Sample Category Title

Currencies: EUR/USD Shows No Clear Trend On Political Issues In US And EMU

Sunrise Market Commentary

- Rates: Profit taking ahead of Friday's payrolls?

Stronger eco data could be countered by increased uncertainty over Catalonia, the next Fed chair and promised tax reforms. Adding the prolonged sell-off, it suggests that investors might take some profit on short positions ahead of Friday's payrolls. The US Note future remains in a sell-on-upticks environment with proposed entry levels around 126. - Currencies: EUR/USD shows no clear trend on political issues in US and EMU

The dollar rally stalled yesterday. EUR/USD might continue a ST consolidation pattern as political issues in the US (nomination of successor for Yellen, tax reform) and in EMU (Catalonia) might prevent investors to take directional positions. The USD/JPY rally might also slow if the equity rally takes a breather.

The Sunrise Headlines

- WS (+ 0.3%) clocked a second straight day of record highs for each of its major indices. Most Asian stock markets trade positive overnight with China still closed. The Japanese services PMI dropped to its weakest level in 11 months.

- Catalonia will declare independence 'in a matter of days', Catalan President Puigdemont was quoted as telling the BBC, a move that would defy Madrid and attempt to implement the directive of Sunday's illegal referendum.

- Donald Trump said 'you can say goodbye' to Puerto Rico's debt. 'They owe a lot of money to your friends on Wall Street and we're going to have to wipe that out,' Mr Trump told a Fox interviewer. 'You can say goodbye to that.'

- President Trump's aides have given him a final short list of recommended candidates to head the Fed, people familiar said. Janet Yellen, Gary Cohn, Kevin Warsh and current governor Jerome Powell are being considered.

- Auto sales hit their briskest monthly pace for the year, as Labor Day discounts, higher fleet sales and hurricane-related replacements restored momentum heading into the final months of the 2017.

- Boris Johnson has distanced himself from leadership speculation, claiming that 'the cabinet is united' on PM May's Brexit strategy. He laughed off what he called 'potshots from behind' as an 'occupational hazard in my line of work.'

- Today's eco calendar heats up with September services PMI's in EMU (final), the UK and the US (ISM). US ADP employment is also on the agenda while Germany holds a 10-yr Bund auction.

Currencies: EUR/USD Shows No Clear Trend On Political Issues In US And EMU

Dollar rally takes a breather

Yesterday, the dollar rally took a breather, awaiting more guidance from key eco data (including the US payrolls) later this week. A series of pending political issues in the US were also a slightly USD negative. EUR/USD made a cautious intraday rebound and closed the day at 1.1744. USD/JPY hovered in the 113 area for most of the day, but finally dropped below the big figure even as major US equity indices continue to set new all-time record levels.

Overnight, Asian equities ex-Australia continue their uptrend. The Japan services PMI dropped from 51.6 to 51.00 in September, indicating modest growth in the sector. However, it didn't hurt the yen. The dollar declined slightly further as the political debate on a successor for Fed's Yellen intensifies. There are rumours that chances of Fed member Powell, also on the shortlist, are growing. USD/JPY dropped to the mid 112 area. In the same vein, EUR/USD settled again in the upper half of the 1.17 big figure.

Today, the EMU calendar contains the final PMI. The preliminary reading rose to 55.6 from 54.7, suggesting buoyant activity in the sector. Any revision is usually limited and with little impact on markets. The US calendar is more interesting. The ADP employment report is expected to show a modest net 135K gain of private sector jobs. Markets discount an negative effect from the tropical storms. Any significant deviation of consensus will probably be ignored. The ISM non-manufacturing business confidence is expected to have marginally increased to 55.5 from 55.3 in August, but risks are firmly on the upside of expectations.

The eco data (US non-manufacturing ISM) might be USD supportive. However, there is also political noise on both sides of the Atlantic. Tensions in Catalonia remain high as the region might declare independence within days. For now, Catalonia was hardly a factor for the euro, but this might change. In the US, investors look for more clarity on the nomination of a successor for Yellen and on the tax reform. However, Investors are unlikely to big directional bets ahead of the payrolls (Friday). EUR/USD might hover in the 1.1696/1.1833 ST consolidation pattern. A more cautious risk sentiment after the recent equity rally might block the topside in USD/JPY

EUR/USD downtrend slows as political issues on both sides of the Atlantic keep investors sidelined

EUR/GBP

EUR/GBP nears 0.89 resistance area .

The positive sterling momentum ebbed recently and this continued yesterday. EUR/GBP rebounded further off the key 0.8742/75 support. The UK construction PMI suggested a contraction in the sector. Coming on the heels of a softer manufacturing PMI on Monday, it was a sterling negative. The BoE also warned for potential disruptions in clearing activity after Brexit and on financing of UK corporations via European banks. EUR/GBP closed the session at 0.8871. Cable still set another ST correction low intraday and finished at 1.3237.

Today, the UK services PMI will be published and UK PM May will give a key speech at the Conservative Party meeting. The services PMI is expected to stabilize at 53.2. Another negative surprise will fuel market expectations that the room for the BoE to raise rates is limited. We don't expect too much from the speech of PM May . Her party is divided on the Brexit strategy and she probably will avoid to give concessions to Europe that will angry the grass root anti-EU party base. The noise on Brexit remain a modest sterling negative. Political uncertainty on Catalonia is a negative for the euro. Even so, we think that the downside in EUR/GBP is becoming ever better protected.

EUR/GBP made an impressive uptrend since April to set a top at 0.9307 late August. UK price data amended the dynamics and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. The prospect of (limited) withdrawal of BOE stimulus triggered a good sterling countermove. However, this rebound has apparently run its course EUR/GBP supports at 0.8743 and 0.8652 are probably difficult to break. We look to buy EUR/GBP on dips. A sustained rebound above the 0.89 area would improve the ST technical picture of EUR/GBP

EUR/GBP: downside support becomes more solid

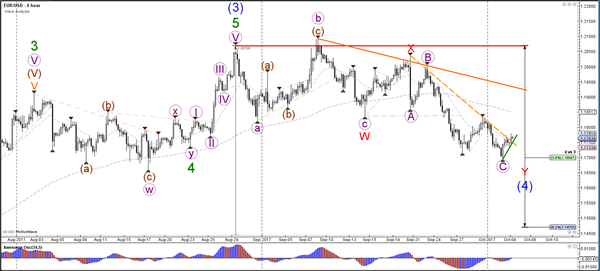

Elliott Wave View: EURUSD Short-Term

EURUSD Elliott Wave view suggests the decline from 9/8 peak is unfolding as an expanded Flat Elliott Wave structure. Down from 9/8 high (1.2094), Intermediate wave (A) ended at 1.1837 and Intermediate wave (B) ended at 1.2034. Intermediate wave (C) remains in progress as 5 waves. Minor wave 1 of (C) ended at 1.186, and Minor wave 2 of (C) ended at 1.2. Below there, Minor wave 3 of (C) ended at 1.1716, and Minor wave 4 of (C) ended at 1.1832.

While below 1.1832, pair has scope to extend lower in Minor wave 5 of (C) and reach as low as 1.16207. This area will also complete Primary wave ((W)) and end cycle from 9/8 peak. Afterwards, pair should bounce in Primary wave ((X)) to correct cycle from 9/8 peak in 3, 7, or 11 swing before turning lower again. If pair breaks above 1.1832 from here, it could be in Minor wave 4 as a flat before turning lower again in Minor wave 5.

EURUSD 1 Hour Elliott Wave Chart

Expanded Flat is a 3 waves corrective pattern, and the inner subdivision is labeled as A,B,C with 3,3,5 structure. That means waves A and B are always corrective structures i.e. could be WXY, WXYXZ, Zigzag or any 3 waves corrective pattern. Wave C is either 5 waves impulse or ending diagonal pattern. In the graphic below, we can see what Expanded Flat structure looks like. Inner structure has ABC labeling, where wave B can complete below or above the starting point of wave A. Wave C should complete below the end point of wave A (usually at 1.236-1.618 fibonacci extension A related to B).

Daily Wave Analysis: Trend Lines Offer Break And Bounce Spots For US Dollar

Currency pair EUR/USD

The EUR/USD broke the resistance trend line (dotted orange) which could indicate that price is making a second bounce at the 23.6% Fibonacci support level of wave 4 (blue). A third attempt to break below the Fib could start a larger correction towards the 38.2% Fib.

The EUR/USD bullish price action broke above two resistance lines (dotted orange) but could still resemble a rising wedge pattern and an ABC (brown). A bullish breakout becomes more likely if price manages to break above resistance (red) and the 1.18 round level.

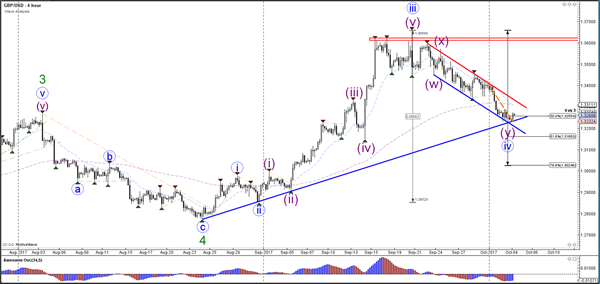

Currency pair GBP/USD

The GBP/USD is at the round level of 1.3250, which is an important support zone as they are two trend lines (blue) and a 50% Fib of wave 4 vs 3. Price will need to break above resistance (red) of the bearish channel before a larger uptrend continuation becomes more likely.

On the 1 hour chart it seems like price is building a bear flag chart pattern after breaking above the steep resistance trend line (dotted orange). A break above the resistance or below support could confirm a potential breakout.

Currency pair USD/JPY

The USD/JPY failed to break the resistance trend line (red) and instead broke below the support trend line (dotted blue). The bearish breakout could indicate the completion of wave A or 1 and the start of wave B or 2.

The USD/JPY could be in a bearish wave 3 (red).

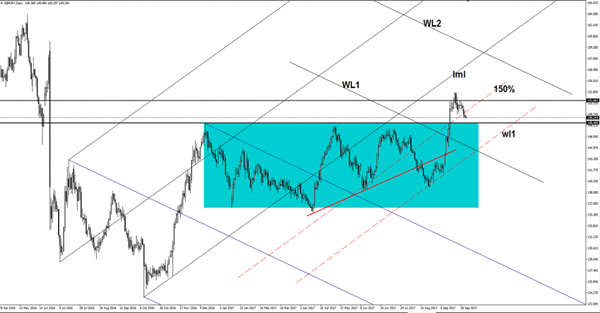

GBP/JPY Pressured By The Nikkei’s Drop

Price drops further as the Nikkei stock index retreats after the yesterday's amazing rally. A further Nikkei's increase forces the Yen the appreciate versus all its rivals on the short term. The next downside target will be at the 148.46 static support, only a valid breakdown will confirm a larger drop.

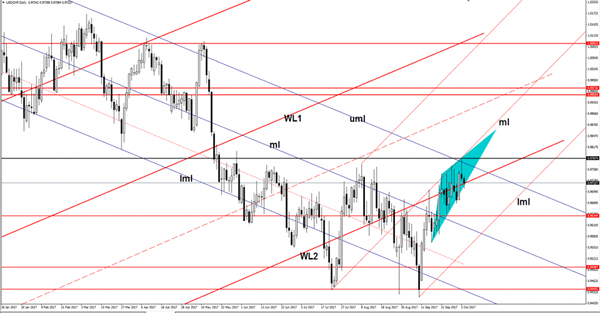

USD/CHF Rising Wedge?

The price has found strong resistance and now drops again on the short term. Has show an overbought in the previous days after the failure to close above the median line (ml) of the minor ascending pitchfork and after the failure to close near this dynamic resistance. The yesterday’s false breakout above the upper median line (uml) of the descending pitchfork signaled another leg lower. Price developed a minor Rising Wedge pattern, a valid breakdown from it will confirm a drop towards the 0.9634. USD/CHF could be attracted by the lower median line (lml) of the ascending pitchfork.

AUD/USD Downside Paused

The AUD/USD has increased sharply in the morning and has ignored a dynamic resistance. Price is trading in the buyer’s territory, but we still need a confirmation because this could be a false breakout if the USDX will start an amazing rally.

The Aussie increased even if the AIG Services Index dropped from 53.0 to 52.1 points. The greenback drops ahead of the US high impact data release, this could be crucial for the USD. The ADP Non-Farm Employment Change could drop from 237K to 131K in the previous months, while the ISM Non-Manufacturing PMI is expected to increase from 55.3 to 55.5 points.

We may have a high volatility in the US trading session, so you should be careful not to ruin your account. The FED Chair will speak tonight, but remains to see if will give some clues regarding the monetary policy.

The rate is trading in the green and tries to recover after the corrective phase. I’ve said in the last day’s that the AUD/USD seems a little oversold, but I’ve said that only a valid breakout above the median line (ml) of the descending pitchfork will confirm a minor increase on the short term. The failure to stay below the median line (ml) of the descending pitchfork will send the rate towards the upper median line (uml) of the descending pitchfork.

Technically, it could e attracted by the confluence area formed between the LML with the upper median line (uml) of the descending pitchfork. This scenario will take shape only if the US data will disappoint in the afternoon.

The Oil Market Is Likely To Be Positioned For EIA Data Today

Market movers today

In the US, Fed Chair Yellen is due to give the opening remarks at a Conference Bank seminar tonight . It is scheduled to take only 15 minutes and we do not expect her to express any new views (also because she has been quite outspoken recently). We think markets are more interested in ADP employment , as it may give us some hints about how jobs growth was affected by Hurricanes Harvey and Irma (but keep in mind that ADP jobs growth has overest imated non-farm payrolls this year). Also note that ISM nonmanufacturing is due at 16:00 CET.

In the UK, PMI service are due, which we estimate fell to 52.7 in September from 53.2 in August . If so, this would be another sign that growth was also weak in Q3 after the weak GDP growth prints in Q1 and Q2. Also, there will be focus on PM Theresa May, due to speak here on the final day of the Conservative Party conference.

In Poland, we expect the central bank to keep the policy rate unchanged at 1.50% in line with consensus.

The Oil market is likely to be positioned for EIA data today (4:30 pm CEST) to show a large drop in crude inventories after API data yesterday posted a 4mb drop last week. There was a limited response in oil market to the news though.

In the Nordics, PMI services in Sweden are due at 08:30 CEST and Norwegian house prices for September at 11:00 CEST. See also the Scandi section on page 2.

Selected market news

The US equity markets closed at record high levels and Asian markets also increased overnight, spurred by strong US September vehicle sales data suggesting that US consumption continues to do well. Meanwhile, the dollar's rally and the fall in US treasuries stalled as investors assessed the prospects for tax reform after a Republican senator raised a question about the deficit impact of such proposals. Prominent investors such as Warren Buffet and Blackrock CEO Larry Fink quest ioned the structure of the tax proposal, calling into question the necessity of deep cuts to corporate income taxes. The various criticism underscores our belief that passing of the tax reform will be difficult (see also our take on the Republican tax reform proposalStill a long way to go for tax reform, 29 August ). Furthermore, the USD witnessed some headwinds after news broke that US Treasury Secretary Steven Mnuchin is said to favour Jerome Powell as new Fed Chair over Kevin Warsh. Powell is seen as less hawkish.

The Chinese financial markets are on a weeklong holiday ahead of the important Party Congress on 18 October. We published a review yesterday of the congress and why it is key for China's road ahead. We are cautiously optimistic that Xi Jinping will find a middle road and not strengthen his power so much that it creates a backlash at a later stage. We also see a good chance that reform implementation will move up the agenda next year following his first term in which Xi has focused on politics and his power base.

Market Update – Asian Session: Asian Trading Subdued As Chinese Holiday Continues

Asia Summary

Asian equity markets have traded mixed with markets in China and South Korea remaining closed for holidays. Markets in Taiwan are also closed on today’s session in observance of a national holiday. Japan’s Topix has underperformed amid weakness in the banking sector. Equity markets in the Philippines and Indonesia trade at record highs.

In corporate news, Amazon Japan is said to be planning to invest in the area of fashion. On the inflation front, beer maker Asahi Group is reported to be planning to raise prices by ~10% in March, which would be the first increase in 10-years. Shares of Japan Display have gained over 25%.

Following the US equity close, Fitch downgraded the credit ratings of banks including Fifth Third and Wells Fargo.

The US dollar has traded with a generally weaker tone ahead of the later today release of the ADP monthly payrolls report. The declines also have come amid lower Treasury yields and speculation related to the Fed chair position.

Bank of Japan (BoJ) Deputy Gov Nakaso did not rule out a deficit related to the central bank’s exit strategy from easing measures, but suggested that officials are prepared for this.

The World Bank raised China’s 2017 and 2018 GDP growth forecasts, putting them in line with those of the IMF.

Key economic data

(AU) Australia Sept AiG Perf of Services Index: 52.1 v 53.0 prior

(JP) Japan Sept Nikkei PMI Services: 51.0 v 51.6 prior

(NZ) New Zealand Sept ANZ Commodity Price: +0.8% v -0.8% prior

(UK) UK Sept BRC Shop Price Index Y/Y: -0.1% v -0.3% prior (smallest decline since May 2013)

Speakers and Press China

(CN) World Bank raises forecast for 2017 China GDP growth to 6.7% (6.5% prior); raises 2018 GDP growth forecast to 6.4% (6.3% prior)

Other

(JP) BoJ Dep Gov Nakaso: Does not rule out BoJ deficit in exit strategy - Japan Press; Revenue fluctuations in the short-term from exit strategy will not hurt policy execution as BoJ had been saving some of its revenues for future losses.

(US) President Trump aides said to deliver shortlist for Fed Chair; According to a separate report, Treasury Sec Mnuchin is said to have given support to Jerome Powell for the position.

(US) DoubleLine's Gundlach: 2018 will be ' much tougher' market environment; expects liquidity to marginally reverse in 2018 and hurt assets; Says 'no chance' President Trump wants Yellen to continue at Fed; "No way' Gary Cohn will be Fed Chairman.

(US) White House said to be readying request for $29B in disaster aid, flood insurance claims – AP

(US) Rep Jim Jordan (R-Ohio): Confirms expects House to pass budget on Thursday

(US) US President Trump: Puerto Rico's debt will have to be 'wiped out' - US media interview

(KR) North Korea negotiator said to meet former US officials later in Oct - US financial press

(MY) Malaysia expected to amend its tax act to include digital economy - Local Press

Uber: Board said to approve $1.0-1.25B investment from Softbank (implied valuation $69B) and corporate governance reforms; said to set 2019 deadline for IPO - US financial press

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.2%, Hang Seng +0.8%, Shanghai Composite closed, ASX200 -0.7%, Kospi closed

Equity Futures: S&P500 flat; Nasdaq flat, Dax +0.2% , FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1736-1.1780; JPY 112.51-112.91; AUD 0.7830-0.7875; NZD 0.7185-0.7206

Aug Gold +0.3% at 1,278/oz; Aug Crude Oil -0.8% at $50.01/brl; Sept Copper +0.1% at $2.963/lb

GLD SPDR Gold Trust ETF daily holdings -0.6% to 854.3 metric tons

(AU) Australia sells A$700M in April 21, 2027 bonds, avg yield 2.7655%, bid to cover 4.46x

Equities notable movers Japan

Japan Display,6740.JP Japan government backed OLED firm said to consider mass production; +25%

Asahi Group, 2502.JP Expected price increase; +3.3%

US markets on close: Dow +0.4%, S&P500 +0.2%, Nasdaq +0.2%, Russell +0.2% - Best Sector in S&P500: Industrials +0.4%

Worst Sector in S&P500: Utilities -0.3%

At the close: VIX 9.51 (+0.06pts); Treasuries: 2-yr 1.475% (-1bp), 10-yr 2.318% (-1bp), 30-yr 2.868% (flat)

US Market Summary

The benchmark US stock indices all set fresh records today, with the S&P 500 notching its sixth consecutive session of gains in a row. The VIX stayed pinned around 9.5 after Warren Buffett acknowledged Berkshire has avoided making some equity sales in anticipation of potential changes to the tax code next year. Airlines climbed after Delta adjusted its Q3 outlook and reported Sept metrics. Sept auto sales topped expectations, helped by the effect of the hurricanes. Crude prices drifted lower, adding onto yesterday's losses. All sectors were in the green for the day except for real estate and utilities.

US Afterhours Movers - CTMX Announces strategic collaboration with Amgen in Immuno-Oncology; Amgen to make $40M upfront payment and acquire $20M in CytomX stock; +37% afterhours

ODP Announced acquisition and cut FY17 forecast; -8.5%

NLNK Files to sell $50M public offering of common stock (15.6% of market cap); -5.7% afterhours

RIGL Files to sell $40M of common stock via Jefferies and BMO (10% of market cap); -8.7% afterhours

Australia’s Services Sector Growth Slowed In September

For the 24 hours to 23:00 GMT, the AUD traded flat against the USD and closed at 0.7834.

LME Copper prices declined 0.1% or $8.0/MT to $6447.0/MT. Aluminium prices rose 2.3% or $47.5/MT to $2114.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7861, with the AUD trading 0.34% higher against the USD from yesterday's close.

Overnight data revealed that Australia's AiG performance of services index dropped to a level of 52.1 in September. In the previous month, the index had recorded a reading of 53.0.

The pair is expected to find support at 0.7806, and a fall through could take it to the next support level of 0.7752. The pair is expected to find its first resistance at 0.7895, and a rise through could take it to the next resistance level of 0.7930.

Going forward, investors will focus on Australia's trade balance and retail sales data, both for August, slated to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro Trading Higher, Ahead Of The Euro-Zone’s Retail Sales Data

For the 24 hours to 23:00 GMT, the EUR marginally rose against the USD and closed at 1.1742.

On the macro front, the Euro-zone's producer price index (PPI) advanced 2.5% on an annual basis in August, beating market expectations for a gain of 2.3%. The PPI had recorded a rise of 2.0% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1770, with the EUR trading 0.24% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1717, and a fall through could take it to the next support level of 1.1665. The pair is expected to find its first resistance at 1.1801, and a rise through could take it to the next resistance level of 1.1833.

Going ahead, investors will closely monitor the final Markit services PMI for September across the Euro-zone along with the region's retail sales data for August, slated to release in a few hours. Additionally, the US ISM non-manufacturing index, ADP employment change and MBA mortgage applications data, all set to release later today, will pique significant amount of investor attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.