Sample Category Title

USD/JPY Entering A Consolidation Phase

USD/JPY is trading mixed. Strong support is located at a distance at 111.12 (20/09/2017 low). The pair is still located into a medium-term bullish trend. Yet, downside risks are rising as markets may soon take some short-term profit.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Riding Downtrend Channel

GBP/USD is pushing lower since the pair has topped 1.3657 (20/09/2017 high). The pair is going towards hourly support is given at 1.3155 (14/09/2017 low). Expected to show continued bearish pressures within downtrend channel.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Low Buying Demand

EUR/USD is way into a bearish trend. Hourly resistance can be found at 1.1833 (29/09/2017 high). Strong support is given at a distance at 1.1662 (17/08/2017 low). Expected to show continued short-term bearish pressures.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

CAC Lower Despite Strong French Services PMI

The CAC index has posted slight losses in the Wednesday session. Currently, the CAC is trading at 5,350.00, down 0.32% on the day. On the release front, services readings were positive. French Services PMI jumped to 57.0, just shy of the estimate of 57.0 points, and Eurozone Services PMI improved to 55.8, above the forecast of 55.6 points. However, Eurozone Retail Sales posted a second straight decline, coming in at -0.5%. This was well below the forecast of +0.3%. Later in the day, ECB head Mario Draghi will speak at an event in Frankfurt. On Thursday, the ECB releases the minutes of its September policy meeting.

The CAC continues to trade at high levels, as investors have given a thumbs-up to the improving French economy. The CAC looked strong in September, as the index jumped 4.1 percent. September PMI reports are pointing to expansion in the manufacturing and services sectors. French Final Manufacturing PMI accelerated for a fourth straight month, and the September reading of 56.1 was the highest level since April 2011. The Services PMI improved to 57.0, marking a 4-month high. The Bank of France has revised upwards its 2017 growth forecast to 1.7 percent, up from 1.6 percent in July and 1.4 percent in June. The OECD has also revised its growth forecast to 1.7 percent, up from 1.3 percent. However, the OECD cautioned that more work needs to be done, saying that France’s growth is contingent upon President Emmanuel Macron implementing a long-term plan to slash public spending, which is the highest in the 35-member OECD.

Investors don’t appear too concerned about the crisis in Catalonia, as European stock markets have been steady this week. The situation remains volatile, as the Spanish government and the Catalan regional government remain deadlocked over Sunday’s independent referendum. The violence between police and voters left close to 900 civilians injured, and tensions remains high. Catalan officials claim that 90 percent of the votes were if favor of independence, but the national government has declared the vote unconstitutional and illegal. On Wednesday, Catalonia declared a general strike and some 700,000 people demonstrated in Barcelona. Catalan Carles Puigdemont has not showed any intent to back down, warning that his government plans to act in a matter of days. The crisis is not expected to weigh on the euro or European stock markets, as the referendum is viewed as an issue local to Spain, and not to the eurozone in general. As well, the Spanish economy is in good shape, so a constitutional crisis is unlikely to affect the country’s economic growth. Still, Catalonia is heavily dependent on tourism, and an ongoing conflict could deter tourists and take a toll on the Spanish economy.

The Pound is Running for its Life

The GBP/USD pair has fallen to three weeks' lows. Taking into account how fast the American currency has been strengthening this Autumn, one can really expect the trend to continue in the future.

Over a short-period of time, the strong USD has easily sent the British Pound to the levels it reached in the middle of September. Investors increased their focus on the technical picture and paid little attention to the fundamental news, although it may offer something really impressive.

Yesterday, it became known that September was a pretty "flat" month for the British manufacturing. The HIS Markit statistics showed that the Manufacturing PMI decreased more than earlier. The indicator fell from 56.7 points in August to 55.9 points in September. It's still above the psychologically-crucial level, 50 points, which shows the difference between growth and decline, but may yet plummet pretty quickly.

The same report confirmed that the output was growing, but also a bit slower than before. The ascending tendency has been continuing for 14 months in a row, but in September the number of new orders was increasing moderately, and that's some kind of a warning sign. However, summarizing the above, one can say that British enterprises and factories are quite optimistic as 51% of them are expecting the British manufacturing to improve in the next 12 months.

The Brexit went on the back burner for a while. The negotiations between the United Kingdom and the European Union are in progress and at present moment the parties are discussing aspects of future legislative and taxation systems, and trade and economic cooperation after the UK exits the Union. There is no point in waiting for any quick news here. The process is going on according to "two steps forwards, one step backwards" principle.

The technical chart of the GBP/USD pair shows that the uptrend continues and the fact that bulls pushed the price above the resistance line only made them stronger. The short-term picture of the previous two weeks indicates the correction inside the current ascending channel. The main target of the descending correction is close to the support level at 1.2975. However, if one takes into account the fact that the uptrend may get stronger, the target of the correction may be close to the fractal level at 1.3148, where the price may reverse. In case the instrument reverses and starts forming a new rising impulse, the target will be at 1.40.

Technical Outlook: WTI OIL – Risk Of Further Downside On Firm Break Below Cracked $50 Support

WTI oil cracked strong support at $50 (Fibo 38.2% of $45.57/$52.84 rally / weekly cloud top / psychological support) on Wednesday, in extension of pullback from fresh recovery high at $52.84 (the highest since mid-Apr).

Oil price stands in red for the fifth straight day, in extended correction that undermined broader bulls.

Markets are concerned that strong uptrend which lasted for the most of Q3 may not extend further, which resulted in profit-taking and dragged the price lower.

Oil prices were well supported on strong signs of market rebalancing on rising demand which offset the impact from global oversupply that kept oil prices depressed for longer period of time.

Also, output reduction from OPEC and top oil producers outside the cartel, gave results and boosted the price.

However, rising oil production in the US, which is not participating in oil production cut limited oil's recovery rally.

Price is now at the breakpoint and sustained break below $50 pivot would spark fresh extension of pullback from $52.84 peak towards initial target at $49.50 (200SMA) and may accelerate towards $49.20 (Fibo 50%) and $48.85 (rising 55SMA).

However, bears may take a breather above $50 pivot as slow stochastic is deeply oversold on daily chart.

Limited upside action is expected, with initial barrier at $50.71 (Tuesday's high) and extended upticks to be capped by south-turning 10SMA (currently at $51.16).

Res: 50.22, 50.71, 51.16, 51.38

Sup: 49.90, 49.50, 49.20, 48.85

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The greenback gained ground at the beginning of the day, but changed course in the American afternoon to end the day marginally lower against the EUR. The pair traded as low as 1.1695 on the back of persistent dollar's demand, fueled during Asian trading hours by a dovish RBA, which not only kept the monetary policy unchanged, but also voiced its concern about Aussie's strength. The European and US macroeconomic calendars had little to offer, with the EU releasing August PPI, up in the month by 0.3% and by 2.5% when compared to a year earlier, having not much effect over the common currency. In the US, the NY ISM Business Conditions Index dropped into contraction territory in September, down to 49.7 from August 56.6, putting the greenback under short-term pressure in the absence of more relevant news.

This Wednesday, market's attention will focus on the final Services and Composites PMIs figures for both economy, while more relevant, ECB's Draghi and Fed's Yellen are scheduled to speak in different events. They are set to deliver opening remarks, Draghi at the inauguration of the ECB visitor center in Frankfurt, and Yellen at a banking conference in St. Louis. Market players will be scrutinizing their words for clues on upcoming monetary policy decisions.

The EUR/USD pair closed the day in the 1.1750, and despite a few pips up for the day, it posted a lower low and a lower high daily basis, a sign that the dominant bearish trend remains firm in place. In the 4 hours chart, an early attempt to recover ground was contained by selling interest around a flat 20 SMA, currently around 1.1770, while technical indicators remain within bearish territory, with limited downward strength amid the restricted intraday action seen this Tuesday. The key support, in the case of further slides comes at 1.1660, August monthly low, with a break below the level opening doors for an extension towards 1.1460 the level that contained rallies for most of 2015 and 2016. The bearish pressure may ease on a recovery above the 1.1820/30 region, but a stronger advance is still out of sight.

Support levels: 1.1720 1.1690 1.1660

Resistance levels: 1.1770 1.1825 1.1860

USD/JPY

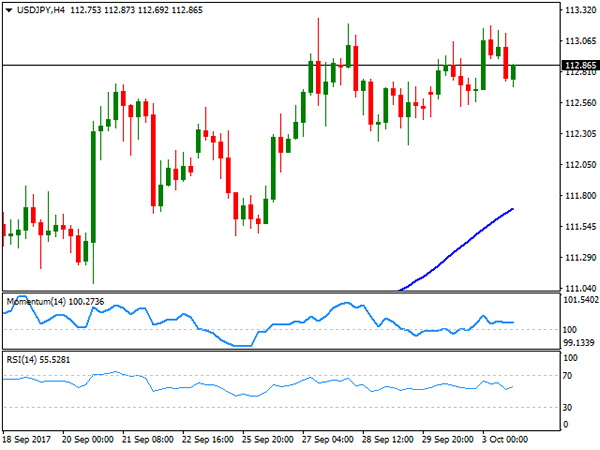

The USD/JPY pair maintained the positive tone, but there was no follow-though, with the pair still consolidating around 113.00. It traded as high as 113.19 intraday, backed by an advance in US Treasury yields, as the 10-year note benchmark traded as high as 2.35% while the 30-yer bond yield reached 2.89% mid-day. Softer-than-expected US data pushed yields and the pair marginally lower in the US session, with the pair ending the day up anyway, at 112.85. There's no data scheduled in Japan during the upcoming Asian session while China will remain on holidays, anticipating further quietness around the pair. Clues will come from local equities, which will likely follow Wall Street's positive lead, therefore keeping the pair afloat. Ahead of the Asian opening, the 4 hours chart maintains a neutral-to-bullish technical stance, as indicators continue heading nowhere around their mid-lines, but the price is developing well above bullish moving averages, with the 100 SMA now standing around 111.70. The pair still needs to accelerate through 113.25, where it topped last week, to be able to advance further, eyeing then a major static resistance at 114.40. Still the pair can continue ranging ahead of US employment data to be released next Friday, usually a big market mover for the pair.

Support levels: 112.60 112.20 111.85

Resistance levels: 113.25 113.60 114.40

GBP/USD

The British Pound was once again the worst performer against the greenback, amid poor UK data, with the GBP/USD pair ending the day in the red at 1.3247 after printing a daily low of 1.3221. UK's Markit construction PMI contracted for the first time since the immediate aftermath of the Brexit referendum, down to 48.1 in September from 51.1 in August. According to the report, the drop was attributed to fragile confidence and subdued risk appetite among clients, especially in the commercial building sector. Another factor weighing on Pound these days is the lack of progress in Brexit negotiations as the clock keeps ticking towards the divorce. At this point, the pair has trimmed pretty much all of the post-BOE's September meeting gains, when the Central Bank offered an unexpected hawkish rhetoric towards rate hikes, although a hike is still on the table. Technically, the bearish momentum decelerated according to readings in the 4 hours chart, but the downward risk persists, as indicators are consolidating within overbought territory, whilst the 20 SMA extended its decline above the current level, now converging with the 61.8% retracement of the latest bullish run, at 1.3340. A break below the mentioned daily low, will likely result in a full retracement, with the pair falling down to 1.3146, September 14th low.

Support levels: 1.3220 1.3185 1.3145

Resistance levels: 1.3300 1.3340 1.3385

GOLD

Spot gold closed the day pretty much unchanged at $1,271.75 a troy ounce, confined to a tight range all through the day. The yellow metal, however, extended its decline intraday towards 1,268.28, its lowest since mid August, indicating that bears remain in the driver seat. Expectations that the US Federal Reserve will raise rates next December have kept the commodity under pressure ever since the early September meeting, and unless the market changes its mind over the event, gold has little chances of recovering ground. From a technical point of view, the daily chart shows that an early advance was contained by selling interest around the 100 DMA, currently at 1.274.50, whilst the RSI indicator extended its downward slope, now nearing oversold territory at 35, and the Momentum stands flat well into negative territory, all of which favors another leg lower ahead. As commented on previous updates, a key support comes now at the 200 DMA, currently at 1,261.40. In the 4 hours chart, the technical outlook is also negative, as the price stands below a bearish 20 SMA, whilst technical indicators hover near oversold readings, with no aims of turning higher.

Support levels: 1,268.30 1,261.40 1,252.90

Resistance levels: 1,283.10 1.294.25 1,303.95

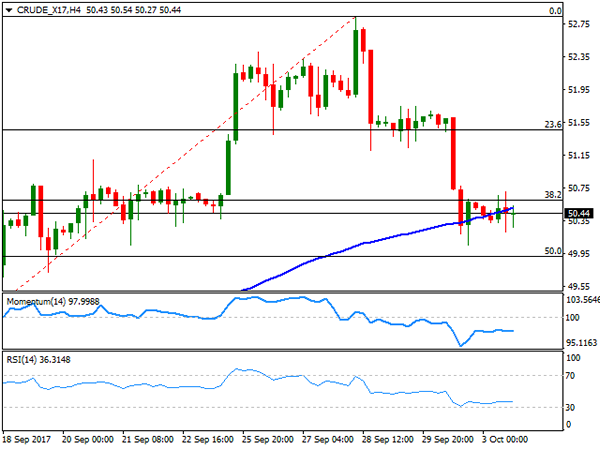

WTI CRUDE OIL

West Texas Intermediate crude oil price ended the day at $50.40 a troy ounce, little changed from its previous close. The commodity held in a limited range this Tuesday, although not far from Monday's low, as the dollar maintained its strength across the board, whilst there were no fresh news for the oil market. Ahead of the API and the more relevant EIA US stockpiles report, the commodity seems poised to extend its decline, according to technical readings in the daily chart, as it held below a key Fibonacci resistance, the 38.2% retracement of the latest bullish run at 50.60, still the immediate resistance. In the same chart, technical indicators keep grinding lower, now about to enter negative territory, although the price remains well above its long-term moving averages. In the 4 hours chart, WTI is biased lower, as it´s now standing below its 100 SMA, whilst technical indicators gain downward strength within negative territory. The immediate support comes at 49.90, the 50% retracement of the mentioned rally, with a break below it opening doors for a continued decline this Wednesday.

Support levels: 49.90 49.30 48.65

Resistance levels: 50.60 51.20 51.85

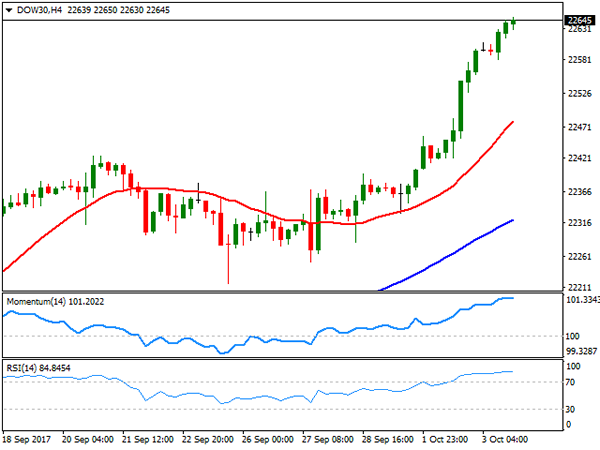

DJIA

US indexes closed at record highs this Tuesday, backed by latest US upbeat data, and a rally in airlines-related equities. The Dow Jones Industrial Average gained 84 points, to end at 22,641.67, the Nasdaq Composite added 15 points to 6,531.71, while the S&P closed at 2,534.58, up by 0.22%. US stocks extended their positive Monday momentum, triggered by a better-than-expected ISM manufacturing PMI, which indicated solid economic growth. Within the Dow, Wal-Mart led advancers, up 1.08%, followed by American Express which added 0.99%. Only six members were down, led by Nike that shed 0.80%. The DJIA is up for a fifth consecutive day, up for over 15% so far this year, and clearly overbought according to long-term technical readings, but offering no signs of changing course. However, as higher it moves, the higher will be the risk of a sudden downward correction. In the daily chart, technical indicators head sharply higher, with the RSI currently at 78, and with moving averages accelerating north below the current level. Shorter term, the index is also bullish and extremely overbought, with the RSI indicator currently heading north around 85, the Momentum also aiming higher, and the 20 SMA gaining further upward strength below the current level, currently at 22,481, in line with the longer term perspective.

Support levels: 22,617 22,581 22,557

Resistance levels: 22,660 22,700 22,740

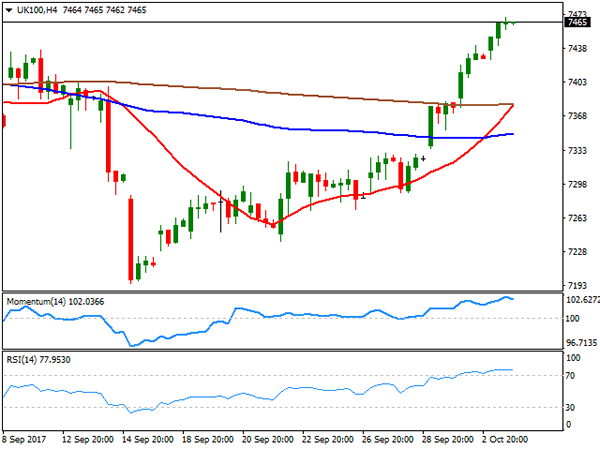

FTSE100

The FTSE 100 advanced 29 points to 7,468.11 this Tuesday, helped by continued Pound weakness. Plumbing supplies group Ferguson was the best performer, up 4.03%, as the company reported an 8.6% raise in annual revenues at its ongoing businesses, with trading profit up 8.7% to £1.03bn. Ashtead Group followed, up by 3.29%. Leading losers was Admiral Group that lost 2.73%, followed by WPP that lost 2.08% after Morgan Stanley sold 22.5 million shares. The Footsie closed at its highest in nearly two months, maintaining the positive momentum in its daily chart, as the index advanced further above its 20 and 100 SMAs, while technical indicators accelerated higher within bullish territory. Shorter term and according to the 4 hours chart, the index settled near its daily high and with moving averages supporting additional gains, as the 20 SMA is about to surpass the 200 SMA after breaking through the 100 SMA, but technical indicators are giving some signs of upward exhaustion in overbought territory, suggesting a downward corrective movement is possible this Wednesday.

Support levels : 7,444 7,408 7,371

Resistance levels: 7,466 7,495 7,535

DAX

European equities gained this Tuesday, although there was no action in the DAX, as Germany had a bank holiday due to the Day of German Unity, with the latest registered close for the index at 12,902.65. Equities in the region were supported by gains in the retail sector, but political concerns may hit European indexes this Wednesday, as tensions within Spain are still a key issue for the region, given that the central government in to will to give its arm to turn, while the Catalonia region prepares to declare its independence. As commented on the previous update, the index is not far from its intraday record high of 12,953, and technical readings in the daily chart favor additional gains ahead, given that technical indicators maintain their upward strength, with the RSI indicator currently at 76, while the index moves further above bullish moving averages. In the 4 hours chart, technical readings also support a new leg higher, as the 20 SMA accelerated north below the current level, whilst technical indicators have turned flat after the close, within extreme overbought readings.

Support levels: 12,796 12,752 12,710

Resistance levels: 12,847 12,881 12,933

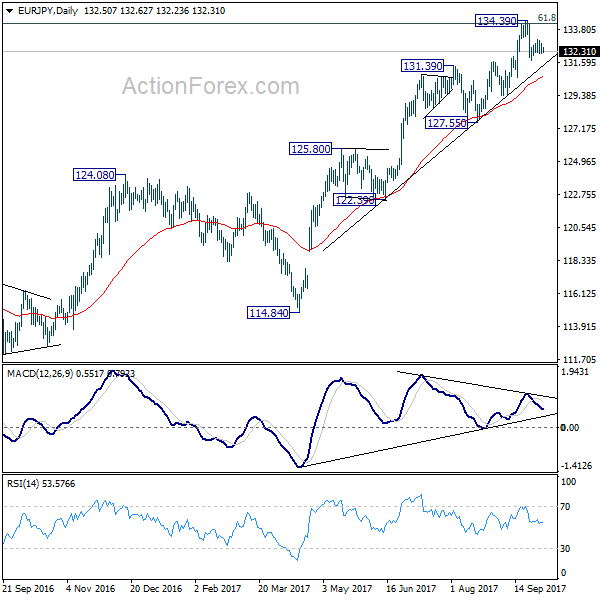

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.16; (P) 132.52; (R1) 132.87; More...

Intraday bias in EUR/JPY remains neutral for consolidative trading below 134.39 high. Near term outlook remains bullish as long as 131.69 holds. Sustained break of 134.20 fibonacci level will extend larger up trend to 141.04 resistance next. However, break of 131.69 will be an early sign of medium term reversal and will target 127.55 key support level instead.

In the bigger picture, current rise from 109.03 is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. On the downside, break of 127.55 support is needed to be the first signal of medium term reversal. Otherwise, outlook will remain bullish.

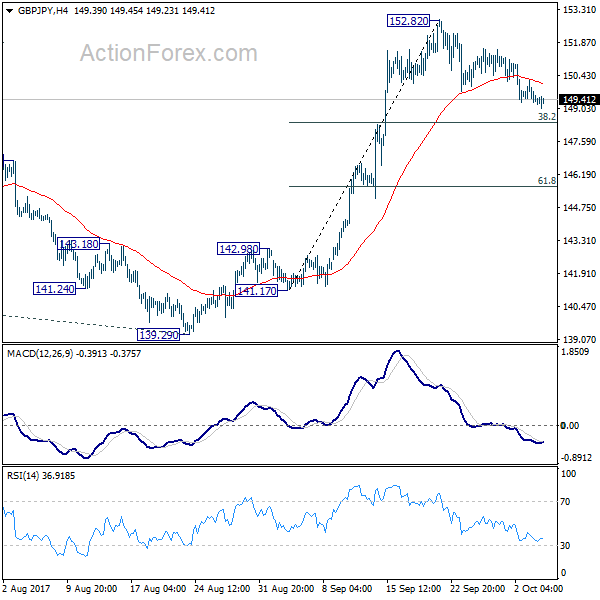

GBP/JPY Daily Outlook

Daily Pivots: (S1) 149.03; (P) 149.64; (R1) 149.99; More

Intraday bias in GBP/JPY remains neutral for consolidation below 152.82. At this point, we'd still expect downside to be contained by 38.2% retracement of 141.17 to 152.82 at 148.36 to bring rebound. Break of 152.82 will extend the larger rise from 122.36 to 61.8% projection of 122.36 to 148.42 from 139.29 at 155.39 next.

In the bigger picture, medium term rebound from 122.36 is in progress. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. For now, the bullish scenario is preferred as long as 139.29 support holds.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1768

The overall bias is still bearish below 1.1830, for a slide through 1.1700, towards 1.1480 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1830 | 1.2070 | 1.1660 | 1.1660 |

| 1.2000 | 1.2240 | 1.1540 | 1.1480 |

USD/JPY

Current level - 112.51

My intraday outlook is counter-trend, for a reversal above 112.15 and break through 113.25 peak.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.20 | 113.80 | 112.15 | 111.50 |

| 113.80 | 114.50 | 111.50 | 107.30 |

GBP/USD

Current level - 1.3273

The rebound above 1.3220 is still underway and despite the risk of a test at 1.3340 major hurdle, the overall bias remains bearish, for 1.3150.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3300 | 1.3650 | 1.3220 | 1.3340 |

| 1.3340 | 1.3830 | 1.3150 | 1.3150 |