the possible short-term USD scramble on a more hawkish Fed Chair nod could present some headwinds to regional currency markets. I expect Traders will tread lightly this week given the level of market uncertainty.