Sample Category Title

USD Basking In The Afterglow

USD Basking in the afterglow

The US dollar is basking in the afterglow of the ECB dovish turn. And while there remains an immense risk in global markets, the latest G-10 central banks dovish turn suggests there are fewer reasons for the USD to underperform this morning.

But when you factor in the new Fed chair is soon to be announced, robust USD economic data and the US House’s budget resolution vote passing, we could be on the verge of an extended US dollar rally

ECB president Draghi completely underwhelmed market expectations as the ECB erred on the side of caution. But the trap door was sprung when Draghi said QE is 'not going to stop suddenly.' The EURO plummeted as traders scurried to re-price the first ECB rate hike expectations well into 2019. And while the weaker euro should not be a means nor a goal of the ECB policy, it’s hard to overlook their recent concerns about the strengthening Euro weighing on exports, and we can only conclude this fear was significant factor in their policy decision

The US dollar then kicked into overdrive thanks to the US House’s budget resolution vote. The bill has passed 216-212, lifting USD and US 10y yields close to 2.45%.But given the slim margin of victory, it is still a footslog to Tax Reform passage due to the non-partisan Senate faction. Put extremely dollar positive turn of events none the less.

The Euro

Asia Traders are wasting no time this morning jumping on the bandwagon.But with the ECB rolling out Praet, Nowotny, and Weidmann for their policy views later today, 1.1600-25 could prove to be a stable interday support level until the airwaves clear.

The 'pain in Spain' is looking more tenuous and with Art155 likely to be triggered, near-term prospects for the EUR should continue to sour

Japanese Yen

Trader finds themselves in unfamiliar territory this morning now looking to ride the dollar wave rather than to fade it. This psyche is likely holding back a further extension of USDJPY move.With the USD dollar stars aligning and the BoJ seemingly committed to the relaxed monetary policy stance with Abe’s set to engage a whole new level of fiscal reform, this should undoubtedly prove detrimental for the JPY

The Australian Dollar

The Aussie dollar fell after an overly cautious RBA Deputy governer Debelle warned about weak wage growth.The lack of wage growth is one of the principal tenants in the lower Aussie dollar narrative as lack of any wage inflation to mollify the household debt burden will continue to weigh dovish on RBA policy.

AUD was then hammered mercilessly after the US House’s budget resolution vote passed as the Aussie the currency with the most to lose from the stronger US dollar and higher US interest rate storyline given the overtly dovish RBA outlook

Canadian Dollar

Adding to the Canadain Dollar swoon, Governor Poloz told the CBC 'a lot of things' need to come together before the bank is confident enough for a hike. Like so many other countries Canada is suffering from skyrocketing household debt, and without wage inflation to soften the burden, the BoC will likely be on hold for some time to come.

Gold And Silver On Shaky Ground

A rampant U.S. has gold longs watching long-term support nervously while silver, although still shakey, continues to outperform relatively.

Gold

Gold's incipient recovery came to an abrupt end overnight as the rally stopped dead at 1282.00 before gold plunged to close at 1267.00 in New York. It wilted in the face of a rampant U.S. dollar as the dollar index climbed by 1.20% overnight. In the process the 100-day moving average finally gave way on a closing basis, having held gold sell-offs for the week to leave gold poised dangerously near longer-term support.

How gold finishes the week will now be entirely at the whim of the U.S. dollar and U.S. yields with little to no geopolitical safe haven premium left in the price. The futures market is still constructively long the yellow metal, and this will continue to weigh on prices as fresh buyers appear to be few and far between.

Gold is unchanged at 1266.25 this morning with trendline resistance at 1272.50 followed by the 100-day moving average at 1275.50 and a triple daily top at 1284.00. The overnight low at 1265.80 is nearby support with a break opening up a possible test of 1260.00. This level is now crucial technical support being the October low and also the 200-day moving average. A daily close below this level may well see a lot of the long futures positioning deciding to hoist the white flag and head for the exit door.

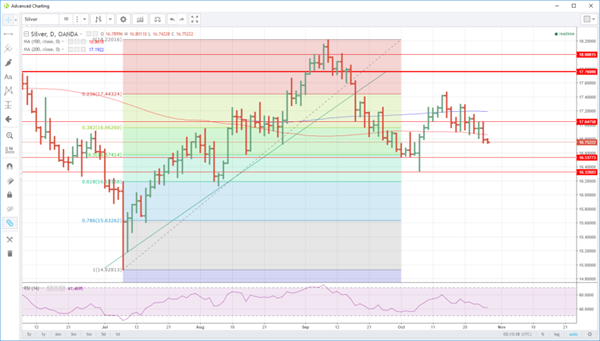

Silver

Silver tells much the same story as it to, fell through its 100-day moving average which had supported the price for the last seven days. Unlike gold though, silver has more technical support, and its selloff has been much less dramatic than golds. It may be because the level of speculative long positioning in the futures markets is substantially lower than golds.

Silver fell from 17.0475 to 16.7900 overnight and has continued to drift slightly lower in Asia to 16.7630. The 100-day moving average is now resistance at 16.8620, and it has formed a double top above at 17.04750 with the 200-day moving average behind this at 17.1925.

Support can be found initially at the overnight low of 16.7500. This is followed by a series of daily lows at 16.5375 as well as the 50% retracement at 16.5700. This should form substantial support, at least initially. Below this is the October low at 16.3270 and then the 61.80% retracement at 16.1900.

USD/CAD Canadian Dollar Lower After USD Surges On ECB Dovish Taper

The Canadian dollar fell against the US dollar on Thursday. There was no economic data on the Canadian calendar, with the market mostly focused on the European Central Bank (ECB) rate statement. The central bank delivered a compromised taper as expected. The ECB will halve the existing bond purchases down to 30 billion euros a month starting in January. The duration of the program was extended by 9 months to September 2018, although the door was open for extending even further if needed. The press conference with President Mario Draghi was even more dovish with the possibility of increasing bond buying if inflation conditions become less favourable and that there would be no sudden end to bond buying.

The lack of a hawkish ECB drove the USD higher as monetary policy divergence will continue to expand with the Fed expected to raise rates once again in December. The Bank of Canada (BoC) kept rates unchanged on Wednesday and also delivered a dovish statement which contrasted heavily with the hawkish comments that tipped the market about the July Canadian benchmark rate hike and the surprise September lift. After the October BoC meeting the probability of a rate hike in the remainder of 2017 are near 20 percent given the increasing headwinds and the unknown fate of the NAFTA agreement.

The Canada Mortgage and Housing Corp said today that the housing market boom is set to slow down in the next two years. Rising rates and a slowdown in the pace of growth of the economy will impact housing starts, with existing home sales to be affected as well. Prices will increase at a more moderate pace. The CMHC sees a 0.16 percent increase in 2018 and 2.4 percent in 2019.

The USD/CAD rose 0.41 percent on Thursday. The currency pair is trading at 1.2849 after the USD rose significantly on the back of a more dovish than expected ECB QE tapering announcement. The European Central Bank wanted to avoid a taper tantrum, and so far mission accomplished. European bond yields are lower after Mario Draghi did not set a specific timeline for the end of European QE. The US tax reform is closer to a reality with the house of representatives passing a budget resolution. US yields rose to 2.45 percent as Republicans are aiming to pass a tax bill before Thanksgiving.

The week will end with the release of the first estimate of the US gross domestic product (GDP) for the third quarter. Bureau of Economic Analysis will release the Advanced GDP at 8:30 am EDT with a forecast of 2.5 percent gain but a slowdown from the previous quarter at 3.1 percent. Much of the slowdown can be attributed to the negative effects of tropical storms that hit the US during the third quarter, but with overall temporary effects. Other US economic indicators have been positive despite the storm, so there is the possibility of the GDP performing better than expected on Friday.

There were no surprises from the Bank of Canada, which maintained the benchmark rate at 1.00 percent. In its rate statement, the Bank noted that wage growth levels remain weak, as there is slack in the labor market. Inflation pressure from wage growth remains muted, but the Bank did not provide a reason why inflation levels are so low. This problem is apparent south of the border as well, where a robust US economy and red-hot labor market has not translated into higher inflation. The cautious tone of the BoC did not impress investors, and the Canadian dollar shed close to 1.0 percent on Wednesday after the rate announcement.

Who will win the race to take over at the Federal Reserve? Janet Yellen’s 3-year term concludes in February 2018, and President Trump has said he will nominate a new Fed in the next few days. The front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen’s monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump’s choice for the new Fed chair could have a significant effect on monetary policy and the strength of the US dollar. If Taylor gets the nod, the US dollar could respond with gains of 3 percent or more.

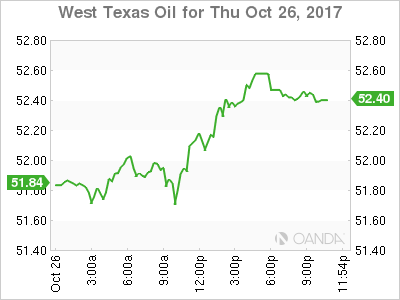

Oil prices rose on Thursday. West Texas Intermediate is trading at $52.40 finding some stability in the comments by Saudi Crown Prince Mohammed bin Salman who backed the extension of Organization of the Petroleum Exporting Countries (OPEC) production cut beyond its current March 2018 deadline. The group will meet in Vienna with Russia and other major producers on November 30 with the extension of the deal to be discussed.

Weekly crude inventories in the US rose 856,000, the first rise after four weeks when the forecast called for another big drawdown. Gasoline stocks dropped by 5.5 million barrels with a forecast that called for a mostly flat inventory statistic. Distillate stockpiles also had a massive drawdown of 5.2 million barrels. Heating oil demand drove the higher than expected demand.

Market events to watch this week:

Friday, October 27

8:30 am USD Advance GDP q/q

Gold Dips As Jobless Claims Beat Estimate, GDP Looms

Gold has posted losses on Thursday, erasing the gains which marked Wednesday trade. In North American trade, the spot price for an ounce of gold is $1272.78, down 0.37% on the day. On the release front, unemployment claims climbed to 233 thousand, just below the forecast of 235 thousand. As well, Pending Home Sales rebounded, coming in at 0.0%. The indicator has struggled, recording five declines in the past 6 months.

It’s report card day for the US economy on Friday, with the release of Advance GDP. The markets are forecasting a gain of 2.5%, after Preliminary GDP posted a sharp gain of 3.0%. US economic numbers remain strong, and the labor market is close to capacity. At the same time, inflation has not moved higher, and wage growth has been weaker than expected. Despite the lack of inflation, the odds of a December rate hike have soared in recent weeks, with the odds of a rate raise at 96%, according to CME FedWatch.

The White House has yet to make a decision on the new Federal Reserve chair, but the latest media reports are that John Taylor or Jerome Powell will get the nod, replacing Janet Yellen. The choice of the new chair could have significant ramifications for interest rate policy as well as the US dollar. Powell is expected to follow Yellen’s stance of incremental rate increases, while Taylor is a proponent of much higher rate levels, which could propel the dollar upwards. President Trump is expected to make his choice before embarking on a tour of Asia on November 3, so traders should be prepared for an announcement next week.

Euro Crumbles, Dollar Soars

Draghi gave himself the flexibility to keep QE going beyond Sept 2018 and the market sent EUR/USD to the lowest since July. The US dollar was the top performer Thursday while the euro lagged. Japanese CPI is due up next. One EURUSD Premium trade was closed at gain, while a new one was opened, currently at a loss.

We warned ahead of the ECB decision that Draghi would want to preserve the option of continuing QE beyond September. “The market could interpret the flexibility as dovish and send the euro lower,' we wrote. “In addition, the large net-long EUR position could be waiting to 'sell the fact' on a taper announcement.'

That's what happened as EUR/USD broke the October and August lows to break the neckline of a well-defined head-and-shoulders pattern. It would be wrong to give all the credit to the euro, the US dollar was broadly stronger and finished at the highs of the day. Commodity currencies weakened substantially and cable reversed virtually all of Wednesday's climb.

Pefect USD Storm?

A driver of USD strength is the bond market as 10-year yields consolidate above 2.40%. A soft 7-year auction added to the bond move, along with the House passing a budget motion that brings a tax cut closer. A report from Politico also said Yellen is out of the running for the Fed chair and that it's now between Taylor and Powell.

The yen will be in focus in the hours ahead with September CPI numbers due at 2330 GMT. The consensus is for a 0.7% y/y rise on the headline and +0.2% y/y on ex-fresh food and energy. Abe is rumored to have asked for a extra budget as he restarts efforts to get the economy moving and inflation higher.

ECB Plans to Keep Interest Rates Unchanged for Some Time

The EUR/USD quotes fell sharply following the ECB's decision to maintain the asset purchasing program until September 2018 but will halve it to 30 billion euro of monthly purchases from January. At the same time Mario Draghi noted that interest rates will not be changed for a long time and will be increased only after the end of the asset purchasing program. These announcements along with the possibility of an interest rate hike in the US this year may see the price of the euro-dollar fall to 1.1500 or lower. Investors' activity today is restrained as they wait for tomorrow's release of GDP data in the US which is likely to lead to significant moves.

The single currency experienced some pressure at the beginning of the trading session from the news on the decline of the German Gfk Consumer climate index to 10.7 in November which is 0.1 below the forecasted figure. On a positive note for the euro, the unemployment rate in Spain fell to 16.4 in the second quarter which is 0.2% better than forecasted and 0.8% less than in the previous period.

The NZD/USD price continued to move within the descending channel after disappointing news on the trade balance in New Zealand. The trade deficit for September grew to $1143 million against the $900 million forecasted.

The USD/JPY resumed positive dynamics on the background of the US dollar strengthening. Volatility levels are likely to remain high due to the expected releases of Japan's consumer price index at 23:30 GMT and the US Gross Domestic Product tomorrow at 12:30 GMT.

EUR/USD

The EUR/USD quotes demonstrated a sharp descending move after ECB President Mario Draghi's statement. As a result, the quotes approached a strong support line at 1.1730, and breaking through it may become a trigger for the bears to pull the price down to 1.1620 or even to 1.1550. The RSI on the 15-minute chart is in the oversold zone, which points to a possible price rebound within the correction.

USD/JPY

The USD/JPY price rebounded from the inclined support line and continued to move along it. Gaining a foothold above the 1.1400 mark may become a firm basis for further price growth to 114.70 and 115.00. On the other hand, breaking through the angled support may result in a further fall to 113.00. Volatility is likely to remain high until the end of the week.

NZD/USD

The NZD/USD was able to fix below the 0.6890 and continued the descending movement within the limits of the channel. The immediate target in case of maintaining the current impulse will be at 0.6825. It's less likely that the trend will change to positive and the basis for it doing so may come from fixing above the upper limit of the descending channel and 0.7000 mark.

Pound Slips as Retail Sales Nosedive

The British pound has posted considerable losses in the Thursday session. In North American trade, GBP/USD is trading at 1.3176, down 0.66% on the day. On the release front, British CBI Realized Sales plunged in October, with a reading of -36 points. This surprised the markets, which expected a gain of 14 points. In the US, unemployment claims climbed to 233 thousand, just below the forecast of 235 thousand. As well, Pending Home Sales rebounded, coming in at 0.0%. The indicator has struggled, recording five declines in the past 6 months.

The pound recorded strong gains on Wednesday after British Preliminary GDP beat expectations in the third quarter. However, the rally proved to be short-lived, as the currency has given up much of these gains on Thursday. GBP/USD responded with losses after a dismal British CBI Realized Sales report. The soft reading, which was the sharpest drop since March 2009, was all the more surprising because the September reading showed a strong gain of 42 points. High inflation is likely having a chilling effect on consumer spending, a key driver of economic growth. The BoE will be taking note of the sharp drop in retail sales, as the Bank must decide at the November 2 meeting whether to raise rates for the first time in a decade. Policymakers remain divided over a rate hike, which would be the first in a decade. Proponents of a rate increase point to inflation running at 3.0%, above the Bank's target of 2.0%, but opponents argue that the economy is showing signs of weakness and a rate hike could hamper economic growth.

It's report card day for the US economy on Friday, with the release of Advance GDP. The markets are forecasting a gain of 2.5%, after Preliminary GDP posted a sharp gain of 3.0%. US economic numbers remain strong, and the labor market is close to capacity. At the same time, inflation has not moved higher, and wage growth has been weaker than expected. Despite the lack of inflation, the odds of a December rate hike have soared in recent weeks, with the odds of a rate raise at 96%, according to CME FedWatch.

CAC Higher as Investors Expect ECB Taper

The CAC index has posted gains in the Thursday session. Currently, the CAC is trading at 5,404.75, up 0.58% on the day. On the release front, the ECB will release its rate statement, followed by a press conference with ECB President Mario Draghi. On Friday, the US releases Advance GDP.

The CAC remains at high levels, and on Wednesday, the index hit its highest level since mid-May. Will the upward movement continue after the ECB policy meeting? No change is expected in interest rates, which are currently at 0.00%. However, Mario & Co. could significantly trim the ECB's asset purchase program (QE). Currently, the ECB is purchasing EUR 60 billion/mth, and there is a strong likelihood that this amount will drop to EUR 30 billion/mth. The stronger eurozone economy is the catalyst behind a taper, but with inflation persistently at low levels, the ECB is expected to announce to extend the program well into 2018 or even later. Eurozone members remain divided as to whether the ECB should signal a clear commitment that it plans to wind up QE. Germany and the Netherlands are in favor of a quick exit, but other members want the scheme to remain open-ended, so that the ECB can continue with extensions, if needed. ECB policymakers will need to perform a balancing act between these views as it shifts its monetary policy.

The French economy has rebounded this year, and service and manufacturing reports on Wednesday suggest that fourth quarter growth will be strong. Manufacturing and Services PMIs came in at 56.7 and 57.4 points respectively, both which beat expectations. The French government is determined to overhaul the economy and has targeted public spending, with plans to cut 120,000 civil servants. The government also expects that the deficit will drop below 3 percent of GDP in 2017, in keeping with EU guidelines. Last year, the deficit stood at 3.4 percent of GDP.

Trade Idea Wrap-up: USD/CHF – Buy at 0.9900

USD/CHF - 0.9958

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9929

Kijun-Sen level : 0.9919

Ichimoku cloud top : 0.9911

Ichimoku cloud bottom : 0.9889

Original strategy :

Buy at 0.9900, Target: 1.0000, Stop: 0.9865

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9900, Target: 1.0000, Stop: 0.9865

Position : -

Target : -

Stop : -

As the greenback has surged again after finding renewed buying interest at 0.9869, adding credence to our bullish view that recent rise from 0.9421 low is still in progress and may extend further gain to 0.9970, having said that, overbought condition should limit upside to psychological resistance at 1.0000 and reckon 1.0030-40 would hold, bring retreat later.

In view of this, we are looking to buy dollar again on pullback as 0.9900-05 should limit downside and bring another rise later. Below said support at 0.9869 would abort and suggest a temporary top is formed instead, bring correction of recent rise to another previous support at 0.9838.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3180

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3208

Kijun-Sen level : 1.3220

Ichimoku cloud top : 1.3191

Ichimoku cloud bottom : 1.3191

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite rising to 1.3279, as cable has retreated after faltering below indicated resistance at 1.3287, suggesting further choppy trading would take place and weakness to 1.3155-60 cannot be ruled out, however, reckon yesterday’s low at 1.3110 would hold and bring another bounce later. Only a break of this level would revive bearishness and signal decline has resumed for retest of 1.3088 first.

On the upside, whilst recovery to 1.3235-40 cannot be ruled out, reckon upside would be limited and said resistance at 1.3279-87 would hold, bring further choppy consolidation. Only a break of said resistance area would signal the fall from 1.3338 has ended at 1.3088, bring further gain to 1.3300-05 but said resistance at 1.3338 should remain intact. As near term outlook is still mixed, would be prudent to stand aside for now.