Sample Category Title

Dollar Firm but Losing Momentum as Fed Chair Race Goes On

Dollar is trading as the strongest one for the week. The greenback was lifted by talks that John Taylor is considered a hawk and has impressed US President Donald Trump in Fed chair interview. But momentum in the greenback is rather weak as it struggled to extend gains in late US session. Dollar was also weighed down mildly by falling yields, with 10 year yield closed down -0.09 at 2.298. Sterling is extending this week's decline as markets are reassessing the dovish possibilities of November BoE meeting. Meanwhile, Canadian Dollar rebounded as NAFTA negotiation is extended. UK job data will be the main focus today. Markets will also keep an eye on Chinese Communist Party Congress in Beijing.

Trump likes Taylor for his hawkishness? Or flexibility?

Dollar's rally since yesterday was built on top of speculations that Standford University economist John Taylor is catching up in the race as the next Fed chair. Analysts point to the fact that Taylor is known for the so called Taylor rule, which implies higher interest rate. He has also criticized Fed's ultra-loose monetary policy before and is seen by some as the most hawkish candidate. However, we'd like to point out again that firstly, US President Donald Trump would likely prefer someone who he can work well with, rather than someone who's most suitable for the job. Or maybe in better words, Trump would see someone he can work well with as the most suitable one, not from Fed's operation nor market stability angle. Secondly, Taylor has demonstrated his flexibility in recent speeches, as he said that rules shouldn't be used as a "way to tie central bankers' hands." Instead, "there are reasons to run policy with a strategy." It could be his "flexibility" that impressed Trump, not his "hawkishness."

Markets reassessing dovish possibilities for BoE November meeting

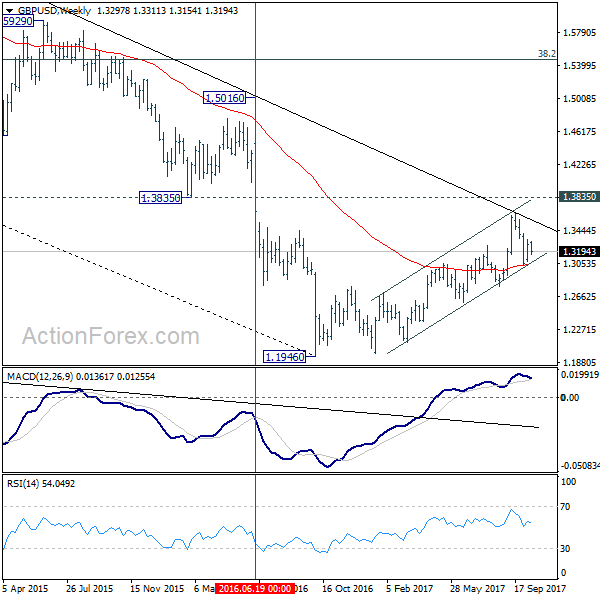

Sterling was sold off yesterday even though CPI hit 3% level in September. BoE Governor Mark Carney also reiterated that "the judgment of the majority of the committee is some raise in interest rates over the coming months may be appropriate". The developments affirmed the central case of a November BoE hike. However, markets are starting to look at some dovish scenarios. Firstly, a November hike is still not a done deal, even though it's the most likely scenario. Secondly, the vote split could be dovish if hawks just win by a margin. Thirdly and most importantly, it could just be a one-off. As we pointed out before, a 25bps hike just brings the Bank Rate back to pre-Brexit referendum level. Back then, GBP/USD was above 1.3835 key support level. And since then federal funds rate was raised from 0.50% to 1.25%, and another hike is coming in December. Based on this, a break above 1.3835 handle in GBP/USD is not justifiable. And upside potential is rather limited.

EU to start preparing trade talks with UK

Ahead of the EU summit later this week, officials are already starting to prepare for trade negotiation with UK after Brexit. It's reported that EU is targeting to have a road map ready by December. And the after the December summit, it's hopeful that sufficient progress is being made on the negotiations to move on to trade talks. But for the moment, preparation work will only be carried out within EU. EU's chief Brexit negotiator said that "this week's European Council will be a stepping stone toward the next get-together." And, "I have said we are ready to accelerate the rhythm, but to accelerate you need two." However, UK's Brexit Secretary David Davis said yesterday that "we are reaching the limits of what we can achieve without consideration of the future relationship." Davis's comments suggests he is unwilling to revolve the key issues of the "past" like the divorce bill, before talking about the "future" trade agreements.

Loonie rebounds as NAFTA negotiations extend

Canadian Dollar rebounded overnight on news regarding North American Free Trade Agreement negotiation. The fourth round of NAFTA negotiation concluded yesterday. U.S. Trade Representative Robert Lighthizer, Mexican Economy Minister Ildefonso Guajardo and Canadian Foreign Minister Chrystia Freeland jointly postponed the target from December to March 2018. The time between negotiating rounds were also extended to give everyone more room to study the proposals. This is seen as a sign of willingness to resolve the differences between the parties. While it's unlikely, there were some speculations that NAFTA could be ripped to zero as the worst case scenario.

On the data front

Australia Westpac leading index rose 0.1% mom in September. UK employment data will be the key focus in European session. Later in the day, Canada will release manufacturing shipments. US will release housing starts and building permits. Fed will also release Beige Book economic reports.

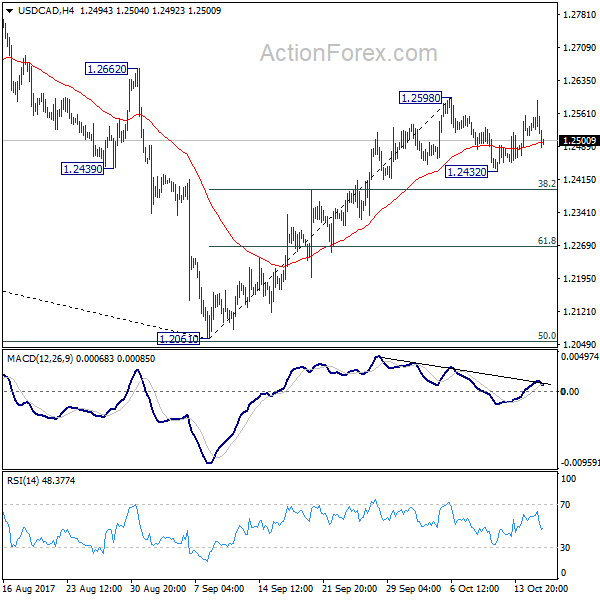

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2491; (P) 1.2541; (R1) 1.2569; More....

USD/CAD's rebound was limited below 1.2598 and weakened again. Intraday bias is turned neutral first. Consolidation from 1.2598 is still in progress. In case of deeper fall, we'd now expect downside to be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption. On the upside, break of 1.2598 will extend the rebound from 1.2061 to 1.2777 resistance next.

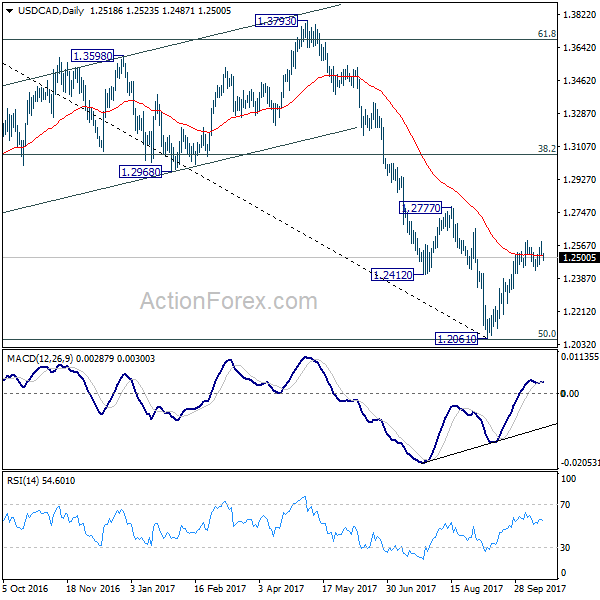

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Sep | 0.10% | -0.08% | ||

| 08:30 | GBP | Jobless Claims Change Sep | 3.2K | -2.8K | ||

| 08:30 | GBP | Claimant Count Rate Sep | 2.30% | |||

| 08:30 | GBP | ILO Unemployment Rate 3M Aug | 4.30% | 4.30% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Aug | 2.10% | 2.10% | ||

| 12:30 | CAD | Manufacturing Shipments M/M Aug | -0.30% | -2.60% | ||

| 12:30 | USD | Housing Starts Sep | 1.18M | 1.18M | ||

| 12:30 | USD | Building Permits Sep | 1.25M | 1.27M | ||

| 14:30 | USD | Crude Oil Inventories | -2.7M | |||

| 18:00 | USD | Federal Reserve Beige Book |

Market Morning Briefing: The Mentioned Support At 1.1730 Has Held Well Enough On The Euro

STOCKS

Dow (22997.44, +0.18%) has finally almost reached to our initial target of 23000 and the upside bullish momentum looks strong for the coming sessions which could take the index higher towards 23250 soon.

Dax (12995.06, -0.07%) is trading along the resistance near 13000-13050 region and could remain sideways within the said region for a few more sessions. The dip could possibly extend towards 12850-12800 levels also in case the rejection from 13050 lasts for the medium term.

Nikkei (21354.56, +0.09%) is stable below 21400 for the last 2-sessions and could possibly face some difficulty in attempting a rise above 21400 just now. While interim resistance near 21400 holds, we could see a fall towards 21200 or lower in the near term.

Shanghai (3378.77, +0.20%) could re-test 3400-3410 while above 3360. Near term look sideways to bullish in the coming sessions.

Nifty (10234.55, +0.04%) was almost stable yesterday. As mentioned earlier, the upside could be limited to 10300-10320 levels in the near term before we see a small corrective dip from there. Today would be the last trading session of the week as the Indian Markets would be closed for the next 2-days for Diwali. A slight upside could possibly be seen today targeting 10300.

COMMODITIES

Gold (1287.20) is likely to remain above 1280 for the coming sessions. Overall broad range of 1310-1280 is likely to remain for the medium term. A bounce back from 1280 to 1300 levels can be seen in the near term. While the US Dollar Index (93.48) remains in the 93.0-94.0 zone, Gold could trade sideways in the 1300-1280 region.

Silver (17.06) can trade in the 17.50-16.75 region, 17.50 being an important near term resistance.

Brent (58.28) is up in line with our expectation and could test 58.50-59.00 soon. A dip from 59.00 looks more likely just now.

WTI (52.12) has risen as expected but may not move above 53.00-52.50 just now. A dip back towards 51 is likely in the near term while below 52.50.

Copper (3.2105) is trading above 3.20 and could possibly come off from current levels as decent resistance is visible just above current levels on the line charts. Preferred view is a dip to 3.15/10 before again rising up to current levels.

FOREX

The mentioned Support at 1.1730 has held well enough on the Euro (1.1772), keeping the preferred bullish possibility alive. Look for a near term range of 1.1730-1860 for the next few days ahead of the ECB next week.

The Euro-Yen (132.07) is stable near yesterday's level while the Dollar Index (93.46) trades just below the 93.50 Resistance mentioned yesterday. We need to see if it comes down from here or not.

Dollar-Yen (112.18) is also stable/ mixed with a slight bullish slant which can target 113.00 on the upside if it works.

The Pound (1.3195) is down a decent bit from Monday's high of 1.3338. Near-term Resistance at 1.3250 now and longer term Resistance is in the 1.34-35 region.

Like the Euro, the Aussie (0.7850) has found good Support on the 21-week Moving Average at 0.7810 and can target 0.80 while that holds. Immediate Resistance seen at 0.7915.

Dollar-Rupee (65.03) might be quiet today on account of Diwali holidays from tomorrow. Next week could see 65.15.

INTEREST RATES

US yields (5Y 1.96%, 10Yr 2.30%, 30Yr 2.80%) dipped slightly yesterday after having moved up on Monday after Yellen's assertion of interest rate hikes to come. In the medium term, there may be room for US yields to rise by 20-25 bp going into December.

The US Yield Curve (30-5 Spread 0.85%, 30-10 Spread 0.51%) is as flat as it was back in 2007-2008. The 30-10 could dip some more towards 0.49%, but the 30-5 could bounce from Support seen near current levels.

Going into the ECB meeting next week, the market will look for the ECB's decisions on how and from when it intends to start reducing its ongoing QE.

In India, the 10Yr GOI (6.7631%) has Resistance at 6.78%, which is likely to hold.

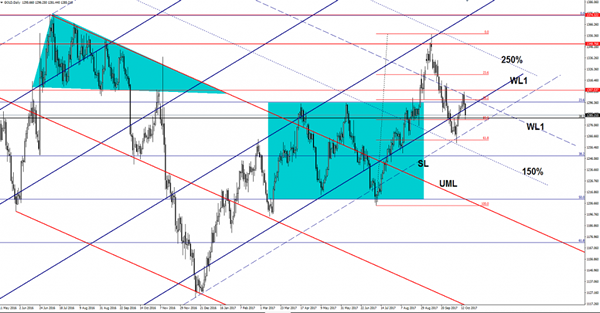

Gold Under Massive Pressure

The Gold plunged on Tuesday and touched the $1281.44 per ounce as the USDX has rallied. The bearish momentum was paused by the long term 38.2% retracement level and the 50% level. A retest of the WL1 will signal a drop at least till will reach the SL of the ascending pitchfork.

USD/CAD Losing Momentum

The USD/CAD rallied and climbed much above the 1.2557 Monday’s high, but failed to stay there. Price retreated as the USDX has slipped lower after the impressive rally. However, the perspective is bullish on the short term after the retest of the upper median line (uml) of the minor descending pitchfork and after the failure to close on the median line (ml) of the blue ascending pitchfork.

The next upside target will be at the ML of the major red descending pitchfork and at the 1.2678 static resistance.

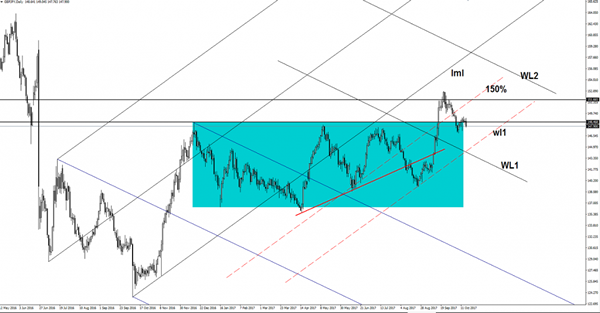

GBP/JPY Turned To The Downside

The currency pair dropped aggressively in the yesterday's trading session and seems to heavy to be stopped at this moment. GBP/JPY is trading in the red even if the Nikkei stock index has managed to reach new highs. The JP225 increased as much as 21392 level, but failed to stay there and has retreated a little.

The Nikkei maintains a bullish perspective on the daily chart, a further increase should force the Yen to drop, but the Japanese currency is not impressed by the index's rally.

The Cable needs serious support from the UK's data to be able to drag the rate higher again. The United Kingdom Unemployment Rate could remain steady at 4.3% in August, while the Claimant Count Change could be reported at 1.3K, versus the -2.8K in the former reading period. Moreover, the Average Earnings Index could increase by 2.1% again.

Price dropped and failed to stay above the 148.46 broken horizontal resistance, signaling that a further drop is favored. A retest of the mentioned upside obstacle will confirm a drop towards the first warning line (wl1) of the ascending pitchfork, where he may find support again. Technically, it should drop after the failure to stabilize above the 151.66 and after the failure to approach and reach the lower median line (lml) of the ascending pitchfork.

Musical Chairs At The Fed

Fed Chair Intrigue

US Yields have been on the rise as has the USD but both still unable to breach any significant near-term level. Most are crediting the move to the increased likelihood of Robert Taylor becoming the Fed Chair and suggesting a more hawkish tilt to the FOMC. Indeed, a rule-based viewpoint from the future sitting Fed Chair does indicate a quicker and higher pace of interest rate normalisation. But Taylor in his admission is no longer a staunch advocate of the 'Taylor Rule, which pegs Fed Fund Rate' considerably higher than the current fixing.So it’s unlikely Fed policy, with Taylor at the helm, will swing too far from the currently projected dot plots. More so given the economic uncertainties surrounding inflation and the disconcerting task of unwinding the Feds colossal balance sheet. But of course, it remains to be seen as to just how aggressive he may be and let us not forget its still anyone’s game.

President Trump spoke on the Fed Chair race, confirming he’s down to five candidates (Yellen, Cohn, Powell, Taylor and Warsh in no particular order) and plans to announce a 'very short-time.'

Of course, markets have no idea how to interpret that, but Reuters sources made a credible case saying that the decision will be made before Trump visits Asia on November 3. That would allow the Senate to make way for the nomination hearing.

US Treasury Report

The US Treasury published its semiannual FX report. TWD has been removed from the dreaded watch list while CNY, JPY, KRW, EUR and CHF remain on the list. China will be pleased to know the US says that CNY is 'moving in the right direction.' Not as approving, INR is a top the manipulation list after 'notable' FX purchases.'

Full US Treasury Report

The British Pound

The Pound climbed slightly after the UK CPI came in on target but a less than emphatical Carney by alluding 'BoE rate hike in coming months may be appropriate' triggered a cascade of GBP selling. I suspect the market focused on 'may be' and not 'rate hike' suggesting that Brexit fall out continues to weigh on BOE sentiment. Also, Silvana Tenreyro, an external member of the Monetary Policy Committee, said the upward pressure on inflation from sterling weakness would start to wane in the coming months. A common viewpoint held by traders as much of the current inflationary pressures is driven by currency weakness.

With the Brexit bluster hanging over Cable like a dark cloud, and growing rate hike debate amongst BOE. The trap door sprung on sterling. In fierce price action, the market quickly moved to price in a one and done rate hike scenario.

The Australian Dollar

Marching to its own beat the RBA minutes bolstered the view that the Australia’s Central Bank won’t necessarily follow others in lifting interest rates. After all, the RBA OCR did not fall as low as other Central banks and remains above both the US Fed and Bank of Canada overnight lending rate. There were few surprises in the minutes, but Thursday China data dump and Australia Jobs numbers could provide some support. Also with the Chinese Communist Congress slated to start today, the antipodeans could get some support from the expected treasure -trove of headlines.

Kiwi traders remain in limbo as they wait for the new government which has been delayed by the NZ First party political wranglings.

The Euro

The ECB has sucked the life out EURO by doing their best to make the October meeting a non-event while laying the ground works for a very dovish QE exit. While Draghi’s guidance has been telegraphed, however, if the ECB turns out to be more dovish than expected on 26th, there is a real risk that the EUR could decline sharply.

I the meantime, we should continue to tread water in the broader 1.1700-1.1850 range but its difficult to get too excited about the EUR in either direction these days as currency markets find themselves caught between a dove ( ECB) and a wannabe hawk( FED). The lack of topside momentum in recent weeks has motivated many dealers to reduce exposure, and while the Euro remains tentatively bid on dips, there’s very little excitement on the EUR post these days

Japanese Yen

US bond yield is the primary driver, but investors are now positioning for an impressive Abe election result. Given this scenario, and a higher trending dollar the USDJPY could firm heading into the weekend.

Asia FX

Local Asian currencies were not immune from the Taylor Rule effect getting weighted down by the broader USD trending higher. The high yielders INR and IDR saw waves of hedging flow which snaked into other ASEAN peer currencies. But the market has stabilised overnight after CNH buying interest appeared just at the 6.62 level after USDCNH wore the brunt of yesterday USD move with trader reducing exposure ahead of the Chinese Communist Congress

The market remains guardedly optimistic in EM Asian currencies, but over the short term with all the USD uncertainty brewing over the next Fed Chairperson, investors will take a very cautious tack.

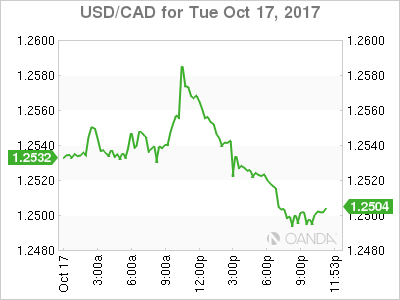

USD/CAD Canadian Dollar Lower On NAFTA Concerns

The Canadian dollar depreciated against the US dollar on Tuesday as the NAFTA negotiations intensify. The American, Canadian and Mexican negotiation teams will deliver a joint statement at 3pm EDT. The US has made proposals that are expected to be rejected by Canada and Mexico, but neither will walk out of the negotiations. The two proposals focus on American content in autos to be increased and to introduce a five year expiry date to the deal.

The Trump administration has made it clear it would prefer to have two bilateral trade agreements, but ending NAFTA would be a economic disaster in the short term, and with looming elections in Mexico and the United States there is no clear timeline of when that would occur. For the time being negotiations are planning to expand the duration of the talks beyond the 5 day sessions.

Canadian mortgage rules were announced today and will take into effect in 2018. The intent of the rules is to require more stress tests on uninsured mortgages. The move is designed to reduce the debt load Canadian households are putting on, but critics point out that it could also lead to pushing borrowers to riskier lenders.

The USD/CAD gained 0.28 percent on Tuesday. The currency pair is trading at 1.2545 heavily influenced by NAFTA comments. The US team is playing hardball and Canada and Mexico will not give any concessions this early even as the window to wrap up renegotiations before the end of the year is fast approaching.

The Canadian economy would be hard hit by a sudden end of the 23 year old trade treaty. The same applies to the Mexico and the United States, but hard stats have taken a back seat to politics and more important optics.

The economic calendar this week won’t feature any major releases for the United States. Canadian data will be scarce with the main events the release of inflation data and retail sales on Friday, October 20 at 8:30 am EDT. The lack of solid economic data leaves the pair vulnerable to shifts in the political arena putting more weight on the NAFTA comments this week.

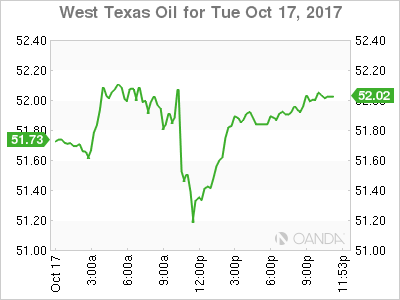

West Texas Intermediate is trading at $51.61. The price of crude rose as tensions intensified in Northern Iraq. Earlier today the Kurds retreated from Kirkuk and oil disruptions should be limited. Interruptions to the global oil supply have been the main drivers of the lift in oil prices. Social and political unrest in some oil producers, but also the landmark production cut agreement between Organization of the Petroleum Exporting Countries (OPEC) and other major suppliers.

The market will be watching the release of the weekly US crude inventories on Wednesday, October 18 at 10:30 am EDT. The report by the Energy Information Administration (EIA) is forecasted to show another major drawdown of around 4.7 million barrels.

Market events to watch this week:

Monday, October 16

5:45pm NZD CPI q/q

8:30pm AUD Monetary Policy Meeting Minutes

Tuesday, October 17

Tentative GBP BOE Gov Carney Speaks

4:30am GBP CPI y/y

Wednesday, October 18

4:30am GBP Average Earnings Index 3m/y

8:30am USD Building Permits

10:30am USD Crude Oil Inventories

8:30pm AUD Employment Change

10:00pm CNY GDP q/y

10:00pm CNY Industrial Production y/y

Thursday, October 19

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, October 20

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

7:15pm USD Fed Chair Yellen Speaks

Gold Slide Continues as Trump favors Hawkish Taylor for Fed Chair

Gold is down considerably in Tuesday trade. In the North American session, the spot price for an ounce of gold is $1284.70, down 0.80% on the day. On the release front, there are no major releases out of the US for a second straight day. Import Prices gained 0.7%, beating the forecast of 0.6%.On Wednesday, the focus will be on housing data, with the release of Housing Starts and Building Permits.

Gold has lost ground this week, declining about 1.5 percent. The metal has been under pressure following reports that President Trump is leaning towards nominating economist John Taylor as the new head of the Federal Reserve. Taylor is considered more hawkish on policy than the current head, Janet Yellen, whose term expires in February 2018. A more hawkish Fed could be more inclined to raise interest rates early in 2018, despite weak inflation, which would strengthen the greenback against gold. Other candidates for the Fed Chair include current Fed Governor Jerome Powell and former Fed official Kevin Warsh.

Gold prices often move higher in response to geopolitical tensions, and the simmering dispute in Catalonia could be one such trouble spot. The constitutional conflict could worsen later this week, as the Spanish government seems intent on ending Catalonia's bid for independence. Spanish Prime Minister Rajoy has insisted there will be no talks about independence with Catalan leaders, and has threatened to disband the Catalan parliament and impose direct rule from Madrid if Catalan President Carles Puigdemont does not recant his recent declaration of independence. The deepening crisis has led hundreds of companies to start leaving Catalonia, and the Standard and Poor's rating agency has said that the region could face a recession if the situation is not resolved. Earlier this month, Spain's economy minister said the uncertainty caused by the crisis had led to a freeze in investment projects in Catalonia. Investors are becoming more nervous about the crisis, and if the situation deteriorates, safe-haven gold could gain ground.

The US Dollar is Vulnerable, But It’s Temporarily

The US Dollar can't manage to continue growing, and the more attempts to rise it makes, the more doubts appear that it can really rise during this particular period of market fluctuations. The EUR/USD has clearly set a course for 1.20 and may resume falling only after reaching this level.

The statistics is against the USD so far. The numbers published last week, which were followed with insight, turned out to be weaker than expected and investors lost their interest (that was already very low) to the American currency. For example, the Retail Sales expanded by 1.6% m/m in September, which is quite good in comparison with the August reading of –0.1% m/m, but it's still less than the expected number of +1.7% m/m. The same can be told about the inflation in September. The CPI increased by 0.5% m/m after adding 0.4% in August. And that'd be okay, but investors expected +0.6% m/m. On top of that, the Core Inflation added only 0.1% m/m although it was expected to increase by 0.2% m/m.

Taken together, these two catalysts were able to make investors' attitude to the USD even more negative. The US Federal Reserve with the plan to sell assets on its balance sheet and the U.S. Department of the Treasury that was ready to increase the national debt were put on the back burner. Like it was already said, and it's still true, both of these plans will lead to the US Dollar strengthening. It's just a question of time.

There will be a lot of interesting statistical reports from the USA this week. In addition to that, Janet Yellen, the Chairwoman of the Federal Reserve, will speak on Friday. Speculations about candidates for her position died down for a while, but may revive at any moment.

Any information about possible activities of the US monetary authorities will support the Dollar regardless the market situation at that moment. One just have to wait, that's all.

The technical chart of the EUR/USD pair shows that the uptrend has transformed into the downtrend. We should also note that after breaking the main trend line, the price has fallen by the distance, which equals the width of the previous channel. If the instrument breaks the current support level, it may fall and reach 1.1550.

This chart shows the current descending movement in more details. The downtrend is clearly defined by the resistance and support levels. The sellers may worry that right now the price is moving close to the resistance level, because the pair may break it to the upside and grow to reach 1.2000, which is a psychologically-crucial level. However, if the "bears" push strong enough, the instrument may reverse and reach the support level at 1.1550.

GBPUSD Continues Falling Following Carney’s Speech

The price of EUR/USD continued to fall due to disappointing statistics from the ZEW Economic sentiment index. The index for Germany came in at 17.6 for October against the 20.1 forecast, while for the Eurozone it hit 26.7 versus the 34.2 forecasted. Growth in industrial production in the US of 0.3% in September against the 0.7% decline in the previous period gave a further downward push to the pair. Investors are waiting for tomorrow's speech by ECB President Mario Draghi where he may give some insights on the plans and timing of cuts to the asset purchasing program.

The British pound got a boost today from consumer inflation which grew to 3.0% in September compared to 2.9% in August. This increases the chance of an interest rate hike by the Bank of England happening sooner rather than later which is good news for the pound. Though an interest rate increase by 0.25% will only compensate the monetary easing from the previous year. However, the Bank of England's Governor, Mark Carney, didn't mention tightening monetary policy during his speech in parliament today. Volatility may remain high tomorrow due to the labour market data release in the UK.

The aussie dollar may see some action later today from the release of the MI leading index due out at 23:30 GMT. Earlier today the minutes of the Reserve Bank of Australia meeting were released with an optimistic forecast on the state of the Australian economy. AUD bulls' positive reaction however was short lived.

EUR/USD

The EUR/USD kept falling within the limits of the local descending channel and as a result is testing the support line at 1.1750. Breaking through 1.1750 may become a stimulus for continued price drops with the closest targets at 1.1700 and 1.1620. The growth potential is limited by the upper limit of the local descending channel.

GBP/USD

After some consolidation near 1.3250 the pound has shown a sharp descending move and is approaching the support level at 1.3150. Breaking through this mark is likely to stimulate the bears to pull the quotes down to the 1.3000-1.3050 range. On the other side, the RSI on the 15-minute chart is near the oversold zone which is the basis for a possible price rebound to 1.3250. Volatility is likely to remain high.

AUD/USD

The AUD/USD price resumed falling after some upward correction. The immediate goals in case of maintaining the current descending dynamics will be 0.7800 and 0.7740. If the quotes fix above the resistance at 0.7870 it may become a strong signal to buy with potentials to increase up to 0.8000 and above. Though today we're more likely to see a bearish sentiment.