Sample Category Title

Daily Wave Analysis: GBP/USD ABC Zigzag Arrives At Key Fibonacci Resistance Zone

Currency pair GBP/USD

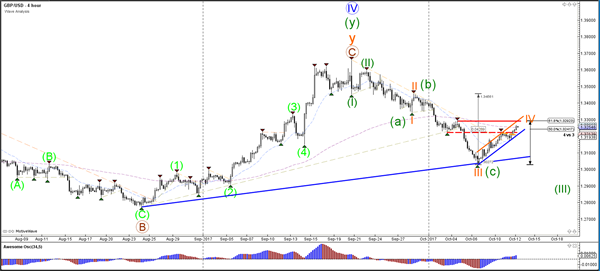

The GBP/USD bullish channel (blue/orange lines) is challenging the Fibonacci levels of wave 4 (orange). A break above the 61.8% Fib makes a wave 4 less likely and could indicate a larger bullish reversal. In that case, an ABC (green) correction has probably occurred. However, a failure to break the resistance zone but a break below the channel could spark a bearish continuation to test the outer trend line connecting the wave 3 (orange bottom).

The GBP/USD bearish break below the support trend line (blue) could indicate the completion of wave 4 (orange) and the continuation of the downtrend. A break above the resistance top and 61.8% Fib makes a wave 4 less likely. For the moment an ABC (green) zigzag correction could be taking place.

Currency pair EUR/USD

The EUR/USD bullish channel (blue lines) is now challenging a potential resistance trend line (orange). It is unclear whether price is in a wave 5 or in an expanded wave 4 at the moment, which depends on how price develops within the bullish channel.

The EUR/USD bullish momentum has reached the 161.8% Fibonacci target and could be in a wave 3 (blue). A shallow retracement could indicate a potential wave 4 and a continuation within the bullish channel.

Currency pair USD/JPY

The USD/JPY could be building a larger correction within wave 2 or B (purple).

The USD/JPY could have completed a potential ABC (purple) correction within wave X (purple).

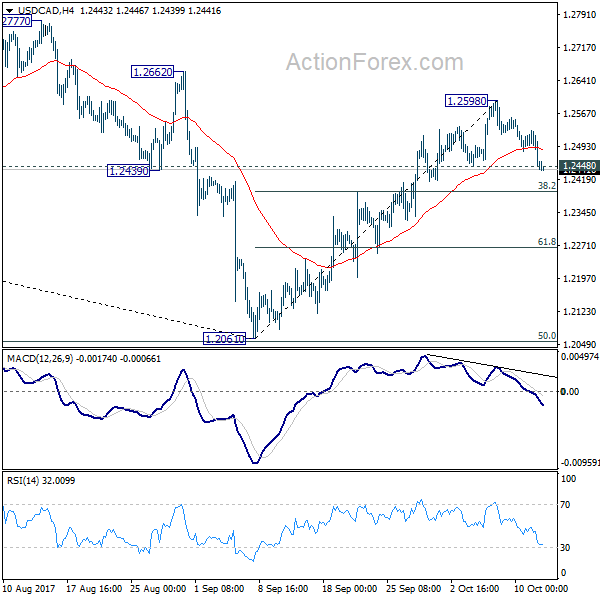

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2431; (P) 1.2481; (R1) 1.2509; More....

USD/CAD's break of 1.2448 minor support suggest that a short term top is formed at 1.2598, after failing to sustain above 55 day EMA. Intraday bias is turned back to the downside for 38.2% retracement of 1.2061 to 1.2598 at 1.2393, or even further to 61.8% retracement at 1.2266. But we'll look for bottoming sign below 1.2266. On the upside, break of 1.2598 will resume the rise from 1.2061 for 1.2777 resistance.

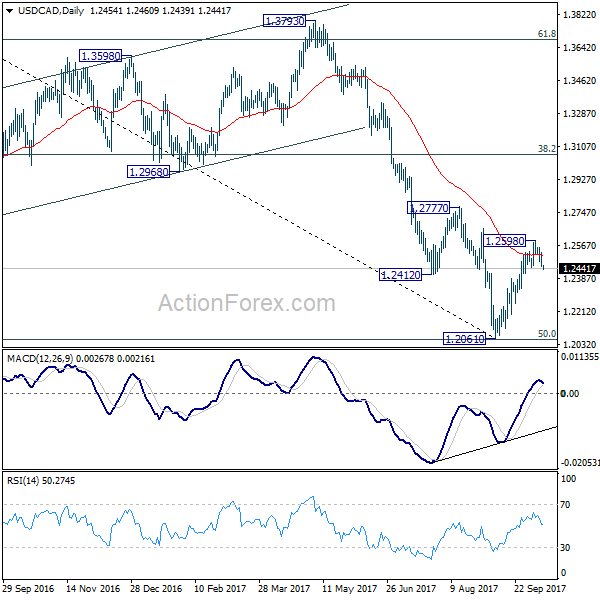

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Trade Idea : EUR/USD – Buy at 1.1820

EUR/USD - 1.1878

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1869

Kijun-Sen level : 1.1841

Ichimoku cloud top : 1.1703

Ichimoku cloud bottom : 1.1774

Original strategy :

Buy at 1.1780, Target: 1.1880, Stop: 1.1745

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1820, Target: 1.1920, Stop: 1.1785

Position : -

Target : -

Stop : -

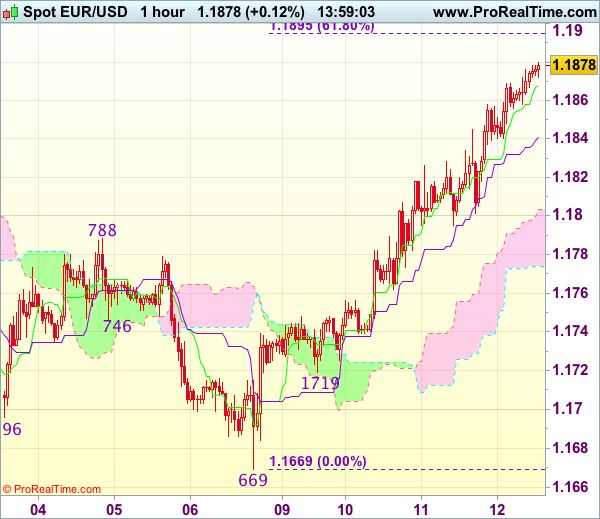

As the single currency has continued heading north after brief pullback, adding credence to our view that recent decline from 1.2093 top has ended at 1.1669 last week and mild upside bias remains for this move to extend gain to 1.1895-00 (61.8% Fibonacci retracement of 1.2035-1.1669), however, near term overbought condition should prevent sharp move beyond 1.1930-35 (61.8% Fibonacci retracement of 1.2093-1.1669) and 1.1970 should remain intact, bring retreat later.

In view of this, would not chase this rise here and we are still looking to buy euro on subsequent pullback as 1.1815-20 should limit downside and bring another rebound. Below minor support at 1.1795 would defer and risk correction to 1.1770 but downside should be limited to 1.1745-50 and price should stay above indicated support at 1.1719, bring another rise later.

Dollar Tumbled, Stocks Surged as Markets Saw FOMC Minutes as Slightly Dovish

US equities surged to new records while Dollar was pressured as markets perceived FOMC minutes released as slightly dovish ones. DOW rose 42.21 pts or 0.18% to close at 22872.89. S&P 500 rose 4.6 pts or 0.18% to close at 2555.24. Both were new record highs. 10 year yield was flat though at 2.345. Dollar index dipped to as low as 92.89 and breach of 92.94 near term support now suggests more downside in near term. Gold hits as high as 1297.9 in Asian session and is set to take on 1300 handle, comparing to last week's low at 1262.8. That is consistent with Dollar's weakness this week. Meanwhile, Sterling and Euro remain the strongest ones for the week so far, Yen trails behind Dollar as the second weakest.

Fed fund futures are pricing in 88% chance of a December hike, slightly lower that yesterday's 93%. Nonetheless, Fed is still on track for a December hike. The markets seemed to be focused more on the split view regarding inflation, seeing the long discussions on the topic in the minutes. As the minutes suggested, 'many' participants continued to believe 'cyclical pressures' would 'show through to higher inflation' in the medium term and 'many judged that at least some of the softening this year to be idiosyncratic'. Moreover, the members 'continued to project that inflation would edge higher in the next couple of years and that it would reach the Committee's longer-run objective in 2019'.

Note that the phrase 'edge high' is less hawkish that the term 'increase' used in July. On the other hand, the minutes also suggested that 'several' participants were concerned that 'the persistence of low rates of inflation might imply that the underlying trend was running below 2%, risking a decline in inflation expectations'. On net, the FOMC 'on balance' forecasted that PCE inflation would stabilize around the target over the medium term. This was compared to 'most participants' in the July minutes.

More on FOMC Minutes

- Fed On Track To Raise Rate In December

- FOMC Minutes: Core Members Still Want To Hike In December

- Fed Minutes Show Confidence in Economic Outlook, But Some Concern Over Weak Inflation

- Fed Reaffirms Likely December Rate Hike Despite Concerns Over Weak Inflation

Fifth round of Brexit negotiations to conclude without conclusions

The fifth and final round of Brexit negotiation before EU summit on October 19/20 is set to end. So far, there is no positive news coming out from UK and EU officials s. Brexit Secretary David Davis and EU's chief Brexit negotiator Michel Barnier will sum up the state later today. There is practically no chance for having "sufficient progress" to move on to post-Brexit trade agreements. And earlier this week, European Council President Donal Tusk warned that if the current "slow pace" of negotiations continued the UK and the EU would "have to think about where we are heading". And, it's doubtful whether that no conclusion could be made even until December.

On the data front

Japan domestic CGPI rose 3.0% yoy in September. Australia consumer inflation expectation rose 4.3% in October, home loans rose 1.0% in August. UK RICS house price balance was unchanged at 6 in September. Eurozone industrial production will be featured in European session. US PPI, jobless claims and Canada new housing price index will be released in US session.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2431; (P) 1.2481; (R1) 1.2509; More....

USD/CAD's break of 1.2448 minor support suggest that a short term top is formed at 1.2598, after failing to sustain above 55 day EMA. Intraday bias is turned back to the downside for 38.2% retracement of 1.2061 to 1.2598 at 1.2393, or even further to 61.8% retracement at 1.2266. But we'll look for bottoming sign below 1.2266. On the upside, break of 1.2598 will resume the rise from 1.2061 for 1.2777 resistance.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Sep | 6.00% | 4.00% | 6.00% | |

| 23:50 | JPY | Domestic CGPI Y/Y Sep | 3.00% | 3.00% | 2.90% | |

| 0:00 | AUD | Consumer Inflation Expectation Oct | 4.30% | 3.80% | ||

| 0:30 | AUD | Home Loans Aug | 1.00% | 0.50% | 2.90% | 2.80% |

| 4:30 | JPY | Tertiary Industry Index M/M Aug | 0.10% | 0.10% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M Aug | 0.60% | 0.10% | ||

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.30% | 0.40% | ||

| 12:30 | USD | PPI M/M Sep | 0.40% | 0.20% | ||

| 12:30 | USD | PPI Y/Y Sep | 2.60% | 2.40% | ||

| 12:30 | USD | PPI Core M/M Sep | 0.20% | 0.10% | ||

| 12:30 | USD | PPI Core Y/Y Sep | 2.00% | 2.00% | ||

| 12:30 | USD | Initial Jobless Claims (OCT 07) | 253K | 260K | ||

| 14:30 | USD | Natural Gas Storage | 42B | |||

| 15:00 | USD | Crude Oil Inventories | -6.0M |

Australia’s Consumer Inflation Expectation Jumped In October

For the 24 hours to 23:00 GMT, the AUD rose 0.22% against the USD and closed at 0.7796.

LME Copper prices rose 0.7% or $44.0/MT to $6685.0/MT. Aluminium prices declined 0.4% or $9.0/MT to $2124.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7809, with the AUD trading 0.17% higher against the USD from yesterday's close.

Data released overnight showed that Australia's consumer inflation expectation rose to 4.3% in October, following a reading of 3.8% in the previous month. Moreover, the nation's seasonally adjusted home loan approvals climbed 1.0% on a monthly basis in August, topping market expectations for an advance of 0.5%. In the previous month, home loan approvals had gained by a revised 2.8%.

The pair is expected to find support at 0.7782, and a fall through could take it to the next support level of 0.7756. The pair is expected to find its first resistance at 0.7824, and a rise through could take it to the next resistance level of 0.7840.

Looking forward, the Reserve Bank of Australia's Financial Stability Review report, due to release overnight, will garner significant market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

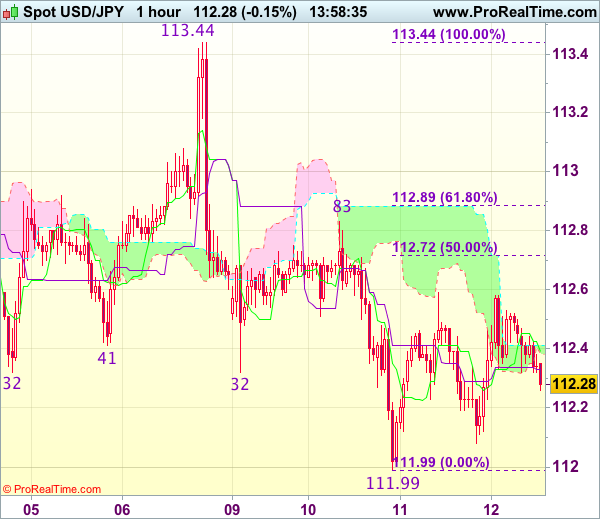

Trade Idea : USD/JPY – Sell at 112.80

USD/JPY - 112.28

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.39

Kijun-Sen level : 112.33

Ichimoku cloud top : 112.41

Ichimoku cloud bottom : 112.39

Original strategy :

Sell at 112.80, Target: 111.80, Stop: 113.15

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.80, Target: 111.80, Stop: 113.15

Position : -

Target : -

Stop : -

Although dollar has retreated after faltering below resistance at 112.59, as long as this week’s low at 111.99 holds, risk of another rebound to 112.70-75 (50% Fibonacci retracement of 113.44-111.99) cannot be ruled out, however, reckon 112.83-89 (yesterday’s high and 61.8% Fibonacci retracement) would limit upside and bring another decline later, below said support at 111.99 would add credence to our view that top has been formed at 113.44 and extend weakness to 111.75-80, then towards 111.47 support but oversold condition would limit downside and reckon 111.11 support would remain intact.

In view of this, we are looking to sell dollar on recovery as 112.83 resistance should limit upside and bring another decline. A break of indicated level at 112.83-89 would abort and signal low is formed, bring a stronger rebound to 113.10-20 but price should falter well below said last week’s high at 113.44.

Euro Trading On A Stronger Footing, Ahead Of The ECB President’s Speech

For the 24 hours to 23:00 GMT, the EUR rose 0.45% against the USD and closed at 1.1862.

The US Dollar traded in the negative territory against its major counterparts, after minutes of the September FOMC meeting revealed lingering concerns about persistently low inflation.

Minutes indicated that policymakers are tilting towards the prospects for another interest rate hike before this year-end. However, officials issued concerns that low inflation could not only be a temporary phenomenon and as such few believed that “some patience” was warranted in hiking interest rates in order to assess trends in inflation.

On the data front, the US JOLTS job openings dropped to a level of 6082.0K in August, higher than market expectations for a fall to a level of 6125.0K. JOLTS job openings had registered a revised reading of 6140.0K in the prior month. Moreover, the nation's MBA mortgage applications eased 2.1% in the week ended 06 October. In the previous week, mortgage applications had fallen 0.4%.

In the Asian session, at GMT0300, the pair is trading at 1.1873, with the EUR trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1820, and a fall through could take it to the next support level of 1.1767. The pair is expected to find its first resistance at 1.1901, and a rise through could take it to the next resistance level of 1.1929.

Moving ahead, investors will keep a close watch on a speech by the European Central Bank (ECB) President, Mario Draghi, due later today. Traders would also eye the Euro-zone's industrial production data for August, slated to release in a few hours. Moreover, the US initial jobless claims and the monthly budget statement for September, both slated to release later in the day, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.2% against the USD and closed at 1.3229.

Meanwhile, UK’s Chancellor of the Exchequer, Philip Hammond, stated that Brexit has clouded Britain’s economic outlook and added that the Government is preparing for the potential of a “hard Brexit” in 2019.

In the Asian session, at GMT0300, the pair is trading at 1.3252, with the GBP trading 0.17% higher against the USD from yesterday’s close.

Overnight data indicated that Britain’s RICS house price balance remained unchanged at a level of 6.0 in September, compared to market expectations of a drop to a level of 4.0.

The pair is expected to find support at 1.3197, and a fall through could take it to the next support level of 1.3142. The pair is expected to find its first resistance at 1.3286, and a rise through could take it to the next resistance level of 1.3320.

Going ahead, traders will look forward to the Bank of England’s credit conditions survey report, due to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Tertiary Industry Index Unexpectedly Declined In August

For the 24 hours to 23:00 GMT, the USD rose 0.1% against the JPY and closed at 112.49.

In economic news, Japan's preliminary machine tool orders recorded a rise of 45.3% YoY in September. In the previous month, machine tool orders had risen 36.2%.

In the Asian session, at GMT0300, the pair is trading at 112.42, with the USD trading 0.06% lower against the JPY from yesterday's close.

Early morning data indicated that Japan's tertiary industry index unexpectedly fell 0.2% in August, compared to a rise of 0.1% in the previous month and defying market consensus for an advance of 0.1%.

The pair is expected to find support at 112.14, and a fall through could take it to the next support level of 111.85. The pair is expected to find its first resistance at 112.65, and a rise through could take it to the next resistance level of 112.87.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Swiss Franc Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.14% against the CHF and closed at 0.9735.

In the Asian session, at GMT0300, the pair is trading at 0.9722, with the USD trading 0.13% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9704, and a fall through could take it to the next support level of 0.9685. The pair is expected to find its first resistance at 0.9754, and a rise through could take it to the next resistance level of 0.9785.

With no macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic news.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.