Sample Category Title

Eye Watering ISM’s

Eye Watering ISM's

ISM services sectors report cropped the dollar losses after policy uncertainly overflowed after the Fed chair contenders were finalised. Purportedly the fantastic four include Yellen, Cohn, Powell and Warsh.But I suspect the inclusion of Yellen was viewed dovish, but frankly, most knew this was the case, and the minor dollar sell-off in yesterdays Aisa session was little more than a storm in a teacup

Last nights eye-watering ISM non -manufacturing index was the talk of the town. After a stellar ISM manufacturing print on Monday, the non-manufacturing release overnight was purely astounding bolstering the view for a December US interest rate hike.

However, the currency markets appear to lack confidence or conviction even with the astonishingly bullish ISM prints, and the buoyant ADP data to boot. Dealers look happy to play ” home on the range ” while questioning the possible data misrepresentation due to the hurricane effect

There were few if any developments on the next chair front despite some outlandish rumours that put Kashkari on the seat as the Federal Reserve Board plays out its version of the Game of Thrones.

The rest of the session was spent digesting more bluster, hullabaloo and even fake news after a report surfaced that Secretary of State Tillerson was on the verge of resigning. But the reality is the market is on razor's edge when it comes to Washington machinations so much so that the that the Secretary of State held an unplanned press conference to quash the rumours

The Non-Farm payrolls are the next focal points.Tail risk is from a stronger print as dealers will most certainly discount any weakness due to the hurricane effect distortions.

The Balance of Risks

Euro

Catalonia referendum fallout has tempered the Euro bulls, but the market is content to sit tight and wait for the October ECB for the next trigger. While today's minutes are unlikely to shed much light on the balance sheet front, the market's focus will be squarely on any possible pushback from the ECB on EUR appreciation.

Japanese Yen

Continue to expect volatility with more polls released as we close in on the OCt 22 election date. But with the market on a hawkish Fed lean. ( Most betting Warsh) long USDJPY continues to be the favoured trade despite current ranges likely to persist up to election day.

The Australian Dolar

With the RBA triggered weakness all but retracted, the Aussie becomes little more than a passenger as the border USD movements remain in the driver's seat. However, it is becoming somewhat apparent that the Aussie is one of the currencies with the most to lose on the stronger USD narrative.

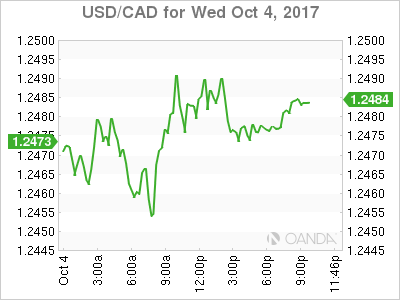

USD/CAD Canadian Dollar Rises On Oil Surge

The Canadian dollar appreciated versus the US dollar on Wednesday. Economic indicators were scarce in Canada, with the spotlight firmly on the start of the jobs reports to be delivered this week. The private payrolls processor ADP showed a gain of 135,000 jobs in September. It was inline with expectations, although there was a slight downward revision to August of 9,000 positions. The non-manufacturing PMI followed in the path of the manufacturing sector with a overachieving 59.8 index when only 55.5 was expected. The ISM reported a 93rd consecutive gain and the highest since August 2005. Inflationary pressures are present with a rising price index that grew 8.4 percent points since August.

The USD was not able to take advantage of solid economic releases as the political strife that has plagued the current administration once again was present. Uncertainty about the next Fed chair is keeping market watchers from predicting what a new look Fed could be in 2018. The short list includes Gary Cohn, Kevin Warsh, Jerome Powell, John Taylor and surprisingly Janet Yellen is still in the running.

The media has paid too much emphasis on the disorganization of the Trump administration where even Rex Tillerson has to go on the record that he did belittle the president and was never intending to quit his post as Secretary of State. The political cloud is keeping the USD lower even as other parts of the world do not have the same growth prospects, but they do have a more stable leadership.

The USD/CAD lost 0.192 percent on Wednesday. The currency is trading at 1.2482 with the loonie regaining some ground after the USD got a temporary boost from purchasing managers in the service sector. US yields are higher as there is still no front runner for the Fed Chair job. The rumour mill and off the cuff comments have made anyone and everyone a candidate. Yellen is still in the running and did not comment on monetary policy today in St. Louis. The Trump’s administration short list does not take anybody off the running, but the fact that known doves are on it has not done the greenback any favours.

The Canadian trade deficit is expected to keep shrinking as the rise of the CAD has cut down import prices. The Trade balance for August will be released on Thursday, October 5 at 8:30 am EDT. Last month the deficit shrank to $3 billion and is forecasted to come in at 2.6 billion. In a day with few economic data releases the Canadian trade balance will impact the USD/CAD but could end up being eclipsed by FOMC member comments. In particular those that are on the short list for the Chair position like Jerome Powell.

The US trade balance will also be released on Thursday, and with the emphasis on trade imbalances by the Trump administration it will be a talking point during NAFTA renegotiations. The US deficit is expected to have shrunk as the effects of Hurricane Harvey would affect the trade during August.

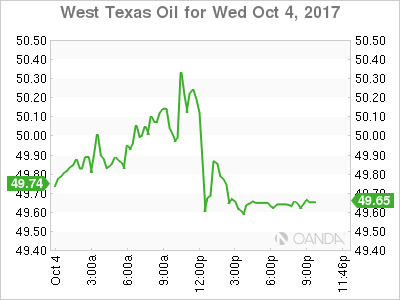

Energy prices rose 0.329 percent in the last 24 hours. The price of West Texas Intermediate is trading $50.32 after the US weekly crude inventories showed a larger than expected drawdown of 6 million barrels. Forecasters were calling for a drop of 500,000. Crude prices rose after the news, but had to setlle for lower gains after Libya has restarted its largest field that was taken offline over the weekend by rebel forces.

Russian Energy Minister in Moscow was supportive of an extension from Organization of the Petroleum Exporting Countries (OPEC) and other major producers to keep cutting production, but the final decision will depend on the market. Russian President Vladimir Putin was also part of the Russian Energy Week Forum and said that the deal could be extended to 2018.

Market events to watch this week:

Thursday, October 5

8:30 am CAD Trade Balance

8:30 am USD Unemployment Claims

Friday, October 6

8:30 am CAD Employment Change

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

What’s The USD Upside?

Another sizzling US economic data point was brushed aside because of storm-related effects but we evaluate how high the dollar could rise if the economy really is heating up. AUD was the top performer while CHF lagged. Aussie retail sales and trade balance are due up next. The latest Premium members video below charts how far and how long will the USD correction be. It also highlights the Premium trade issued today.

US ISM non-manufacturing survey hit a 12-year high on Wednesday. It was at 59.8 compared to 55.5 expected and 55.3 prior. It was coupled with a jump in the prices paid component. The dollar climbed at first but the survey chairman downplayed the strength, saying respondents were expecting work due to the storms. In addition, the rise in the prices paid component was driven by the climb in fuel prices around the time of the storm.

It was a similar story a day earlier when US auto sales climbed by the most since 2005. The US dollar hardly made any headway on two of the best headlines in months. Part of the reason might be that ADP employment fell to 135K from 228K in August but that was bang-on expectations.

Chances are, the market is right. That the hurricanes will skew economic data but that the trend hasn't changed. Still, the alternative is worth considering. What if the economy has turned a corner, wages are starting to pick up and a big tax cut is coming?

The USD upside would be substantial, especially against the yen because Japanese rates are pinned to the floor. Part of the reason for the dollar sluggishness has to be the Fed and the expectation that Trump will appoint a dove. If that's unfounded then there is a real possibility of three or more rate hikes in the year ahead. If so, USD/JPY could easily rally 10 cents from here and perhaps much more.

The odds of a tax cut are tough to evaluate but Warren Buffett said Tuesday he thinks it's higher than most believe. What if it comes at the same time as the economy is already heating up?

That will be a question to consider in the weeks ahead but in the hours ahead, the focus will be on the Australian dollar. It bounced Wednesday after two weeks of struggles but the next chapter will be written by data. The August trade balance and retail sales reports are due at 0030 GMT. The consensus is for a surplus of $850m and sales up 0.3%.

Euro Correction Deepens as Political Risks Resurface

The euro has stumbled upon some unexpected headwinds during the past month, taking some of the heat off the currency's incredible rally this year. Soon after peaking at a 32-month high of $1.2092 on September 8, the euro entered a corrective phase, triggered by a more cautious-than-anticipated European Central Bank at its policy meeting on September 7.

Expectations that the ECB would begin the process of winding down its massive stimulus program, receding political uncertainty after the French elections, as well as the unravelling of the Trumpflation trade have been the main drivers of the euro rally. However, while signalling that policy tightening is forthcoming, the ECB has avoided referring to the tapering discussions as an exit strategy, preferring instead to use words such as "calibration" or "adjustment" of policy. The central bank has also been more careful with its communication, with Governing Council members all signalling a very gradual withdrawal of monetary stimulus in the coming months in a series of public appearances in recent weeks.

Slow progress in achieving a sustained pick-up in underlying inflation in the Eurozone is the main reason why the ECB is dubious about making a hasty exit from its ultra-loose monetary policy program. However, concerns about the euro rising too fast and by too much has also been weighing on policymakers' minds. Although President Mario Draghi has so far refrained from verbal intervention in talking down the euro, he has expressed concerns about the possible impact of an appreciating exchange rate on growth and inflation. Discomfort about the rising euro is even stronger among the heads of the Eurozone's periphery central banks.

All of this has led to many analysts readjusting their outlook about ECB policy, with some now predicting the ECB tapering story to become a topic for late 2018 rather than 2017. The euro has retreated by around 3% from its September peak as investors reassess their positions on the single currency. But monetary policy has not been the only factor in inducing the euro's corrective move lower.

Renewed risks of political instability have remerged to cast doubt about the decline of populist movements across the Eurozone. The inconclusive election outcome in Germany on September 24, which resulted in Chancellor Angela Merkel having to seek coalition partners with smaller parties in potentially protracted negotiations, and this Sunday's independence vote in the Spanish region of Catalonia, which was declared "unconstitutional" by Spain's government, have reignited fears of fresh political turmoil in the region.

While Merkel will likely succeed in forming a new coalition, it could make it more difficult for her to join France's President Emmanuelle Macron in pushing for further EU integration, as one of the prospective coalition partners, the FDP party, is sceptical about closer EU ties. It's worth noting that markets were pleased with Macron's win in the French presidential elections in April not only for reducing the political uncertainty but also about the hopes of greater Eurozone integration. Another question that needs to be asked after the elections is how the far right AfD party will shape German politics after winning seats in parliament for the first time.

In Spain, the yes vote in Sunday's independence referendum could fuel the rise of other separatist movements in Europe, especially in Italy, which is required to hold a general election before May 20, 2018. Italy is seen by many investors as the most vulnerable to a debt crisis. It is also the most at risk of leaving the common currency bloc or even the European Union given the rise of populist parties such as the Five Star Movement, and the separatist Northern League party, who want more autonomy for the northern regions of Italy.

Following these developments, the euro is now in danger of reversing to a downtrend after forming a double top. A key support lies in the $1.1650-1.660 area. A breach of this support level could signal a more bearish outlook in the medium term. The longer-term picture, however, remains very much bullish.

With the ECB expected to eventually pull the plug on its stimulus program, the prospect of a continuation of the current uptrend in euro/dollar is strong. However, the speed and the extent of the uptrend will depend on the ECB's tolerance level of euro appreciation and developments in the United States.

A rapid rise towards and past the possible ECB pain threshold of $1.25 level could prompt much stronger verbal warnings by policymakers against further appreciation of the currency. Fears by some traders that this threshold is closer to $1.20 contributed to the euro's pull back from its September high. In addition, further sharp gains could slow the tightening cycle, which the central bank is expected to embark on at its next meeting on October 26.

Meanwhile, progress on the tax reform front in the US, which appears to be gathering more support lately, could revive the Trump-led rally for the US dollar and heighten expectations of further rate hikes by the Federal Reserve. Also potentially fuelling rate rise expectations is the choice of a hawkish nominee to be the next head of the Fed. President Trump is expected to decide in the next few weeks who will replace Fed Chair Janet Yellen when her term expires in February 2018. As Yellen is seen to be a dovish chair, the appointment of a more hawkish candidate could further slow the euro's ascent over the coming months.

Traders Anticipate Central Bankers Speeches Today

Volatility in the currency markets fell today as traders await the all-important labour market report from the US on Friday and the speeches of ECB President Mario Draghi at 17:15 and the Fed Chair Janet Yellen at 19:15 GMT. Rhetoric by the central bankers may result in a sharp rise in volatility. The greenback weakened somewhat today around speculations about possible changes of the Fed Governor to an individual with dovish views on monetary policy settings. This scenario may lead to a further depreciation of the US dollar against other major currencies.

The euro today was negatively affected by news of the decline in the common region's retail sales by 0.5% in August compared to an anticipated increase of 0.3%. A small bright note came from the final services PMI report which grew in the Eurozone to 55.8 against the 55.6 forecasted.

GBP/USD bulls received some good news with the services PMI in the UK growing 53.6 which is 0.4 above the average expectations. Current price consolidation is explained by the influence of controversial factors. On the one hand, the chance of monetary tightening in the UK increased lately, while on the other hand the fears of a negative outcome to the Brexit talks are restraining the bulls from buying up the pound.

Expect to see increased trader activity for the AUD/USD following the release of retail sales and trade balance in Australia at 00:30 GMT tomorrow. These indicators traditionally have a strong influence on the mood of investors.

EUR/USD

The EUR/USD has left the limits of the local descending channel and keeps consolidating above the 1.1750 mark. Fixing the price beyond the limits of the channel may be a stimulus for continued increases up to 1.1825 and 1.1925. In case of a fall resuming, the nearest targets will be at 1.1620 and 1.1550.

GBP/USD

The British pound keeps consolidating near the important 1.3250 mark. A low amplitude of price fluctuations points to the possibility of a sharp movement soon. The signal to buy may come from gaining a foothold above the upper limit of the descending channel, but a more likely scenario may be the continued descending movement within the limits of the channel, with the closest targets at 1.3150 and 1.3050.

AUD/USD

Bulls were able to pull the AUD/USD price to the upper limit of the descending channel and the resistance at 0.7870. Breaking through these levels may become a strong trigger for massive buying with potential targets at 0.8000 and 0.8030. In case of crossing the SMA100 on the 15-minute chart, we may see a fall resume with the immediate goal at 0.7800 after which the quotes my reach 0.7740 and 0.7700.

Dollar Shines on ISM Non-Manufacturing PMI Numbers; Oil Up after Putin’s Remarks and EIA Report

Not long before the session-end, the dollar index shot higher against its peers, reversing daily losses after the ISM non-manufacturing PMI readings for the month of September posted the highest mark since August 2015. The index surged by 4.5 points to 59.8, whilst projections were for a smaller increase to 55.5. New orders, employment and price PMI indices within the services industry also touched fresh highs, with prices surging the most in five years. The Markit equivalent also came in better than expected, with the composite PMI arriving at a two-year high of 51.1.

Earlier, the ADP national employment report indicated that 135,000 private jobs were added to the economy in September, surpassing the forecast of 125,000 but falling below August's downwardly revised mark of 228,000. This comes ahead of the nonfarm payrolls reading to be released on Friday.

Even though news of a less hawkish Fed chair candidate (specifically, Jerome Powell) being preferred by the US Treasury Secretary Steven Mnuchin made traders scratch their heads and pressured the dollar index near the 93-key level, the release of upbeat non-manufacturing PMI numbers lifted the index back to 93.51. Dollar/yen jumped to an intra-day high of 112.89 before falling to 112.71. Gold fell from a five-day high of $1,281.45 per ounce to $1,270.49, being 0.20% up on the day.

Later in the day, investors will eye a speech given by the Fed chairwoman, Janet Yellen, at the Community Banking in the 21st Century Conference in St. Louis.

The pound gained some ground against the dollar, picking up to an intra-day high of $1.3287 following the release of better-than-expected Markit services PMI numbers for the month of September. The sector's index edged up to 53.6, while forecasts were for the index to remain steady at August's level of 53.2.

Final Markit services PMI readings out of the Eurozone also surprised analysts to the upside, rising by 1.1 points to a four-month high of 55.8 in September compared to the expected 55.6. The region's composite PMI figure also climbed to a four-month high, gaining 1 point and rising to 56.7 as expected. However, a few hours later, August's retail sales out of the region disappointed analysts after the numbers showed that yearly retail sales fell from the downwardly revised 2.3% to 1.2% instead of growing by 2.6%. This was also the lowest growth seen since February.

Meanwhile, in Catalonia, a government official said that regional parties who are in favor of independence and hold most seats in the Catalan parliament have asked for a debate and a vote on breaking away from Spain on Monday.

Euro/dollar gave up gains in the wake of the US PMI data, falling to 1.1760. Nevertheless, it remained 0.14% up on the day. Euro/pound dropped by 0.16% to 0.8858.

In Moscow, an energy forum attended by several OPEC energy ministers and the Russian President, Vladimir Putin, boosted confidence on longer oil supply cuts after Putin said that the OPEC/non-OPEC deal on production cuts could be extended "at least until the end of 2018".

The Energy Information Administration's report on US crude oil inventories showed stockpiles falling by 6.02 million barrels in the week ending September 29, a much bigger drawdown than the expected 0.76m and the preceding week's reduction by 1.85m barrels. Gasoline inventories over the same period grew faster than expected though, rising by 1.64m barrels as opposed to the anticipated 1.09m. WTI jumped higher within the first few minutes of data release with Brent crude also recording gains. The former last traded 0.3% up on the day, at $50.57 per barrel. Brent was 0.1% higher at $56.04 a barrel.

Dollar/loonie rebounded during the session, rising from a five-day low of 1.2449 to 1.2479 after the EIA report.

US Non-Manufacturing Sector Expanding Rapidly in September

The Institute for Supply Management's (ISM) non-manufacturing index surged by 4.5 points to 59.8 in September - the highest reading since August 2005. The headline print surprised to the upside, with market expectations set on a slight uptick to 55.5.

September marked the second consecutive month of broad-based gains among the sub-indices, with pullbacks recorded only in inventories and inventory sentiment.

Notable gains were recorded in business activity (+3.8 to 61.3), new orders (+5.9 to 63) and prices paid (+8.4 to 66.3), with the latter indicating that prices increased for the fourth consecutive month to the highest level in more than five years.

The acceleration in activity and demand slowed supplier deliveries in September with the sub-index increasing by 7.5 to 58 (a reading above 50 indicates slower deliveries). Comments from industry contacts pointed to weather conditions and the inability of suppliers to respond to increased demand as reasons for the slowdown.

Comments from survey contacts remained largely positive and nearly all industries reported growth on the month, with Arts, Entertainment & Recreation, and Mining being the only exceptions.

Key Implications

The ISM non-manufacturing index surprised significantly to the upside in September, in line with its manufacturing cousin. Just as in the case of the manufacturing index, some of the September gains appear to be driven by supply chain disruptions and rebuilding efforts in the aftermath of Hurricane Harvey and Irma.

Improvements in the employment and prices paid sub-indices are very encouraging. The former, taken together with an uptick in its manufacturing equivalent, point to some upside risk regarding expectations for a subdued payrolls report this Friday - given the likely Irma impacts. Meanwhile, the surge in the prices paid sub-index, while likely temporarily boosted by hurricane disruptions, nonetheless provides some comfort with regards to the inflation outlook.

While this is definitely a solid report, we are reluctant to put too much emphasis on the surprisingly upbeat headline print given the transitory forces at play. But, while the current headline may be overstated in light of the disruptions, we believe that underlying momentum remains solid given the details of the report and breadth of improvement.

Dollar Going Nowhere on Conflicting Stories

- European stock markets lost up to 0.5% with Spain underperforming (-2%) as sources indicated that Catalonia will declare independence on Monday. US stock markets opened with minor losses.

- The pace of hiring in the US private sector slowed to its weakest pace in 13 months last month, as Hurricane Irma and Harvey disrupted businesses across a large swath of the south-eastern US. Non-farm private employers added 135,000 jobs from August to September, according to a report from payroll processor ADP.

- America's service industries expanded in September at the fastest clip in 12 years (from 55.3 to 59.8), signalling vibrancy across the bulk of the economy following two major hurricanes, a survey from the ISM showed.

- Catalonia will move on Monday to declare independence from Spain, a regional government source said, as the EU nation nears a rupture that threatens the foundations of its young democracy and has unnerved financial markets.

- Firms in the UK's important services sector reported better than expected growth in September (53.6 from 53.2) in the closely-watched PMI survey, but warned of potential difficulties ahead as new business growth fell to its lowest level in more than a year. The final EMU services PMI was upwardly revised from 55.6 to 55.8.

- President Donald Trump's tax plan would let US companies take bigger, faster deductions on capital investments, a step some experts said would deplete Washington's policy arsenal by using up a tax break normally reserved for fighting recessions.

- President Vladimir Putin said Russia may agree to extend a deal with OPEC to curb oil supplies beyond March to the end of 2018, though he'll wait to make a decision until nearer the end of the existing pact.

- The ECB's supervisors want lenders to be fully covered against losses from new loans that have gone sour, in a move that could hurt credit creation in weaker economies in the region.

- The National Bank of Poland kept its policy rate unchanged at 1.5%. NBP governor Glapinski holds a press conference later today.

- A month before a snap parliamentary election, Iceland's central bank cut its key interest for the fifth time in little more than a year, from 4.5% to 4.25%, in a move to offset the impact of lower inflation. The Reserve Bank of India kept its policy rates unchanged at 6%.

Rates

Volatile session, but limited changes after all

Core bonds had a constructive session helped by a volatile mild risk off sentiment and technical factors. The Bund outperformed US Treasuries, but this time in a sphere of (modestly) falling yields. The tide turned in the afternoon session on the core bond markets and gains melted partly away.

The Bund started strong on Spanish developments. The German Dax opened at an all-time high in a catch-up move (German markets closed for Day of the Unity yesterday), but couldn't sustain at these levels with other European indices losing ground (Spain underperforming). However, by the time of writing our report, the Dax is again upwardly oriented. The Bund managed to eke out additional gains because of technical reasons. The German 10-yr yield tried already a few days to break through 0.5% resistance, but didn't succeed, encouraging some bulls to take profit on shorts/open long positions. However in lockstep with rising equities, the Bund lost again some ground in the afternoon session. The EMU final PMI stayed nearly unrevised and EMU retail sales were weaker, but markets ignored the eco data, just like the US ADP employment report that was bang in line with (modest) expectations.

On intra-EMU bond markets, 10-yr yield spread changes versus Germany ranged between +9 bps (Spain) and +4 bps (Italy and Portugal). The stand-off between the central government and the Catalonian authorities became grim again. The Spanish King condemned in harsh words the illegal referendum . The Catalonian leaders rebuked the King for not mentioning the violent policy action against peaceful voters and insisted they would call independence of the region soon. Investors are noticing now the situation and become worried. The spread increased 20 bps since the referendum and the Madrid bourse lost ground too.

US president Trump suggested that Puerto Rico's staggering $74B debt will be wiped out (default) to help the island recover from the effects of the hurricane Maria, estimated at $95B of damages. This might have serious implications for the big municipal market and could help safe-haven US Treasuries. However, once more there was no firm evidence that it effectively played a role. Fed Fischer, who leaves office later this month, continues to expect a tightening US labour market to lift wages and prices even though the process can take longer than anticipated. He is yesterdays' man for markets and thus unimportant. Gold and the yen rose in the morning session, but lost (part) of the gains in the afternoon, confirming that volatile risk sentiment was behind market movements.

The German Finanzagentur tapped the on the run 10-yr Bund (€3B 0.5% Aug2027). Total bids amounted €3.75B, slightly below the €4.07B average at the previous 4 Bund auctions. The Bundesbank set aside €0.59B for secondary market operations, resulting in an official bid cover of 1.6. The auction had no tail.

Currencies

Dollar going nowhere on conflicting stories

Today, USD traders faced several conflicting issues including strong EMU eco data, uncertainty on Catalonia and the US debate on who will succeed Yellen at the helm of the Fed. EUR/USD and USD/JPY hovered up and down. In the end, the trade-weighted dollar is little changed from the start in Europe. EUR/USD is changing hands in the 1.1770 area. USD/JPY tries to hold 112.50 area.

Overnight, Asian equities ex-Australia continued their uptrend. The Japan services PMI indicated modest growth, but didn't hurt the yen. The dollar declined slightly further as the political debate on a successor for Fed's Yellen intensified. There were rumours that chances of Fed member Powell, also on the shortlist, were growing. USD/JPY dropped to the mid 112 area. In the same vein, EUR/USD settled again in the upper half of the 1.17 big figure.

European FX traders faced a complex environment. The EMU PMI's were strong but rising tensions on Catalonia were a negative for euro sentiment. The rebound of European equities stalled and German bunds outperformed US Treasuries, widening the interest rate differential in favour of the dollar. However, it didn't help the US currency. EUR/USD gradually reversed an early dip and returned to the 1.1770/80 area. USD/JPY traded with a negative bias as core bond yields declined and as risk sentiment turned cautiously negative. Uncertainty on the successor of Fed Chair Yellen kept USD bulls side-lined. USD/JPY drifted (temporary?) below 112.50.

In the US, the ADP labour report showed a modest net growth of 135 000 private jobs in September, in line with consensus. ADP said the dip in job growth was in part due to the impact from the hurricanes. There was no dollar reaction, but the dollar tried to bottom going into the start of US equity trading. Maybe uncertainty on the financial position of Puerto Rico was also a slightly dollar negative. EUR/USD trades currently in the 1.1770 area. USD/JPY trades near 112.50 awaiting the US non-manufacturing ISM.

Sterling decline blocked by decent services PMI

Sterling hovered near the recent lows against the euro early today. EUR/GBP held a tight range in the 0.8875 area. Cable tried to move a bit further away from yesterday's correction low (1.3222) but this was due to dollar softness. On Monday and Tuesday , the manufacturing and the services PMI's were reported weaker than expected and weighted on the UK currency. Today, the services PMI rebounded from 53.2 to 53.6, while a stabilization was expected. The details from the report were not strong, but upward prices pressures persist. The report fits a scenario of a limited BOE tightening in the near future. However, the BOE will act very cautiously. Sterling rebounded, but the move was limited given the recent correction. EUR/GBP trades in the 0.8865 area. Cable hovers around 1.3275. The text of May's speech at the conservative party conference was released just before noon. The PM said she is seeking a Brexit deal that works, but the government is also preparing for a no-deal scenario. The impact on markets was very limited.

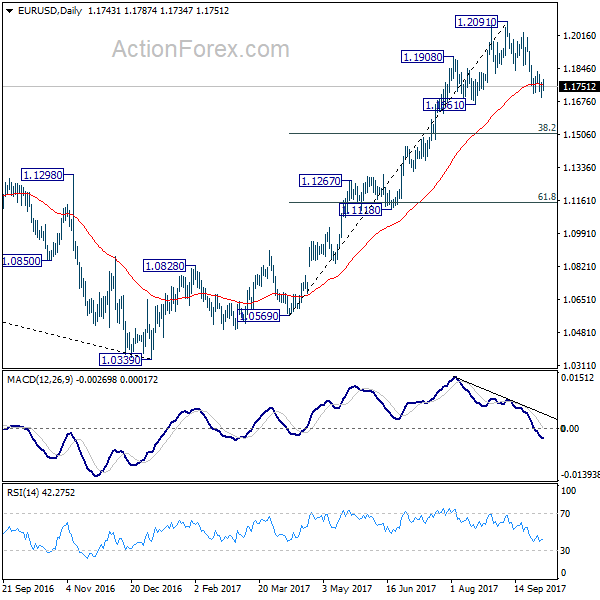

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1702; (P) 1.1738 (R1) 1.1780; More...

Since 1.1832 minor resistance remains intact, deeper decline is in favor in EUR/USD. Fall from 1.2091 would extend through 1.1661 support. Decline from 1.2091 is correcting whole rise from 1.0569. Deeper fall should be seen to 38.2% retracement of 1.0569 to 1.2091 at 1.1510, where we're expecting support to bring rebound. On the upside, break of 1.1832 minor resistance will suggest that the corrective fall is completed and turn bias back to the upside.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

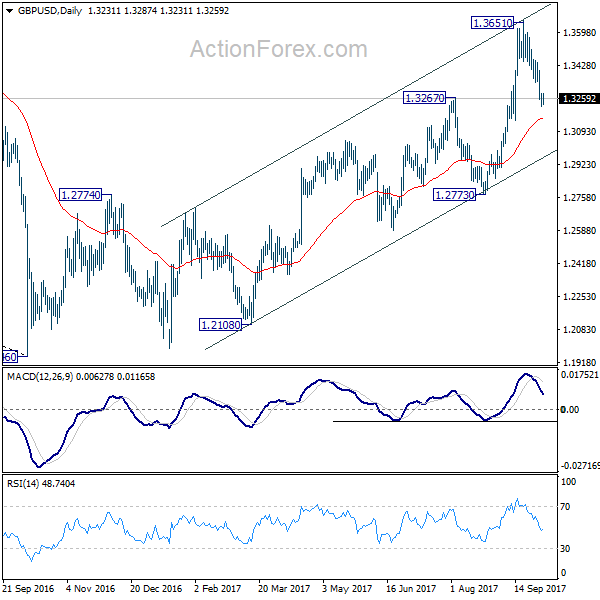

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3212; (P) 1.3249; (R1) 1.3277; More....

At this point, GBP/USD's corrective fall from 1.3651 could still extend to 61.8% retracement of 1.2773 to 1.3651 at 1.3108 and below. However, break of 1.3454 will indicate completion of the pull back. In that case, intraday bias will be turned back to the upside for retesting 1.3651 high.

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.