Sample Category Title

USD/CHF Mid-Day Outlook

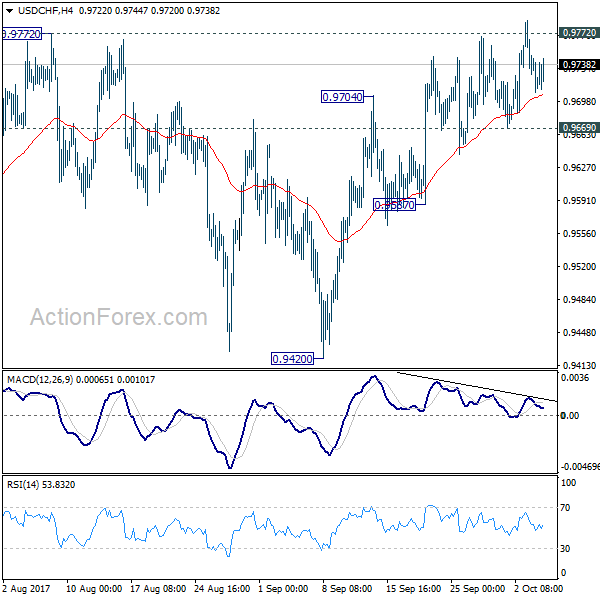

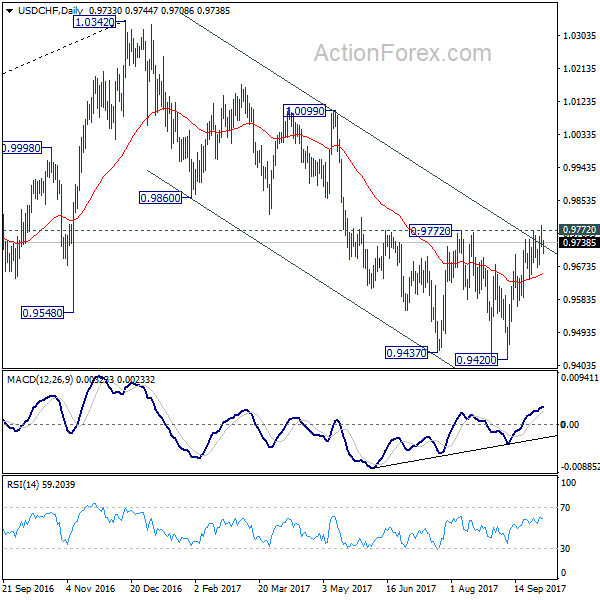

Daily Pivots: (S1) 0.9714; (P) 0.9749; (R1) 0.9771; More....

Intraday bias in USD/CHF remains neutral with focus staying on 0.9772 key resistance. And outlook remains unchanged. On the upside, decisive break of 0.9772 key resistance will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. However, break of 09669 minor support will suggest rejection from 09772 and turn bias back to the downside for 0.9587 support. Break will target retesting 0.9420 low.

In the bigger picture, focus remains on whether 0.9443 key support (2016 low) could be taken out firmly as down trend from 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

Cars the Latest Driver?

Stepping back momentarily from central banks & macro data, could the best month for US automakers since 2005 mean consumers are finding another gear? ADP slowed to 135K in September (meeting expectations) from a revised 228K partly due to the hurricanes. All currencies are up against USD since the close of Tuesday's NY session, with gold and GBP in the lead, CHF and CAD at the bottom. GBP got a lift from better than expected services PMI, keeping alive hopes of a November BoE hike. We turn to the US services ISM at 15:00 and Yellen's speech at 20:15 London time. A new Premium trade has been posted and sent.

US auto sales smashed expectations in September with sales at an 18.57m pace, up from 16.14m in December and beating the 17.4m estimate. Optimists will say consumers are opening their wallets, buoyed by a better jobs market and hopes for a tax cut. Pessimists will sale say that replacements after hurricane Harvey simply took place more-quickly than anticipated.

The Fed's bias is to see good news as real and bad news as temporary so the numbers are more-likely to strengthen the case for a December rate hike, especially because the buying wasn't entirely limited to hurricane-hit areas. Odds of a December Fed hike remain little changed at 70%. Yellen's speech today fires up an avalanche of speeches from Fed members this week (Williams, Harker, George, Bostic, Dudley, Kaplan & Bullard).

S&P 500 hit yet-another record high, climbing 5 points to 2534. NASDAQ is now at 4800.

GOLD Puts In Temporary Bottom, Eyes More Recovery

GOLD - The commodity put in a temporary bottom and triggered a corrective recovery on Wednesday. This development has opened the door for more strength. On the downside, support comes in at the 1,270.00 level where a break will turn attention to the 1,260.00 level. Further down, a cut through here will open the door for a move lower towards the 1,250.00 level. Below here if seen could trigger further downside pressure targeting the 1,240.00 level. Conversely, resistance resides at the 1,280.00 level where a break will aim at the 1,290.00 level. A turn above there will expose the 1,300.00 level. Further out, resistance stands at the 1,320.00 level. All in all, GOLD looks to strengthen further on bull pressure.

Gold Gains Limited as ADP Nonfarm Payrolls Beats Expectations

Gold has posted gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1275.10, up 0.26% on the day. In economic news, ADP Nonfarm Payrolls came in at 135 thousand, but managed to beat the estimate of 131 thousand. Later in the day, the US releases the ISM Nonfarm Manufacturing report, and Federal Reserve Chair Janet Yellen will speak at an event in hosted by the St. Louis Fed.

Gold prices showed some strength earlier on Wednesday, but the metal has retracted in the North American session, in response to the ADP Nonfarm Payrolls report. The key indicator dropped sharply, from 237 thousand in August to just 135 thousand, but this was better than expected. The hurricanes which tore through Texas and Florida caused extensive damage, and with many workers in those states unable to work, the markets were braced for low employment numbers. The official nonfarm payrolls, which will be released on Friday, are also expected to sharply decline in September, with a forecast of 85 thousand, compared to the August release of 156 thousand. Will the official release follow suit and beat the estimate?

Has the Federal Reserve decided to raise rates one final time in 2017? Just a few weeks ago, federal futures had priced in a December hike at below 50 percent, but the odds have surged to 76 percent, according to the latest CME Fed Watch release. Although FOMC members remain divided on the prudence of another rate hike in 2017, Fed Chair Janet Yellen has broadly hinted that she favors a December move, and the markets have picked up on her message. The US economy continues to perform well, and the labor market remains close to capacity. The Achilles heel in an otherwise strong economy is inflation, which remains well below the Fed's target of 2 percent. If sentiment towards a December hike remains high, the US dollar will be attractive to investors and could gain ground.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.56; (P) 112.87; (R1) 113.15; More...

USD/JPY continues stay in tight range below 113.25, around medium term channel resistance. Intraday bias stays neutral at this point. On the upside, sustained break of medium term channel resistance will argue that correction from 118.65 is already completed with three waves down to 107.31. Break of 114.49 will confirm this bullish case and target a test on 118.65 next. On the downside, considering bearish divergence condition in 4 hour MACD, break of 111.46 will suggest rejection from the channel resistance and turn bias back to the downside.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Dollar Stays Soft after ADP Job Report, UK Fails to Ride on PMI Services

Quick update: ISM services came in higher than expected. But Dollar's reaction is muted.

Dollar remains generally soft today after job data comes in slightly below expectation. ADP report shows 135k growth in private sector jobs in September, slightly below consensus of 140k. Prior month's figure was revised from from 237k to 228k. For the week, the greenback is trading as the second strongest, next to Aussie. But it's pointed out in out earlier report that Dollar struggles to power through key near term resistance against Yen, Swiss Franc and Aussie. Elsewhere, Sterling attempts a recovery after better than expected PMI services but there is no follow through buying seen. In other markets, Gold is trying to regain 1280 after dipping to as low as 1271 earlier this week. WTI crude oil is trying to dry support from 50 after last week's steep selloff.

Outgoing Fed Vice Fischer: We will have higher inflation

Out-going Fed Vice Chairman Stanley Fischer said that the current soft batch of inflation data will not last. And "we will have higher inflation" as wages will rise "at some stage". Fischer declined to comment on who he prefers as the next Fed chair after Janet Yellen's term expires next year. Fischer said that it's a "choice clearly of the president and the administration". Nonetheless, he also noted that Fed chair should have "the flexibility of mind to see that he or she needs to take a different route at a particular moment in time or over the next year or two." It's believed that US President Donald Trump has met four candidates already, including Yellen, chief economic advisor Gary Cohn, Fed Governor Jerome Powell and former Fed Governor Kevin Warsh. Standford University economist John Taylor is reported to be in the short list too.

UK PMI services beat expectation

UK PMI services rose to 53.6 in September, up from 53.2 and above expectation of 53.2. Markit noted that "service providers commented on subdued business-to-business sales and delayed decision making on large projects in response to Brexit-related uncertainty." And, "the net balance of survey respondents anticipating a rise in business activity over the next 12 months was the lowest since June, meaning that business confidence remained close to its weakest since the end of 2011." Also from UK, BRC shop price index dropped -0.1% yoy in September.

S&P sceptical on BoE rate hike

Rating agency S&P said it's "a bit sceptical" that UK economy justifies an interest rate hike soon. And it noted in a statement that "Overall, we believe the Bank and Mark Carney's recent statements are primarily aimed at propping up sterling to reduce imported inflation pressures. This strategy may include an actual 25 basis point hike in November, thus bringing the policy rate back to where it was before the Brexit referendum. Additional moves in 2018 do not appear warranted on the back of a slowing economy." Meanwhile, S&P also warned that there is a high risk of a disruptive Brexit with "tangible lack of progress" and ongoing "infighting within the UK political establishment.

MEP voted to delay trade negotiations with UK

Members of the European Parliament voted to delay trade discussions with UK until there is a "major breakthrough" in the negotiation. The motion was backed by 557 MEPs, with 92 against and 29 abstained. While the vote was not binding, it did show the united stance among EU officials on the issue. And, some EU officials are clearly dissatisfied with the way UK is taking the negotiations. The Parliament's chief Brexit spokesman Guy Verhofstadt blamed the open splits among UK officials for the of progress. He pointed out that "there are differences between Hammond and Fox... and Johnson and May."

ECB Nowotny: Aiming for cautious normalization of polices

ECB Governing Council member Ewald Nowotny said that policymakers are "aiming for the prospect of a cautious normalization" of monetary policies. And he explained that "Caution means not hitting the brakes abruptly, but slowly taking your foot off the pedal." And added that "not only with cars but also with central banks, there is the problem of braking distance - and therefore I think it is wise to drive at a safe distance, but to react quickly to problems as they arise." He also acknowledged that inflation has stayed below 2% target for some time and there were debates on whether Eurozone is now in a long period of low inflation. He also noted that " it is not so easy to explain to the public why an inflation rate of 1.5 percent is so much worse than an inflation rate of 1.9 percent."

Catalonia could declare independence early next week

In Spain, Catalan President Carles Puigdemont said he would ask the region's parliament to declare independence after finishing counting the votes of the independence referendum. He noted that "this will probably finish once we get all the votes in from abroad at the end of the week and therefore we shall probably act over the weekend or early next week." Meanwhile, Spanish High Court launched an investigation against top Catalan police and referendum organizes for inciting rebellion against the state. Head of Catalonia's regional police Josep Lluis Trapero is included in the probe. Yesterday, Spanish King Felipe VI criticized that Catalan leaders have broken the law of the stat and showed and "inadmissable lack of loyalty."

Released from Eurozone, retail sales dropped -0.5% mom in August. Services PMI was revised up by 0.2 to 55.8 in September.

BoJ Nakaso: Could incur red ink during stimulus exit

Bank of Japan Deputy Governor Hiroshi Nakaso said that during the exit of monetary stimulus, the BoJ could incur "red ink". But he expressed his confidence that "short-term fluctuations in the BOJ's revenues won't disrupt our policy-making." And, the central bank could learn from Fed's experience on tapering of quantitative easing. Meanwhile, Nakaso also urged the government to take a "balanced" approach on fiscal policies and emphasized that "it's important to create a sustainable fiscal framework in Japan." This was seen as a response to Prime Minister Shinzo Abe's plan to delay the target of reaching primary budget surplus by a few years.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.56; (P) 112.87; (R1) 113.15; More...

USD/JPY continues stay in tight range below 113.25, around medium term channel resistance. Intraday bias stays neutral at this point. On the upside, sustained break of medium term channel resistance will argue that correction from 118.65 is already completed with three waves down to 107.31. Break of 114.49 will confirm this bullish case and target a test on 118.65 next. On the downside, considering bearish divergence condition in 4 hour MACD, break of 111.46 will suggest rejection from the channel resistance and turn bias back to the downside.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Sep | -0.10% | -0.30% | ||

| 07:45 | EUR | Italy Services PMI Sep | 53.2 | 55 | 55.1 | |

| 07:50 | EUR | France Services PMI Sep F | 57 | 57.1 | 57.1 | |

| 07:55 | EUR | Germany Services PMI Sep F | 55.6 | 55.6 | 55.6 | |

| 08:00 | EUR | Eurozone Services PMI Sep F | 55.8 | 55.6 | 55.6 | |

| 08:30 | GBP | Services PMI Sep | 53.6 | 53.2 | 53.2 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | -0.50% | 0.30% | -0.30% | |

| 12:15 | USD | ADP Employment Change Sep | 135K | 140K | 237K | 228K |

| 13:45 | USD | Services PMI Sep F | 55.3 | 55.1 | 55.1 | |

| 14:00 | USD | ISM Services/Non-Manufacturing Composite Sep | 59.8 | 55.5 | 55.3 | |

| 14:30 | USD | Crude Oil Inventories | -6.0M | -0.5M | -1.8M |

EUR/USD Downward 4 Hour Channel is Broken

The EUR/USD is trying to break the downward PPR channel and at the same time push above the AP channel. I am favoring a bullish bias as long as 1.1692 holds as I previously analysed in the EUR/USD analysis. If bullish scenario persists 1.1822 is the target followed by 1.1873 and 1.1916. Of course, for that to happen bullish momentum needs to be strong. 4h close above each important level is needed for the price to stair-step to next level (1.1822-1.1873-1.1916) The bullish bias is accompanied by a bullish divergence within the POC zone 1.1750-80. Have in mind this is a completely counter trend outlook.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 - Daily Camarilla Pivot (Daily Support)

D L4 - Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

UK Services PMI Lifts Pound off 3-Week Lows but Growth Lags Eurozone

Manufacturing and services PMI released in the UK this week indicate the British economy continues to expand at a moderate pace, easing concerns of a sharper slowdown or a recession as the Brexit uncertainty bites on growth. However, when put against the backdrop of a weaker sterling and accelerating growth elsewhere in the world, notably the Eurozone, recent UK economic data leaves much to be desired.

Data out on Monday showed the IHS Markit/CIPS manufacturing PMI eased to 55.9 in September from a downwardly revised 56.7 in August. Forecasts were for a smaller decline to 56.4. Although the figure remains comfortably above the 50 mark which separates expansion from contraction, it points to a loss of momentum. In contrast, the Eurozone's manufacturing PMI rose to a 6½-year high of 58.1 during the same period. However, there were a number of positives in the PMI report, such as solid growth in output, new orders and exports.

The services PMI released today surprised to the upside, coming in at 53.6 in September, beating expectations that it would stay unchanged at 53.2. While the positive figure provided an immediate boost to the pound, which jumped to $1.3285 in forex markets after the data, from a session low of $1.3242, it does little to change the near-term outlook for the UK economy. The index has averaged 53.5 in the past three months compared to 54.3 in the second quarter, suggesting growth failed to pick up in the third quarter. Today's report also highlighted that new business growth was at its lowest in 13 months, while input costs continued to rise, putting pressure on operating expenses.

Construction was the worst performing sector among the three gauged by IHS Markit, with the PMI missing expectations of 51.0 to drop to 48.1 in September from the prior 51.1, according to yesterday's data. This was the first drop in construction activity in 13 months and the lowest reading since July 2016. Uncertainty over Brexit was blamed for the sharp drop in civil engineering work, which fell at its steepest pace since April 2013. New business orders were also down, with house building being the only bright spot.

The UK's combined composite PMI fell to a seven-month low of 53.6 in September, underscoring the sluggishness in the economy and raising doubts about the Bank of England's well signalled plans to raise rates in November. While it could be argued that the British economy's resilience is impressive given the strong headwinds being generated by Brexit, the loss of potential output is also significant, which is perhaps best accentuated by the performance of the Eurozone economy.

IHS Markit's composite PMI for the Eurozone rose to a four-month high of 56.7 in September, driven by strong growth in Germany, Ireland, France and Spain. The euro fell to 0.8850 pounds after today's strong UK services PMI, reversing the small gains made a short while earlier from the release of the Eurozone PMIs. However, despite having retreated by about 4.7% from August's 10-month highs due to sterling's BoE-led rally, the euro remains up 4% in the year to date against the British currency on the back of the diverging outlook for the two economies.

EURO Stoxx 50 Index Overbought But Still Bullish

The Euro Stoxx 50 index surged to a 2 ½-month high of 3612.36 on October 3, retracing more than 70% of the downtrend it recorded from May 8 to August 29. Technical indicators signal a bullish picture both in the short and the medium term. However, the index might continue stretching its current red candle during the day as the index is overbought.

According to the RSI and the MACD oscillators, the bias in the short term is bullish, with the former being above 50 and the latter above zero and its signal line. Still, a risk to the downside remains high as the RSI is pointing to the downside in an overbought area (above 70), while the MACD has slowed down. Moreover, the Ichimoku analysis also hints a positive structure as the index is located above the Ichimoku cloud and the bullish cross between the Tenkan-sen and the Kijun sen is still intact.

Should the index head downwards, an immediate support could be met at the 61.8% Fibonacci of 3561.09 of the downtrend from 3683.53 to 3360.55 (May 8- August 29), a level tested repeatedly between May and June. From here, further declines would target the 50% Fibonacci of 3522.75. If this comes into view then the bullish phase would turn into neutral. Another barrier also could be found at the 23.6% Fibonacci of 3436.81.

In case the index hits up, an immediate resistance would be the 2 ½-month high of 3612.36 reached yesterday before the index turns higher towards the top of 3683.53 seen on May 8. Additional extensions to the upside would shift focus to the April's 2015 high of 3835.20.

Looking at the medium term, the outlook has switched from bearish to bullish after the 20-day exponential moving average crossed above the 50-day exponential moving average on September 19.

Sterling Claws Back Losses, ADP in Focus

Sterling received a lifeline on Wednesday, after UK services unexpectedly accelerated in September, easing some concerns over the health of the economy.

The Purchasing Managers' Index for the UK's services beat market estimates in September, rising to 53.6 from August's 53.2. While the rebound in services is encouraging and may support expectations for higher UK interest rates, some fears still linger over the cooldown in manufacturing, and contraction in construction. Sentiment towards Sterling remains fragile despite today's appreciation; with prices destined to dip lower as Brexit-fueled uncertainties continue, this could repel investor attraction towards the currency.

Speaking of uncertainty, the lack of progress in the Brexit talks has left market players anxious. This anxiety can be reflected in the Sterling's overall price action, with the GBPUSD currently trading below 1.3300 as of writing. Taking a look at the currency from a technical perspective, prices are still depressed on the daily charts. Previous support around 1.3300 could transform into a dynamic resistance that results in a further decline towards 1.3150.

Dollar lower ahead of ADP

The Greenback depreciated slightly against a basket of major currencies on Wednesday, ahead of the US ADP private sector jobs data and ISM non-manufacturing PMI for September.

Economists have forecasted that ADP will rise by 131k in the month of September, after an initial print of 237k in August. The negative impact of Hurricanes Irma and Harvey are likely to add some random ingredients into the mix and as such, could result in a weaker jobs print.

Technical traders will continue to closely observe how the Dollar Index behaves, before and after the ADP release this afternoon. A disappointing figure may encourage short term bears to target 93.00. In an alternative scenario, a daily close above 93.70 should open a path back towards 94.00.

Commodity spotlight – WTI Crude

WTI Crude was under noticeable selling pressure this week as investors started to question the sustainability of an oil rally, which lasted for a fair chunk of the third quarter.

Market players who were itching for an opportunity to send the commodity lower, received permission on Tuesday, after US industry estimates on inventories were a mixed bag. US Crude oil inventories declined by 4.08 million barrels last week, while the API reported on Tuesday that Gasoline supplies rose by 4.91 million barrels. However, Gasoline supplies rose by 4.91 million barrels and this rekindled some oversupply concerns.

Investors will continue to closely watch for signs on whether OPEC will extend their production cuts beyond the current expiry date of March 2018. While an extension of the deal may support oil prices, this could encourage US Shale producers to increase production. As the final trading quarter of 2017 gets underway, Oil markets are likely to be exposed to downside risks, if rising production in the United States obstructs OPEC's efforts to rebalance the saturated markets.

Focusing on today, the Energy Information Administration (EIA) report will be in the spotlight and could compound oil's downside, if it follows the same pattern as yesterday's API report.

From a technical standpoint, WTI Crude is under assault by sellers on the daily chart. Sustained weakness below $50 may encourage a further decline towards $49.50 and $48.50, respectively.