Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3110; (P) 1.3195; (R1) 1.3244; More....

GBP/USD is still gyrating in range of 1.3026/3337 at this moment. And intraday bias stays neutral first. On the downside, break of 1.3026 will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. Meanwhile, on the upside, break of 1.3337 will resume the rebound from 1.3026 to 61.8% retracement of 1.3651 to 1.3026 at 1.3412 and above.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

ECB Extends QE But Halves The Pace

Market movers today

After an intense central bank day yesterday, the data calendar is fairly thin today and hence market focus will probably be on absorbing yest erday's policy message from the ECB.

Russia. The cent ral bank (CBR) will release its decision today. While a 25bp cut to 8.25% is widely expected (Bloomberg consensus and Danske Bank), there is a possibility that the CBR could do more and deliver a 50bp cut , or do nothing and keep the key rate unchanged. However, a cautious cut would be well justified, in our view, given that inflation has hit its post -Soviet lowest at 3.0% y/y, falling far below the CBR's t arget of 4.0% y/y. On t he other hand, inflation expectations remain st icky, declining marginally. The CBR has been cautiously hawkish in its inflation comments recently and are not concerned about the high real rates. In it s Friday's statement , we expect the CBR to praise economic development, enhancing the need for firmer CPI, anchoring around the target in the long run. We expect the key rate to end up at 8.00% by end-2017.

US. We are due to get the first estimate of Q3 GDP growth today, which is likely to have been affected negatively by the hurricanes, making it more difficult to estimate. While the At lant a Fed's GDP indicator says growth was 2.7% q/q AR, the New York Fed's indicator says 1.7% q/q. Our est imate is 2.0% q/q AR. Even if we get a weak print , it should be temporary and it would not change our view that the US is in the middle of an expansion. Of interest is also the PCE core number where consensus is looking for 1.3% q/q AR growth, up from 0.9% in Q2.

Selected market news

ECB extends QE but halves the pace. As broadly expected in the market and in line with our forecast , the ECB yesterday announced an extension of its QE programme by nine months unt il September 2018, albeit at a reduced pace of EUR30bn compared to EUR60bn current ly. Importantly, the ECB also left its forward guidance unchanged and retained the possibility to extend the QE programme in size and/or durat ion, leaving it open-ended. Furthermore, ECB reiterated that policy rates will remain at their current levels for an extended period of t ime and well past the horizon of asset purchases. The ECB also released further details on the reinvestments of maturing bonds that are made alongside new QE purchases and which wil l become increasingly sizable over the course of 2018. See our ECB review for further details.

Weaker euro, support to bond markets . The market react ion in the wake of the meet ing suggests t raders had posit ioned for a more hawkish tone at the press conference. The euro weakened and around the t ime of the European market close, EUR/USD had fallen by around 1% to 1.1650. European fixed income rallied, benefitting peripheral markets the most with, e.g. Spanish and Italian 10Y yields falling 9bp and 7bp respect ively into the close.

Oil prices rallied late yesterday. The price on Brent crude topped USD59/bbl on the news that the House in the US passed a bill on non-nuclear sanct ions on Iran. The oil market is concerned that the harder stance on Iran could eventually lead to a repeal of the 2015 nuclear deal and reinst at ement of sanctions on Iran's oil exports.

Market Update – Asian Session: US Dollar Gains Ahead Of Q3 GDP Data

Asia Summary

Asian equity markets have opened the session mostly higher, as most of the US equity indices ended up. In the US afterhours, shares of Microsoft, Amazon and Alphabet all rose following their respective earnings reports. Nasdaq Futures are up over 0.2%

Japanese tech companies, Fujitsu and Seiko Epson have each declined by over 6% on weaker than expected financial results.

However, the Nikkei 225 has risen by over 0.9%. Fuji Electric has gained over 13% as the company raised its FY forecast. Softbank has traded higher by over 0.7%, while Fast Retailing has gained over 1.5%. Japanese ‘mega banks’ are trading higher on the session, with shares of Mitsubishi UFJ gaining by over 1.5%.

Australian financial, Macquarie Group has gained over 3%, after reporting its H1 results and announcing an A$1B stock buyback. Dairy producer Murray Goulburn is higher by over 10% after receiving an A$1.31B takeover offer from Canada’s Saputo.

South Korea’s LG Chemical has gained over 2%, following speculation that the company could receive a battery order from Tesla. Kia Motors has traded slightly higher after the company reported better than expected Q3 results.

Hong Kong listed Wynn Macau has traded lower by over 0.3%, after releasing its quarterly earnings report. Great Wall Motor’s shares have lost over 1% following Q3 earnings. At the same time, the overall Hang Seng index has risen by over 0.7%. Shares of Guangzhou Auto are up over 5% after its Q3 figures. Chinese insurers have continued to rise as China’s government bond yield is near multi-year highs.

Earlier today, China’s 10-year bond yield hit the highest level since Dec 2014. In terms of the country’s US dollar denominated bond sale, orders for the 5 and 10-year bonds are said to total around $21B. The PBoC said that it would inject CNY50B into the money markets with a 63-day reverse repo at 2.9%.

On the macro front, industrial profits growth for Chinese companies accelerated to 27.7% in Sept vs. 24.0% prior. According to the government, the data was driven by lower costs and improving trends were noted for Q4.

JGB Futures are little changed. The earlier released Sept national CPI figures for Japan held steady versus the prior data.

In the currency markets, the US dollar has traded broadly firmer. The Euro has added to the losses seen in the aftermath of Thursday’s ECB policy meeting. The Aussie has declined by over 0.2%. According to Australia’s High Court, Deputy PM Joyce is not eligible to serve in parliament due to dual citizenship. The court ruling could cost the government its majority in parliament, according to press reports. Looking ahead, US Q3 preliminary GDP figures are due later today.

Japanese companies expected to report results later today include Chubu Electric, East Japan Railway, HOYA, Kansai Electric, Komatsu, Nippon Steel, Nippon Light Metal, Nissin Steel, Sharp, Shin-Etsu Chemical and Tokyo Gas.

US corporate earnings are expected to include Chevron, Colgate, Exxon, Goodyear Tire, Huntsman, LyondellBasel, Merck, Phillips 66 and Weyerhaeuser.

Key economic data

(CN) CHINA SEPT INDUSTRIAL PROFITS Y/Y: 27.7% V 24.0% PRIOR

(JP) JAPAN SEPT NATIONAL CPI Y/Y: 0.7% V 0.7%E; EX FRESH FOOD (CORE) Y/Y: 0.7% V 0.7%E

(JP) TOKYO OCT CPI Y/Y:-0.2% V +0.1%E; EX FRESH FOOD Y/Y: 0.6% V 0.5%E

(AU) Australia Q3 PPI Q/Q: 0.2% v 0.5% prior; Y/Y: 1.6% v 1.7% prior

(KR) South Korea Oct Consumer Confidence: 109.2 v 107.7 prior

Speakers and Press

Other

(HK) Hong Kong to begin pilot related to dual-class shares in 2018 - HK Press

(JP) Japan Economy Min Motegi: CPI is flat, but output gap is improving and wages have been rising for past 4 years; need to confirm that there is no risk of returning to deflation

(US) Fed Chairman position contender John Taylor: Lower US growth due to economic policy

Asian Equity Indices/Futures (00:30ET)

Nikkei +1.2%, Hang Seng +0.8%, Shanghai Composite +0.3%, ASX200 -0.5%, Kospi +0.6%

Equity Futures: S&P500 +0.1% ; Nasdaq +0.3% , Dax +0.2% , FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1625-1.1658; JPY 113.97-114.27; AUD 0.7626-0.7664; NZD 0.6818-0.6846

Aug Gold flat at1,269 /oz; Aug Crude Oil flat at $52.63/brl; Sept Copper -0.9% at $3.15/lb

GLD SPDR Gold Trust ETF daily holdings -0.1% to 851.9 metric tons

(CN) PBOC TO INJECT CNY50B WITH 63-DAY REVERSE REPO

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6473 V 6.6288 PRIOR

(AU) Australia sells A$1.0B in 2028 Bonds, avg yield 2.8556%, bid to cover 4.33x

US markets on close: Dow +0.3%, S&P500 +0.1%, Nasdaq -0.1%, Russell +0.3%

Best Sector in S&P500: Materials +1.3%

Worst Sector in S&P500: Healthcare -1%

At the close: VIX 11.30 (+0.07pts); Treasuries: 2-yr 1.619% (+2bps), 10-yr 2.457% (+2bps), 30-yr 2.968% (+2bps)

US Market Summary

The S&P and Dow ended modestly higher today, while the Nasdaq ended in negative territory at the day's lows, as a host of moving parts had traders absorbing information from all sides. Coming into the session, much of the focus was on perceived dovish comments from the ECB's Draghi, along with Q3 earnings season, which remained in full effect. Major US cable companies disappointed due to continued losses in TV subscriptions. The Dow moved higher on the back of follow-through from yesterday's upbeat Nike analyst day. The Transports ran upwards after earnings from UPS and UNP. The NASDAQ lagged as biotech names Amgen and Celgene disappointed with their Q3 results and outlook. The Dollar index rose 1% in late afternoon trading, set for its biggest single-day gain since last December. Healthcare and real estate were the only sectors in the red, while materials and telecom led the day's gainers.

US Afterhours Movers

AMZN Reports Q3 $0.52 v $0.01e, Rev $44B v $42.2Be; Guides Q4 Rev $56-60.5B v $58.9Be; +7.4% afterhours

FSLR Reports Q3 $1.95 v $0.85e, Rev $1.1B v $824Me; Raises Non-GAAP FY17 $2.40-2.60 v $2.22e; +4.7% afterhours

GOOGL Reports Q3 $9.57 v $8.43e, Rev $27.8B v $21.9Be; +3.0% afterhours

MSFT Reports Q1 $0.84 v $0.72e, Rev $24.5B v $23.5Be; +2.5% afterhours

BIDU Reports Q3 $3.89 v $2.19e, Rev $3.53B v $3.47Be; Guides Q4 Rev $3.34-3.52B v $3.60Be; -10.6% afterhours

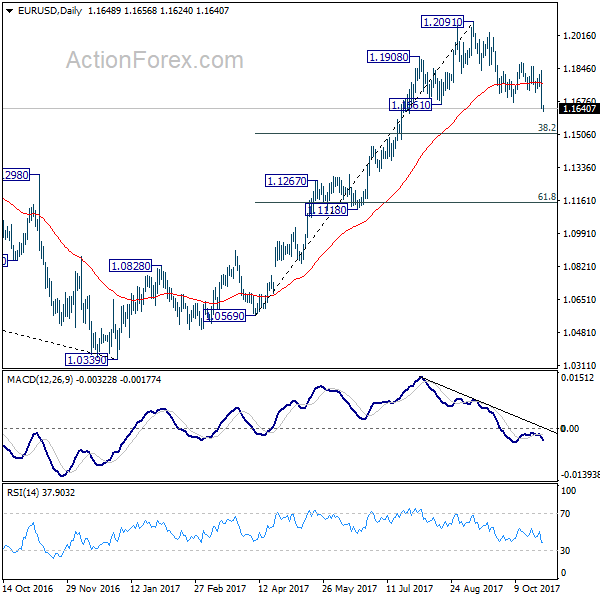

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1582; (P) 1.1709 (R1) 1.1779; More...

EUR/USD dives to as low as 1.1624 so far today. The break of 1.1669 support confirms resumption of whole fall from 1.2091. Intraday bias is back on the downside for 38.2% retracement of 1.0569 to 1.2091 at 1.1510 next. At this point, such decline is still viewed as a correction. Hence, we'd expect strong support from 1.1510 to bring rebound, at least during first attempt. However, firm break there will bring deeper decline to 61.8% retracement at 1.1150. On the upside, above 1.1724 support turned resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 1.1879 resistance holds.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Daily Wave Analysis: EUR/USD Bearish Breakout Targets 38.2% Fibonacci At 1.15

Currency pair EUR/USD

The EUR/USD broke below the support trend line and zone (dotted blue) yesterday when the European Central Bank (EBC) president Draghi was announcing the continuation of the Quantitative Easing program. The Euro reacted bearishly and fell against the USD, which invalidated a larger bullish correction and makes a continuation towards the 38.2% Fib of wave 4 vs 3 likely now.

EUR/USD is showing strong bearish momentum and is most likely in a wave 3 (blue) which could become extended if a triangle or bear flag pattern appears (purple lines).

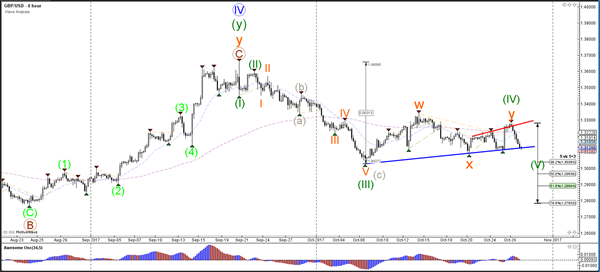

Currency pair GBP/USD

The GBP/USD has not broken below the support trend line (blue) as yet but the strong bearishmomentum makes a bearish breakout likely, which could be part of a wave 5 (green).

The GBP/USD bearish momentum is probably a wave 1 (orange) which could see a bounce and a retracement for a wave 2 (orange).

Currency pair USD/JPY

The USD/JPY has completed a wave 4 (blue) within the uptrend andbroke above the resistance (red) trend line to challenge the 114.50-115 target zone.

The USD/JPYis approaching the Fibonacci targets of waves 5 (pink/blue).

Greenback Soars as Tax Cuts Procedural Path Cleared, Dollar Index Confirm Medium Term Reversal

Dollar surged overnight and remains firm in Asian session today. ECB's dovish tapering is seen as a key factor driving the greenback higher. But more importantly, another step was taken forward as House passed Senate's versions of the budget bill. That procedural path is now cleared to move on to US President Donald Trump's tax cuts. Staying in the currency markets, commodity currencies remain the weakest ones for the week. Aussie's selloff accelerated after CPI miss earlier this week and weighed further down by PPI miss today. Canadian Dollar remains weak as post cautious BoC statement selloff continues. Euro, while weak, is trading mixed only.

Dollar index confirms reversal

Dollar index's strong break of 94.14 key resistance finally confirms medium term reversal. That is the pull back from 2016 high at 103.82 should have completed at 91.01, on bullish convergence condition in daily MACD. That also came after drawing support from 91.91/3 long term cluster support (38.2% retracement of 72.69, 2011 low, to 103.82, 2016 high) at 91.93. Near term outlook will now remain bullish as long as 93.47 support holds. Further rise should be seen to 38.2% retracement of 103.82 to 91.01 at 95.90 at least. There is prospect of hitting 61.8% retracement at 98.92 and above. But we'll monitor the upside momentum to assess the chance later.

ECB's dovish Tapering

ECB announced that it would begin in January 2018 to reduce the asset purchase size to 30 B euro per month. The program would last until September, "or beyond, if necessary". It added that stimulus measures would be implemented "in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim". In order not to let the market interpret the move as a trim in stimulus, President Mario Draghi called it "recalibration".

The accompanying statement affirmed that "if the outlook becomes less favorable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the APP in terms of size and/or duration". Moreover, the ECB announced that it would reinvest the principal payments from maturing securities "for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary". It would also continue to provide liquidity via fixed rate full allotment refi operations until at least the end of 2019.

More on ECB:

- ECB Begins Trimming Asset Purchase in 2018, Pledges to Expand/ Extend if Necessary

- ECB Tightening Remains Distant

- ECB Review: ECB Opts For 'Lower-For-Longer' QE Extension

- 'Soft' ECB Decision Triggers Modest Euro Setback

- ECB to Halve Monthly Pace of Asset Purchases to €30 Billion Starting in January 2018

- (ECB) Introductory Statement to the Press Conference

- (ECB) Monetary Policy Decisions

On the data front

Japan national CPI core was unchanged at 0.70% yoy in September, in line with consensus. Tokyo CPI core rose to 0.6% yoy in October, above expectation of 0.5% yoy. Australia PPI rose 0.2% qoq, 1.6% yoy in Q3.

US Q3 GDP is the main focus of the day ahead and is expected to show 2.6% annualized growth.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1582; (P) 1.1709 (R1) 1.1779; More...

EUR/USD dives to as low as 1.1624 so far today. The break of 1.1669 support confirms resumption of whole fall from 1.2091. Intraday bias is back on the downside for 38.2% retracement of 1.0569 to 1.2091 at 1.1510 next. At this point, such decline is still viewed as a correction. Hence, we'd expect strong support from 1.1510 to bring rebound, at least during first attempt. However, firm break there will bring deeper decline to 61.8% retracement at 1.1150. ON the upside, above 1.1724 support turned resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 1.1879 resistance holds.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Sep | 0.70% | 0.70% | 0.70% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 0.60% | 0.50% | 0.50% | |

| 0:30 | AUD | PPI Q/Q Q3 | 0.20% | 0.40% | 0.50% | |

| 0:30 | AUD | PPI Y/Y Q3 | 1.60% | 1.70% | ||

| 6:00 | EUR | German Import Price Index M/M Sep | 0.9% | 0.50% | 0.00% | |

| 12:30 | USD | GDP (Annualized) Q3 A | 2.60% | 3.10% | ||

| 12:30 | USD | GDP Price Index Q3 A | 1.80% | 1.00% | ||

| 14:00 | USD | U. of Michigan Confidence Oct F | 101 | 101.1 |

Elliott Wave View: FTSE Ended Correction

FTSE Elliott Wave view suggests that decline to 7199.5 ended Primary wave ((4)). Up from there, the rally is unfolding as an impulse Elliott Wave structure where Minor wave 1 ended at 7327.5 and pullback to 7289.75 ended Minor wave 2. Rally to 7494.34 ended Minor wave 3, and pullback to 7473.12 ended Minor wave 4. Minor wave 5 ended at 7565.11 and this also ended Intermediate wave (A) of a zigzag Elliott Wave structure from 9/15 low (7199.5).

Intermediate wave (B) pullback unfolded as a double three Elliott Wave structure where Minor wave W of (B) ended at 7485.42, Minor wave X of (B) ended at 7560.04 and Minor wave Y of (B) ended at 7437.42. Near term, while pullbacks stay above 7347.42, and more importantly as far as pivot at 9/15 low (7196.09) stays intact, expect Index to extend higher. We don’t like selling the Index.

FTSE 1 Hour Elliott Wave Analysis

ECB Tightening Remains Distant

- ECB extends bond-buying until September 2018 at a reduced rate

- Decision widely expected but should be seen as an easing not just an extension

- Dovish comments signals ECB sees interest rates remaining lower for longer

- Draghi emphasizes bond-buying recalibration isn't tapering

- Did fear of adverse market reaction lead Draghi to overdo dovishness?

- ECB also sounds more upbeat on economy but no near term inflation spike seen

- Strong growth could spark price pressures in 2018

The ECB's decision to extend its Asset Purchase Programme by nine months at a reduced monthly pace of €30 billion had been widely expected. However, the tone of ECB president Mario Draghi's explanation of this decision was probably more dovish than expected and implies the ECB expects to maintain a very accommodative stance of monetary policy for the foreseeable future.

Draghi errs on the side of dovishness

Our strong sense is that Mr Draghi wanted to avoid an adverse market reaction that would likely have followed any indication that the central bank's decision was effectively the last instalment in ECB quantitative easing. The ECB has previously signalled its concern that misinterpreted comments could lead to a premature tightening in financial conditions. This may have pushed him a little too far in the opposite direction. Market thinking on ECB policy is unlikely to change materially in the near term but it will be interesting to see if or when it might be challenged by the continuing build-up in momentum in the Euro area economy.

The clear inference from Mr Draghi's comments was that ECB bond buying would not come to an abrupt end in September 2018. By extension, given the repeated ECB assertion that it continues to expect its key policy interest rates 'to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases', this would imply the ECB doesn't currently envisage raising interest rates until well into 2019 at the earliest.

Markets have been primed for indications of ‘lower for longer' in ECB commentary and there was little expectation of any hawkish tilt in yesterday's decision or explanation. However as Mr Draghi's pronouncements point towards a further albeit modest delay in the expected timing of any initial tightening of monetary policy in the Euro area, the exchange rate of Euro softened and market interest rates edged lower.

APP extended to Septemberand beyond?

The most notable decision announced was that the ECB would continue its Asset Purchase Programme (APP) beyond the mooted end date of December 2017. This extension was universally expected. A series of media reports quoting ECB sources had also largely prepared the market for a reduction in the monthly purchase volume from €60 billion at present to a €30billion pace between January and September next year.

Importantly, Mr Draghi indicated that this ‘recalibration' of the monthly pace of bond buying shouldn't be seen as a step towards ending the APP. He emphasised that the adjustment shouldn't be seen as ‘tapering', noting that particular word had not been used in council deliberations. Instead, he suggested this ‘downsize' was a consistent response to improved economic conditions.

Mr Draghi also emphasised that the APP was not going to stop suddenly, repeating that ‘it has never been our view that it should stop suddenly'. This would imply that a further ‘recalibration' might be envisaged for the final months of 2018 and possibly beyond, leading to the possibility that Mr Draghi might retire (his term as ECB president expires in October 2019) before any marked tightening of monetary policy occurs.

Mr Draghi also noted that a strong majority on the governing council favoured keeping the programme openended and, in response to a question, stated that the ECB had no ‘ceiling' in mind for the APP. He strongly argued that the programme had sufficient flexibility to handle widely felt market concerns that the ECB might face technical difficulties sourcing sufficient bonds to continue purchases through the coming year.

These various comments are likely to encourage the view that the ‘recalibration' might not be the last and this could weigh further on the Euro and interest rate markets. However, as we discuss below such forward guidance has to be seen in the context of a growth spurt in the Euro area that may have further to run.

Increase in stock of APP a further easing

The ECB's decision will result in the stock of the APP increasing materially in 2018, it should properly be seen as a further easing by the ECB. However, as it was widely discounted and most commentary has focussed on the cut in the amount of monthly purchases rather than the extension of the programme, the additional support to an already healthy Euro area recovery has attracted little attention

The ECB also re-stated that it would continue to reinvest the principal payments from maturing securities purchased under the APP. While it doesn't represent any shift in ECB policy, as this approach was signalled as far back as 2015, Mr Draghi suggested that such reinvestments were ‘going to be massive' , with ECB vice-president Constancio suggesting they would come to ‘many billions'.

This will ensure the stock of assets purchased by the ECB continues to rise significantly through 2018 and, on some estimates, the reinvestment could add as much as €15 billion to average gross monthly purchases. However, as Mr Constancio indicated, the amounts re-invested could vary considerably from month to month.

By ensuring the stock of APP will continue to increase in the coming year, the reinvestment of maturing bond purchases contributes to a further easing in ECB policy. Mr Draghi likely sought to emphasise the continuation of the ECB's current reinvestment policy to underline the contrast with the Fed's recently announced intention to begin to reduce its balance sheet. The resultant difference in monetary stance might be expected to influence currency trading and thereby help limit the possibility of a rising Euro that undoubtedly represents the risk identified as ‘developments in foreign exchange markets' mentioned in the opening press statement.

The ECB also signalled that it would continue to operate its main liquidity operations on a ‘fixed rate full allotment' basis. While this is largely technical, it is important in that it should ensure the persistence of favourable liquidity conditions in Euro area money markets in coming years

When questioned, Mr Draghi indicated this decision had no implications for the level of interest rates although it could be speculated that retaining this approach would make it easier to ensure an orderly adjustment of market rates to an eventual rise in policy rates. More generally, regardless of the monetary stance, there is a widely held view that Central Banks are likely to be slow to move from current practices such as this that provide increased certainty in relation to the provision of liquidity to money markets.

At odds with an improving economy?

Our sense is that the main takeaway for markets from the ECB meeting is likely to be one of ‘lower for even longer' although any extension of the timeframe for easy policy will probably be seen as modest rather than major. This is largely because the Euro area economy is showing signs of exceptionally fast growth at present and this should eventually translate into higher inflation.

While most focus was understandably on the decision to extend the APP, the ECB struck an increasingly positive note on the Euro area economy. The opening press statement refers to ‘unabated growth momentum in the second half of this year' while Mr Draghi also noted how well the economy was performing at present. Wednesday's better than expected IFO survey for Germany is the latest in a range of indicators to hint that momentum could build further and push Euro area growth even higher to a point where now largely dormant price pressures might quickly emerge.

As the graph shows, an uneven pick-up in Euro area growth and inflation has coincided with a dramatic step-up in the ECB's APP from an initially envisaged level of just over €1.1 trillion to €2.2 trillion now and after yesterday's decision close to €2.6 trillion in just under a year's time. Our sense is that this significant stimulus has contributed materially to the substantial improvement in the Euro area economy now underway even if debate continues as to exactly how such quantitative easing might work.

The trajectory now envisaged for the ECB's APP relative to those in Euro area activity and inflation could become notably less compatible as 2018 develops. Such a prospect may appear remote in coming months as base effects are expected to push down on headline inflation. However, such technical influences might quickly give way to a firmer trend in inflation on foot of stronger growth and improving sentiment that should feed through to wage and price setting.

Mr Draghi buys some time

The ECB's decision likely brings a period of calm in the near term and it is likely that Mr Draghi's comments were significantly influenced by a desire to avoid the unfavourable market reaction that would have followed if, instead, he had indicated that the measures represent the last instalment of ECB quantitative easing. However, it is widely expected that robust growth will continue and there is also a strong likelihood that the ECB's December projections will show signs of the required sustained adjustment in the path of inflation within the new forecast period. In that event, markets might begin to consider whether the current projected path for ECB monetary policy is sustainable.

Market Morning Briefing: Quite A Bearish Turn For The Euro

STOCKS

Dow (23400.86, +0.31%) could remain stable above 23250, eventually trying to attempt a rise towards 23750. On the longer term, 23750-24000 levels could be an immediate top for the index.

Dax (13133.28, +1.39%) surged higher breaking above the 13100 levels possibly inviting the bulls to take the index up in the near term. While it trades above 13100, we may look for a 100-300points upward rally in the coming sessions with some corrective dips. View remains bullish.

Nikkei (21952.35, +0.98%) is maintaining its upward rally and could test 22250 in the coming sessions. Target for the longer term (say 2-3 weeks) would be 22666. Some interim rejection is possible from 22250 levels. Near to medium term looks bullish.

Shanghai (3419.67, +0.36%) has tested our 3420 target and could continue to move up in the near term. A small dip is possible from 3425 before resuming the rally towards 3450 in the medium term.

Nifty (10343.80, +0.47%) tested decent resistance at 10355, which if holds could bring the index down towards 10250-10200 in the next couple of sessions. But in case the index rises further today, it could test 10400 on the upside.

COMMODITIES

Gold (1267.40) is trading below 1275 and could possibly test 1260/50 in the coming sessions. While the US Dollar Index (94.77) moves above 95, there is scope for weakness in Gold in the near to medium term. Silver (16.74) could test 16.50-16.25 levels in the near term. View likely to be bearish.

Brent (59.34) is rising as expected, heading towards 60-61 levels in the near term. Near term looks bullish with the target of 60-61 levels intact. WTI (52.64) has some scope of rising towards 55 in the near to medium term while it manages to break above 53. Immediate resistance on the weekly charts seem to be breaking on the upside, opening up further upside of 54-55 levels for the medium term.

Copper (3.1465) could come off towards 3.10 or lower in the medium term. A stable consolidation in the 3.25-3.10 region is possible for some time.

FOREX

All round Dollar strength today.

Quite a bearish turn for the Euro (1.1638) with Draghi being seen as dovish yesterday despite halving the AAP (asset purchase programme) from EUR 60 bln p.m. to EUR 30 bln p.m. See Interest Rates section below. With the Euro now firmly below 1.1700-1670, the focus will now be on 1.1510 on the downside, maybe even 1.1415.

The Euro's weakness has pushed Dollar Index (94.76) well past the earlier resistance at 94.00 and brings 96 onto the radar, although immediate Channel Resistance is seen at 95.00.

The fresh Dollar strength is also reflected in the rise in Dollar-Yen (114.15). Although the Resistance at 114.50 holds as of now, there are increased chances of further rise to 115.00 as well. Tempering the rise in Dollar-Yen would be Euro-Yen (132.83) which has been pulled down rudely by the decline in the Euro and is trading just below important trendline at 133 which might act as Resistance now. Need to watch this.

All of Pound's (1.3127) gains on Wednesday were erased by weak UK Retail Sales data yesterday, which again reversed the sentiment on a possible rate hike next week. With both Bulls and Bears having been trapped in the last two days, the Pound may now trade sideways between 1.31-33 for some days.

As feared, the Aussie (0.7649) has fallen further to and below 0.7655. This is quite a letdown for the Aussie as most of the gains from July have been erased, making the Aussie vulnerable to further decline towards 0.7520.

Dollar-Yuan (USDCNY = 6.6521) has also risen and should see 6.67+ soon. Dollar-Rupee (64.82/83) could well rise past 65.00 today.

INTEREST RATES

Draghi's statement that the APP (asset purchase programme) is "open ended" and is well likely to continue even after Sep '18, has been seen as pushing an interest rate hike out into mid 2019. Thus, the interest rate advantage is given over to the Dollar. This works well enough for Draghi as the ECB had started becoming concerned about Euro strength and he would like Europe to continue to benefit from export growth also.

The German-US 10 Yr Yield Spread (-2.03%) has fallen well below -1.95%, leading to the weakness in the Euro. This is largely due to dip in the German 10Yr yield from 0.486% on Wednesday to 0.418% now. But, Support is possible near 0.40% as well.

Eyes on the BOJ meeting next week (Tuesday, 31st Oct), FOMC meeting (Wednesday, 1st Nov) and BOE meeeting (Thursday, 2nd Nov).

On US yields, there is Resistance at 3.00% on the 30Yr (currently 2.96%), at 2.50% on the 10Yr (currently 2.45%) and near 2.15-20% on the 5Yr (currently 2.07%). The market clearly does not anticipate a rate hike next week, Wednesday. But, a lot of volatility will take place if the Fed surprises the market and raises rates. Chances are less, of course, but let us see.

ECB Review: ECB Opts For ‘Lower-For-Longer’ QE Extension

- ECB opts for a 'lower-for-longer' QE extension in 2018 and leaves forward guidance unchanged as we expected.

- ECB will publish details on reinvestment from November 2017 onwards.

- EUR/USD range bound for now, but the 'smell of exit' could bring cross back to the 1.20s in 2018.

- Continued support for peripheral-core EU spreads and Scandi covered bonds.

In line with our expectation, the ECB today announced an extension of its QE programme until September 2018, but also scaled down its asset purchases to EUR30bn from January 2018 onwards (see Chart 1). Importantly, the ECB also left its forward guidance unchanged and retained the possibility to extend the QE programme in size and/or duration, leaving it open-ended. The ECB reiterated that policy rates will remain at their current levels for an extended period of time and well past the horizon of asset purchases. During the press conference Draghi clarified that no changes in the QE parameters and the sequencing on interest rates were discussed at today's meeting.

The ECB's QE scale down decision reflected growing confidence by the Governing Council that inflation will eventually converge to target based on an increasingly robust and broad-based economic expansion in the eurozone, an uptick in measures of underlying inflation and continued favourable financing conditions due to accommodative monetary policy measures. Nevertheless, inflation pressures remain muted and hence the ECB stressed the continued need for monetary support through the net QE purchases, forward guidance on interest rates and forthcoming reinvestments.

The introductory statement now also excluded any reference to the risks from exchange rate volatility, which is, however, not so surprising given that the effective euro appreciation pace has abated significantly since September, which we think matters more for the ECB than the exchange rate level as such

ECB releases more details on QE reinvestments in 2018

The ECB also released further details on the reinvestments of maturing bonds which are made alongside new QE purchases and which will become increasingly sizable over the course of 2018.

1. Time horizon: Reinvestments will be made 'for an extended period of time' after the end of the net QE purchases and 'for as long as necessary'.

2. Composition: From 6 November 2017 the ECB will also now publish the expected monthly redemption amounts for the QE programme over a rolling 12-month horizon as well as historical redemption figures since the start of QE. The data will provide redemptions information for each of the four components (PSPP, CSPP, CBPP3 and ABSPP), but not reveal the individual country breakdown.

3. Timing: Reinvestments will be flexible and made in the month they fall due or otherwise in the subsequent two months, if warranted by liquidity conditions.

4. No change in country composition for now: Reinvestments will be made in the jurisdiction in which the maturing bonds were issued, during the period of net asset purchases.

Overall, we think the ECB's communication will increasingly focus on the reinvestments and the stock rather than the flow of QE purchases in the future, as it gradually scales back monetary stimulus over the coming years.

FX: EUR/USD range bound now – 'smell of exit' to bring back 1.20s 2018

With the ECB's QE scheme extended as widely expected and the forward guidance essentially unchanged, little has materially changed for the single currency. But the drop in EUR/USD on the initial policy statement clearly suggests that some expectations in the FX markets had been building ahead of the meeting that the ECB could go with a more hawkish taper as price action earlier in the week is indeed testament to.

In our view, while today's policy message underpins that the ECB is taking tapering to the next level, the continued commitment to stay accommodative on a still data-dependent basis suggests a firm move in EUR/USD above 1.20 is not on the cards until 2018, as the ECB seems very wary of taking exit talk too far at the current stage.

The longer period of QE purchases notably ensures that rate hike expectations will be kept at bay, meaning that relative rates are unlikely to provide significant support to the euro in the near term. As such, e.g. the 2Y swap spread is unlikely to drag EUR/USD higher on, say, a 3M horizon. However, we still argue that the potential for notably debt outflows to fade should support the single currency more broadly as a continued taper cements the sense that has grabbed notably the FX market that ECB normalisation is ongoing. Thus, we continue to see risks to EUR/USD being to the upside in 2018 and still target 1.25 in 12M.

Overall, the dovish tapering message from the ECB today cements our sense that EUR/USD is range bound (1.19-1.16) on a 1-3M horizon with risks tilted a tad to the downside near term. Notably, if Trump goes with Taylor as Fed chair, this opens for a move below the 1.1700 mark; we still see good support at the 1.1670 level (6 Oct low) though. In the coming days, we would expect EUR/USD to settle around the 1.1750 level with the risk of next week's FOMC meeting fuelling a move towards 1.1700 as focus returns to Fed's determinedness to 'normalise'. On the upside, we think resistance at 1.1910 (2-Aug high) will hold, but in order to revisit the 1.20s we would likely need to see better prospects of eurozone core inflation edging higher on a sustained basis (a mid-2018 story) and/or markets to speculate (again) that the ECB is running into toolbox constraints

Fixed income: very supportive for the periphery and Bund spread

The statement from the ECB is very supportive for the European government bond markets both outright and relative to swaps. The combination of the extending of QE into 2018 as well as reinvesting the redemptions for an extended period of time after the QE ends is very supportive for the periphery. Finally, the MRO and the 3mth TLRO are set to continue with full allotment and a fixed rate until at least 2019. The combination of a dovish ECB, less supply in 2018 and a positive rating cycle for the EU countries is very supportive for the peripheral-core EU spreads. If we look at the combination of issuance, redemptions/reinvestments and QE, then there will still be a negative supply of European government bonds in 2018, as shown in the table below. However, the negative net supply is set to be substantially lower than the negative net supply from 2017 as shown below.

Germany still stands out with a very negative net supply in 2018. This is partly due to the surplus on the public finances as well as the QE. We have assumed a reduction in the QE amount in Germany in 2018 as the ECB/Bundesbank is close to the 33% issuer limit. Hence, the ECB/Bundesbank is set to buy well below the capital key in Germany. In total, we expect that the ECB will buy EUR186bn in the PSPP programme or 70% of the total QE in 2018. This is a substantial reduction in the PSPP programme, which as currently 85% of the total QE programme. This leaves 30% to the covered bond, ABS and corporate bond programme. We still consider it likely that the ECB will buy a higher share of corporate bonds due to the more direct economic impact, although this will probably only be revealed by the QE details in coming months.

Investment conclusions for EU government bonds

There is negative supply in Germany, while the political uncertainty/problems in Spain seem to be fading. The reduction in the QE programme for e.g. Portugal, Ireland and Finland is likely to have a modest impact, as the ECB is already buying well below the capital key Hence, we see the following trades/targets for some of the trades we have or had on in 2017 and going into 2018:

1. Bund spread widener: target 55bp 2. Long 10Y PGB versus 10Y BTPS. Target 0bp 3. Long 10Y Ireland versus 10Y France. Target 0bp 4. Long 10Y Spain versus 10Y Germany. Target 100bp

If we look at the slope of the curve, then the action today from the ECB should give room for flattening of the curves as it confirms the “low for long” policy. Furthermore, if the economic outlook becomes “less favourable”, then the ECB is ready to scale on the QE etc. Hence, we could see a flattening of the 10-30Y curve, partly because of the ECB and partly because of a substantial reduction in the funding need of the EFSF/ESM in 2018. The funding need for EFSF is reduced from EUR49bn to EUR22bn.

In Fixed Income Strategy: Buy 2W10Y ATMF EUR payer ahead of next week's ECB meeting, 26 October 2017, we recommended to buy a 2W10Y ATMF EUR payer swaption. In our view, the low implied volatility offered an attractive short-term hedge against any hawkish 'twist' from ECB. Although, the option maturity still covers the eurozone October CPI data releases, we take a 2bp profit on the back of yesterday's dovish stance from the ECB.

Impact on the Scandinavian markets – Buy Scandi covered bonds

The 'dovish' ECB and the extension of the QE has an impact on the Scandinavian markets as the ECB continues to limit volatility in the market. Furthermore, the extension of the QE in the covered bond market will still be a drag on liquidity even though the QE is scaled down to EUR30bn. However, as the PSPP programme is scaled down more than the CBPP3, ABSPP and CSPP programmes, then the ECB will still be in the market.

Low volatility, plenty of excess liquidity and 'low for long' monetary policy is very positive for the Danish covered bond market, especially the Danish callable mortgage bonds. Given that the Riksbank is on hold, then given the steepness of the Swedish yield curves (govt, covered bond and swap curves) relative to Euroland, combined with the yield pick-up from an FX-hedge into euros, then both 30Y Danish callable mortgage bonds as well as 5Y Swedish covered bonds are attractive alternatives to EU peers. But although today's ECB decision should be supportive for SEK covered bonds in isolation, uncertainty about the housing market might pose some risk since the knee-jerk reaction to a deteriorating situation in the housing market would not be in favour of the bonds (at least not relative to swaps or SGBs).