Sample Category Title

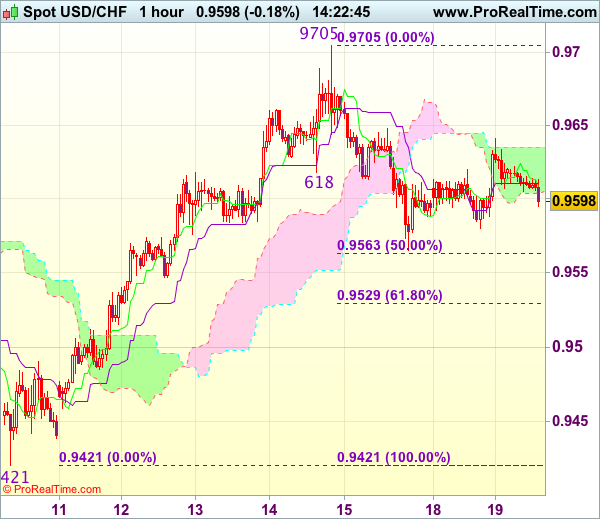

Trade Idea : USD/CHF – Sell at 0.9625

USD/CHF - 0.9599

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9609

Kijun-Sen level : 0.9611

Ichimoku cloud top : 0.9635

Ichimoku cloud bottom : 0.9609

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9625, Target: 0.9525, Stop: 0.9660

Position : -

Target : -

Stop : -

The greenback only recovered to 0.9641 (just missed our short entry at 0.9645) before retreating, bearishness remains for another test of 0.9563-65 (50% Fibonacci retracement of 0.9421-0.9705 and Friday’s low) would extend weakness to 0.9525-30 (61.8% Fibonacci retracement), however, downside should be limited to 0.9500 and 0.9480-85 should hold from here.

In view of this, we are looking to sell dollar again on minor recovery as 0.9625-30 should limit upside. Above 0.9648 would defer and risk rebound to 0.9675-80, break there would signal the pullback from 0.9705 has ended, bring retest of this level, a breach of this last week’s high would extend recent rise from 0.9421 to 0.9740-50 later.

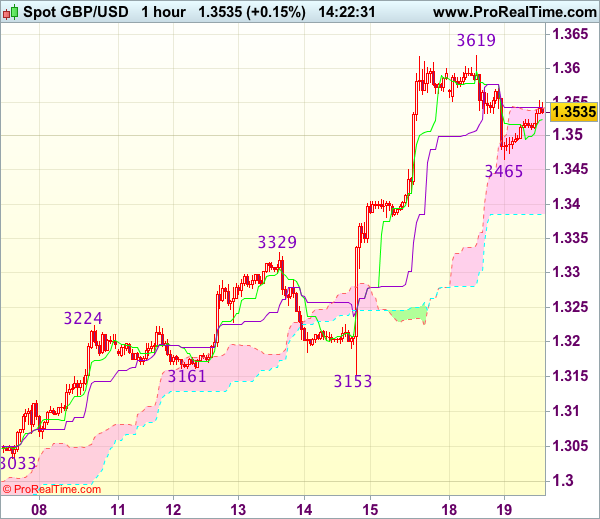

Trade Idea : GBP/USD – Buy at 1.3400

GBP/USD - 1.3527

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.3524

Kijun-Sen level : 1.3542

Ichimoku cloud top : 1.3541

Ichimoku cloud bottom : 1.3385

Original strategy :

Buy at 1.3420, Target: 1.3600, Stop: 1.3385

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3400, Target: 1.3560, Stop: 1.3365

Position : -

Target : -

Stop : -

Although cable found support at 1.3465 and has recovered, reckon upside would be limited to 1.3570 and risk of another corrective fall remains, below 1.3500 would bring test of said support at 1.3465, then 1.3430 but reckon 1.3400 would attract renewed buying interest, bring another rise later, above 1.3570 would signal the pullback from 1.3619 (yesterday’s high) has ended, bring retest of this level, then 1.3650.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as 1.3400-10 should limit downside. Only below the lower Kumo (now at 1.3385) would defer and signal a temporary top is formed, bring retracement of recent rise to 1.3350, then 1.3320-25 but 1.3300 should remain intact.

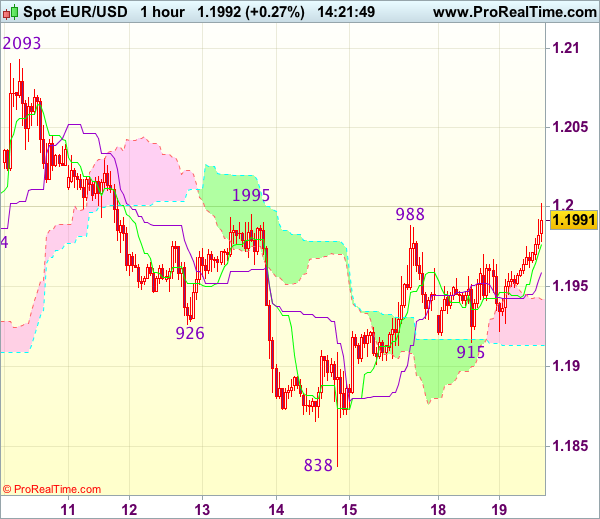

Trade Idea : EUR/USD – Buy at 1.1970

EUR/USD - 1.2001

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1978

Kijun-Sen level : 1.1960

Ichimoku cloud top : 1.1942

Ichimoku cloud bottom : 1.1913

Original strategy :

Buy at 1.1905, Target: 1.2005, Stop: 1.1870

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1970, Target: 1.2070, Stop: 1.1935

Position : -

Target : -

Stop : -

Current break of indicated resistance at 1.1995-00 (previous resistance and 61.8% Fibonacci retracement of 1.2093-1.1838) adds credence to our view that the fall from 1.2093 top has ended at 1.1838 last week and consolidation with upside bias remains for further gain to 1.2030-35, then 1.2050-55, however, break of 1.2070 is needed to signal early upmove has resumed for retest of 1.2093 first.

In view of this, we are looking to buy euro again on dips but at a higher level as 1.1965-70 should limit downside, bring another rise later. Below 1.1945-50 would defer and risk weakness towards support at 1.1915 (yesterday’s low) but only break there wold signal the rebound from 1.1838 has ended instead, bring further fall to 1.1880.

European Open Briefing: Asian Equity Markets Were Mixed Early On Tuesday

Global Markets:

- Asian stock markets: Nikkei rose 1.65 %, Shanghai Composite fell 0.29 %, Hang Seng down 0.08 %, ASX 200 up 0.11 %

- Commodities: Gold at $1311.30 (0.03 %), Silver at $17.20 (0.32 %), WTI Oil at $50.29 (-0.12 %), Brent Oil at $55.38 (-0.18%)

- Rates: US 10-year yield at 2.20, UK 10-year yield at 1.30, German 10-year yield at 0.45

News & Data:

- (AUD) HPI q/q 1.9 % vs 1.2 % expected

- (USD) TIC Long-Term Purchases 1.3 B vs 42.3 B expected

- (EUR) Italian Trade Balance 6.56 B vs 3.89 B expected

- (EUR) Final CPI y/y 1.5 % vs 1.5 % expected

- (EUR) Final Core CPI y/y 1.2 % vs 1.2 % expected

- (CAD) Foreign Securities Purchases 23.95 B vs 4.46 B expected

- Oil stable on lower Saudi exports, but rising U.S. shale output caps market – RTRS

- UK PM May Calls Special Brexit Cabinet Meeting – Times

- Toys 'R' Us Files for Bankruptcy In Richmond, Virginia – CNBC

Markets Update:

Asian equity markets were mixed early on Tuesday, while the wall street ended on a record high on Monday, Global investors deferred taking any major positions ahead of the Federal Reserve’s policy meeting that’s expected to focus on unwinding stimulus efforts. Japan was a bright spot in global markets Tuesday, coming off a holiday a day earlier

USD/JPY is currently seen trading steadily around 110.50, The yen was mostly seen ranging between 111.40 to 111.60 for most of the session early on Tuesday with no major movements as investors wait on sidelines ahead of The Bank of Japan meet this week. Notably, the Yen had lost 0.7 percent against the US dollar on Monday.

AUDUSD jumped as high as 0.7994 against the US Dollar during the RBA minutes earlier on Tuesday, but lost most of its gains and is currently seen trading back under 0.7970. The Newzealand dollar is currently seen trading around 0.7280 as the Kiwi added 0.2 percent against the US Dollar after falling 0.5 percent in the previous session

EUR/USD is currently seen trading at 1.1967 as the Euro was up 0.1 percent against the US Dollar. The dollar index, which tracks the dollar against a basket of currencies was flat and is currently valued at 91.95 after climbing 0.3 percent on Monday.

Upcoming Events:

- 09:00 GMT – (EUR) German ZEW Economic Sentiment

- 12:30 GMT – (CAD) Manufacturing Sales m/m

- 12:30 GMT – (USD) Building Permits

- 12:30 GMT – (USD) Current Account

- 12:30 GMT – (USD) Housing Starts

- 12:30 GMT – (USD) Import Prices m/m

- 22:45 GMT – (NZD) Current Account

- Tentative – (NZD) GDT Price Index

Trade Idea : USD/JPY – Buy at 111.00

USD/JPY - 111.73

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 111.63

Kijun-Sen level : 111.51

Ichimoku cloud top : 110.99

Ichimoku cloud bottom : 110.45

New strategy :

Buy at 111.00, Target: 112.00, Stop: 110.65

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone after recent anticipated rally, suggesting the reversal from 107.32 low is still in progress and further gain to 112.00, then 112.20 resistance would be seen, however, near term overbought condition should prevent sharp move beyond 112.40-45, risk from there has increased for a retreat later.

In view of this, would not chase this move here and would be prudent to buy dollar on subsequent pullback as 111.00-05 should limit downside. Below 110.62 support would abort and signal a temporary top is formed instead, risk correction to 110.30-35, then towards 110.00 which is likely to hold from here.

The RBA Expects The Economy To Pick Up Gradually

Market movers today

Today, German ZEW expectations. In August , the figure dropped to 10.0, due to weaker exports and the growing scandal in Germany's automobile sect or. Together with the appreciating euro's pressure on exports, this could cause economic sentiment to deteriorate. However, both business expectations (Ifo) and German PMIs increased in August , signalling still increasing opimism on the part of business. Overall, we expect the ZEW expectations to show a small decline to 9.5.

The Central Bank of Hungary will hold its monetary policy meeting today, where it might expand liquidity further by lowering the cap of the three-month deposit and/or cutting the O/N interest rate, despite inflation starting to pick up recently.

Selected market news

It has been a relatively quiet session overnight both in terms of news and price act ions as investors await the FOMC meeting tomorrow. In the US, equity indices ended the day higher with S&P500 and Dow Jones gaining 0.15% and 0.28%, respectively. In Asia this morning, trading is more mixed with most regional indices trading lower while Japanese equity indices are up 1.3-1.5%.

While a large part of today's outperformance in Japanese equities can be explained by Japan catching up yesterday after returning from holiday, rising expectations of an early election might also boost the rally. Japanese equity markets have previously gained ahead of the dissolutions of the parliament on calls for elections. According to several media, it seems increasingly likely that Japan's Prime Minister Shinzo Abe will dissolve the Lower House later this month and call for a general election. If an early election is called this month, the Bank of Japan (BoJ) and consumption taxes are likely to come to the fore of political discussions. In particular, the questions about who will lead the BoJ when Haruhiko Kuroda's current five year terms ends in April is a theme that could induce uncertainty about the BoJ's monetary policy , as investors will probably link the fate of the Abe administration with the current accommodative policy regime (Abenomics).

In a speech last night in Washington, Bank of England (BoE) governor Mark Carney echoed the surprisingly hawkish statement from the BoE last week and signalled that the MPC might soon hike the Bank Rate as global factors in combination wit h a decline in the economy's potential due to Brexit have increased the chance of overheating and warrant s higher interest rates. We expect the BoE to hike in November.

There were no surprises in the minutes from the Reserve Bank of Australia's (RBA) meeting on 5 September published this morning. The RBA expects the economy to pick up gradually but there was no signal that the RBA is about to change its policy rate. We expect the RBA to deliver one 25bp hike within the next 12 months, which is in line with market pricing.

RBA Sees Strength In Jobs Market, Remain Concerned About Sluggish Wages

For the 24 hours to 23:00 GMT, the AUD declined 0.75% against the USD and closed at 0.7964.

LME Copper prices rose 0.5% or $30.0/MT to $6487.0/MT. Aluminium prices declined 0.1% or $1.5/MT to $2066.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7968, with the AUD trading slightly higher against the USD from yesterday’s close.

Earlier today, minutes of the Reserve Bank of Australia’s (RBA) September meeting showed that officials grew more upbeat on Australia’s economic outlook, citing an improving labour market. Although policymakers expressed concerns about rising household debt and a strong local currency.

The pair is expected to find support at 0.7927, and a fall through could take it to the next support level of 0.7886. The pair is expected to find its first resistance at 0.8022, and a rise through could take it to the next resistance level of 0.8076.

Looking ahead, market participants will closely monitor Australia’s Westpac leading index for August, scheduled to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Growth Confirmed At A 4-Month High In August

For the 24 hours to 23:00 GMT, the EUR slightly rose against the USD and closed at 1.1957.

On the economic front, the Euro-zone's final consumer price index (CPI) rose to a four-month high of 1.5% on an annual basis in August, confirming the preliminary print. In the previous month, the CPI had risen 1.3%.

Separately, according to the Bundesbank monthly report, Germany's consumer price inflation is likely to retreat in the autumn, due to the “base effects” of sharp increases a year earlier.

Macroeconomic data released in the US indicated that the NAHB housing market index unexpectedly fell to a level of 64.0 in September, amid concerns that Hurricane Harvey as well as Irma will lead to higher material costs and shortage of labour. Investors had envisaged the index to remain steady at a revised reading of 67.0.

In the Asian session, at GMT0300, the pair is trading at 1.1965, with the EUR trading 0.07% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1928, and a fall through could take it to the next support level of 1.1892. The pair is expected to find its first resistance at 1.1988, and a rise through could take it to the next resistance level of 1.2012.

Going ahead, market participants will focus on the release of ZEW expectations survey for September across the Euro-zone along with the region's construction output data for July, slated to release in a few hours. Additionally, the US housing starts and building permits data, both for August, set to release later in the day, will attract significant amount of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoE’s Carney Hints At Gradual Interest Rate Rises, Warns Of Brexit Repercussions

For the 24 hours to 23:00 GMT, the GBP declined 0.6% against the USD and closed at 1.3515, after the Bank of England (BoE) Governor, Mark Carney, indicated that any future interest rate hikes would be limited and gradual.

Further, Carney, in a speech at the International Monetary Fund (IMF), warned that economic implications of Brexit has yet to be felt and will likely slowdown the British economic growth until the middle of next year and push inflation up, as it has already prompted households to cut back on spending and businesses to invest less than usual.

In the Asian session, at GMT0300, the pair is trading at 1.3512, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.3445, and a fall through could take it to the next support level of 1.3378. The pair is expected to find its first resistance at 1.3599, and a rise through could take it to the next resistance level of 1.3686.

In absence of any macroeconomic releases in the UK today, investors will look forward to global macroeconomic events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.3% against the JPY and closed at 111.47.

In the Asian session, at GMT0300, the pair is trading at 111.52, with the USD trading slightly higher against the JPY from yesterday’s close.

The pair is expected to find support at 111.21, and a fall through could take it to the next support level of 110.91. The pair is expected to find its first resistance at 111.74, and a rise through could take it to the next resistance level of 111.97.

Moving ahead, traders will look forward to Japan’s adjusted merchandise trade balance data for August, due to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.