Sample Category Title

Loonie Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.5% against the CAD and closed at 1.2455.

In the Asian session, at GMT0300, the pair is trading at 1.2454, with the USD trading marginally lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2421, and a fall through could take it to the next support level of 1.2388. The pair is expected to find its first resistance at 1.2509, and a rise through could take it to the next resistance level of 1.2564.

Ahead in the day, market participants will focus on Canada’s new housing price index for August.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

GBP/JPY Yen Demolished By Nikkei’s Rally

The GBP/JPY increased in the last days and now stands above the 148.46 static resistance (support turned into resistance). The Yen is punished by the Nikkei's rally and could depreciate further versus all its rivals, not only against the Pound. A minor consolidation will send the rate towards the 151.66 static resistance.

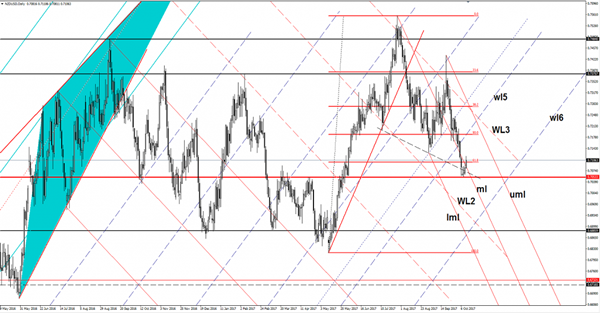

NZD/USD Breakout In Play

The NZD/USD jumped above the median line (ml) of the minor descending pitchfork and above the 61.8% retracement level. A valid breakout above these levels will signal a further increase on the short term. It could approach the upper median line (uml) of the minor descending pitchfork if the USDX will slide further.

Resistance could be found at the 0.7131 level and much higher at the 50% retracement level. I’ve said in a previous report that the rate could develop a Falling Wedge pattern, but this is far from being confirmed.

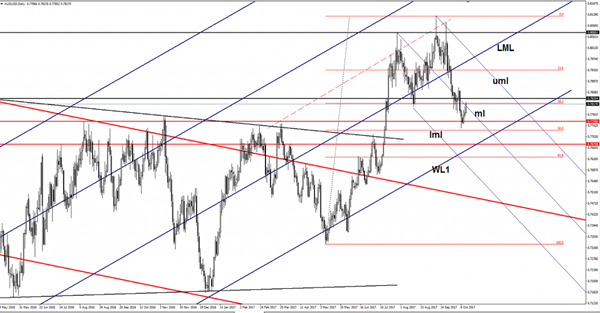

AUD/USD Bulls In Control

The AUD/USD rallies and extends the minor bounce back movement. Price climbed above a dynamic resistance line and tries to reach new obstacles on the short term. The AUD has taken full control on the short term as the USD is punished by the USDX’s aggressive drop. The dollar index continues to drop after the FOMC Meeting Minutes were released, but this could be only a temporary drop.

The Aussie received a helping hand from the Australian Home Loans, which has increased by 1.0% in August, more versus the 0.5% estimate, while the MI Inflation Expectations rose by 4.3%, more versus the 2.8% estimate.

You should be careful in the afternoon as the US is to release high impact data, the PPI is expected to increase by 0.4%, more versus the 0.2% in the previous reading period, while the Unemployment Claims could drop to 251K in the previous week.

Price rallied after the false breakdown below the 0.7755 static support and now is located above the median line (ml) of the minor descending pitchfork. Right now is pressuring the 38.2% retracement level and could reach the 0.7835 static resistance very soon.

A retest of the broken median line (ml) will confirm an increase towards the upper median line (uml) of the minor descending pitchfork. Price maintains a bearish perspective on the short term as long as is trading within the minor pitchfork’s body.

Elliott Wave View: FTSE Short-Term

FTSE Short term Elliott Wave structure shows Primary wave ((4)) ended at 7196.58 on 9/15 low. Rally in Primary wave ((5)) up from there has internal subdivision of a zigzag Elliott Wave structure. Intermediate wave (A) of this zigzag structure is in progress as 5 waves impulse where rally to 7327.50 ended Minor wave 1 and bounce to 7289.75 ended Minor wave 2. Rally to 7527.59 ended Minor wave 3 and Minor wave 4 pullback ended at 7493.68. Minor wave 5 of (A) higher remains in play and could see more upside before ending the cycle from 9/15 low.

Chasing the rally higher at this stage is risky since cycle from 9/15 low is mature and Intermediate wave (A) could end soon. After Intermediate wave (A) is complete, expect Index to pullback in Intermediate wave (B) in 3, 7, or 11 swing to correct cycle from 9/15 low (7196.58) before the rally resumes. We do not like selling the proposed pullback. We favor Index to extend to a new high after Intermediate wave (B) pullback has ended later as far as pivot at 9/15 low stays intact.

FTSE 1 Hour Elliott Wave Chart

Zigzag is one of the most popular Elliott Wave corrective structures. It’s subdivided into 3 waves and labelled as ABC. The first leg wave A has an internal subdivision of 5 waves and it can either be an impulse or a diagonal. The second leg wave B can unfold in any corrective structure. Finally, the third leg wave C also has an internal subdivision of 5 waves and can also be either an impulse or a diagonal. Zigzag therefore is a 5-3-5 Elliott Wave structure. Wave C typically ends at 100% – 123.6% of wave A.

Market Update – Asian Session: Dollar Weakness Resumes After Fed Minutes

Asia Summary

Asian equity markets opened mostly higher. China markets remains muted ahead of next week’s Communist Party congress, while as expected Nikkei closed at a 20-yr high yesterday. While currencies were muted early in the session, dollar weakness resumed heading into afternoon trade, with US Fed minutes showed there is still uncertainty on timing of rate increases. South Korea’s Q3 FDI fell 9.7%, notably YTD China investment into South Korea fell 63% y/y to $608M amid rising tension between the two countries.

China Govt said to be pushing some of the large tech firms to give the Govt a stake in the company and a direct role in corporate decisions. Internet regulators have discussed taking 1% stakes in Tencent, Weibo, Youku Tudou and Alibaba.

Looking ahead to tomorrow we will see Singapore Central Bank (MAS) announces any changes to policy. MAS is widely seen sticking to a neutral stance tomorrow, but it may be moving closer to tightening policy as the economy continues to strengthen. China will also report Sept trade data.

Key economic data

(AU) AUSTRALIA AUG HOME LOANS M/M: 1.0% V 0.5%E; INVESTMENT LENDING: +4.3% V -3.9% PRIOR

(JP) JAPAN SEPT PPI (CGPI) M/M: 0.2% V 0.2%E; Y/Y: 3.0% V 3.0%E

(AU) Australia Oct Consumer Inflation Expectation: 4.3% v 3.8% prior

(NZ) New Zealand Oct ANZ Consumer Confidence Index: 126.3 v 129.9 prior; m/m: -2.8% v 2.9% prior

(KR) South Korea Q3 Foreign Direct Investment (FDI) y/y: -9.7% v -9.0% prior

(JP) Japan Sept Tokyo Avg Office Vacancies m/m: 3.2% v 3.4% prior (lowest level since Apr 2008)

Speakers and Press

Japan

(JP) Nikkei poll shows Japan's ruling coalition winning close to 300 of the 465 seats in the Diet's lower house ahead of Oct 22nd election

US

(US) Fed’s Bostic (non-voter, dove): Balance sheet size once normalized is an open question; balance sheet rolloff start not seen significant timing - speaking in Hong Kong

(US) US President Trump: Looking at ~10% repatriation tax rate (from current 35%)

Australia/New Zealand

(NZ) New Zealand First Party Leader Peters: NZ First board not likely to meet Friday

(AU) IMF lowers Australia 2017 GDP outlook to 2.2% from 3.1% in Apr

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.5%, Hang Seng +0.3%; Shanghai Composite -0.2%; ASX200 +0.2%, Kospi +0.3%

Equity Futures: S&P500 -0.1%; Nasdaq100 +0.0%, Dax +0.0%; FTSE100 +0.0%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1878-1.1858; JPY 112.52-112.32; AUD 0.7824-0.7788;NZD 0.7110-0.7087

Dec Gold +0.7% at $1,297/oz; Nov Crude Oil -0.5% at $51.03/brl; Dec Copper -0.1% at $3.09/lb

(CN) China PBOC injects CNY20B v CNY20B in 7-day reverse repos prior; drains net CNY40B v none prior

USD/CNY (CN) China PBOC sets yuan reference rate at 6.5808 v 6.5841 prior

(TH) Thailand Central Bank sells THB20B in 14-day bonds; avg yield 1.12188%; bid-to-cover 2.38x

Equities notable movers

Australia/New Zealand

BAL.AU Raises FY18 Rev target 15-20% y/y (prior 5-10%); EBITDA margin 17-20% (prior 15-20%); +6%

LOV.AU To open pilot store in US – press; +8%

Japan

8028.JP Reports H1 Net ¥22.4B v ¥11.9B y/y; Op ¥33.5B v ¥20.1B y/y; Rev ¥633.6B v ¥211.5B y/y; -4%

5406.JP CEO apologizes for false data, have finished probes for ~100 of 200 companies; more 'irregularities' may come to light; Thus far no customers have cancelled orders; +1.1%

Korea

047810.KR Former and current executives were indicted by South Korean prosecutors over charges of inflating KRW535.8B in sales and KRW46.5B in net profit from 2013 to Q1 2017; halted

China/Hong Kong

2382.HK Reports Sept shipments of handset lens: +0.9% m/m; production -9.1% m/m; -4%

Fed Split On Inflation Intensified At September Policy Meeting

Dollar Sagged after Fed Showed Guarded View Towards Inflation. Fed policymakers had a prolonged debate about the inflation and the path of future interest rate. While this did little to cool strong expectations for the Fed to raise interest rates in December, it did make the central bank appear slightly less hawkish than it appeared right after the September policy meeting when it signaled the year-end monetary tightening. The dollar index slipped to a two-week low of 92.891.

Gold Extends Gains After Latest Fed Meeting Minutes. Gold continued its rally for a fourth straight day after U.S. Federal Reserve showed policymakers debated the prospects of a pickup in inflation and the path of future interest rate rises if it did not. The U.S. central bank should gradually increase interest rates over the next two years, bringing the federal funds rate to 2.5 percent. Spot gold was up 0.4 percent at $1,293.92 per ounce, silver rose 0.8 percent to $17.22 per ounce.

Oil Drops on Rising U.S. Crude Inventories, OPEC Seen to Extend Cuts. Oil prices eased on Thursday as U.S. fuel inventories rose despite efforts by OPEC to cut production and tighten the market. U.S. WTI crude futures were trading at $51.08 per barrel, down 0.4 percent from their last settlement, Brent crude futures were at $56.62, down 0.6 percent from the previous close.

Market Morning Briefing: Gold And Silver Are Almost Stable

STOCKS

Dow (22872.89, +0.18%) is trading just on the resistance on the 3-day candles but at the same time has broken resistance on the weekly candles indicating a further rise towards 23250 on the cards. While above 22850, 23000-23250 levels could be tested soon. .

Dax (12970.68, +0.17%) is trapped in the 13000-12900 region and could trade sideways for some time. While trading below 13000-13035 levels it is likely that the index would come off towards 12850 in the near term. A break above 13035 would be surprising and could indicate fresh bulls coming into the picture.

Nikkei (20978.56, +0.47%) has been rallying up and has almost reached our target resistance of 21000. This would be crucial to watch. A sustained break above 21000, if seen could indicate strong bullish momentum and could take the index towards 22000 and higher while a rejection from 21000, could initiate fresh bears for the longer term.

Shanghai (3383.44, -0.14%) is almost stable and could trade within 3400-3375 region in the near term.

Nifty (9984.80, -0.32%) came off sharply yesterday to levels below 10000. In case the index fails to bounce back again above 10000 in the near term., the corrective dip could continue towards 9900.

COMMODITIES

Gold (1293.6) and Silver (17.17) are almost stable. Gold could test 1300 in the next few sessions while Silver could see a corrective dip towards 17.00-16.80 or at least remain stable near current levels.

Brent (56.61) and WTI (51.02) are almost stable as seen yesterday. As mentioned yesterday, Brent has scope of rising towards 57.45 and WTI could rise to 51.50-52.00 before seeing another down leg.

Copper (3.0895) has moved up sharply as expected. Either the price may pause near 3.10 or if it moves higher, we could see a re-test of levels near 3.18-3.20 in the near term.

FOREX

Keep a close watch on the German-US 10YR spread (See Interest Rates Section below) which had indicated a rise in Euro in the last couple of sessions. Euro (1.1873) could further strengthen towards 1.1950 while the yield spread remains higher.

Dollar Index (92.84) is headed towards 92.50 again and looks bearish for the near term.

The down move has come in faster than our expectation and a break below 92.50 could turn bearish towards 92 in the medium term.

Dollar Yen (112.374) is unable to give any directional clarity just now. While the price tries to break below 112.00, it could eventually head towards 111.50; else a rise back towards 113.00-113.25 is possible.

Dollar Rupee (65.15) could possibly move up towards 65.20/25 again while trying to attempt a test of 65.10-65.00 on the downside.

INTEREST RATES

The US yields look slightly positive today. The US 10-5YR (0.39%) has fallen sharply and could test support near 0.3750 before again bouncing back to higher levels. This could indicate that the 10YR could possibly fall compared to the 5Yr in the coming sessions or the 5Yr (1.96%) could rise fast keeping the 10Yr yield (2.35%) stable.

The German-US 10YR (-1.88%) has bounced as expected pulling up Euro also with itself. The spread looks positive for the near term and could indicate a further rise in Euro in the coming sessions.

Fed On Track To Raise Rate In December

The FOMC minutes for the September meeting anchored the Fed's stance to hike policy rate for one more time this year. While the views on economic growth developments remained broadly unchanged from previous meetings, the members appeared more concerned over the inflation outlook. The minutes included detailed discussions on the impacts hurricanes Harvey, Irma, and Maria. Yet, they were expected to have limited impacts on US growth and inflation. The market has priced in almost 90% chance of a rate hike in December. The bet shows little change after the release of the minutes.

There was a long discussion on inflation. As the minutes suggested, 'many' participants continued to believe 'cyclical pressures' would 'show through to higher inflation' in the medium term and 'many judged that at least some of the softening this year to be idiosyncratic'. Moreover, the members 'continued to project that inflation would edge higher in the next couple of years and that it would reach the Committee's longer-run objective in 2019'. Note that the phrase 'edge high' is less hawkish that the term 'increase' used in July. On the other hand, the minutes also suggested that 'several' participants were concerned that 'the persistence of low rates of inflation might imply that the underlying trend was running below 2%, risking a decline in inflation expectations'. On net, the FOMC 'on balance' forecasted that PCE inflation would stabilize around the target over the medium term. This was compared to 'most participants' in the July minutes.

On the growth outlook, the members suggested that that the economy was 'rising at a moderate pace' in 3Q17 'before the landfall of Hurricanes Harvey and Irma'. They expected the negative effects of those disasters would 'restrain national economic activity only in the near term'. The members acknowledged solid payroll growth and noted that the unemployment rate remained low. They, however, also noted that the 'Increases in most aggregate measures of hourly wages and labor compensation remained subdued'.

These would unlikely alter the Fed's rate hike schedule. The minutes revealed that 12 out of 16 participants projected three rate hikes in 2017. Many believed that another rate increase in this year was likely to be warranted 'if the medium term outlook remained broadly unchanged'. 'Several' would see if 'the economic data in coming months increased their confidence that inflation was moving up toward the Committee's objective' while 'a few' indicated that 'additional increases in the federal funds rate should be deferred until incoming information confirmed that the low readings on inflation this year were not likely to persist' and 'that inflation was clearly on a path toward the Committee's symmetric 2%' target in the medium term.

FOMC Minutes: Core Members Still Want To Hike In December

In our view, there was nothing new of great importance in the FOMC minutes, as we already know the different positions among the FOMC members. This also explains why markets did not react to the minutes. While the most dovish FOMC members (Brainard, Evans and Kashkari) are arguing that the Fed should not hike further this year, as low inflation may not be just transitory due to low inflation expectations and labour market slack, the core FOMC members think it is appropriate to tighten monetary policy further, as above-trend growth tightens the labour market further, which eventually leads to higher wage growth and hence higher inflation; in other words, they still have a strong belief in the Phillips curve. They will likely feel relieved by the latest average hourly earnings figures, which came out much higher than expected in September.

It remains our base case that the Fed hikes in December, as the core voting FOMC members put more weight on labour market data than current inflation data, although we agree with the dovish camp that low inflation may not be temporary due to low inflation expectations. It is difficult to say what happens next year, as we do not know who the next Fed chair is and who the Fed nominates for the vacant seats on the Board of Governors. Our base case is right now two hikes. While market pricing for a December hike seems fair, markets still price in too few hikes next year.

What we looked for were any discussions on the Fed's target level for its balance sheet. However, as expected, there was nothing on this, as the Fed likely wants to keep its flexibility adjusting the target along the way. ‘Quantitative tightening' is new to the Fed, so it likely does not see any benefits from pre-committing. As we have written previously, it is not straightforward just to shrink the balance sheet due to increased regulation, see Research US: Fed's regulatory hurdle for starting quantitative tightening. The Fed has also acknowledged this and said that the level will be higher than before the crisis.