Sample Category Title

British Pound Reaching Key Support Vs US Dollar

Key Highlights

- The British Pound is in a major downtrend from the 1.3650 swing high against the US Dollar.

- There is a crucial descending channel forming with resistance near 1.3320 on the 4-hours chart of GBP/USD.

- UK's British Retail Consortium (BRC) Shop Price Index in Sep 2017 decreased 0.1% (YoY).

- Today in the US, the ADP Employment Change figure will be released for Sep 2017, which is forecasted to register 130K, down from 237K.

GBPUSD Technical Analysis

The British Pound after an impressive run found a strong barrier near 1.3650 against the US Dollar. The GBP/USD pair declined below 1.3300, but remains well above a major support near 1.3160.

During the downside move, the pair broke the 100 simple moving averages (H4) (Red Color SMA) and the 23.6% Fib retracement level of the last wave from the 1.2852 low to 1.3657 high.

A crucial descending channel with resistance near 1.3320 on the 4-hours chart is acting as a downside move catalyst. At the moment, the pair is finding bids near 1.3220 and the 50% Fib retracement level of the last wave from the 1.2852 low to 1.3657 high.

On the downside, there is a major support at 1.3160. If the pair dips further, the mentioned 1.3160 support might act as a barrier for sellers in the near term.

UK's British Retail Consortium (BRC) Shop Price Index

Today in the UK, the British Retail Consortium (BRC) Shop Price Index for Sep 2017 was released. The forecast was slated for a minor increase of 0.1% in the index compared with the same month a year ago.

The actual result was on the lower side, as there was a decline of 0.1% in the index (Sep 2017). However, it was up from the last decline of 0.3%.

Commenting on the report, the Chief Executive, British Retail Consortium, Helen Dickinson OBE, stated:

Overall shop price deflation reached an all-time low in September with prices now teetering on the edge of inflation. A number of factors have combined to drive a sharp jump in food price inflation to 2.2 per cent over the year to September.

The non-food index was down 1.5% in Sep 2017 (YoY) and the food index was up 2.2%.

Economic Releases to Watch Today

US Services PMI for Sep 2017 – Forecast 55.1, versus 55.1 previous.

US ISM Non-Manufacturing Index for Sep 2017 – Forecast 55.5, versus 55.3 previous.

US ADP Employment Change Sep 2017 – Forecast 130K, versus 237K previous.

Forex: GBP Suffers On Poor Data

On Tuesday, the UK HIS Markit/CIPS construction Purchasing Managers Index (PMI) for September fell to 48.1 from the previous data release in August of 51.1. With market consensus expecting an unchanged figure for September, the markets reacted negatively and GBP was sold against its peers. The contraction is blamed on weak new orders and this is the first time the index has been below the key 50-change threshold in just over a year – with this release indicating the fastest decline in construction since July of last year. Such poor data, along with the political and economic uncertainty surrounding Brexit, continues to worry the market. In the last week, GBPUSD has fallen 2%, albeit aided by a stronger USD. The markets will be keenly watching today’s’ Service PMI for further clarity as to the “state” of the UK economy.

There is speculation that President Trump’s choice for the next Chairperson of the Federal Reserve could be a more hawkish candidate than many expect. With current Fed Chair Janet Yellen’s term expiring in February, there appears to be a number of “front runners” who both recently had interviews at the White House last week. One such candidate is Kevin Warsh, who was the first candidate to be interviewed and is rumored to be Trump’s preferred choice. Warsh has been vocally critical of the Fed’s bond-buying program and its current policy, and he is considered much more hawkish than Janet Yellen. Indeed, a Warsh nomination would most likely result in higher interest rates and a stronger USD.

EURUSD is 0.2% higher in early Wednesday trading, at 1.1765.

USDJPY is little changed overnight and currently trades around 112.65.

GBPUSD has retraced higher from yesterday’s lows, gaining 0.3% in early trading. Currently, GBPUSD is trading around 1.3270.

Gold has improved against USD overnight to currently trade around $1,276.

WTI is unchanged from last nights close, currently trading around $50.35.

Major economic data releases for today:

At 08:00 BST, the European Central Bank will hold a Non-Monetary Policy Meeting in Frankfurt, Germany.

At 08:55 BST, Markit Economics will release German Services PMI and Composite PMI for September. Composite is forecast to be unchanged at 57.8 and Services also unchanged at 55.6.

At 09:00, Markit Economics will release Eurozone Services PMI and Composite PMI for September. Composite is forecast to be unchanged at 56.7 and Services also unchanged at 55.6.

At 9:30, Markit Economics and the UK Chartered Institute of Purchasing & Supply will release UK Services PMI for September. The release is expected to be unchanged from the previous reading of 53.2.

At 18:15 BST, ECB President Mario Draghi is scheduled to provide opening remarks at the Inauguration of the ECB Visitor Centre in Frankfurt, Germany.

At 20:15, Federal Reserve Chair Janet Yellen gives brief welcome remarks before the Community Banking in the 21st Century Research and Policy Conference, hosted by the Federal Reserve Bank of St. Louis, Missouri.

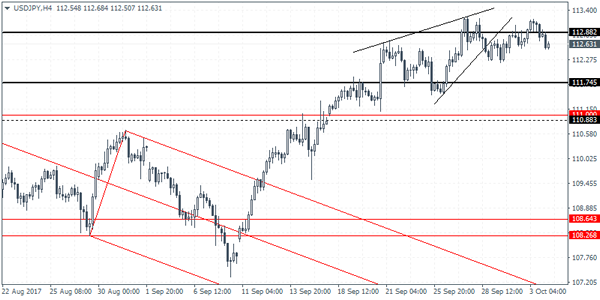

USDJPY Intraday Analysis

USDJPY (112.63): The USDJPY closed with a doji type candlestick yesterday. Price action has been consolidating near a long-term falling trend line for the past few daily sessions. This indicates a near-term decline to the downside. On the 4-hour chart, the rising wedge pattern remains in play although price action briefly rallied above the resistance level of 112.88. The reversal near this resistance level signals a possible downside move. Support at 111.74 remains in the picture as the likely downside target.

GBPJPY Intraday Analysis

GBPJPY (149.41): The British pound was seen extending the losses as price action cleared the support level at the support zone of 150.40 - 150.05. This breakdown below the support also validated the descending triangle pattern we see on the 4-hour chart. GBPJPY briefly rallied back to the support level to establish resistance. The reversal off this level could now signal a downside move. Support at 148.23 comes into focus and also marks the measured move of the descending triangle pattern. A decline to 148.23 will signal a reversal off this support level in the short term with GBPJPY likely to move sideways thereafter.

EURUSD Intraday Analysis

EURUSD (1.1768): The EURUSD closed with an indecisive candlestick pattern following the declines off the resistance level at 1.1822. Price action is currently attempting for a bullish day but the risks remain equally balanced. To the downside, the decline to 1.1688 will mark the completion of the descending triangle pattern. Price action was seen falling short of a few pips before the reversal yesterday. Resistance at 1.1822 - 1.1843 remains in focus for another retest to this level. The bias will shift to the upside on a close above this resistance level. In this case, EURUSD could be attempting to push higher with a new range between 1.2058 resistance and the support at 1.1822 - 1.1843 coming into play.

Dollar Pauses Gains As Investors Await ADP Data

The US dollar was seen taking a break following the previous sessions which saw the greenback posting some gains. Lack of any clear market moving events from the US yesterday saw investors in a holding pattern, ahead of today's private payroll numbers.

In the UK, the construction PMI was weak, falling to 48.1. This was below forecasts of 51.1 and weakened from the same level from a month ago. The data marked a contraction in the construction sector for the first time since the July 2016 Brexit vote.

Looking ahead the ADP/Moody's private payrolls data will be the main event for the day. Economists forecast that private payroll hiring rose 131k for the month of September, after an initial payroll print of 237k in August. With the hurricanes hitting the US shores last month, the possibility of a weaker jobs print is quite a possibility.

Among the central bank speeches today, the ECB president Mario Draghi and the Fed Chair, Janet Yellen will be speaking closer to the evening.

USDJPY Gives Way To Technical Selling

The USDJPY has slipped below key weekly support, after the pair gave way to strong technical selling, after several failed attempts to push price-above the former weekly price-high, at 113.25.

Today's trading sentiment surround the USDJPY pair is neutral to slightly bearish, as the pair awaits the ADP jobs report for the month of September, and a key-note speech from FED Chair Janet Yellen.

Going forward, the USDJPY pair risks deeper trading losses whilst price-action remains beneath its daily pivot, at 112.90 and the key 112.70 support level.

The U.S dollar index is also seeing broad-based weakness across the board, and that is also a contributing factor to recent softness in the USDJPY pair.

Key intraday technical support below the 112.70 level is found at 112.40, which represents the pairs weekly pivot point. Further support is also found at 112.28 and 111.90, and the USDJPY 200-week moving average, at 111.69.

To the upside, key intraday technical resistance above 112.70 is found at 112.90 and 113.25. Once above 113.25, further resistance is seen at 113.57 and 113.89.

Euro Testing 1.1770 Pivot

The EURUSD has moved higher to test the pivotal 1.1770 technical area, after the U.S dollar index slipped back towards the 93.00 mark, and the euro found strong buying interest from the 1.1700 level.

Today, the euro's directional bias will be influenced by high-impact jobs data from the United States, and key-note speeches after the European market close, from ECB president Mario Draghi and FED Chair Janet Yellen.

Going forward, the 1.1770 level will be key for the EURUSD, with the pair needing to gain traction above this level to further buying interest.

Technical failure around the 1.1770 level will likely see the euro sold back towards key intraday technical support, around the 1.1736 level.

Key intraday resistance above the 1.1770 level is found at 1.1800, and the pairs weekly pivot point, at 1.1823. Above the weekly pivot point, the former swing price-high, at 1.1832, and the monthly pivot, at 1.1875, are key resistance areas.

To the downside, key intraday support is found at the pairs 100-hour moving average, at 1.1764 and the euro's daily pivot point, at 1.1736. Once below the 1.1736 level, traders focus will turn towards a further technical retest of the key 1.1710 level.

Economic Data , Monetary Policy In The Spotlight On Wednesday

A deluge of market-moving events will take the spotlight on Wednesday, with reports from both sides of the Atlantic set to be released.

Europe will see a deluge of PMI reports beginning at 07:15 GMT. Spain, Italy, France, Germany, United Kingdom and Eurozone are all expected to see final PMI numbers for the month of September. For the Eurozone, the PMI Composite Index is expected to read 56.7. Germany’s Composite index is forecast to read 57.8.

The European Commission’s statistical agency will also report on Eurozone retail sales at 10:00 GMT. Receipts at retail stores are forecast to rise 0.3% on month and 2.6% annually.

In North America, payrolls processor ADP Inc. will report on private sector job creation for the month of September. Private payrolls likely rose by 130,000 last month, based on a median estimate of economists. That follows a 237,000 gain the month before.

Later in the session, IHS Markit and the Institute for Supply Management (ISM) will release separate PMI indicators for the US services sector. Both reports are expected to show steady growth in services for the month of September.

On the monetary policy front, Federal Reserve Chairwoman Janet Yellen and European Central Bank (ECB) President Mario Draghi will each deliver speeches during the afternoon.

The US dollar index (DXY) was down 0.2% on Wednesday, giving up some of its recent gains. Dollar pairs will face heavy action in the coming days as investors turn their attention to US jobs data. The nonfarm payrolls report on Friday could elicit heavy volatility in the currency market.

EUR/USD

The euro is back in recovery mode on Wednesday, as calm returned to the market following the Catalan independence vote. The EUR/USD exchange rate rose 0.2% to 1.1765 in Asian trading. The pair faces immediate support at 1.1696, which represents the daily low from 3 October. On the opposite side of the ledger, the bulls are eyeing 1.18 as a significant milestone.

GBP/USD

The British pound rose against the dollar on Wednesday, although cable remains several hundred pips below last month’s high. The GBP/USD exchange rate rose 0.2% to 1.3262 in the Asian session. From a technical perspective, the pair has the support of the 1.3220 region. A break below that level would expose the 14 September low of 1.3146. On the opposite side of the spectrum, immediate resistance is seen at 1.3340.

USD/JPY

The USD/JPY slammed on the breaks Wednesday, as the greenback paused following multiple rallies. The pair was down 0.2% in Asian trading, where it was seen consolidating in the low 112.60 region. The bulls retain control of the market, with investors expecting a more bullish push toward 113.80.

Oil And Gold Enter The Holding Pattern

Oil and Gold entered a holding pattern overnight with quiet range trading ahead of key data.

Oil prices ended Tuesday with more of a whimper than a roar, with Brent and WTI falling around 40 cents to open in Asia at 55.80 and 49.80 respectively. An unexpectedly large drawdown of 4.079 million barrels from the American Petroleum Institute (API) crude inventories, was more than offset by an equally large 4 million plus build in gasoline stocks. It appears that the overhang of speculative long positioning is continuing to overhang oil markets although one suspects this has now been substantially reduced over the past week.

Traders’ will be watching tonight’s official Department of Energy crude inventory data for more clues with the street expecting a small drawdown of around 0.5 million barrels. An unexpected increase from this number could see more short-term pain for speculative longs, particularly in WTI.

Brent spot is perched just above support at 55.50 this morning, the bottom of the long-term resistance zone the contract took out last week. Failure here suggests a test of the 54.80 level ahead of trend line support for the entire June to September rally at 53.65 this morning. Resistance is at 56.60 and 57.00 although both levels now look unlikely to be seen in the Asia session.

WTI spot has nearby support at 49.60 followed by a series of daily lows and the 200-day moving average at 49.25. A break of 49.25 implies a much deeper correction is on the cards to the 100-day moving average at 47.60. Resistance is at 50.50 initially followed by the 51.40 regions, a daily double top and the former trend line support that WTI broke on Monday.

Gold

Gold ranged quietly overnight, climbing slightly to finish three dollars higher at 1275.00 as Asia trading gets underway. With China on holiday this week we would expect precious metals to be subdued in Asia. However, volatility should pick up in North America as we head into a data-heavy end of the week. The street appears to be on hold for just that given a general lack of volatility in markets overnight.

Gold has initial resistance at 1281.00 and then 1296.00 with the 100-day moving average, just below at 1272.00, serving as an intra-day pivot point. Below here, support appears at 1268.50 and then 1263.00 ahead of the 200-day moving average at 1251.00.