Sample Category Title

Eco Data 9/18/17

[php_everywhere] [/php_everywhere]

Eco Data 9/21/17

[php_everywhere] [/php_everywhere]

Summary 9/18 – 9/22

Monday, Sep 18, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Sep 19, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Sep 20, 2017

[php_everywhere] [/php_everywhere]

Thursday, Sep 21, 2017

[php_everywhere] [/php_everywhere]

Friday, Sep 22, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Economic Data under Close Watch by the Fed

U.S. Review

Slight Firming in Inflation Ahead of FOMC Meeting

- After three months of lower-than-expected inflation readings, the CPI came in higher than expectations. Despite inflation's relatively tepid trend, FOMC members have continued to signal that they are set to announce the start of balance sheet normalization at next week's meeting.

- Hurricane damage is beginning to show up in the monthly data. August retail sales contracted from the previous month, with notable weakness in auto sales.

- Industrial production surprised to the downside with manufacturing production contracting 0.3 percent in August.

Economic Data under Close Watch by the Fed

Consumer prices rose 0.4 percent in August, the largest monthly jump since January. Leading the index was a 2.8 percent rise in energy costs. Prices for gasoline had already been inching higher ahead of the Harvey-related surge late in the month. To what will likely be a relief to Fed officials, core inflation rose 0.2 percent in August, which was the largest monthly gain since February. On a year-over-year basis, core inflation continues to undershoot the Fed's 2 percent inflation target. Ex-food and energy, prices were up just 1.7 percent over the past 12 months. Following the firming in August, however, the recent trend looks stronger; over the past three months, the core index has risen at a 1.9 percent annualized pace.

August's gain should help alleviate concerns among Fed members that the slowdown in inflation that began in the spring might prove more lasting. FOMC members have continued to telegraph that they are set to announce the start of balance sheet normalization at next week's meeting. We do not expect the inflation data to get in the way of that plan. What is likely to be affected, however, is the Fed's Summary of Economic Projections. There will be three more readings on CPI and PCE inflation before the FOMC's December meeting, but the soft patch hit in prior months is likely to lead to lower estimates of year-end core inflation, which may push out the members' projections for the timing of the next rate hike.

Retail Sales and Industrial Production Disappoint

While August's CPI print may have lessened concerns about the recent slowdown in inflation among Fed members, notable weakness in the retail sales and industrial production reports may make the members reassess the general strength of the economy. The pronounced weakness in these two reports may be related to Hurricane Harvey.

Headline retail sales dropped 0.2 percent, with auto sales trimming 0.3 percentage points from topline growth. The decline in auto sales more than offset the boost from the 2.5 percent rise at gas stations. The surge in gasoline sales was largely expected, due to stocking up in storm affected areas. Moreover, the 0.5 percent decline in building material sales on the month, suggests most of that spending took place in September – this category will likely see a boost in September as Houston and the state of Florida rebuild and recover from the storm.

Industrial production data was also off sharply in August, declining 0.9 percent. Manufacturing production, which includes petroleum refining and petrochemical production in and around Houston, declined 0.3 percent in August, following a flat reading in July. Utilities posted the steepest drop, contracting 5.5 percent. Mild temperatures across the U.S. led to lower usage of air conditioning. The weaker than expected data appears to be largely accounted for Harvey-related effects which are likely transitory in nature. The Empire State Manufacturing index for September, a regional purchasing managers' index, suggests that beyond the recent weather-related industrial disruptions, factory activity remains strong.

U.S. Outlook

Housing Starts • Tuesday

Housing starts had a disappointing month of July, falling 4.8 percent on the month and down 5.6 on a year-ago basis. The weakness in July was concentrated in the multifamily component of the index, which fell 15.3 percent. Given the late-cycle fundamentals in that market, the drop is not surprising. Shortages in both lots and labor are holding back starts. Houston has been a key driver of housing construction this year, and Hurricane Harvey will almost certainly cause delays in planned housing starts.

Looking ahead, we expect August starts at a 1.174 million unit pace, an increase of 1.6 percent. We estimate that starts will be around 1.220 million units for 2017, down slightly from our prior forecast due to implications from both Hurricane Harvey and Irma, as single-family building will be held back in parts of Texas and Florida due to delays tied to those storms.

Previous: 1,155K Wells Fargo: 1,174K Consensus: 1,175K

Import Prices • Tuesday

In July, import prices rose a paltry 0.1 percent due to a 0.7 percent increase in imported petroleum prices, matching expectations. Import prices ex-fuel declined last month, however, the first drop since January. Last month, autos & parts prices fell, while capital goods and food & beverages prices increased. The greenback is down around 7 percent year-to-date, and is expected to take on further declines. This should boost prices on imported goods through the end of the year.

Next week, we expect to see import prices gain 0.5 percent monthto- month due to the dollar slide. However, we also expect the effect of elevated import prices will be limited on consumers, as prices on goods and services that are domestically produced should not be pushed upward by global exchange rates.

Previous: 0.1% Wells Fargo: 0.5% Consensus: 0.4% (Month-over-Month)

Existing Home Sales • Wednesday

The low inventory of existing homes for sale capped sales in July, with sales slipping to a 5.44 million unit pace, compared to a 5.51 million unit pace in June. Demand for housing remains strong thanks to low mortgage rates, job growth and rising income. Competition among buyers is stiff. Supply remains low and prices are rising as a result. First-time homebuyers are being priced out of the market with the high prices of homes, and home sales at the lower-end of the price spectrum have declined in every region of the nation over the year.

We expect existing home sales in the month of August to slightly fall to a 5.43 million unit pace. Texas and Florida account for 18.8 percent of existing home sales year-to-date, so we could see a stall in existing home sales in these markets throughout the end of the year, but this will likely be seen more in September compared to August.

Previous: 5.44M Wells Fargo: 5.43M Consensus: 5.46M

Global Review

Chinese Economy Cools at Summer's End

- Economic data out of China disappointed across the board this week. Retail sales and industrial production growth both came in below consensus.

- In the United Kingdom, the Bank of England's Monetary Policy Committee voted 7-2 in favor of keeping its policy rate and balance sheet unchanged. The pound and U.K. government bond yields jumped on hawkish language.

- The Brazilian economy continued its long climb back from a severe recession. The economic activity index for July topped expectations, rising 0.4 percent over the month in addition to a small upward revision to the previous month.

Chinese Economy Cools at Summer's End

Economic data out of China disappointed across the board this week. Retail sales growth on a year-over-year basis was 10.1 percent in August, 0.4 percentage points below the consensus. Industrial production growth also missed the mark, slowing to 6.0 percent year-over-year despite expectations for a 6.6 percent gain. Both readings were the slowest pace so far in 2017.

Leverage in the non-financial corporate (NFC) sector in China has become a growing concern. Chinese authorities are well aware of the leverage that has been built up in the NFC sector in recent years, and they are trying to rebalance the economy away from its over-reliance on investment spending toward more consumer spending before a debt crisis causes the economy to implode. As a result, authorities have eased up on the policy pedal in recent months, and it appears the economy has begun to feel the effects.

High debt levels and less free flowing credit, coupled with longerterm challenges such as an aging population, support our view for a continued but gradual deceleration in the Chinese economy next year. For more on NFC leverage in China, see our report released Thursday "Should We Worry about Chinese SOEs?"

In the United Kingdom, the Bank of England's (BoE) Monetary Policy Committee (MPC) voted 7-2 in favor of keeping its main policy rate and balance sheet unchanged. The language in the policy statement noted that "monetary policy could need to be tightened by a somewhat greater extent over the forecast period than current market expectations." This hawkish tact led the pound and U.K. government bond yields to jump.

Above-target inflation is the key to the Bank of England's bias towards tightening policy next year. The sharp depreciation of the currency in the wake of Brexit last year has driven consumer price inflation to nearly 3 percent, almost a full point above the central bank's target (middle chart). An above-consensus print for the August consumer price index released this past Tuesday only reinforced that point. Sluggish wage growth has kept the MPC in check; despite the acceleration in prices and an unemployment rate at a 42-year low, wages have decelerated in 2017 relative to H2-2016. We look for the Bank of England to next hike rates in Q2-2018.

Across the channel, industrial production growth continued to firm in the Eurozone, rising 3.2 percent year-over-year in July from an upwardly revised 2.8 percent in June. Industrial production has accelerated, helping corroborate the marked improvement in sentiment demonstrated by manufacturing purchasing manager indices.

Elsewhere, the Brazilian economy continued its long climb back from a severe recession. The economic activity index for July topped expectations, rising 0.4 percent over the month in addition to a small upward revision to the previous month. Although the Brazilian political corruption crisis has continued on, it appears that a more firm environment for commodities and global economic growth more generally have helped the Brazilian economy turn the corner after several years of contraction.

Global Outlook

United Kingdom Retail Sales • Wednesday

The U.K. is scheduled to release August retail sales data this upcoming Wednesday. Real retail sales have been decelerating recently as rising inflation and stagnant wage growth have taken a bite out of household purchasing power. The consensus estimate expects that retail sales grew 0.1 percent in August, month over month, and 1.2 percent on a year-ago basis. Both these estimates represent a slowdown from July in which retail sales grew 0.3 percent month over month and 1.5 percent year over year. On a year-over-year basis, real retail spending was up only 2.6 percent in Q2, which clearly represents a slowdown relative to the breakneck pace of the past few years.

Looking ahead, we forecast that real GDP growth will strengthen modestly in 2018 as some of the forces that have led to a slowdown this year reverse, although uncertainty related to Brexit continues to lurk in the background as a major downside risk to the economy. Previous: 0.3%

Consensus: 0.1% (Month-over-Month)

Canada CPI • Friday

Canadian consumer price inflation data are scheduled to be released next Friday. Last week, the Bank of Canada (BoC) raised rates in a move that was somewhat anticipated by markets, but generally not expected by most economists. Economic data coming out of our northern neighbor have been stronger than expected, leading the BoC to judge that the faster rate of growth to be "more broadly based and self-sustaining." The September rate hike likely takes another hike in October off the table.

The headline rate of CPI inflation in Canada is just 1.2 percent at present, near the low end of the target range. We expect CPI to have grown 0.1 percent month over month in August and 1.4 percent year over year. Also on the docket for next week is Canadian retail sales data for July. Retail sales were up 7.3 percent on a year-ago basis in June.

Previous: 1.2% Wells Fargo: 1.4% Consensus: 1.5% (Year-over-Year)

Eurozone PMIs • Friday

Preliminary Eurozone manufacturing and service PMI data for September will be released next Friday. The PMI for manufacturing in August was well in expansion territory at 57.4, tying the series' high. The service sector PMI dropped to 54.7 in August from 55.4 in July, and has slowly come off its April series' high, but remains firmly in expansionary territory. Real GDP in the Eurozone accelerated in Q2, as economic growth has become increasingly broad based in recent quarters amid steady employment gains and improving business sentiment. This marks the 17th consecutive quarter in which real GDP has risen on a sequential basis.

Looking forward, we expect that the increasingly self-sustaining economic expansion will remain intact. Our current forecast looks for real GDP in the Eurozone to grow 2.1 percent in 2017 and 2.0 percent in 2018.

Previous: Manufacturing: 57.4; Services: 54.7 Consensus: Manufacturing: 57.2; Services: 54.8

Point of View

Interest Rate Watch

Student Loan Breakout

Details of the student credit experience provide a number of insights into the strength of consumer spending and the outlook going forward.

Origination By Credit Quality

As the economic expansion has matured, the share of deep-subprime and subprime loans originated has declined compared to 2010-2012 (top graph). This is expected since individual credit quality improves as job growth strengthens and many individuals reduce their outstanding debt. Over the same past four years, the share of prime and super-prime loans has risen.

Another Signal of Improvement

Over the past four years for which data is available, cohort default rates have declined after a peak in FY2010 (middle graph). This improvement has coincided with a rise in the average award since the 2008-2009 recession.

Default Rates by Borrowing Amounts

What remains a surprise to many casual observers is that the details signal that the five-year default rates by borrowing amount actually decline with the size of the borrowing amount (bottom graph).

The smaller borrowing amounts may reflect drop-outs. These are students that took one or two semesters, borrowed the money but never completed their degree. They have the liability (the student loan) but not the asset (diploma).

Not shown, but also critical, is that five-year default rates decline by the average income of the borrower's zip code. This again signals that a higher income may be associated with a better ability to pay off the debt even during what may be perceived as a weak job market.

Interest Rates on Student Loans

Interest rates on new student loans track the 10-year Treasury note rates set at the May auction, and then remain fixed for the life of the loan. For students starting college this academic year, interest rates are 0.69 percentage points higher than a year ago, due to a spike in the 10-year yield. Along with future increases as the Fed normalizes policy, this could negatively impact default rates going forward.

Credit Market Insights

Safety Hammers Convenience

As roughly 143 million Americans were affected by the expansive data breach disclosed last week, consumer fears may weigh on the convenience of accessing credit. In an attempt to combat the lost sense of security, there has been a surge in freezing credit. As freezes were traditionally utilized by individuals who have experienced identity theft, or repetitive fraudulent activity, this recent rise could have implications on the financial industry.

A credit freeze prevents a lender from freely accessing a potential borrower's credit, affixing a password authentication as a road block prior to accessibility. Although this extra step of safety appears enticing, it lessens the convenient nature of openness to a consumer's creditworthiness. This lack of accessibility has implications on the lender, increasing the timeframe between a request for credit, and the actual installment. The rise may limit credit volume and could cause a decline in the quantity of loans.

The Federal Reserve Bank of Philadelphia published a report in 2014 on credit fraud, linking the 2012 data breach at the South Carolina Department of Revenue with a rise in credit freezes. But with scarce government data on credit freezes, it remains difficult to truly assess any future implications of such a rise. Although a rise in the freezing of credit appears to be an effect of the recent data breach, we must remain cautious of any implications on the future of the credit markets.

Topic of the Week

Legislative Hurricane Blows Through DC

Last week Congress unexpectedly passed a combined funding bill, debt limit suspension and Hurricane Harvey aid package. The package uses a continuing resolution to fund the government and suspends the debt limit through December 8. The bill also allocates $15.3 billion toward Hurricane Harvey relief, $7.4 billion towards FEMA's Disaster Relief Fund and extends the National Flood Insurance Program through December 8.

Importantly, the provision suspending the debt ceiling does not set December 8 as a "hard" deadline. After exhausting all of its extraordinary measures over the past six months, lifting the debt ceiling will allow the Treasury to refresh these maneuvers in the coming months. We are skeptical that the extraordinary measures will be able to last far beyond the December 8 reestablishment of the debt ceiling due to the timing of tax filing season. February and March usually see large outflows due to individuals who file their taxes early in anticipation of a tax refund, resulting in large monthly deficits. That said, the take away is that there will be some time between when the government's authority to borrow ends on December 8 and when the Treasury actually runs out of the ability to issue new debt.

The short-term deal sets up a fight in December over how to 1) fund the government beyond December 8, 2) whether to include funding for a wall on the southern U.S. border as requested by the White House and 3) find a permanent fix for DACA that Democrats are likely to demand. With the debt ceiling likely out of the picture in December, we see a high probability that December's fiscal fights are not going to end quickly. We are assigning a higher probability of a partial government shutdown in December relative to September given the inclusion of contentious immigration provisions into the debate. We do, however, expect a "clean" longer-term debt ceiling suspension to be passed in advance of the Treasury's extraordinary measures expiring, which will likely occur in Q1 of next year.

The Weekly Bottom Line: The Data Giveth and the Data Taketh Away

U.S. Highlights

- Investors and analysts reading the economic tea leaves were given mixed messages this week. On the one hand, inflation ticked up, but on the other, consumer spending softened.

- Consumer prices rose 0.4% (m/m) in August, pushing inflation to 1.9% (y/y) from 1.7%. A sharp rise in gasoline prices on the back of refinery shutdowns contributed to the gain. Core prices accelerated to 0.2% (m/m).

- Retail sales, on the other hand, fell 0.2% in August. With downward revisions to June and July, momentum in consumer spending has slowed heading into the third quarter relative to its blistering pace in Q2.

Canadian Highlights

- Housing data for August was fairly positive, with starts trending higher and resale activity recovering slightly.

- Canadians continued to pile on debt in the second quarter, sending the household debt-to-disposable income ratio to a new high of 167.8%. Despite a slight uptick, household leverage ratios remain well below post-crisis highs, reflecting strong asset value gains over this time.

- Census data provides an interesting insight into the post-crisis evolution of Canadian incomes. Commodity-oriented provinces saw marked gains in median incomes, while much more modest growth was recorded elsewhere, reflecting the uneven impact of macroeconomic drivers over the 2010-2015 period.

U.S. - The Data Giveth and the Data Taketh Away

Investors and analysts reading the economic tea leaves for signals on future Federal Reserve policy were given mixed messages this week. On the one hand, inflation ticked up, but on the other, consumer spending softened. Further muddying the water, both the CPI and retail sales reports were affected by Hurricane Harvey, a phenomenon that will continue in the months ahead.

One of the chief concerns of the Federal Reserve recently has been the persistent weakness in inflation. Despite ongoing improvement in the job market and an unemployment rate comfortably below target, price growth been slowing for much of this year. Inflation according to both the overall CPI and the core measure peaked in February. Energy prices contributed to inflation early in the year, but the impact was fleeting. Moreover, the weakness in inflation cannot be attributed entirely to idiosyncratic factors. Measures that strip them out, such as median and trimmed-mean inflation, have also decelerated noticeably.

One month does not a trend make, but August may be an early sign of a reversal in this downward trend. Headline consumer prices rose 0.4% on the month, pushing year-on-year inflation to 1.9% from 1.7%. A sharp rise in gasoline prices (6.3% month-over-month) on the back of refinery shutdowns due to Hurricane Harvey contributed to the gain in the headline.

More convincing was the gain in core prices and in the aforementioned median and trimmed mean measures. Core prices rose 0.2% on the month (0.249% to be precise), the strongest gain since January. While Harvey may have had some impact on core prices, the acceleration was broad-based with both median and trimmed-mean prices accelerating noticeably (both up 0.2%).

For the Federal Reserve, evidence that inflation may finally be heading higher should provide confidence that the economy is ready for higher interest rates. However, it will also want to see signs that the economic recovery remains on track. In that regard the pullback in retail sales (down 0.2% in August) provided a cautionary note As with the CPI data, Hurricane Harvey was likely an influence, especially for auto sales, which fell 1.6% in dollar terms (units fell 4%). Nonetheless, downward revisions to both June and July suggest less momentum in consumer spending even prior to Harvey. While spending is likely to rebound as the recovery efforts from Harvey and Irma take shape, a broader-based slowdown will not go unnoticed at the Fed.

All of this comes as the FOMC is due to meet to deliberate policy early next week. The Fed appears unlikely to hike its key lending rate at this meeting, but it is likely to announce plans to gradually begin unwinding its balance sheet. These have been well telegraphed to markets with most of the impact on bond yields already priced in. More important will be how much the statement recognizes the recent moves in inflation and how this comes through in the expectations of FOMC members for future policy rates, which will be released in the Survey of Economic Projections along with the policy statement. Stay tuned until Wednesday afternoon for more details.

Canada - A Decent August for Housing

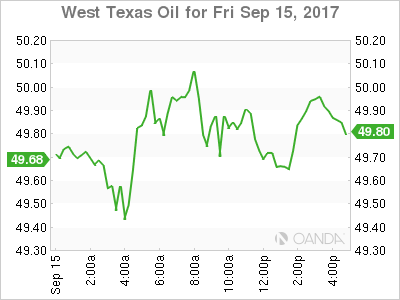

It was a mixed week in the markets, with the Canadian dollar back roughly near where it started the week as of writing, reflecting the offsetting impacts of rising oil prices (which touched $50/barrel on Thursday) and a more positive outlook for U.S. rates. Improved oil prices supported Canadian equities, which were up slightly as of mid-morning Friday.

Data this week was focused on housing and borrowing. To begin with, the resale housing market might have softened in Ontario, but housing starts rebounded in August, helping push the national trend higher (Chart 1). Once again, multi-family homebuilding led the way, likely driven by the pre-sale of projects in the year prior. Because of the prevalence of multi-unit projects (about 60% of total starts), housing starts provide more of a backwards-looking view of how the market is evolving. As such, we remain of the view that starts are likely to trend lower as the year progresses, consistent with the evolution of the Toronto market earlier this year. It is important to remember that despite all the attention Toronto receives, most other major markets are expected to see steady activity, keeping overall starts around 200k on a medium-term basis.

Indeed, the Toronto market is already showing signs of turning the corner, with data for August showing a 14.3% month-on-month increase in sales activity (although it remains well below earlier peaks), and a roughly balanced sales-to-listing ratio. It is clearly early days and there are many moving parts (not least of which are rising borrowing costs and potential changes to mortgage qualification rules for uninsured borrowers), but there is at least some scope for cautious optimism regarding the Greater Toronto Area housing market.

The rise in rates comes against a backdrop of further indebted Canadian households. Data for the second quarter showed a 1.2%-point increase in the ratio of debt-to-income, as household borrowing outpaced income growth. The debt service ratio remained flat as interest costs hit a record low 6.0% of income (covering the second quarter of the year, this data does not include the effects of the Bank of Canada's back-to-back interest rate hikes). Although the debt-to-asset ratio ticked up slightly, indicating rising household leverage, it nevertheless remains well below post-crisis highs as the value of household assets grew more quickly than borrowing over this time.

Dialing the focus back a bit from the high frequency data, Census data released this week provides an interesting insight into the relative performance of the provinces over the post crisis period, in terms of median household income (Chart 2). The impact of the resource boom is clear, despite the Census data capturing the first year of the oil price downturn. Income growth was strongest in the commodity producing provinces of Saskatchewan, Newfoundland and Labrador, and Alberta. Conversely, its high starting point resulted in Ontario remaining near the top of the ranks, but Ontario saw the weakest income growth, likely a reflection of the challenges facing its industrial base over this period. If this data tells us anything, it serves as a clear reminder that beneath the aggregate data often lurk divergent outcomes among groups and regions.

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales - July

Release Date: September 19, 2017

Previous Result: -1.8% m/m

TD Forecast: -1.5% m/m

Consensus: -0.7% m/m

Canadian manufacturers' summer doldrums are expected to continue into July with nominal sales forecast to decline a further 1.5% m/m. Much of this reflects the unruly appreciation in the Canadian dollar, which was the driving force behind a sharp decline in factory prices, though we do anticipate some pullback in real activity as well. Transportation shipments are expected to exert a sizeable drag after international trade data showed a significant pullback in exports of both motor vehicles and aircraft. We see scope for a pullback in machinery shipments, which are up over 20% on the year, after a sharp decline in export activity. We also see downside risks to forestry product shipments after a series of wildfires shuttered BC lumber mills for part of the month.

While the decline in real manufacturing sales should prove to be more modest than the nominal print, they are coming off a 1.0% decline in June so another negative print will be to the detriment of Q3. While our current tracking points towards GDP growth in the mid-2% range, this is due largely to the resilience of consumer spending and the outlook for exports is less upbeat.

Canadian Retail Sales - July

Release Date: September 22, 2017

Previous Result: 0.1% m/m, ex-auto 0.7% m/m

TD Forecast: 0.1% m/m, ex-auto 0.3% m/m

Consensus: 0.3% m/m, ex-auto 0.5% m/m

Retail sales are forecast to rise by 0.1% m/m in July while weaker motor vehicle spending should leave the ex-autos measure up 0.3% on the month. Last month's report showed that the slowdown in the Toronto housing market has weighed on big ticket purchases by local residents, and we expect this regional underperformance to continue into July. Outside of the Toronto region, labour market gains and elevated consumer confidence should continue to drive spending and sesquicentennial Canada Day celebrations could add to general merchandise and food and beverage sales. Meanwhile, the increase in consumer prices should see real retail sales underperform the nominal print. Given the solid handoff from June and a stabilization in the Toronto housing market, we think that household spending will remain one of the prominent drivers of growth in Q3 but expect PCE to moderate from the 4.6% advance in Q2.

Canadian Consumer Price Index - August

Release Date: September 22, 2017

Previous Result: 0.0% m/m, 1.2% y/y

TD Forecast: 0.2% m/m, 1.5% y/y

Consensus: 0.2% m/m, 1.5% y/y

TD expects headline inflation to firm to 1.5% in August from 1.2%, reflecting a 0.2% monthly increase in consumer prices and favourable base effects. Gasoline prices should serve as a key source of inflationary pressure though some of this can be faded due Hurricane Harvey's impact on refineries. Shelter prices should also provide a tailwind as new home prices have yet to adjust to the slowdown in the housing market. However, food prices are likely to offset the strength elsewhere due to the combination of falling agricultural prices and FX passthrough. We expect measures of core inflation to remain stable but the risks lean towards another modest improvement.

Week Ahead – Dollar Mixed Awaiting Fed Policy Meeting

Mixed Data and North Korea did not keep USD down

The US dollar managed to end the week in a positive note despite a lower than expected retail sales reading on Friday and flat US inflation data on Thursday. Economic data has begun to reflect the impact of Hurricane Harvey and later in the month the effects of storm Irma will be taken into account. The pound was one of the few currencies that gained against the dollar after the Bank of England (BoE) left rates unchanged on Thursday, but said rate hike could home sooner than expected boosting the currency against the USD. Central banks will remain in the spotlight with the Fed and the Bank of Japan set to publish their September monetary policies in the week of September 18-22.

The U.S. Federal Reserve will publish its rate statement on Wednesday, September 20 at 2:00 pm EDT. The US central bank will also release its updated economic projections and will host a press conference at 2:30 pm with Fed Chair Janet Yellen. Last month the Fed added that "relatively soon" it would start shrinking its massive balance sheet accumulated during its QE program. On the topic of a change to the benchmark Fed funds rate the CME FedWatch tool rates the probability of a September rate hike at 0 percent, with December a 50 percent chance.

The Bank of Japan (BOJ) will publish its monetary policy statement on Wednesday, September 20 at 11:50 pm EDT with a press conference to follow on Thursday, September 21 at 2:30 am EDT. The Japanese central is not expected to make a change to its monetary policy as inflation remains stubbornly low despite unprecedented stimulus by the BOJ. Growth has continued its upward trend but with little help from inflationary pressures no reduction in stimulus is in the horizon.

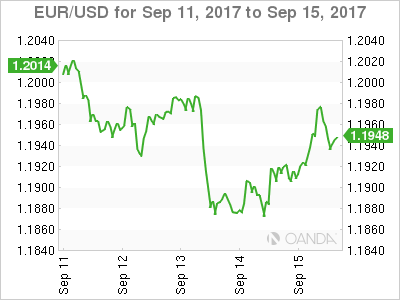

The EUR/USD lost 0.812 percent in the last five trading days. The single currency is trading at 1.1932 after US tax reform got closer to reality this week. The euro had advanced at the start of the week as more USD weakness was anticipated, but a turnaround in market expectations on a December rate hike and a show of momentum on tax reforms started a dollar rally putting the pair below 1.20. Political uncertainty has been a big factor of USD trading and a Trump administration ready to embrace dialogue with Democrats is seen as a productive development.

Next up will be the September Federal Open Market Committee (FOMC) meeting. The market is expecting the Fed to formally announce the start of the reduction of its balance sheet. Since the move is expected to be gradual the Fed could push the announcement back, specially if there is some uncertainty about a December rate hike but the dollar would suffer if that is the case. The White House has remained tight lipped about who will be the Fed Chair next year. Yellen's term ends in February, and with the falling out to favour of Gary Cohn, she could even remain in the job. While Janet Yellen was not the first choice of the Obama administration she got the nod, after a scandal took the front runner Larry Summers out of contention.

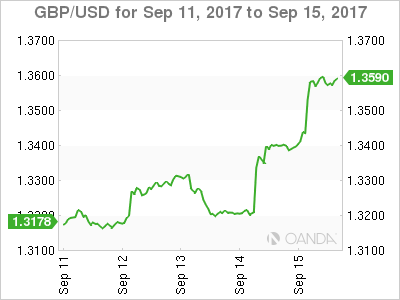

The GBP/USD gained 2.867 percent during the week. The currency pair is trading at 1.3567 near weekly highs of 1.3617. The hawkish policy by the Bank of England (BoE) drove the pound to its highest post Brexit referendum. Even the doves within the central bank have endorsed a rate hike in the near future. Rising inflation and a tighter job market have convinced uber dove Gertjan Vlieghe to back a higher interest rate.

The Office for National Statistics will release UK retail sales on Wednesday September 20 at 4:30 am EDT. The forecast calls for a rise of 1.1 percent, but taking the volatile items out of the equation will show a 0.1 percent gain. Rising inflation in the UK is a concern because despite a tighter job market wages remain flat putting more pressure on households to cope with higher prices.

US oil prices surged 4.016 percent in the last five days. The West Texas Intermediate is trading at $49.63 after briefly touching $50 per barrel. Oil prices recorded near two month highs as demand expectations picked up after the Organization of the Petroleum Exporting Countries (OPEC) released higher demand in 2018. US refineries getting back online also boosted energy prices. Higher demand with limited production due to Hurricanes Harvey and Irma boosted prices.

The International Energy Agency (IEA) also published a report this week that forecasts strong demand keeping the price of Brent above $55 and WTI near $50.

Market events to watch this week:

Monday, September 18

- 9:30pm AUD Monetary Policy Meeting Minutes

Tuesday, September 19

- 8:30am USD Building Permits

Wednesday, September 20

- 4:30am GBP Retail Sales m/m

- 10:30am USD Crude Oil Inventories

- 2:00pm USD FOMC Economic Projections

- 2:00pm USD FOMC Statement

- 2:00pm USD Federal Funds Rate

- 2:30pm USD FOMC Press Conference

- 6:45pm NZD GDP q/q

- 11:50pm JPY Monetary Policy Statement

Thursday, September 21

- Tentative JPY BOJ Policy Rate

- 2:30am JPY BOJ Press Conference

- 8:30am USD Unemployment Claims

Friday, September 22

- 8:30am CAD CPI m/m

- 8:30am CAD Core Retail Sales m/m

- 8:30am All Day NZD Parliamentary Elections

*All times EDT

Week Ahead – FOMC: Balance Sheet Announcement and Rate Projections Eyed; BoJ to Stand Pat

The Federal Reserve is expected to make its long-awaited announcement on its balance sheet reduction plan next week, though investors will probably be more interested in the FOMC's latest dot plot chart. The Bank of Japan also holds a monetary policy meeting but it will likely be a less exciting event than the Fed's. On the data front, Eurozone flash PMIs, UK retail sales, Canadian inflation and New Zealand GDP will be the highlights.

Eurozone data unlikely to shift euro out of consolidative phase

As the European Central Bank works on the details of its stimulus withdrawal plan, the euro rally has taken a pause. Data releases next week should provide some support for the euro but are not seen to drive the single currency to fresh highs, especially amid a stronger dollar and pound. First on the calendar is Monday's final inflation readings for the block. The annual rate of change in Eurozone CPI is expected to be confirmed at 1.5% in August, but core CPI is forecast to be revised down to 1.2% from the flash estimate of 1.2%. Germany's ZEW business survey will be watched on Tuesday. The ZEW economic sentiment and current conditions indices are both expected to improve in September. Eurozone producer prices for August will follow on Wednesday, but all eyes will be on Friday's flash PMI readings. Economic activity in the euro area is expected to remain steady with the IHS Markit composite PMI falling marginally to 55.6 in September's flash reading. The services PMI is forecast to stay unchanged at 54.7, while the manufacturing PMI is expected to decline by 0.2 to 57.2.

Bank of Japan meeting to be a non-event?

The Bank of Japan's policy meetings are known just as much for being non-events as for surprising markets with unconventional stimulus measures. The meeting on September 20-21 is looking like it will be the former as the Bank is not likely to make any changes to its forecasts before the October meeting when it will publish its quarterly outlook report. It's possible that next month the Bank could once again delay the timing of when its expects to hit its 2% inflation target. This would reinforce expectations that the BoJ will be the last of the major central banks to start tightening monetary policy. Before the BoJ meeting, trade data will come in focus on Tuesday. Exports from Japan are forecast to rise by 14.7% year-on-year in August as a weaker yen and improving global demand continue to boost Japanese manufacturing output. Another positive figure in August would make it the ninth consecutive month of annual gains in exports.

New Zealand GDP eyed ahead of elections

GDP figures out of New Zealand next week may provide a welcome distraction away from the September 23 election campaign that is proving to be a much tighter race than anyone anticipated. An unexpected strong showing for the Labour party has made the New Zealand dollar highly volatile in recent weeks as the prospect of the ruling National party losing power has unnerved investors. Solid GDP data on Wednesday could remind markets that the country's economic fundamentals remain strong and possibly provide some indication to the timing of a rate hike by the Reserve Bank of New Zealand. After growing at a relatively modest pace in the previous two quarters, New Zealand's economy is forecast to pick up speed in the June quarter, with growth accelerating to close to 1% over the quarter.

Canadian inflation and retail sales data to be watched after surprise rate hike

The Bank of Canada had to defend itself this week after receiving criticism for not clearly communicating that a rate hike at its September 6 meeting was on the cards. Market participants will therefore be watching next week's inflation and retail sales numbers more carefully for clues about a possible third rate hike in as many months. Canadian CPI, due on Friday, is forecast to rise from 1.2% to 1.5% y/y in August, suggesting that inflation is moving back towards the BoC's target as expected. Retail sales, also out the same day, are forecast to grow by 0.2% month-on-month. An upside surprise could add fresh impetus to the loonie's rally, which is currently trading near two-year highs against the greenback.

UK retail sales growth to moderate further

An IT problem at the Office for National Statistics caused a delay to the retail sales data, which are normally published in the same week as the inflation and employment reports. The delayed release may act in cooling the pound's 3% surge this week as retail sales are forecast to ease in August. Annual growth in retail sales is expected to moderate for the second month in a row to just 1.1% in August, while the month-on-month rate is forecast at 0.2%. A worse-than-anticipated reading may feed doubt into the expectations that the Bank of England will begin raising rates in the coming months.

Fed to start balance sheet normalization

The Fed will move into the limelight next week as it holds its two-day monetary policy meeting on September 19-20. However, second-tier data releases should also attract some attention, starting with a batch of August housing data on Tuesday. Building permits and housing starts are both released on Tuesday, followed by existing home sales on Wednesday. The Philly Fed's diffusion index of manufacturing activity for September is out on Thursday, and the IHS Markit flash manufacturing and services PMIs (also for September) will round up the week on Friday.

An announcement on reducing its $4.5 trillion balance sheet is widely expected by the Fed on Wednesday given that such a decision has been well telegraphed by FOMC members over the past few months. Market reaction, in particular for US treasury yields, will likely be muted as the Fed has said it will proceed with scaling back its reinvestments in maturing treasuries and mortgage-backed securities very gradually.

The bigger surprise at Wednesday's announcement and press conference by Chair Janet Yellen might come from the FOMC's revised economic projections. After this week's stronger-than-expected inflation data, a December rate hike is back in play. Therefore, any indication that Yellen is becoming more confident that inflation is heading back up again could fuel the dollar's gains from this week. More importantly, the Fed's latest dot plot chart should reveal whether or not FOMC members still expect to see a third rate hike this year and if there's been any change to their rate path prediction for 2018.

Weekly Market Outlook: FOMC, BoJ, & Norges Bank Policy Meetings

Next week's market movers

- The main event will probably be the FOMC policy meeting. Markets may focus on any potential changes to the "dot plot", as well as the timing of balance sheet normalization.

- In Japan, the BoJ is likely to keep its ultra-loose framework unchanged once again. That said, we expect a more upbeat tone from policymakers, amid encouraging economic developments.

- The Norges Bank is likely to stand pat as well. We suspect officials could appear a bit more concerned, given the latest slowdown in inflation, and could push slightly back the timing of their first planned rate hike.

- We also get key economic data from the Eurozone, the UK and Canada.

On Monday and Tuesday, the economic calendar is relatively light, with no major events or indicators coming out..

On Wednesday, the main event will be the FOMC policy announcement. This is one of the "bigger" meetings, meaning that besides the rate decision we will also get fresh economic forecasts for the US economy, an updated "dot plot", as well as a press conference by Chair Yellen. According to the Fed funds futures, the financial community is almost certain that policymakers will keep interest rates unchanged, and we agree with that given that inflation remained subdued in the aftermath of the latest meeting. Although August's data showed that both the headline and core CPI rates rebounded, we doubt that just a single data set will be enough to ease the concerns of those policymakers who believe that the latest softness in inflation is not due to idiosyncratic factors.

We believe that the market will place most of its emphasis on any signals regarding the beginning of the balance sheet normalization. Market chatter suggests that this process may start at this meeting or the next one, in October. As for our view, we don't expect the Bank to start the process now, but it could provide clear signals that this may happen in October. The risk to that view is officials leaving the language around that subject unchanged. Specifically, they could keep the part saying that the reduction will begin "relatively soon" in order to leave themselves some room for maneuvering if economic data continue to disappoint.

As for the forecasts, we will mainly focus on the "dot plot" to see whether the Committee as a whole continues to anticipate another rate increase this year. We expect the plot to still signal another hike this year. Although we got increasingly dovish comments last week, these remarks came mostly from members we suspect that they have already indicated they won't support additional hikes in 2017. As for the pace of future hikes, we believe that they may keep it untouched as well and wait to see whether the latest rebound in inflation will continue. If not, they may revise down the "dot plot" in December.

On Thursday, during the Asian day, the BoJ policy decision will be in the spotlight. With no forecast available, we see the case for the Bank to keep its QQE with yield-curve control framework intact once again, and to appear slightly more optimistic than previously. Economic developments since the latest BoJ meeting have been positive on every front. With regards to inflation, both the national and the BoJ's core CPI rates rose further in July, while the forward-looking Tokyo core CPI rate for August rose as well, suggesting that this recovery in inflation is likely to continue. Meanwhile, the unemployment rate declined further, while economic growth accelerated.

Given this cocktail of encouraging developments, we think the BoJ is likely to upgrade its language around the Japanese economy, and perhaps even revise up its economic forecasts. That said though, we still think it's too early for speculation regarding a potential reduction in stimulus in the near-term. Under its current framework, the Bank has explicitly committed not only to achieve its 2% inflation target, but to actually overshoot it. Thus, although the CPI rates rose somewhat, as long as they remain so far away from the target, we doubt any change in policy is looming.

During the European day, the Norges Bank will announce its own rate decision. When it last met, the Bank revised up its GDP forecasts for 2017, and even though it marked down its expectations for near-term inflation, it upgraded them for the long term. Perhaps the most notable change was that the Bank removed its easing bias and now expects the key policy rate to remain at the current level in the period ahead, while it revised slightly higher its expected rate path for 2017 and 2018.

Since then economic data have been mixed. The nation's GDP accelerated notably in Q2, which is in line with the Bank's forecast, while the unemployment rate slid further in August. On the other hand, inflation slowed in August, confounding expectations of rising. We don't expect the Bank to take any action at this meeting, neither to change its language. However, due to declining inflation, officials could push further back the timing of when they expect to start raising interest rates.

Finally on Friday, the economic indicators likely to attract market attention are Eurozone's preliminary PMIs for September, and Canada's CPI data for August.

Weekly Market Outlook: Low Key BoJ Meeting

- Low Key BoJ Meeting - Peter Rosenstreich

- BoE Hawkish Shift Changes The Game - Arnaud Masset

- Gold Consolidates And Bitcoin Takes A Serious Hit - Yann Quelenn

- Global High Dividends

FX Market - Low Key BoJ Meeting

The BoJ meeting should be an uneventful event. Despite the one-year anniversary of yield curve control (YCC), growing question of stability and political pressure, now is not the time for the BoJ to act. Governor Kuroda will likely keep the BoJs primary policy framework unchanged. In July, the BoJ decreased its inflation forecast, which in turns changed the time for reaching the banks well published 2% inflation target. The new date is a distant 2019 as inflation trajectory is far from their stated goal. July core CPI, which excludes only fresh foods, increased to 0.5% y/y, core CPI, a strong view of underlying inflation pressures, remained around 0%. Initially, YCC policy likely help to an acceleration of yen weakening in Q4 2016, but much more depreciation would be required to achieve the 2% goal and effect is now limited. Growth on the other hand has picked up with solid activity in 2Q as real GDP growth was 2.5% but spillover into prices have not materialized. So from a stated objective standpoint there is not rush to shift policy position. Recent communications from Kuroda indicates its too early to discuss exits strategies.

Markets will be focused on vote composition after the board members changes (Mr. Kataoka and Mr. Suzuki first meeting) and communication guidelines regarding JGB purchase operation (BoJ have decelerated JGB purchases per operation since mid-August). In addition, timing of the meeting will provide Kuroda a platform to discuss the FOMC. The JPY is now at the crossroads. YCC no longer pro-actively weakens the yen but does setup up environment allowing hawkish foreign central banks (ECB, BoE, Fed, BoC) shift toward normalization to drive JPY downwards. Events around N. Korea has created a safe haven buying rationale, yet in reality real yield differentials remains the primary driver of USDJPY pricing. However, political pressure on Abe could spill over into BoJ policy. Although the board is made up of policy doves a political changes could threaten the BoJ policy path. Without extraordinary measure, the JPY will likely appreciate.

Economics - BoE Hawkish Shift Changes The Game

It has climbed to multi-month amid volatile week as investors anticipate the Bank of England is about to reduce its support to the economy. However, prior to the BoE hawkish shift, the week was punctuated by the release of several key economic indicators. On the inflation side, an upside surprise in August CPI readings gave a first booster to the pound. It was followed by

The headline gauge printed at 2.9y/y versus 2.8% median forecast and 2.6% in the previous month. The core measure, which excludes the most volatile components, came in at 2.7%y/y versus 2.5% expected and 2.4% in July, suggesting that the tick up in fuel price is not the sole explanation. Indeed, the sharp depreciation of the pound sterling over the last few months impacted positively the cost of imported goods. Clothing and footwear component rose 4.6% over the last 12 months, contributing to 0.26 points to the CPIH rate (compared to -0.07 a year ago), while the surge in restaurant and hotels prices contributed to 0.35 points (compared 0.23 a year ago).

On the unemployment front, the July's jobs report added more impetus to the GBP bulls. The ILO unemployment rate fell to 4.3% July from 4.4% a month ago as employment change rose to 181,000 versus 150,000 median forecast and 125,000 in June. However, average weekly earnings stayed stable at 2.1%y/y versus 2.2% expected. The lack upside pressure in basic wage growth suggest that households' stalling disposable income won't accelerate the pick-up in inflation. In addition, the pound sterling has stabilised since the beginning of the year, if not recovered, and this would somehow eases the upside pressure in inflation stemming from the exchange rate.

Finally, the BoE took a more hawkish stance on Thursday and appeared ready to hike borrowing rates against the backdrop of an improving economic picture and most importantly stronger inflation. Prior to the BoE decision, we thought the central bank would take a more dovish stance and would rather emphasized the downside risk created by the Brexit situation. Nevertheless, it is clear now that the BoE believe the economy is strong enough to take a 25bps hike, regardless the potential negative effect a hard Brexit. In addition, it seems that the Brexit negotiations will take longer than expected and that UK lawmakers are finally to take a conciliatory tone and abandon the harsh rhetoric.

Economics - Gold Consolidates And Bitcoin Takes A Serious Hit

Gold has largely increased since the start of the year going from $1150 to $1350. The sharpest increase was during the summer. The decline of the dollar was largely followed by an increase in the precious metal. Now that central banks needs to deliver within the short-term (balance sheet normalization for the Fed, reduction of the asset purchase program for the ECB), we believe that there are more upside for the yellow metal as we consider that global economic conditions are clearly not good enough to support a change in the monetary policy.

Technically, gold is in a clear uptrend channel and as inflation is back in the US, this is another strong point regarding the potential appreciation of the commodity. Yet competition appears and gold, which is one great asset for storage of value is now competing against Bitcoin.

This year has been a great year for the first cryptocurrency so far. Debates are strong regarding the question if Bitcoin will become a safe haven. Jamie Dimon, JP Morgan Chase CEO, has declared that "Bitcoin is a fraud". Cryptocurrencies are a new asset class and the war between fiat money and cryptocurrencies will be on regulatory issues. Recently the People's Bank of China has triggered a sell-off in the whole cryptocurrency market by forbidding exchanges. Yet, rumours are stating that exchanges will be able to buy licenses in order to be allowed.

Needless to say that the power of money is not a power central banks are willing to let decentralize. Bitcoin took a hit since this comment. Other would also say that China and its ICO ban are weighing on the most famous cryptocurrency. Further downsides are happening but Bitcoin still has a lot of potential. Only less than 0.01% of the global population has a bitcoin wallet.

If this would reach 1%, the demand for Bitcoin would skyrocket, knowing that there are only 18 million coins available at the moment.

Themes Trading - Global High Dividends

Dividends are set to become increasingly important to global investors. Over the past century, dividends have accounted for approximately 50% of total returns earned by investors. Should stock returns flatten, it will be expected dividends that will likely drive growth for investors. This means that in today's low-yield and low-volatility environment, the stability of dividend-paying stocks with historical total return characteristics has been in high demand.

Companies selected for this theme provide investors with geographical and industry perspective diversification, while offering the potential for capital appreciation and reliable income. This theme attempts to avoid the `dividend trap' by focusing on companies that have delivered consistent dividend growth with limited share price volatility.

IMPORTANT

The subscription period opens on September 12 and will run until September 25, 2017. This means the price will not move until September 25, the date on which the initial allocation will be made. Do not hesitate to contact us if you have any questions.

Weekly Focus: Riksbank May be Next to Join ‘Exit Camp’

Market Movers ahead

We look for the FOMC to announce "quantitative tightening" and signal one more rate hike this year when it meets on Wednesday.

We expect EUR manufacturing PMI to show a slight drop from the current strong level as the stronger euro is likely to weigh a bit on euro exports. We also look for a small decline in the German ZEW index.

Chinese house price inflation for August is likely to show a further moderation as tightening measures are starting to dampen home sales and prices.

Bank of Japan: we expect it to keep its policy stance unchanged.

In Scandinavia, the Riksbank's minutes should give more insight into how close the bank is to joining the 'exit' camp. We don't expect any rate change or change to the rate path from Norges Bank at its meeting on Thursday.

Global macro and market themes

Central bankers look increasingly divided into those in the 'exit' camp (Fed, BoE, ECB), those in the 'no exit camp' (BoJ, SNB), and those in between (Riksbank, Norges Bank).

While the Fed looks determined to hike in December, it is unlikely to drive a major selloff in EUR/USD.