Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.00; (P) 149.50; (R1) 149.95; More

Intraday bias in GBP/JPY remains mildly on the downside for 149.82 support. Break there will resume the correction from 152.82 and target 61.8% retracement of 139.29 to 152.82 at 144.45. Such decline is seen as a correction and we'd look for strong support from 144.45 to bring rebound. On the upside, above 151.38 will target a test on 152.82 high instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

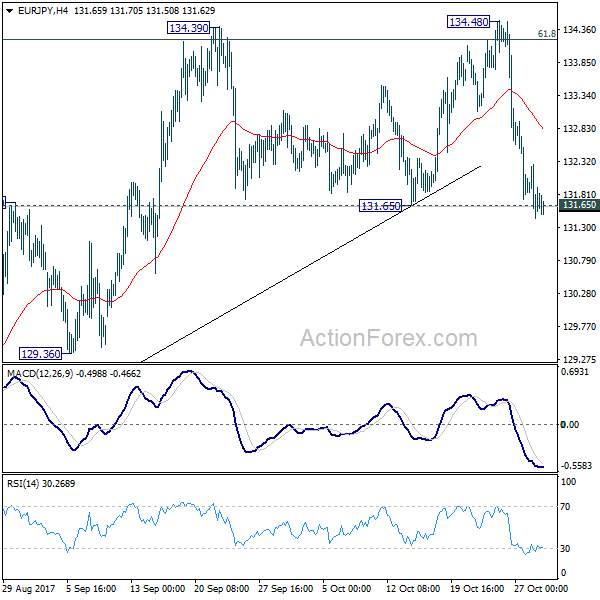

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.45; (P) 131.86; (R1) 132.28; More....

Focus remains on 131.65 key support in EUR/JPY Decisive break there will confirm rejection from 134.20 fibonacci level. That will also complete and double top pattern (134.39, 134.48) and confirms near term reversal. 55 day EMA will also be firmly taken out. In that case, deeper decline should be seen back to 127.55 key support. On the upside, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best.

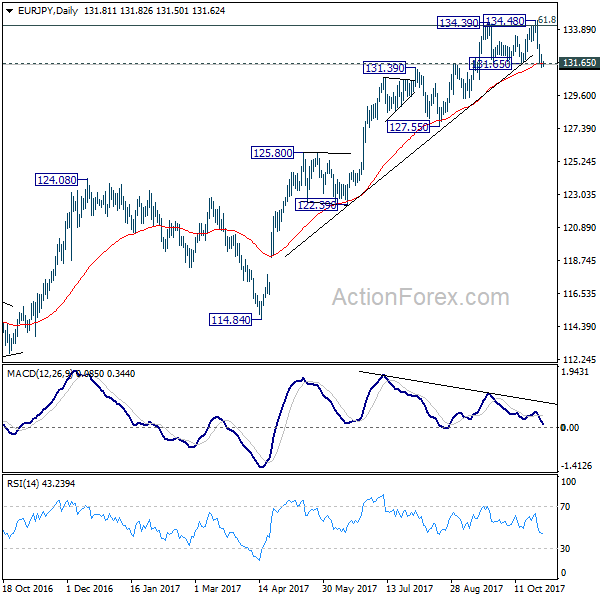

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

XAUUSD Intraday Analysis

XAUUSD (1275.48): Gold prices managed to post a modest rally as price cleared the minor support/resistance level of 1272. Having cleared this level, we could expect to see further gains that could push price towards the 1285 handle. However, in the medium term, the outlook for gold prices remains flat. A close above 1285 will be required in order to push prices higher towards the 1320 - 1324 region. To the downside, if price continues to consolidate near the 1272 level, we could expect to see a short term decline towards 1262.

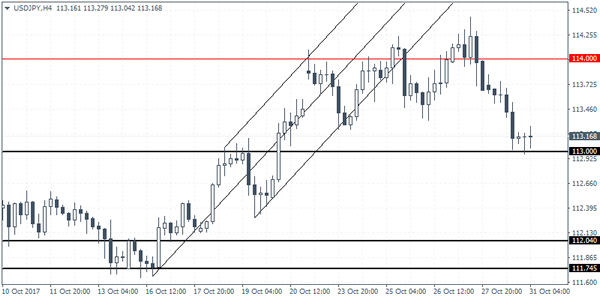

USDJPY Intraday Analysis

USDJPY (113.16): The USDJPY is showing sign of weakness as price action is currently seen hovering near the lower trend line of the rising wedge pattern. This pattern formed on the daily chart signals a possible downside price action. Support is seen at 110.70 which could be the likely target. On the 4-hour chart, USDJPY touched down to the support level at 113.00 briefly. We expect to see a modest rebound off this level as USDJPY remains flat within 114.00 and 113.00 price levels. A breakout to the downside below 113.00 will signal a move to the next support at 112.00 ahead of further declines that can be expected towards 110.70.

EURUSD Intraday Analysis

EURUSD (1.1636): EURUSD managed to close on a bullish note yesterday following two consecutive days of declines. Price action was however muted as the euro approaches the previously breached support level. If resistance is formed here, the EURUSD could be seen reversing the modest gains. Further downside could be expected as the currency pair is likely to follow through to the downside. The initial target level of 1.1552 is likely to be tested followed by further declines towards 1.5500 level of support. This will mark the minimum price objective to the downside, following the descending triangle pattern that was formed.

USD Pauses Ahead Of Trump’s Announcement On Fed Chair Nominee

The US dollar was seen pausing on its tracks on Monday. Lack of economic data saw the markets looking to the broader themes. President Trump is expected to announce his nomination for the next Federal Reserve Chair as Yellen's term ends in February next year. Political developments on the day also saw the former campaign manager, Paul Manafort facing charges in the Russia scandal.

On the economic front, the Bank of Japan held its benchmark interest rates steady at today's meeting. The central bank also retained its QE purchases steady signaling no change. The Japanese yen was seen trading stronger since Monday.

Looking ahead, the economic calendar today will see the Canadian GDP numbers. Economists estimate a 0.1% increase on the month in GDP. Later in the day, the BoC Governor Poloz is also expected to speak which brings some downside risks to the Canadian dollar. Later in the evening, New Zealand's unemployment figures will be coming out. The unemployment rate is forecast to fall to 4.7% from 4.8% previously.

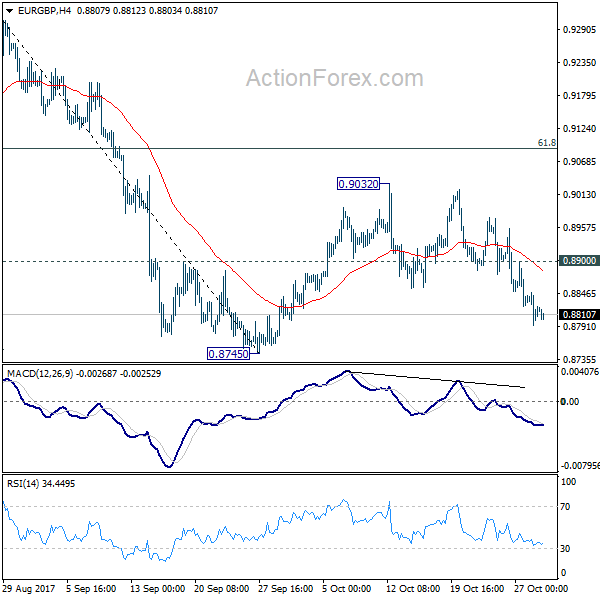

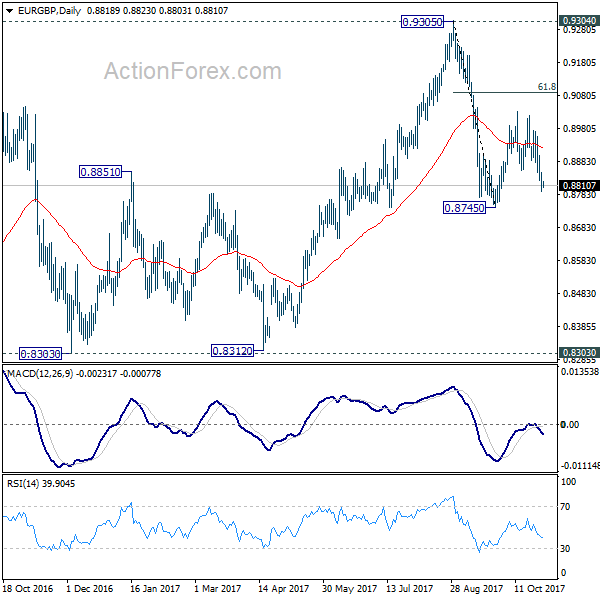

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8793; (P) 0.8820; (R1) 0.8849; More...

Intraday bias in EUR/GBP remains mildly on the downside for 0.8745 support. Break will resume whole fall from 0.9305 and target 0.8303 key support level. On the upside, above 0.8900 minor resistance will extend the corrective pattern from 0.8745 with another rise. But upside should be limited by 61.8% retracement of 0.9305 to 0.8745 at 0.9091 to bring fall resumption eventually.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Currencies: Dollar Rally Against Euro Stopped For Now

Sunrise Market Commentary

- Rates: Corrective upward bias remains in place

Last week's failed test of key US yield resistance levels (10y & 30y) induced technical-inspired buying. We hold our corrective upward bias today even if US activity data are expected strong. The German Bund could profit from disappointing core inflation though we fear that the ECB's 9-month APP extension removed market relevance of EMU data. - Currencies: Dollar rally against euro stopped for now

The euro regained some ground yesterday, but couldn't take out key resistance. Today, the eco calendar is busy and pressure mounts on president Trump after the prosecutor indicted former campaign chief Manafort. With some key events in the next days, traders will be cautious to put on aggressive positions

The Sunrise Headlines

- US stock markets eventually closed up to 0.35% lower as the Tech rally lost steam. Asian stock markets recover from initial weakness (Chinese PMI's) and are currently mixed.

- The Bank of Japan kept its massive monetary stimulus program unchanged even as it trimmed its inflation forecasts, signalling further divergence ahead from its global peers.

- Growth in China's manufacturing sector cooled more than expected in October (PMI dropped to 51.6 from 52.4) in the face of tighter pollution rules that are forcing many steel mills, smelters and factories to curtail production over the winter. The non-manufacturing PMI declined to 54.3 from 55.4.

- Court documents show that interactions between Trump's campaign and Russia occurred earlier and were deeper than previously documented. Former campaign chair Manafort and his partner are under house arrest after pleading not guilty to tax crimes, money laundering, conspiracy and lying to the FBI. Former advisor Papadopoulos cut a plea deal weeks ago and is cooperating.

- Spain's state prosecutor accused sacked Catalan leader Puigdemont of rebellion and sedition as the former regional president travelled to Belgium with other members of his ousted administration and hired a lawyer there.

- The IMF has warned that the increasing use of exotic financial products tied to equity volatility by investors such as pension funds is creating unknown risks that could result in a severe shock to financial markets.

- Today's eco calendar contains EMU CPI inflation, unemployment rate and Q3 GDP. In the US, S&P CS housing data, Chicago PMI and consumer confidence are on the agenda.

Currencies: Dollar Rally Against Euro Stopped For Now

EUR/USD fights back, but gains inconclusive

EUR/USD managed to eke out modest gains yesterday, but key resistance played its role, meaning the advance isn't significant. A euro rally attempt in the morning didn't go far (1.1644) and gains were undone when German inflation was weak and surprised on the downside. Special prosecutor Mueller's unsealed indictment against former Trump campaign director Manafort and revelations former foreign policy advisor Papadopoulos had lied against the FBI and is now cooperating with the FBI should have been a dollar negative, but its precise impact is difficult to measure. Anyway, the dollar lost ground across the board in the US afternoon session. US equities dropped lower and the US-German yield spread narrowed further, common drivers of the pair. EUR/USD moved back higher to 1.1660 and closed at 1.1652, a 45 ticks daily gain. The key resistance (1.1662) was untested. USD/JPY traded sideways until in the US session when lower yields and equities favoured the yen. USD/JPY closed at 113.20 versus 113.67 on Friday.

Overnight, Asian equities trade narrowly mixed, not too far from WS modest closing losses. US Treasuries are insignificantly higher. That's not enough to move USD/JPY , which is trading flat at 113.20, ahead of BOJ Kuroda's press conference. The BOJ, as expected, kept its policy unchanged, but revised down its inflation forecasts. The euro is weaker against dollar (1.1625 from 1.1650) and sterling (0.8805 versus 0.8821). EUR/USD failed yesterday to recapture the 1.1662 neckline head and shoulder formation, teasing Asian traders to sell the euro, but dollar gains are evaporating as the European opening nears. Eco calendar busy (see fixed income part: details)

We see some upside risk to Q3 GDP (0.6% Q/Q instead of 0.5% Q/Q?) that will remain strong anyway, while euro area HICP inflation should surprise on the downside after yesterday's weak German HICP. The key for market reaction will be the core inflation. Has it declined too? If so the euro might weaken. In the US, consumer confidence will be strong, maybe stronger than expected, and Chicago PMI should be strong too, but off last month peak value. The Cost Employment Index is expected to have rebounded. It is no strong market mover, but an upward surprise combined with strong activity data may be dollar positive

Dollar to make more corrective gains versus euro?

The technical picture points to more corrective gains of the dollar versus euro, but some hurdles may avoid these gains to crystallise today or in the next days. The FOMC meeting on Wednesday, while likely a non-event will keep traders cautious, as does the imminent choice on Thursday (?) of the next Fed chairman and the US payrolls on Friday. The judicial action in the Trump-Russian election campaign affaire is a wildcard. Regarding the eco data, activity data will be strong in the US and EMU, but a downward surprise in EMU core inflation could give the dollar an advantage today.

Longer term, the dollar failed to gain against the euro despite widening interest rate differentials since early September. This trading dynamic was broken after the ECB decision and extended on Friday. Policy divergence between the ECB and the Fed is again on the radar. A EUR/USD sell-on upticks bias remains favoured with 1.1662 an interesting level. Any additional rate support for the dollar will probably be modest near term, especially if Powell is nominated to succeed Yellen. So, further EUR/USD decline might develop gradually.

EUR/USD broke below 1.1662 support. Return action yesterday failed, but test may not be over.

EUR/GBP

Technicals: EUR/USD uptrend broken

From a technical point of view, EUR/USD dropped below 1.1670/62 support, which was re-approached yesterday. If the break is confirmed, it would signal that the uptrend in place since the turn of the year is broken, as the higher highs, higher lows pattern is shattered. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY's momentum was positive in September. The pair regained 110.67/95 resistance, a positive. The 114.49 correction top is the next resistance. Sentiment improved last week, but the first test on Friday failed. We don't preposition for a sustained break higher.

Sterling in ST positive flow

Sterling was already for some days in a positive flow and that continued yesterday. The UK eco calendar is empty today. Earlier this morning, consumer confidence was slightly weaker in October (but as expected), while Lloyds business barometer increased to 26 from 23. These are no market movers. Nevertheless sterling traded overnight again with a minor positive bias against the euro. For today, impetus should come from euro trading. If weak inflation hits the euro overall, sterling may make some more gains. However after a four day winning streak, the going will get tougher. The upcoming BOE meeting on Thursday should protect sterling against a significant countermove. Ahead of the BOE we expect sideways trading in the 0.8743 to 0.9033 range maybe with slight sterling gains on the basis of the technical elements. We maintain a EUR/GBP buy-on-dip bias but are in no hurry to add exposure.

EUR/GBP staged a strong uptrend from April till late August with a top at 0.9307. Rising UK inflation and the BoE preparing markets for a rate hike caused a sterling rebound, but it has run its course. EUR/GBP recently tried to regain the 0.90 area, but there were no follow-through gains. The drop below the 0.8855 area (neckline minor double top) on Friday may open the way for a return to 0.8743 or even 0.8652 supports. This area will be tough to break.

EUR/GBP: minor double top may push sterling correction a bit further. Still sell sterling on up-ticks.

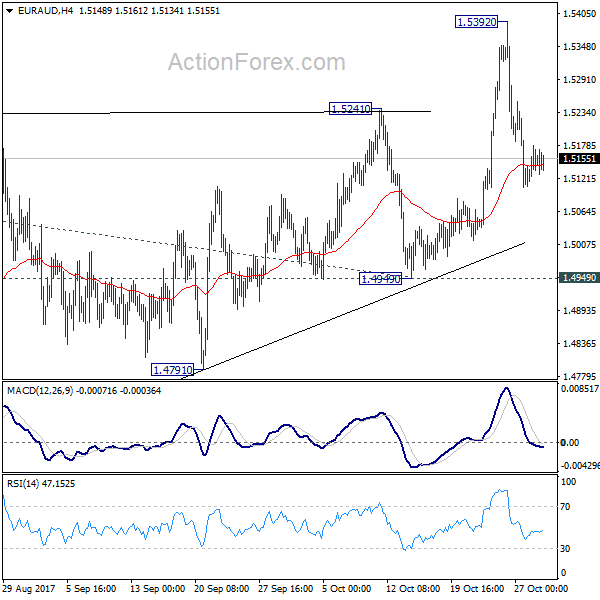

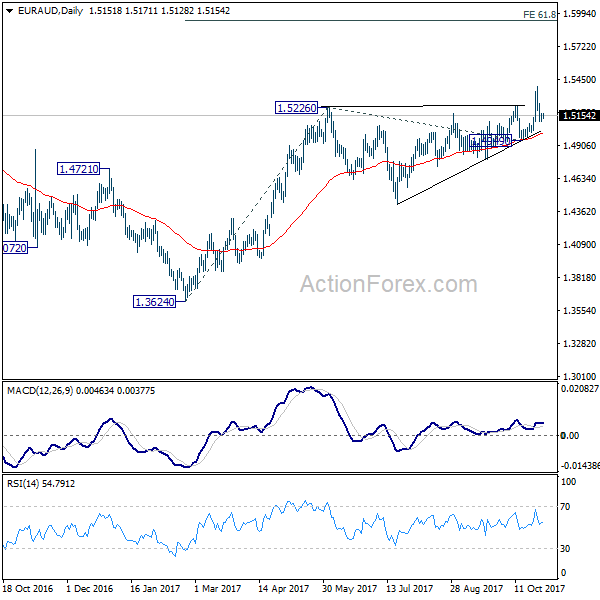

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5115; (P) 1.5146; (R1) 1.5185; More....

The corrective pull back from 1.5392 is still in progress and could extend lower. But after all, with 1.4949 support intact, outlook remains bullish and medium term rally is still in favor to resume. On the upside, break of 1.5392 will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. However, decisive break of 1.4949 will carry larger bearish implication and turn bias to the downside.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

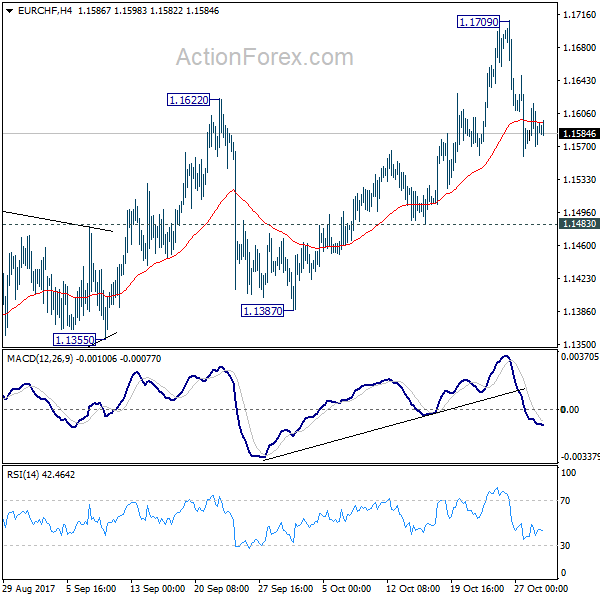

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1562; (P) 1.1590; (R1) 1.1613; More...

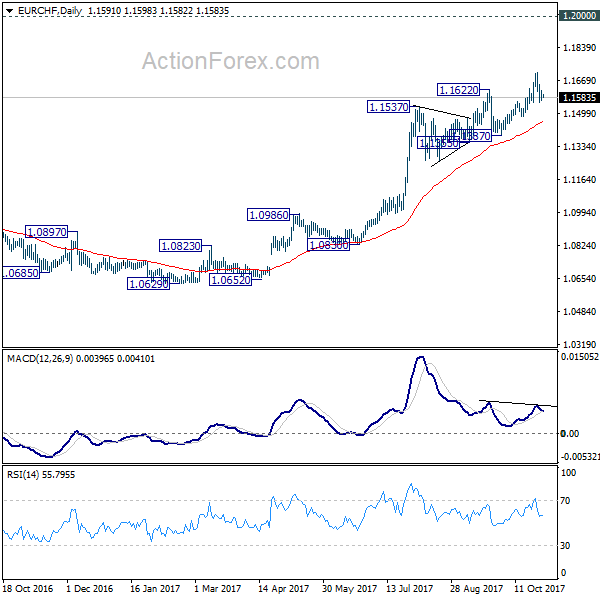

EUR/CHF's corrective pull back from 1.1709 is still in progress and could extend. But after all, as long as 1.1483 minor support holds, outlook remains bullish and we'd expect further rally ahead. Break of 1.1709 will target 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1067) and possibly below.