Sample Category Title

Market Update – European Session: European Service PMIs Mixed But Remain In Expansion

Notes/Observations

Euro Area Service PMI data mixed in session (Beats: Euro Zone, UK, Spain; Misses:France, Italy, Russia; in-line: Germany )

Overnight

Asia:

BOJ Dep Gov Nakaso said not to rule out BoJ deficit in exit strategy. Revenue fluctuations in the short-term from exit strategy would not hurt policy execution as BoJ had been saving some of its revenues for future losses.

Japan Sept PMI Services: 51.0 v 51.6 prior (11-month low)

The World Bank raised China’s 2017 and 2018 GDP growth forecasts, putting them in line with those of the IMF

Europe:

UK Trade Min Fox: have reached agreement with EU on the methodology of WTO quotas

PM May reiterated seeks a deal on Northern Ireland power sharing agreement; UK will do everything it can to get to a deal. UK PM May said to plan to tell her Tory party to “shape up and go forward together” in her closing speech at today’s annual party conference

UK Foreign Min Johnson: things are going well in the EU Brexit negotiations, but it's amid too much gloom. Expected to complete many free trade deals before the next election

UK Sept BRC Shop Price Index Y/Y: -0.1% v -0.3% prior (smallest decline since May 2013)

Catalan govt President Puigdemont confirmed planning to declare independence within day

Spain King Felipe VI: Spanish democracy is in a serious moment; referendum plans by Catalan leaders were illegal. Committed to Spanish unity; Spanish crown firmly committed to constitutional order

Americas:

President Trump aides said to deliver shortlist for Fed Chair, Treasury Sec Mnuchin is said to have given support to Jerome Powell for the position. President could bring in a wild-card candidate, but some said this is not likely (**Note: 4 candidates for the Fed chair position that President Trump interviewed including Yellen, Gary Cohn, Jerome Powell and Kevin Warsh)

House GOP tax plan reportedly likely to include fourth tax bracket on high earners; not likely to exceed 39.6%

Bank of Canada (BOC) Leduc: Need to promote economic stability by aiming for 2% CPI target (did not comment directly on BOC interest rates)

Energy:

Weekly API Oil Inventories: Crude: -4.1M v -0.8M prior

Economic data

(IE) Ireland Sept Services PMI: 58.7 v 58.4 prior; Composite PMI: No est v 58.2 prior

(RU) Russia Sept PMI Services: 55.2 v 54.6e (20th month of expansion); Composite PMI: 54.8 v 54.2 prior

(SE) Sweden Sept PMI Services: 68.3 v 55.4 prior

(ES) Spain Sept Services PMI: 56.7 v 55.5e 47th month of expansion and highest since Aug 2015); Composite PMI: # v 55.1e

(ZA) South Africa Sept PMI (Whole Economy): 48.5 v 49.8 prior (2nd straight contraction)

(IT) Italy Sept Services PMI: 53.2 v 55.0e (16th month of expansion) ; Composite PMI: 54.3 v 55.9e

(FR) France Sept Final Services PMI: 57.0 v 57.1e (confirmed 15th month of expansion); Composite PMI: 57.1 v 57.2e

(DE) Germany Sept Final Services PMI: 55.6 v 55.6e (confirmed 51st month of expansion); Composite PMI: # v 57.8e

(EU) Euro Zone Sept Final Services PMI: 55.8 v 55.6e (confirmed 51st month of expansion);; Composite PMI: 56.7 v 56.7e

(BR) Brazil Sept FIPE CPI (Sao Paulo) M/M: 0.0% v 0.0%e

(UK) Sept Services PMI: 53.6 v 53.2e (14th month of expansion); Composite PMI: 54.1 v 53.8e

(IS) Iceland Central Bank (Sedabanki) cut its 7-Day Deposit Rate by 25bps to 4.25%

(IN) India Central Bank (RBI) left its Repurchase Rate at 6.00% (as expected)

(EU) Euro Zone Aug Retail Sales M/M: -0.5% v +0.3%e; Y/Y: 1.2% v 2.6%e

Fixed Income Issuance:

(IE) Ireland Debt Agency (NTMA) opened its book to sell Oct 2022 IGB bond; guidance seen -23bps to mid-swaps

(IN) India sold total INR140B vs. INBR140B indicated in 3-month, 6-month and 12-month Bills

(DK) Denmark sold total DKK2.12B in 2020 and 2027 DGB bonds

(SE) Sweden sold total SEK2.5B vs. SEK2.5B indicated in 2026 and 2032 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.4% at 3,581, FTSE flat at 7,423, DAX +0.2% at 12,909, CAC-40 -0.3% at 5,348, IBEX-35 -1.9% at 10,030, FTSE MIB -1.0% at 22,497, SMI -0.1% at 9,255, S&P 500 Futures flat]

Market Focal Points/Key Themes: European stocks opened mixed and slipped lower as trading progressed; Catalan independence worries keep markets depressed in the periphery; oil slipped adding additional pressure on energy stocks; safe havens supported; Israel closed for holiday; attention turning to new Fed Chair pick, with President Trump said to have received a shortlist of candidates; reminder that China and South Korea remain closed for holiday this week; upcoming earnings in US session include Pepsico and Monsanto

Equities

Consumer discretionary: Bang & Olufsen BO.DK +3.4% (results),Tesco TSCO.UK -1.9% (results), Eniro ENRO.SE +51.0% (recapitalization plan completion)

Consumer staples: Bakkafrost BAKKO.NO +2.5% (harvest update)

Energy: Scatec Solar SSO.NO +6.1% (JV with Statoil)

Financials: International Personal Finance IPF.UK -9.5% (comments on tax proposal in Poland)

Healthcare: Motif Bio MTFB.UK +30.6% (sudy results)

Industrials: Grupo Ezentis RDT.DE -12.8% (share issue), Pirelli PIRC.IT -0.9% (first day of trading), Royal Mail RMG.UK -2.7% (strike notice)

Technology: Worldline WLN.FR +2.9% (analyst action)

Telecom: Telefonica Deutschland O2D.DE -2.3% (analyst action)

Speakers

ECB proposed new guidance for banks’ bad-loan provisioning (NPL); as speculated. Starting Jan. 1, banks will have at most two years to set aside funds to cover 100 percent of the value of their newly classified non-performing unsecured debt and seven years to cover all secured bad debt

Euro Working Group (EWG) chief Wieser: Expect member States to order the completion of banking union

Iceland Central Bank policy statement noted that GDP growth to be weaker in 2017 due to easing in tourism

India Central Bank (RBI) policy statement noted that the vote was 5-1 to keep policy steady with memberDholakia votingd for at least 25bps cut. Saw inflation picking up from recent record lows and cuts its FY18 GVA from 7.3% to 6.7%. Forecasted H2 inflation between 4.2-4.6%

Saudi Arabia Central Bank Gov Alkholifey: FX Reserves are adequate

Russia Energy Min Novak: To keep 2017 oil exports flat y/y. Reiterated view that expected oil market to achieve balance in Apr 2018

Venezuela Oil Min Del Pino: There are talks whether to extend oil production cuts or even deepen them - comments from Russia oil forum

IEA raised its forecast for Renewable energy growth over the next 5 years. Expects global renewable electricity capacity to rise by more than 920 gigawatts, or 43 percent, by 2022, due to supportive policies for low-carbon energy and cost reductions for solar PV and wind

LIbya's Sharara oil field said to have reopened (was closed since late Sunday)

Currencies

The USD was slightly softer in a quiet session with some dealers noting of a report that President Trump aides delivered a shortlist for Fed Chair position (Treasury Sec Mnuchin is said to have given support to Jerome Powell for the position)

EUR/USD was higher by 0.2% and holding above 1.1750 area as various European Services PMI data came in mixed but holding onto expansion territory.

GBP/USD was aided by the UK Services PMI data which beat expectations. Pair trading around 1.3270 area.

Fixed Income

Bund futures trades at 161.36 up 24 ticks being aided by continued tensions in Spain, with a take out of 161.62 high targeting 161.98 followed by 162.23. A reversal continues to target 160.86 initially then 160.66.

Gilt futures

Wedneday's liquidity report showed Tuesday's excess liquidity rose to €1.778T from €1.767T prior, use of the marginal lending facility rose to €497M from €344M prior.

Corporate issuance saw $3.5B come to market via 2 issuers headlined by Enel Finance $3B 3 part offering, bringing weekly issuance to $6.65B.

Looking Ahead

(US) Senate Intelligence Committee update on Russia probe

05:30 (DE) Germany to sell €3.0B in 0.50% Aug 2027 Bund

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:00 (EU) EU Parliament votes on non-binding Brexit Resolution

06:00 (RU) Russia to sell combined OFZ bonds

06:30 (US) Fed's Fischer – media interview

07:00 (US) MBA Mortgage Applications w/e Sept 29th: No est v -0.5% prior

07:00 (FI) Finland Parliament on possible no-confidence vote

07:30 (TR) Turkey Sept Effective Exchange Rate(REER): No est v 89.71 prior

08:00 (HU) Hungary Central Bank (NBH) Sept Minutes

08:05 (UK) Baltic Dry Bulk Index

08:15 (US) Sept ADP Employment Change: +138Ke v +237K prior

09:00 (EU) Weekly ECB Forex Reserves:

09:00 (MX) Mexico July Gross Fixed Investment: -1.4%e v -0.9% prior

09:00 (BR) Brazil Sept PMI Services: No est v 49.0 prior; Composite PMI: No est v 49.6 prior

09:45 (US) Sept Final Markit Services PMI: 55.1 v 55.1 prelim; Composite PMI: No est v 54.6 prelim

10:00 (US) Sept ISM Non-Manufacturing Composite: 55.5e v 55.3 prior

10:00 (PT) Portugal PM Costa in Parliament

10:00 (PL) Poland Central Bank Gov Glapinski to hold post rate decision press conference

10:30 (US) Weekly DOE Crude Oil Inventories

12:15 (EU) ECB chief Draghi in Frankfurt

15:00 (CO) Colombia Sept Total PPI M/M: No est v 0.6% prior

15:00 (ES) Spain region of Catalon President Puigdemont statement on referendum

15:15 (US) Fed Chair Yellen at community banking event

BITCOIN Riding Uptrend Channel

Bitcoin is still on a strong momentum. Strong support is given at 2975 (22/08/2017 low). Sell walls around $4000 have been broken. Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further increase.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Short-Term Bearish

EUR/CHF is back into bearish. Short-term downside pressures are increasing. Strong resistance is now at 1.1623 (22/09/2017 high). Expected to show further short-term weakness.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Monitoring Resistance Area

EUR/GBP is ready to bounce back lower.. As long as prices remain below the resistance at 0.8899 (19/09/2017 low), the short-term technical structure is biased to the downside. Hourly support is given at 0.8746 (27/09/2017).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

CRUDE OIL Declining Towards $50

Crude Oil is pushing lower towards $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show continued weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Lack Of Follow-Through

Silver has reversed and has broken uptrend channel by breaking support implied by its lower bound. Strong resistance is given at 18.65 (17/04/2017 high) while the metal has broken support found at 16.58 (15/08/2017 high) before bouncing back. Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

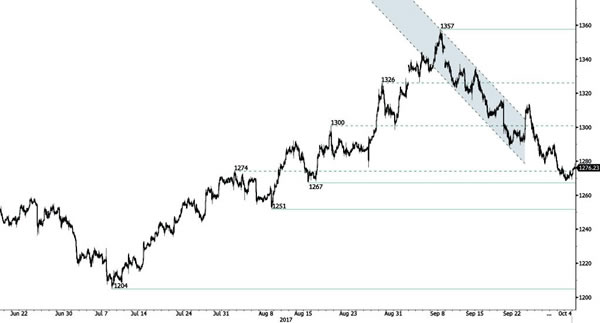

GOLD Selling Pressures Are Still Lively

Gold is ready to go lower. The precious metal has bounced back on hourly support given at 1267 (15/08/2017 low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further bearish move.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

AUD/USD Bouncing Back Above Support At 0.7786

AUD/USD is consolidating over the past weeks. Hourly resistance is given at 0.7883 (27/05/2017 high). The pair is approaching support at 0.7786 (18/07/2017 low). Expected to show continued consolidation.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Slight Consolidation Within Bullish Momentum

USD/CAD continues to move higher despite ongoing consolidation. Strong support is located at a distance 1.2062 (08/09/2017 low). Hourly support lies at 1.2331 (26/09/2017 high). Resistance is given at 1.2532 (29/09/2017 high). Expected to show continued short-term bullish pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Ready For Another Leg Higher

USD/CHF is trading higher within short-term uptrend channel. Yet, demand is has been increasing since September. Closest resistance is given at 0.9808 (30/05/2017 high). There are nonetheless decent downside risks. Strong support is given at 0.9421 (03/05/2017). Expected to show bullish pressures.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.