Sample Category Title

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.77; (P) 132.07; (R1) 132.29; More...

EUR/JPY is trying to recovery after drawing support from 131.69. Intraday bias stays neutral first. On the downside decisive break of 131.69 will be an early sign of medium term reversal and will target 127.55 key support level. On the upside, firm break of 134.39 is needed to confirm up trend resumption. Otherwise, more corrective trading would be seen.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversal and will turn outlook bearish for deeper fall.

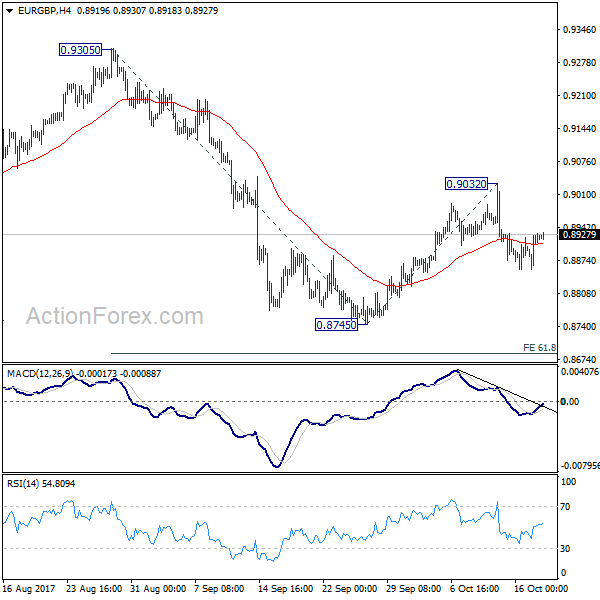

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8873; (P) 0.8901; (R1) 0.8945; More...

As long as 0.9032 resistance holds, risk will stay on the downside for EUR/GBP. Fall from 0.9032 should target 0.8745 low first. Break there will resume whole decline from 0.9305. In that case, it should target 61.8% projection of 0.9305 to 0.8745 from 0.9032 at 0.8686, and then 100% projection at 0.8472.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4961; (P) 1.4999; (R1) 1.5035; More....

No change in EUR/AUD's outlook. Deeper decline is expected as long as minor resistance holds. Consolidation pattern from 1.5226 is still unfolding with fall from 1.5241 as the third leg. Break of 1.4945 will affirm this case and send EUR/AUD through 1.4791 to 1.4421 support cluster support (50% retracement of 1.3624 to 1.5226 at 1.4425). We'd expect strong support from there to bring rebound. On the upside, though, above 1.5101 will turn focus back to 1.5241 instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Sustained trading above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

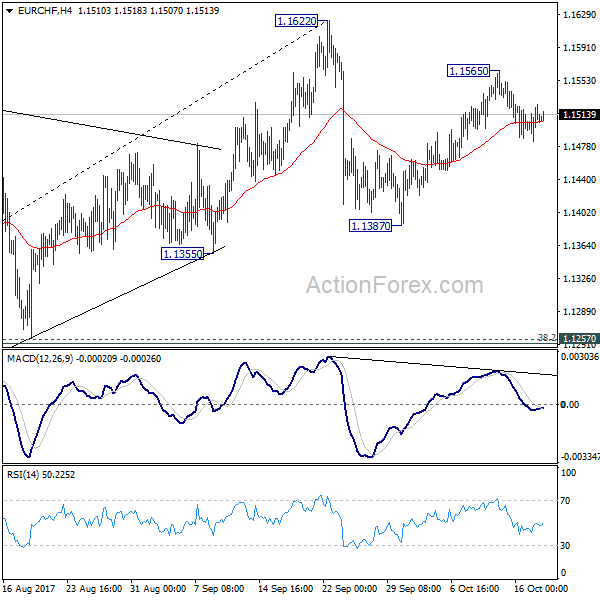

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1507; (R1) 1.1530; More....

As noted before, the recovery from 1.1387 could have completed at 1.1565 already. Intraday bias is mildly on the downside for 1.1387 support first. Break there will extend the correction from 1.1622 and should target 1.1257 cluster support (38.2% retracement of 1.0652 to 1.1622 at 1.1251). We'd expect strong support from there to bring rebound.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1198 resistance turned support holds.

AUDUSD Maintains Soft Undertone In Short-Term

AUDUSD maintains a soft undertone and the neutral to bearish technical indicators are supporting the bearish view for the short term.

The downward move from the 0.8124 peak is still in progress after the recent bounce off 0.7732 reversed back down as prices found resistance at the 50-day moving average.

AUDUSD may be forming a lower top at 0.7897 to continue the downtrend. This would be confirmed if prices break below the 50% Fibonacci retracement level of the uptrend from 0.7328 to 0.8124. This level is acting as support at 0.7725. From here the market remains at risk of additional losses towards the 0.7500 area before re-testing the 0.7328 low.

Should prices break above the 50-day MA (0.7909), AUDUSD would shift the focus back to the upside to target the key 0.8000 level and then the 0.8124 peak, with scope to resume the uptrend that started from 0.7328.

Looking at the bigger picture, the underlying market structure is still bullish as the pullback from 0.8124 is not that deep yet. Prices are currently only at the 38.2% Fibonacci retracement level.

Central Bank Speakers Headline Wednesday Session

Wednesday will be an active session in the global financial markets, as investors sift through a steady stream of economic data and key remarks from a parade of central bank speakers.

Monetary policy is on the docket early Wednesday as European Central Bank (ECB) President Mario Draghi delivers a speech at 08:10 GMT. A stronger Eurozone recovery through the first nine months of the year suggests the ECB could be willing to begin normalizing monetary policy in the near future.

ECB officials Peter Praet and Benoit Coeure are also scheduled to speak during the North American session.

Europe’s data wire kicks off at 08:30 GMT with British employment numbers. The UK’s claimant count change is forecast to rise by 1,000 for the month of September. The ILO-calculated unemployment rate is projected to hold steady at 4.3% annually in the three months ending August.

Average hourly earnings for UK workers is forecast to rise 2% annually over the same period.

The European Commission’s statistical agency will report on Eurozone construction output at 09:00 GMT.

A pair of Federal Reserve officials will kick off the North American session. Federal Open Market Committee (FOMC) member Robert Kaplan and New York Fed president William Dudley will deliver speeches around 12:00 GMT.

Data from the US Commerce Department will report on housing starts and building permits at 12:30 GMT. North of the border, Canada will also release manufacturing data at the same time.

Traders will also be keeping an eye on the Fed’s Beige Book, which is scheduled for release at 18:00 GMT. The Beige Book provides a snapshot of the current US economic situation.

Finally, energy traders will monitor the weekly crude inventory report at 14:30 GMT.

EUR/USD

The euro succumbed to pressure on Tuesday, falling back below 1.1800 US. While the common currency remains supported over the short-term, there is a risk of a further breakdown toward the 1.1700 region. The EUR/USD is currently feeling the pinch of a rebounding US dollar. The world’s most actively traded currency has gained in each of the past four sessions.

GBP/USD

The British pound also backtracked on Tuesday, as investors continued to back the US dollar. Cable opened around 1.3190, and was little changed at the time of writing. Above 1.32, the GBP/USD is likely to run into resistance near 1.3260. On the flipside, a fall back toward the 1.3160 region would expose the short-term support signal near the 12 October low of 1.3120.

USD/CAD

The USD/CAD reached a high of 1.2573 on Tuesday, which would have marked the best settlement in 11 days. The pair would later surrender most of its gains to settle near 1.2500. The bulls appear to be hesitating now that the USD/CAD is back at 1.2500. This suggests the market will remain neutral for the time being.

EURO Still Bearish Below 1.1780

The euro continues to struggle below the 1.1780 level against the U.S dollar, after earlier finding strong support from the 1.1736 level. Price-action continues to consolidate around the 1.1760 level, as investors begin to focus on a scheduled speech by European Central Bank President Mario Draghi later this morning.

The EURUSD continues to remain under bearish selling pressure while price trades below the 1.1780 resistance level. Further losses can be expected towards the former weekly pivot point, at 1.1740, and the 2015 price-high, at 1.1713. Extended support is found at the euro's 200-week moving average, at 1.1685.

If price-action moves above the 1.1780 level during Wednesday trading, further gains can be seen towards the daily pivot point, at 1.1798, and the euro's weekly pivot point, at 1.1807. Extended intraday resistance is found at the 1.1821 and 1.1833 levels.

Further GBPUSD Losses Expected Below 1.3200

The British pound continues to weaken against the U.S dollar, as Brexit negotiations remain deadlocked between the UK and the European Union. The pair is currently trading around the 1.3180 support level, after yesterday slipping to 1.3154. Traders now await the release of key unemployment and wage data from the United Kingdom economy.

Further GBPUSD selling pressure is expected while the pair trades below the key 1.3200 level. Intraday losses can be seen towards the 1.3154 and 1.3130 support level, with extended intraday support located at 1.3121 and 1.3080.

A sustained move above the 1.3200 level can lead to further intraday gains towards 1.3224 and 1.3233. Extended intraday resistance is located at the 1.3255 and 1.3280 levels.

British Pound Downtrend Intact Vs US Dollar

Key Highlights

- The British Pound recovered well from 1.3030, but faced strong offers near 1.3300 against the US Dollar.

- A key bearish trend line with current resistance at 1.3260 on the 4-hours chart of GBP/USD is acting as a barrier.

- The US Industrial Production in Sep 2017 posted a 0.3% rise, more than the +0.2% forecast.

- Today in the UK, the Claimant Count Change for Sep 2017 will be released, which is forecasted to register 1.0K.

GBPUSD Technical Analysis

The British Pound corrected sharply from the 1.3030 level against the US Dollar. However, the GBP/USD pair is struggling to settle above 1.3300 and remains at a risk of more declines.

The pair recently failed to break the 100 simple moving average near 1.3330 (4-hour, red) and started a downside move. It also failed near a key bearish trend line with current resistance at 1.3260 on the 4-hours chart.

Sellers succeeded in pushing the pair below the 50% Fib retracement level of the last wave from the 1.3027 low to 1.3337 high.

Therefore, there are chances of further losses in GBP/USD as long as the pair is below the 1.3300 resistance.

US Industrial Production

Recently in the US, the Industrial Production for Sep 2017 was released by the Board of Governors of the Federal Reserve. The forecast was slated for a 0.2% rise compared with the previous month.

The actual result was better the forecast, as there was an increase of 0.3% in the production in Sep 2017. It was way above the last revised decline of 0.7%.

The report stated:

For the third quarter as a whole, industrial production fell 1.5 percent at an annual rate; excluding the effects of the hurricanes, the index would have risen at least 1/2 percent. Manufacturing output edged up 0.1 percent in September but fell 2.2 percent at an annual rate in the third quarter.

The GBP/USD was pressured after the release and is currently at risk of more losses below 1.3240.

Economic Releases to Watch Today

- UK Claimant Count Change Sep 2017 – Forecast 1K, versus -2.8K previous.

- UK ILO Unemployment Rate August 2017 (3M) – Forecast 4.3%, versus 4.3% previous.

- UK Average Earnings Including Bonus August 2017 (3Mo/Year) – Forecast +2.1%, versus +2.1% previous.

- UK Average Earnings Excluding Bonus August 2017 (3Mo/Year) – Forecast +2.0%, versus +2.1% previous.

- US Housing Starts Sep 2017 (MoM) – Forecast 1.175M, versus 1.180M previous.

- US Building Permits Sep 2017 (MoM) – Forecast 1.25M, versus 1.30M previous.

Forex: UK Inflation At 5-Year High

The likelihood of a rise in UK interest rates, for the first time in a decade, gained momentum on Tuesday as UK CPI edged up from 2.9% to 3.0% – its highest level since April 2012. Bank of England Governor Mark Carney did nothing to dispel a rate hike as he gave evidence to the UK Treasury select committee where he stated that the fall in the value of GBP, since the Brexit vote last year, has resulted in higher prices paid for imported goods which will take up to three years to 'work its way through the economy'. With poor economic data, uncertainty over the Brexit process and a squeeze on real earnings the Bank of England's decision to hike rates is delicately balanced.

With raised tensions in the Middle East, the price of Oil rose on Tuesday as the markets are concerned that supply distribution could be disrupted. The API report out of the US showed a bigger than expected drawdown in US inventories which, when added to the fighting in Kirkuk, Iraq and the continued tensions between Iran and the US, helped push Oil prices higher. Official US fuel inventory will be released today by the EIA which may help push Oil prices higher if, as forecast, there is a significant drawdown.

China's President Xi Jinping delivered a keynote speech to the Communist Party congress in Beijing. The twice-a-decade congress is expected to cement the power of Xi who stated early on in his speech that the 'market will be allowed to play a decisive role in allocating resources'. 'Currently, conditions domestically and abroad are undergoing deep and complicated changes, our country is in an important period of strategic opportunity in its development,' he said in a calm, steady voice. 'The outlook is extremely bright; the challenges are also extremely grim.' The markets will be watching the congress meeting this week for any suggestion of whether Xi may be looking to appoint a successor to take over after his traditional second five-year term in office.

EURUSD is little changed in early Wednesday trading. Currently, EURUSD is trading around 1.1760.

USDJPY is trading close to Tuesday's close. Currently, USDJPY is trading around 112.30.

GBPUSD is currently trading near early session lows around 1.3182.

Gold is 0.12% higher in early trading. Currently, Gold is trading around $1,285.

WTI is 0.2% higher on Wednesday to currently trade around $52.32.

Major data releases for today:

At 09:10 BST, ECB President Mario Draghi is scheduled to present the opening speech at the ECB Conference 'Structural reforms in the euro area' in Frankfurt, Germany.

At 09:30 BST, UK National Statistics are scheduled to release Average Earnings including bonus (3Mo/Yr) for August. Consensus is calling for an unchanged 2.1%. The markets will be keen to see if UK average earnings are rising in line with inflation. If they are, we can expect the Bank of England to raise rates in the near future. If they are lagging inflation, then real earnings are lower and it may be difficult for the Central Bank to justify a rate hike.

At 13:00 BST, New York Federal Reserve Bank President William Dudley and Dallas Federal Reserve Bank President Robert Kaplan are scheduled to speak on New York & Texas (respectively) at the Centers of Growth breakfast conversation at Hearst, in New York.

At 13:30 BST, the Us Census Bureau, at the Department of Commerce, is scheduled to release Housing Starts Change for September. The previous poor release of -0.8% is expected to be improved upon with consensus suggesting a release of -0.5%. Whilst the data is still expected to be negative, the markets are aware that the recent Hurricanes are still impacting building in certain states.

At 15:30 BST, the US Energy Information Administration will release data for Crude Oil Stocks change for the week ending October 13. The consensus is calling for a drawdown of -4.750M compared to the previous draw of -2.747M. Expect volatility in Oil if the released number is significantly different from the consensus.