Sample Category Title

Sombre Start

Sombre Start

Finding the desire to discuss forex markets this morning in the wake of the worst mass shooting in US history is a challenge.

But with heavy hearts, the global markets trudge on searching for opportunities realising these tragedies are becoming all too commonplace. And as cynical as that may seem, that is the reality we've come to accept.

Markets

Peering at the screens this morning, it's apparent that US yields are providing the primary catalyst for the USD revival.

But the deep-seated tension in Spain is certainly weighing on the view that European political risk has faded, by all accounts anti-establishment populism is alive and well.

While the market is likely to sidestep the restlessness in Catalan, the short-term picture for EU risk remains clouded.Expect short-term EUR bulls to take the sidelines limiting top side appeal ahead of this weeks ECB meeting.Speaking of which, the ECB could present some challenges for them as the central bank is apt to show some concern about the EURO's recent strength.

And while the footings are solid to anchor the USD ( US tax reforms, a new Fed governor, Hawkish Fed) if price action is telling us anything, the dollar bulls remain tentative and appear almost uncomfortable to hold long positioning. Even a juicy good ISM manufacturing print overnight failed to get a rise form dollar bulls.

Indeed, the markets ingrained scepticism regarding Fed policy along with political challenges in Washington continues to temper expectations. But the reality is the Fed rate hikes( 2017-2018) remain underpriced as speculation continues to swirl around the shift to a Hawkish Fed Chair.

The Reserve Bank of Australia is on tap later today but it would be out of the ordinary if they lit off any hawkish fireworks. Recent RBA rhetoric runs counter to interest rate normalisation.Governor Lowe has continued to dampen any market expectation that more hawkish stance by global central banks does not necessarily have pass through implication in Australia. With CPI still below RBA target, there's not much risk for the RBA to nudge rates higher anytime soon.

IN the Asia FX space we should expect currency markets to remain in flux until global yields stabilise and regional equities see increased inflows. Mainland holiday thinned-trading conditions are also weighing on sentiment. Overall the market remains nervous on the INR and KRW but are showing some small pockets of interest int CNH and MYR at current levels

Views

USD: Longs remain uncomfortable awaiting the next bullish signal.It's difficult to read too much in this weeks NFP given the expected hurricane effect, but an aggressive top side surprise could send the dollar bulls into a frenzy

EUR: Expect limited fallout from the chaos in Catalan, but this weeks ECB risk will contain any rally

JPY: Tough trade gave the Japanese election risk and as you can tell traders are respecting current ranges

AUD: Remains extremely susceptible the to a dovish RBA

USD/CAD Canadian Dollar Lower Despite Strong PMI Data

Stronger US PMI Data and Geopolitics overshadowed Loonie

The Canadian dollar began the week under pressure against the US dollar. The lonnie failed to appreciate versus the greenback despite a strong manufacturing sector report in September. The Markit Canada Manufacturing Purchasing Managers index (PMI) rose to 55 from a previous 54.6 in August. Released half an hour later the US Institute for Supply Management PMI jump to 60.8, the fasted pace in 13 years. The leading indicator boosted the USD as a strong pace of growth would lead to a third interest rate hike by the U.S. Federal Reserve.

Following a mixed third round of NAFTA talks in Ottawa last week the US is back to business by filing a trade complaint over the sale of Canadian wine in retail shops. The US Commerce department also slapped a 200 percent tariff on Bombardier CSeries jets. The actions taken into context have almost eroded any possibility of NAFTA negotiations finishing this year. The US and Mexico want to avoid the matter from dragging into 2018 as it is an election year (presidential in Mexico and primaries in the US).

The CAD got little support from oil prices on Monday. Energy prices tumbled more than 2 percent with reports of higher output from Iraq and Lybia at the same time US drillers and refineries recovered from the tropical storms.

The USD/CAD gained 0.263 on Monday. The currency pair is trading at 1.2504 after the US currency appreciated on the back of rising anticipation of a third interest rate hike this year. Geopolitics were a major factor over the weekend as the Catalunya referendum is reducing confidence in the EUR after the Spanish government cracked down on voters. The single currency has survived two close calls after the French and German elections, but stability of the region is once again in question after this weekend’s events.

U.S. Federal Reserve and Federal Open Market Committee (FOMC) voting member Neil Kashkari continues to be a dove. He has dissented from raising rates in the last two votes and in his view the current monetary policy tightening is keeping inflation down. He would rather wait for inflation to pick up to the 2 percent target before pulling the trigger on another interest rate hike. Dallas Fed President Robert Kaplan was more moderate and is willing to be convinced by upcoming indicators if he is to vote for a rate hike in December. Kaplan did mention that while the Fed has room to raise rates, it might not be as much as people might think.

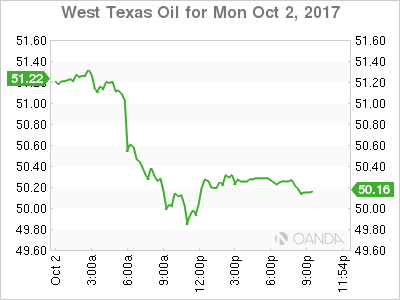

Energy prices fell 2.055 percent in the last 24 hours. West Texas Intermediate is trading at 50.24 after news of higher supply from Organization of the Petroleum Exporting Countries (OPEC) and US based operations. The disruptions due to tropical storms in the US are slowly working themselves out and the geopolitical situation in Northern Iraq has not affected global supply. Iraq in fact announced a rise in exports in September. Risks remain that the situation could escalate as the Kurdish region has voted for independence but lacks the recognition of the central government.

Market events to watch this week:

Tuesday, October 3

4:30 am GBP Construction PMI

Wednesday, October 4

4:30 am GBP Services PMI

8:15 am USD ADP Non-Farm Employment Change

10:00 am USD ISM Non-Manufacturing PMI

10:30 am USD Crude Oil Inventories

3:15pm USD Fed Chair Yellen Speaks

8:30 pm AUD Retail Sales m/m

8:30 pm AUD Trade Balance

Thursday, October 5

8:30 am CAD Trade Balance

8:30 am USD Unemployment Claims

Friday, October 6

8:30 am CAD Employment Change

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

Gold Dips To 6-Week Low As ISM Manufacturing PMI Hits 6-Year High

Gold has posted slight losses in the Monday session. In North American trade, the spot price for an ounce of gold is $1275.52, down 0.34% on the day. On the release front, ISM Manufacturing PMI accelerated to 60.8, beating the forecast of 57.9. This marked the indicator’s highest level since April 2011.

The US manufacturing sector remains strong, as a stronger global economy has led to increased demand for US goods. The primary gauge of manufacturing activity, ISM Manufacturing PMI, accelerated in September to 60.8, indicating sharp expansion. The strong reading increased has sent gold prices lower on Monday. September was a rough month for gold, which declined 3.2 percent. With the North Korean conflict again on the back burner and the US continuing to post strong numbers, investors have a renewed appetite for riskier assets, which has weighed on safe-haven gold.

The US dollar gained some ground last week from an unexpected source – President Donald Trump. Trump has all but given up on his health care proposal, as the plan lacks enough support from Republican lawmakers. Next on the Trump Express is tax reform, which was a key campaign plank. Last week, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 35 percent to 20 percent, as well as a 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump’s tax agenda, it’s likely his that tax reform proposal will face a stiff battle in Congress. Still, the markets like the idea of lower taxes, and this has helped the dollar gain ground against gold.

Pound Slips as British Manufacturing PMI Disappoints

The British pound has recorded considerable losses in the Monday session. In North American trade, GBP/USD is trading at 1.3267, down 0.97% on the day. On the release front, British Manufacturing PMI slowed to 55.9, but still fell short of the forecast of 56.3 points. There was better news in the US, as ISM Manufacturing PMI accelerated to 60.8, beating the forecast of 57.9. This was the indicator's highest level since April 2011. On Tuesday, the UK releases Construction PMI, which is expected at 51.2 points. As well, the BoE will release the minutes of the quarterly Financial Policy Committee meeting.

With investors keeping a nervous glance on the slow pace of the Brexit negotiations, any key British indicators which fall short of expectations could send the pound sharply lower. This was the case on Monday, as British Manufacturing PMI softened and missed the forecast. Although the reading of 55.9 indicates respectable expansion in the manufacturing sector, perception is key in the markets, and negative sentiment about the British economy could spell trouble for the pound.

Prime Minister Theresa May is putting on a brave face, and said in a weekend BBC interview that the Conservative party is united behind her leadership. However, there are reports that May is facing increasing unrest in the party, and could be gone as leader within 12 months. The Conservatives are gathered this week in Manchester for a party gathering. May has been widely blamed for the Conservative's poor showing in the June election, and has failed to present a consistent line in the Brexit negotiations with the European Union. The Brexit talks have been tortuous until now, with little progress to report after several rounds of negotiations. Key sticking points include the amount that Britain will pay upon leaving, whether the European High Court will have jurisdiction over EU citizens living in Britain, and the border with Ireland.

The US dollar continues to gain ground against the pound, as GBP/USD has dropped to its lowest level since September 14th. Trump has all but given up on his health care proposal, as the plan lacks enough support from Republican lawmakers. Next on the Trump Express is tax reform, which was a key campaign plank. Last week, Trump proposed a major overhaul of the US tax code, which includes reducing the corporate tax rate from 35 percent to 20 percent, as well as a 25 percent tax rate for small businesses, such as partnerships. Like other Trump proposals, the tax plan was sketchy on details, including how the tax plan would be paid for. With Democrats and some Republicans wary of Trump's tax agenda, it's likely his that tax reform proposal will face a stiff battle in Congress. Still, the markets like the idea of lower taxes, and the US dollar posted back-to-back weekly gains.

ISM Manufacturing: Factory Sector Rides Out Recent Storms

Manufacturing activity picked up in September with the ISM index notching its highest reading this cycle. Some of the gain can be traced to the effects of recent storms, but details suggest more fundamental strength.

Longer Delivery Times Support New Cycle High for the ISM

The ISM manufacturing index backed up a solid report in August with another standout reading in September. The composite index rose to a cycle high of 60.8. The gain in part looks to reflect some of the fallout of Hurricanes Harvey and Irma, but the breadth of strength suggests factory activity remains solid.

Among the composite's sub-indices, supplier deliveries posted the largest gain, jumping 7.3 points to 64.4. Disruptions from the Gulf area storms have caused delivery times to lengthen. The bottle necks have extended beyond the chemicals industry, with respondents from the paper products and food, beverage & tobacco industries also reporting storm-related supply issues.

That said, supplier deliveries have been lengthening over the year, consistent with improving manufacturing activity. The production index notched its fourth consecutive month of above-60 readings, rising to 62.2. Moreover, the new orders index improved to 64.6 and suggests strength is set to continue over at least the next couple of months.

Manufacturers have been adding to inventories to meet growing demand. The inventory index came in at 52.5, closely in line with its average for the quarter. As we have been noting, inventories look set to provide a sizeable boost to third quarter GDP. Although much of the "hard" data on inventories has yet to come available, the ISM signals the strongest quarter of inventory building at the nation's factories in more than two years. Moreover, the buildup appears intentional, as customer inventories were reported as too low for a third consecutive month.

One area where hurricane effects were clear was in prices. The prices paid index jumped to 71.5 in September with multiple respondents specifically citing higher input costs due to the recent storms.

Factory Hiring Remains Solid

Hiring in the manufacturing sector has been solid this year as the industry has shaken off last year's commodity slump, the dollar has weakened and global growth has strengthened. Manufacturing payrolls have risen by an average of 17,100 jobs per month.

The ISM employment index points to continued strength for September. The hiring index edged up from an already elevated reading to 60.3. The solid pace of hiring in recent months suggests that longer supplier delivery times are not solely due to temporary weather disruptions. We look for the factory sector to add to payroll growth in Friday's employment report, but note that hiring disruptions due to the recent hurricanes generate the potential for readings that may not be indicative of the underlying trend in factory hiring.

U.S. Manufacturing Activity Strengthens Further in September Despite Hurricane Harvey Supply Chain Disruptions

The Institute for Supply Management (ISM) manufacturing index rose 2 points to 60.8 in September, the thirteenth consecutive monthly expansion and achieving a cycle high. Market consensus expected a pullback to 58.1.

All components except inventories (-3 points to 52.5) and imports (-0.5 to 54) advanced in the month. The biggest gains were recorded in prices paid (+9.5 to 71.5), supplier deliveries (+7.3 to 64.4), and new orders (+4.3 to 64.6).

Growth in new orders coupled with decline in inventories results in the spread between the two - useful as a leading indicator of activity - rising to 12.1 (+7 points). This suggests that activity could hold or strengthen in coming months.

Seventeen of the eighteen manufacturing industries reported expansion in September, with textile mills, machinery, and nonmetallic mineral products registering the strongest expansions on the month. The furniture and related products industry recorded a contraction in September.

Key Implications

For the second consecutive month, the U.S. manufacturing sector has beaten expectations, bolstered by strength across 9 of 11 categories. The surge in prices is likely a temporary phenomenon, and appears to be largely driven by supply chain disruptions in the aftermath of hurricane Harvey.

Rebuilding from hurricanes is likely to support manufacturing activity in the next few months, suggesting that there may be some inertia in components such as new orders and production before we see the index pull-back to more sustainable levels. Nevertheless, this report sends a strong positive signal that the U.S. manufacturing sector continues to prove resilient, supported by strong foreign demand that is helping to offset domestic concerns about policy uncertainty, dollar movements, or natural disasters.

Oil Production Growth in OPEC Pulls Down the Quotes

The market's attention today was on the referendum in Catalonia where most of the voters supported independence of the region from Spain. The Spanish government claimed the referendum as illegal and as a result of attempts by authorities to restrict people from voting, more than 800 people have been injured. In case of a continuation of this political crisis, the euro may weaken against other major currencies. Further pressure for EUR/USD bulls came from the final manufacturing PMI in the US that declined to 58.1 in September, 0.1 less than the previous figure. The unemployment rate in the Eurozone stayed at 9.1% in August against the forecasted decline to 9.0%.

We may see volatility grow for the AUD/USD after the RBA's monetary policy statement due to be published at 03:30 GMT tomorrow. Most analysts are not expecting any changes in monetary policy settings, but the rhetoric of the central bank's officials may influence the mood of traders. In previous statements, GDP was slated to grow by 3.0% in 2018 and positive forecasts were made for the labour market. The course of trading may also be affected by reports on new home sales at 00:00 GMT and building approvals in Australia at 00:30 GMT.

Oil prices are falling on the background of rising drilling activity in the US where the number of active oil rigs, according to Baker Hughes, increased by 6 to 750 during the last week. At the same time, oil production growth in Iraq and Libya resulted in crude oil production growth within OPEC to 32.86 million barrels per day in September, and that is also negative for the oil bulls.

EUR/USD

The single currency is trying to restore some of the previously lost positions and is currently above 1.1750. Fixing below this figure may become a trigger for continued price drops to 1.1620 and 1.1550. On the other hand, potential growth within the correction may be restricted by resistance at 1.1825. Crossing the zero point by the MACD signal line may provide additional stimulus for growth.

AUD/USD

The AUD/USD price rebounded from the support at 0.7800 and in case of saving the positive momentum we may see the quotes returning to the resistance range of 0.7850-0.7870. In case of continued falls within the limits of the channel, immediate targets will be located at 0.7740 and 0.7700. The recent crossing of the zero point by the MACD signal line may stimulate the bulls to push the price higher today.

USD/WTI

The American crude oil benchmark WTI demonstrated a confident descending movement where it may test the strong support at 50.00. Breaking through this psychologically important mark may become a trigger for further falls to 48.50 and 47.75. On the other hand, the RSI on the 15-minute chart is in the oversold zone that points to an increased possibility of a price rebound with the first target at 51.00.

Dollar Strengthens after Manufacturing PMI Beat; Pound Hits Three-Week Low as Manufacturing Industry Slows

The dollar continued its rally during the European session and managed to peak at a two-week high against its major peers following upbeat manufacturing PMI releases, although a music festival in Las Vegas turned into the deadliest mass shooting in US history. However, gains from positive data were short-lived following dovish remarks by the Minneapolis Fed President Neel Kashkari. The UK manufacturing PMI numbers failed to provide support to the pound, which was one of the worst performing currencies relative to the dollar during the day, hitting a three-week low.

The US ISM manufacturing PMI for the month of September surprised to the upside, with the index touching a six-year high of 60.8 instead of falling by 0.8 points to 58.0 as analysts projected. Manufacturing indices for new orders, employment and prices also came in better than expected.

However, a dovish speech by the Minneapolis Fed President, Neel Kashkari, pushed immediately the dollar index lower from a two-week high of 93.49 touched earlier. Kashkari claimed that the Fed's policy was responsible for the weaker inflation and not transitory factors, while he added that policymakers should wait for price growth to reach the Fed's 2% target before raising interest rates.

The dollar index was last trading at 93.35. Dollar/yen was up at 112.68.

The euro gained some ground against the greenback in the session but remained 0.57% down on the day at $1.1745 after a violent independence vote in Spain's Catalonia region on Sunday exacerbated political risks in the eurozone. The ballot, which was declared illegitimate by the Spanish government, showed that 90% of the votes were in favor of breaking away from Spain.

In terms of data out of the eurozone, the Markit Manufacturing PMI slipped below expectations to 58.1 in September, while analysts anticipated the figure to remain steady at 58.2. Nevertheless, the index held at six-year highs, highlighting the strength of the manufacturing sector. Eurozone's unemployment rate stood flat at 9.1%, but forecasts were for the rate to inch down to 9.0%.

In the UK, the Finance Minister, Philip Hammond, speaking at his Conservative party annual conference starting today (expected to conclude on October 4), argued that Britain must accelerate Brexit talks and offer at least a two-year transition period for businesses to adjust in order to mitigate short-term risks arising from the process. However, the pound could not gain on Hammond's words as worse-than-expected Markit/CIPS manufacturing PMI readings released earlier weighed on the currency. The index dropped from the downwardly revised 56.7 to 55.9, while projections were for the figure to slip to 56.4.

Pound/dollar reached a three-week low of 1.3274, while euro/pound surged to a one-week high of 0.8867 before falling to 0.8847.

The aussie rebounded to 0.7829 ahead of the RBA policy meeting on Tuesday where policymakers would likely keep rates steady at a record low of 1.5%.

In energy markets, WTI crude oil retreated to a one-week low of $50.19 per barrel, while Brent declined to $55.49 as uncertainties around a rising US oil production and Chinese crude imports rose. An IEA market analyst said on Friday that even if the OPEC production remains constant, the agency does not see any "big draw in OECD crude inventories over the next 6-9 months", as it expects US production to increase by 1.1 million bpd. Moreover, he expressed concerns over a rising crude demand in China, where imports have already offset part of crude inventory reductions elsewhere.

The loonie found support on September's RBC manufacturing PMI numbers, which increased to 55.0 from 54.6 in the previous month, standing at three-year high levels. Though the commodity-linked currency was still 0.24% down on the day, weighed by declining oil prices, with dollar/loonie rising to 1.2494.

Euro and Pound Underperform on Heightened Political Worries

Just a week after an indecisive general election outcome in Germany threatened to derail the euro rally, a separatist vote in Spain's Catalonia region on Sunday has further dampened sentiment for the single currency at the start of trading in the fourth quarter. The pound has also started the new quarter on a weak note as uncertainty about the UK's Brexit strategy and doubts about Theresa May's fragile government have pulled sterling below the key $1.33 level.

An attempt by the Spanish government to disrupt and prevent an independence referendum in the Spanish region of Catalonia by sending in riot police has failed to quell the situation. The regional government said almost 90% of the 2.26 million people who voted yesterday backed independence. Catalonia's president, Carles Puigdemont, said he will send the results, once finalized, to the Catalan parliament, which will then have 48 hours to declare independence from Madrid.

However, Spain's Justice Minister, Rafael Catala, said today the Spanish government will do "everything within the law" to prevent the secession of the region, while the European Commission has described it as "an internal matter for Spain" given that the referendum was illegal under Spanish Law. Apart from the vote being unconstitutional, a low turnout of just over 42% also casts doubt about its legality, not to mention that about 770,000 votes were lost due to ballot boxes being seized by the police.

The euro headed back towards last week's more than one month-low of $1.1715 in European trading today, as the latest political troubles added to the uncertainty emerging from the German election result. German Chancellor Angela Merkel's CDU/CSU party gained a fewer share of the vote on September 24's general election, forcing her into possibly prolonged coalition talks with two smaller parties.

However, despite the negative developments, reaction in financial markets has been fairly contained as few believe the referendum will lead to Catalonia's independence from Spain. The vote is unlikely to be recognized by the Spanish government, which has threatened to suspend autonomy to the regional parliament if local politicians press ahead with declaring independence.

In Britain, politics also looks set to dominate the week's headlines as the ruling Conservative party hold their annual conference. The UK finance minister, Philip Hammond, today admitted publicly that there were "differences of view" within the cabinet regarding what type of relationship Britain should have with the European Union post-Brexit. He was critical of the foreign minister, Boris Johnson, who in recent days has been breaking ranks with the government's official position on Brexit.

Johnson's actions have fuelled speculation he may challenge the Prime Minister, Theresa May, for party leadership, which could risk a fresh snap general election given the Conservatives' lack of majority in parliament. Adding to the political headaches for May, is the growing criticism by British businesses of the government's handling of Brexit, particularly about the lack of clarity and slow progress in the negotiations. Businesses are demanding a long transition period of possibly up to three years once the UK leaves the EU so as to smoothen the exit process and to lessen some of the uncertainty.

The pound slid to a 2½-week low of $1.3255 on Monday, losing almost 3% of its value from the 15-month high of $1.3645 set on September 20.

GBPJPY Taking Clearer Direction after Triple-Doji

The cross is taking clearer direction after triple-Doji on Strong bearish acceleration on Monday. Fresh weakness broke below psychological 150 support and dented support at 149.65 (Fibo 23.6% of 139.30/152.85 ascend. Daily RSI reversed from overbought territory and shows plenty of room for further downside, with close below 149.65 seen as bearish signal for extension towards initial support at 149.00 (4-hr cloud base), followed by former tops at 148.10/147.77 (10 May/11 July) and pivotal 147.67 support (Fibo 38.2% retracement). Broken 10SMA (150.94) and 4-hr cloud top (151.15) should cap recovery attempts.

Res: 150.00; 150.96; 151.15; 151.60

Sup: 149.00; 148.10; 147.67; 146.43