Sample Category Title

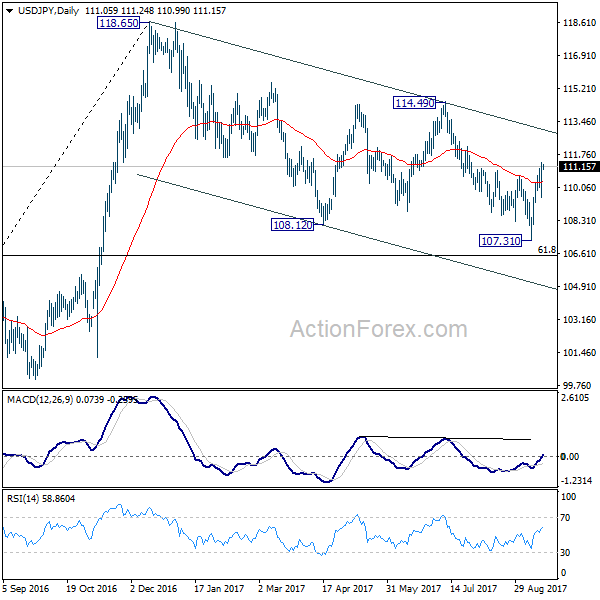

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.79; (P) 110.56; (R1) 111.59; More...

Intraday bias in USD/JPY remains on the upside for the moment. Fall from 114.49 should have completed at 107.31 already. Further rally would be seen for medium term channel resistance (now at 112.91). Sustained break there will argue that whole correction from 118.65 has completed too. In that case, further rise should be seen to 114.49 resistance for confirmation. On the downside, below 109.54 minor support will turn bias back to the downside for 107.31 instead.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

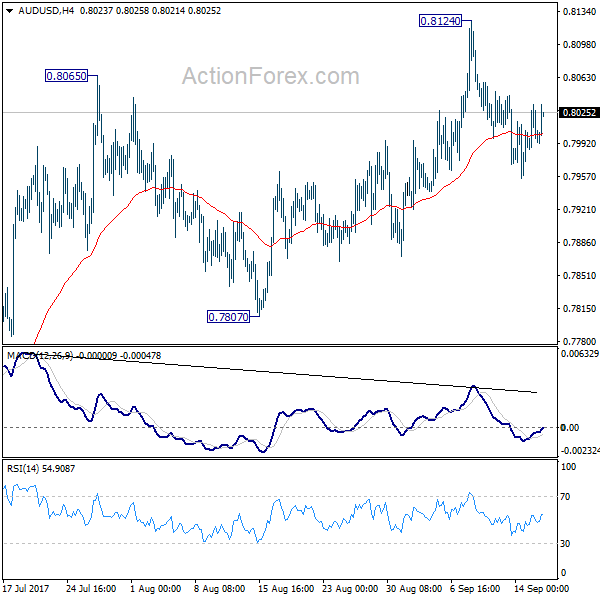

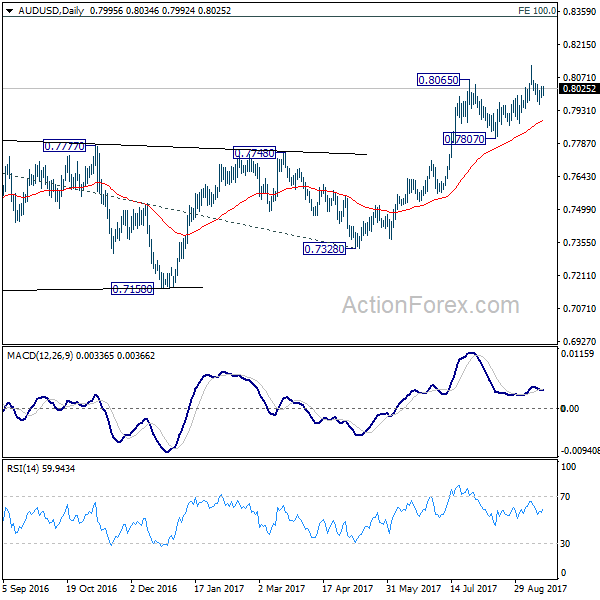

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7979; (P) 0.8007; (R1) 0.8028; More...

Intraday bias in AUD/USD remains neutral as correction from 0.8124 is still in progress. Deeper fall could be seen. But still, with 0.7807 support intact, near term outlook stays bearish and another rise is expected. Break of 0.8124 will turn bias to the upside and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335 next. However, considering bearish divergence condition in 4 hour MACD, firm break of 0.7807 will indicate near term reversal and turn bias back to the downside for 0.7328 key support.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8090) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7807 support is needed to to be the first sign of completion of the rebound. Otherwise, further rise is now in favor.

Weekly Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

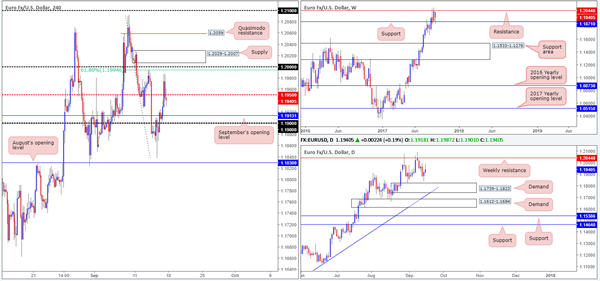

EUR/USD

Weekly gain/loss: – 94 pips

Weekly closing price: 1.1940

Over the past three weeks, upward momentum has somewhat diminished thanks to the weekly resistance pegged at 1.2044. Despite this, weekly bulls managed to chalk up a mild end-of-week correction last week from weekly support seen below at 1.1871, possibly encouraging buyers into the market. In addition to this, we can see that weekly price over on the USDX formed a nice-looking bearish pin bar off resistance at 11854, and shows room to move down to at least weekly support at 11687 (converges with a long-term weekly trendline support etched from the low 9322).

Since the 29th August, the daily candles have been consolidating between the noted weekly resistance level and a demand coming in at 1.1739-1.1823. Looking at the USDX daily timeframe, however, there's a possibility that we may see further selling from resistance at 11868, as the next area of interest does not come into view until the 11681-11749 neighborhood (fuses with a channel support taken from the low 12352). As such, this could pressure the EUR up to the weekly barrier sometime this week.

A quick look at recent dealings on the H4 timeframe show US retail sales figures contracted on Friday, immediately forcing the pair higher. As you can probably see though (check the M30 chart), price quickly stalled following the move and began paring gains. Trade concluded with the piece closing below the H4 mid-level support logged at 1.1950.

Suggestions: For ease, let's just recap what we have here:

Weekly price seen within moderate range – weekly USDX shows possible selling on the cards, which could force EUR higher.

Daily, at current price, is positioned mid-range with price likely heading higher to retest weekly resistance, thanks largely to USDX daily action pointing to the possibility of further selling.

H4 closed sub 1.1950. Next downside target located at September's opening level drawn from 1.1913, followed closely by the 1.19 handle.

So, with the above in mind, our team has absolutely no interest in shorting sub 1.1950.

Although both weekly and daily price suggest buys, nevertheless, traders may want to note the large psychological number 0.80 lurking above. Not only is this a watched number, but it is also bolstered by a strong-looking H4 supply just above it at 1.2029-1.2007 and a nearby H4 61.8% Fib resistance at 1.1994 taken from the high 1.2092. For that reason, we have to be prepared for a possible bounce lower from here. Why we only expect a bounce should be obvious: the higher timeframes!

To trade any bounce seen from 0.80, we would highly recommend drilling down to the lower timeframes to secure a tighter entry (see the top of this report for information on how to do this). This will likely help with risk/reward should price reverse before reaching 1.1950.

Data points to consider: EUR Final CPI figures y/y at 10 am GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.80 region ([waiting for a lower-timeframe entry signal to form is advised] stop loss: dependent on where one confirms this area).

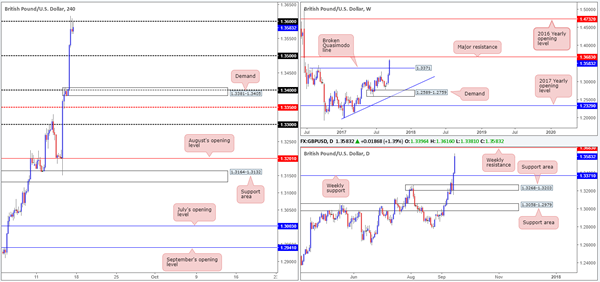

GBP/USD:

Weekly gain/loss: + 395 pips

Weekly closing price: 1.3583

Cable printed another impressive weekly candle last week, consequently breaking through the weekly Quasimodo resistance level at 1.3371 and landing the unit within touching distance of a major resistance coming in at 1.3683 (seen as far back as 2001). With USDX weekly action printing a bearish pin bar last week from resistance at 11854, there's a strong possibility GBP resistance will come into play this week. Looking down to the daily timeframe, there's not really much to add except that the USDX daily candles show further selling could be seen down to demand at 11681-11749 (fuses with a channel support taken from the low 12352).

Reviewing Friday's movement on the H4 timeframe reveals that the pound surged higher on Friday, after BoE policy maker Gertjan Vlieghe, a usual dove, signaled a shift in the BoE's bias towards an interest-rate hike. The pair, after trading nearly 200 pips on the day, eventually found some refuge at the 1.36 handle going into the closing bell.

Suggestions: Though there are three beautiful-looking H4 selling wicks in view from 1.36, this would be a challenging sell. Aside from strong sentiment, price may want to push up to the aforesaid weekly resistance before any serious sellers begin making a play. As a result, the desk will be watching for 1.36 to give way. Should this occur and price retests the number as support, followed by a full, or near-full-bodied bull candle, we would look to long this market up to the 1.3680 neighborhood.

Data points to consider: No high-impacting events on the docket today.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf 1.36 and then look to trade any retest seen thereafter ([waiting for a H4 confirming bull candle to form following the retest is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

AUD/USD:

Weekly gain/loss: – 55 pips

Weekly closing price: 0.7999

On the whole, the commodity currency remains entrenched within a relatively strong uptrend at the moment. However, weekly price does show bearish intent being seen from resistance penciled in at 0.8075, but whether it'll be sufficient enough to half further buying is difficult to judge. Above the current resistance is another resistance level at 0.8224, seen converging with two trendline resistances (0.9757/0.7722).

Turning our attention to the daily candles, the pair is currently seen meandering between the noted weekly resistance and a support level drawn from 0.7955. A violation of this daily level would likely pressure the major back down to demand coming in at 0.7786-0.7838 (seen positioned within the walls of a weekly support area at 0.7849-0.7752 – the next downside target on the weekly scale).

During the course of Friday's sessions H4 price reclaimed the large psychological level 0.80, following a somewhat decisive move lower from supply marked at 0.8044-0.8028. Aside from this being a widely watched number and converging with August's opening level at 0.7998, this is not a level we expect price to reverse from. The team actually favors the 0.7950 neighborhood for longs due to the following points:

Daily support lodged at 0.7955.

Just below 0.7950 there is a strong-looking H4 demand base at 0.7921-0.7946.

Nearby September's opening level at 0.7939.

61.8%78.6% H4 Fib supports at 0.7928/0.7925.

H4 trendline support etched from the low 0.7807.

Suggestions: Given that the H4 demand is located only a few pips below daily support, this would be an ideal area to buy, in our humble view. Not only would a move down to this area likely trigger stops from below daily support and the H4 mid-level support, it would also be a trade in line with the underlying trend and therefore could print a substantial move higher. Of course, the only grumble here is the current weekly resistance, but given the confluence bolstering a long, we feel a buy is worth the risk.

Data points to consider: No high-impacting events on the docket today.

Levels to watch/live orders:

- Buys: 0.7939 ([pending order] stop loss: 0.7918).

- Sells: Flat (stop loss: N/A).

USD/JPY:

Weekly gain/loss: + 300 pips

Weekly closing price: 110.83

After clipping the top edge of a weekly support area at 105.19-107.54, USD/JPY bulls staged an aggressive recovery last week, completely engulfing the prior week's losses. Although the USDX formed a bearish pin bar from weekly resistance at 11854 last week, the path north on the USD/JPY appears reasonably free up to as far as the weekly supply area punched in at 115.50-113.85.

Daily resistance at 110.76, as you can see, suffered a rather brutal blow on Friday as price struck highs of 111.32. While a marginal close was printed above this line, it is very difficult to judge whether this is enough to spark further buying on this scale up to resistance planted at 111.91/61.8% daily Fib resistance at 111.77.

A quick recap of Friday's movement on the H4 timeframe shows price failed to sustain gains beyond the 111 handle, largely influenced by lower-than-expected US Retail sales. Although the move generated seller interest, there wasn't much follow-through action seen. This was, as far as we can see, due to the US consumer sentiment index measured by Reuters/Michigan coming in a 95.3 against an expected reading of 95.1.

Suggestions: The H4 selling wicks chalked in around 111 have likely stirred candlestick traders – but we would advise treading carefully here! Both weekly and daily price suggest that further upside may be on the horizon. Therefore, we have absolutely no plans to sell this market anytime soon. In fact, similar to the GBP analysis above, we will be watching for the H4 candles to run above 111 and hold firm as support. Should this occur and price prints a full, or near-full-bodied bull candle following the retest, we would look to long this market up to the 111.80ish area (see daily resistances noted above).

Data points to consider: Japanese banks will be closed in observance of Respect-for-the-Aged Day. No US events on the docket today.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf 111 and then look to trade any retest seen thereafter ([waiting for a H4 confirming bull candle to form following the retest is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

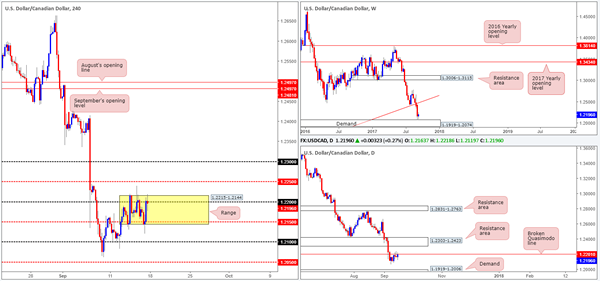

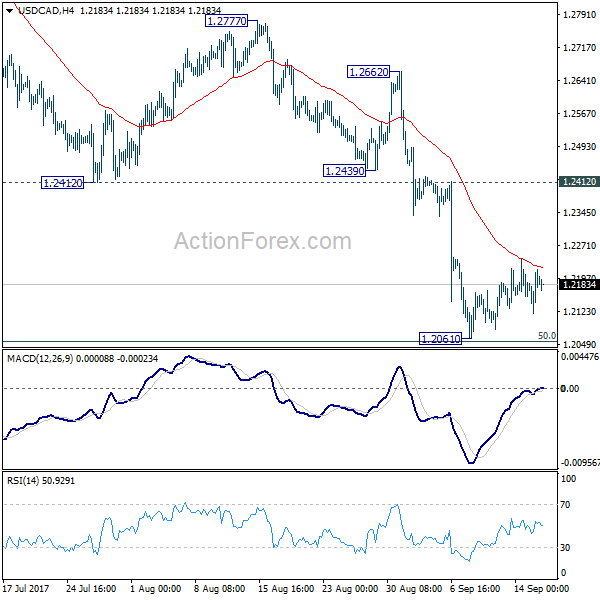

USD/CAD:

Weekly gain/loss: + 40 pips

Weekly closing price: 1.2196

The USD/CAD closed marginally stronger last week after crossing paths with weekly demand fixed at 1.1919-1.2074. Why we have not seen a more explosive move transpire from here, at least from a technical standpoint, likely comes down to three things:

The strong downtrend that has been in play since the beginning of May. Notice price only managed to correct once over five months, and this only lasted two weeks!

There is also the fact that daily price is seen capped below a broken Quasimodo line at 1.2201. What's more, a break above here will only free price up to nearby resistance area at 1.2303-1.2423.

Weakness seen from USDX weekly resistance at 11854 – notice last week's selling wick and room to move lower.

Moving across to the H4 timeframe, we can see that the pair dipped to a fresh session low of 1.2119 on Friday following a disappointing US retail sales print. Price did, however, manage to recover relatively quickly, posturing itself back above the mid-level support 1.2150 and rallying to the 1.22 handle into the close. The other key thing to note here is the clear range that has been forming since the 13th September between 1.2215-1.2144 (yellow area).

Suggestions: On the account of weekly and daily structure, this is a somewhat difficult market to trade at this time. Yes, the overall trend is facing south, but we don't want to become a seller when a weekly demand is in play!

Even with a decisive close above the current H4 consolidation, buyers then have to contend with potential offers from the H4 mid-level resistance 1.2250. It will only be once this line is cleared will the path north be clear up to the 1.23 neighborhood, which also happens to intersect with the underside of the aforementioned daily resistance area. So, intraday longs could be a possibility above 1.2250 up to 1.23. With that being said, nevertheless, do consider the risk/reward element here. Try to pin down a setup that'll allow for at least two times your risk. If not, it might be worth passing.

Data points to consider: No high-impacting events on the docket today.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf 1.2250 and then look to trade any retest seen thereafter (stop loss: ideally beyond the rejection candle's tail).

- Sells: Flat (stop loss: N/A).

USD/CHF:

Weekly gain/loss: + 152 pips

Weekly closing price: 0.9590

The weekly support area at 0.9443-0.9515, as you can see, remains in play. Irrespective of last week's end-of-week correction, if the bulls push higher this week this could see the unit challenge a weekly trendline resistance extended from the low 0.9257. One other thing to keep in mind here though is weekly USDX price sold off from resistance at 11854 last week and printed a strong-looking selling wick.

Turning our attention to the daily timeframe, Thursday's movement chalked up a nice-looking bearish selling wick around supply penciled in at 0.9699-0.9641, which encouraged further selling on Friday and placed price within striking distance of support at 0.9546. Also of particular interest is the daily USDX showing space to trade down to demand at 11681-11749 (fuses with a channel support taken from the low 12352).

Looking at Friday's action on the H4 timeframe, price settled for the week just beneath the 0.96 handle, following a modest bid from demand pegged at 0.9546-0.9568 (sits on top of the daily support mentioned above at 0.9546). A sell from current price would be challenging not only because of the aforesaid demand, but also July's opening level at 0.9580. A long above 0.96 on the other hand may be something to consider, but the move may only be good for 30 pips up to nearby supply at 0.9647-0.9633.

Suggestions: Personally, we do not see much to hang our hat on here at the moment, and as such, remaining on the sidelines may be the better route to take today.

Data points to consider: No high-impacting events on the docket today.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

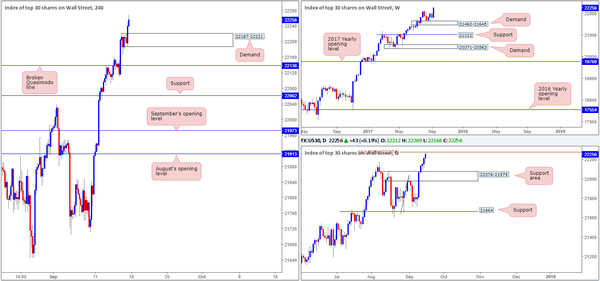

DOW 30:

Weekly gain/loss: + 448 points

Weekly closing price: 22256

After price struck weekly demand at 21462-21645 five weeks ago, US equities eventually printed a fresh record high of 22256 last week. With absolutely no overhead resistance on the horizon, further buying could be seen this week. On the whole, traders have largely shrugged off latest North Korean tensions and the terrorist attack in London.

Down on the daily timeframe, nonetheless, we may see the index correct should price join with the 161.8% Fib ext. point at 22274 extended from the low 21645. On this scale, the next downside support target can be seen at 22076-21979.

In the event that price reverses from record highs today, the H4 demand zone at 22187-22221 will be the first port of call to keep an eye on. A violation of this area, however, likely opens the door for a test of the broken Quasimodo line at 22138, which happens to sit just above the noted daily support area.

Suggestions: As far as we're concerned, this is a buyers' market right now .Therefore, we'll be watching both the above said H4 supports for possible buying opportunities today. To be on the safe side though, waiting for a H4 bull candle to form, preferably in the shape of a full, or near-full-bodied candle, before pulling the trigger may be best, since it is difficult to know which of the two areas will hold, if any at all.

Data points to consider: No high-impacting events on the docket today.

Levels to watch/live orders:

- Buys: 22187-22221 ([waiting for a reasonably sized H4 bullish candle to form – preferably a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle's tail). 22138 ([waiting for a reasonably sized H4 bullish candle to form – preferably a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

GOLD:

Weekly gain/loss: – $26.3

Weekly closing price: 1319.7

Following a rather decisive close above weekly resistance at 1337.3, which connected with a channel resistance extended from a high of 1295.4, the bulls generated little to no follow through last week. In fact, price erased all of the prior week's losses and now looks poised to challenge nearby support coming in at 1295.4.

On the other side of the field, daily action closed the week out forming a near-full-bodied bearish candle, and has firmly positioned price just ahead of support coming in at 1308.4 (unites with a trendline support extended from the low 1205.0).

Across on the H4 timeframe, the unit ended the week marginally closing beyond September's opening level at 1320.4. To our way of seeing things, the majority of buyers here are already likely consumed given the large consumption tail seen marked with a black arrow at 1315.4, thus the door down to the noted daily support is wide open, followed closely by a H4 Quasimodo support logged in at 1304.9.

Suggestions: Put simply, a short trade could be possible on any retest seen at September's opening level today, targeting the daily support. Our only concern is that weekly USDX price shows price selling off from resistance at 11854 in the shape of selling wick. Therefore, it may be worth waiting for a H4 bearish candle to form following a retest of 1320.4, before committing to a trade.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1320.4 region ([waiting for a reasonably sized H4 bearish candle to form – preferably a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle's wick).

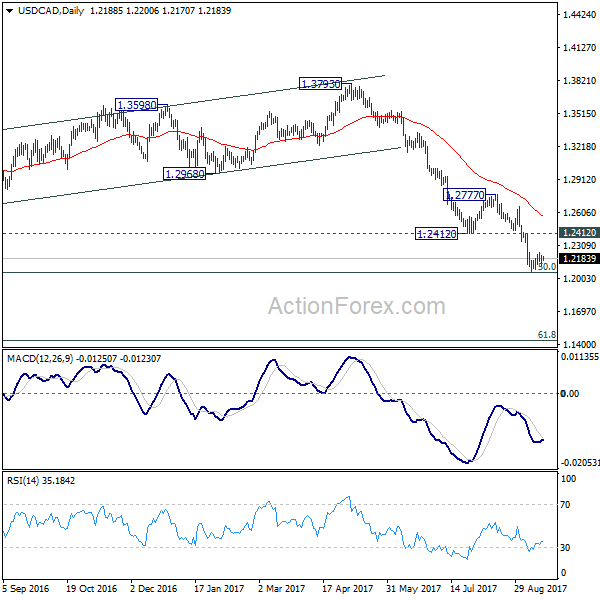

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2175; (R1) 1.2234; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.2061 temporary low continues. The corrective price actions so far suggests that larger decline is not completed yet. And firm break of 1.2049 key fibonacci level will pave the way to next fibonacci level at 1.1424. Still, we'd remain cautious on strong support from 1.2048 to bring sustainable rebound. But still, break of 1.2439 support turned resistance is needed to be the first sign of trend reversal. Otherwise, outlook will remain bearish.

In the bigger picture, current downside acceleration is raising the chance that whole long term rise from 0.9406 (2011 low), and that from 0.9056 (2007 low) is completed at 1.4689. Focus is now on 50% retracement of 0.9406 to 1.4869 at 1.2048. As long as this level holds, we'd still favor that case that fall from 1.4689 is a correction. However, firm break of 1.2048 will indicate that fall fro 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Politics and Central Banks to Drive the Markets This Week

Politics and central bank events will be the main drivers in the markets this week, with economic data taking a back seat. FOMC policy decisions and press conference is one of the main highlights. Fed is expected to finally announce unwinding of its USD 4.5T balance sheet. But spotlight will first be on BoE Governor Mark Carney's speech at IMF in Washington. Markets will look to Carney for his view on the chance of a November hike. Meanwhile, Germany and New Zealand will have their general elections the coming weekend. Talking about elections, Japan Prime Minister Shinzo Abe might announce to dissolve the Lower House and call for a snap election. UK Prime Minister Theresa May will deliver a Brexit speech in Italy on Friday. And there could be more verbal exchanges out of UK and EU ahead of the fourth round of Brexit negotiation starting next week. And, let's not forget also US President Donald Trump will address the United Nations in New York on Tuesday when North Korea tensions are still present. Trump is given a chance to confront North Korean representative face-to-face.

Merkel's CDU maintains lead according to latest poll

Ahead of the German election on September 24, latest poll reported by Bild am Sonntag showed that Chancellor Angela Merkel's Christian Democratic Union (CDU) is maintaining solid lead at 36%. Rival Social Democratic Party (SPD) follows at 22%. Meanwhile, far right anti-immigrant Alternative for Germany (AfD) is staying as the strongest among the "small parties", at 11%, staying in the third place. The Left, Free Democrats (FDP), and the Green are at 10%, 9% and 8% respectively. It's believed that with double digit support, AfD will very likely enter German parliament after the election. That will be the first presence of a right-wing party in the Bundestag in over half a century. According to the poll, 58% said that Merkel's policies were partially responsible for the rise of the nationalist party AfD. Meanwhile, as FDP is likely to re-enter into the Parliament, FDP, Greens and the CDU could eventually form a so called "Jamaica coalition".

Kiwi to stay volatile on polls

New Zealand dollar trades mildly higher today but indecisiveness could remain ahead of the general election on September 23. The election is described by many as the closest contest in more than a decade. And so far, reactions show that Kiwi will dip whenever the opposition Labour Party is running ahead in polls. On the other hand, Kiwi will be lifted if ruling National Party is leading. Markets generally perceive that a change of government to Labour as a negative event. And analysts noted that the markets are not against the Labour, but just against change.

Japan PM Abe considering to call for snap election

In Japan, it's reported that Prime Minister Shinzo Abe is considering to dissolve the Lower House and call for a snap election, as early as in late October. Abe's approval rating sunk earlier this year and broke 30% mark in July on alleged scandals of government favoritism. However, the rising tensions with North Korea helped and lifted the rating back above 50%. A cabinet reshuffle in August also helped improved his popularity. Abe will be ending his term as ruling Liberal Democratic Party president next September. But an early election at the current time would help the party in extending theirs power beyond that.

Looking ahead

FOMC policy decision and press conference on September 20 will be a major focus. The Fed would formally announce the schedule of the long-awaited normalization of its US$ 4.5 trillion balance sheet. At the Addendum to the Committee's Policy Normalization Principles and Plans released in June, Fed indicated how it intends to gradually reduce the balance sheet. We expect more details including the formal start day would be announced this week. Inflation has remained persistently soft despite the upside surprise in the August data. We believe some members would raise concerns that weak price levels might last longer than previously anticipated. There might be downward revisions in the inflation forecast in 2018. Meanwhile, there are some speculations that the Fed might reduce its average Fed funds rates projections.

RBA would release the minutes on September 19. The central bank left the cash rate unchanged at 1.5% in September. While remaining confident over the economic outlook, the members warned of the recent appreciation in Australian dollar. We do not expect much news from the minutes. BoJ will also meet this week and it will likely be a non-event.

Here are some highlights for the week ahead:

- Monday: Eurozone CPI final; Canada foreign securities transactions; US NAHB housing index

- Tuesday: RBA minutes, Australia house price; German ZEW economic sentiment; Canada manufacturing sales; US housing starts and building permits, current account, import price

- Wednesday: New Zealand current account; Japan trade balance; German PPI; UK retail sales; US existing home sales, FOMC rate decision and press conference

- Thursday: BoJ rate decision; New Zealand GDP; Swiss trade balance, SECO economist forecasts; ECB bulletin; UK public sector net borrowing; US jobless claims, Philly Fed survey; Canada wholesale sales

- Friday: Eurozone PMIs; Canada CPI, retail sales; US PMIs

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2175; (R1) 1.2234; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.2061 temporary low continues. The corrective price actions so far suggests that larger decline is not completed yet. And firm break of 1.2049 key fibonacci level will pave the way to next fibonacci level at 1.1424. Still, we'd remain cautious on strong support from 1.2048 to bring sustainable rebound. But still, break of 1.2439 support turned resistance is needed to be the first sign of trend reversal. Otherwise, outlook will remain bearish.

In the bigger picture, current downside acceleration is raising the chance that whole long term rise from 0.9406 (2011 low), and that from 0.9056 (2007 low) is completed at 1.4689. Focus is now on 50% retracement of 0.9406 to 1.4869 at 1.2048. As long as this level holds, we'd still favor that case that fall from 1.4689 is a correction. However, firm break of 1.2048 will indicate that fall fro 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Sep | -1.20% | -0.90% | ||

| 9:00 | EUR | Eurozone CPI M/M Aug | 0.30% | -0.50% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Aug F | 1.50% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Aug F | 1.20% | 1.20% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jul | 4.46B | -0.92B | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 67 | 68 | ||

| 20:00 | USD | Net Long-term TIC Flows Jul | 42.3B | 34.4B |

Potential For A Cut And Reverse In AUD/NZD

When a higher time frame level fails, the setup doesn't have to be discarded. If the higher time frame level is strong, don't ever discount a cut and reverse strategy to play the level from the opposite side.

We have one such example of this strategy playing out on the AUD/NZD chart today.

AUD/NZD Daily:

The daily chart shows the key AUD/NZD level that's in play. As you can see, price has broken higher through the zone formed by previous swing high resistance, and then pulled back to retest it on the other side.

But after failing to make a new higher high, price has dropped straight to the bottom of the zone and is looking like going straight through on momentum.

AUD/NZD Hourly:

Now zooming into an intraday chart with a look at the hourly, I've drawn up the price action that I was describing above. The green markings represents short term resistance turned support, while the red represents the shot term support turned resistance.

With the initial long failing to make a higher high, shorts now comes into play. Aggressive traders would manage their risk around the short term level, while more conservative shorters will place their stops above the higher time frame level.

Market Morning Briefing: The Aussie Has Obliged By Moving Up To Our Target Of 0.8025

STOCKS

Dow (22268.34, +0.29%) looks strongly bullish just now and has been rising fast targeting 22400-22500 levels in the near term. Dax (12518.81, -0.17%) on the other hand is stable below 12600. A break on the upside could take it higher towards 12750-13000 levels in the coming sessions.

Nikkei (19909.50, +0.52%) could test 20050 on the upside before again coming off from there. Near term looks bullish followed by a dip or sideways consolidation for sometime. While Dollar Yen trades higher, Nikkei could continue to remain bullish in the near term.

Shanghai (3364.14, +0.31%) has bounced back from levels near 3350 and while that holds, we may see a rise towards 3400 in the near term. A break below 3350, if seen could take the index lower towards 3325. Need to watch price action at current levels.

Nifty (10085.40, -0.01%) could possibly remain trapped within 10050-10140 region for a couple of more sessions. Thereafter preference is for a fall towards 9950 before again rising afresh towards 10150.

COMMODITIES

Brent (55.72) has been rising in line with our expectations and could rise towards 56.65 in the coming sessions. WTI (49.91) is stable just now and could possibly trade sideways for a couple of sessions before moving up towards 51. Near term is likely to remain bullish.

Gold (1318) and Silver (17.598) have risen slightly compared to previous levels. But overall the precious metals do not look very strong just now. For Gold 1320-1315 levels are important and if it breaks on the downside, we may expect a test of 1300-1296 in the coming sessions. Silver is also testing support at current levels. While that holds, the price could bounce back towards 17.50-18.00 else we will have to focus on lower levels.

Copper (2.98) is trading at immediate support near 2.95. In case that holds, we may expect a bounce back towards 3.05 or even higher. Watch price action near current levels.

FOREX

Dollar Index (91.85) pushed lower by strong rise in the Pound (1.3596) and stability in the Euro (1.1949) despite weakness in the Yen (111.21).

As expected, the Euro (1.1949) rose again on Friday, seeing a high near 1.1987. Two possibilities from here - either further sustained rise past 1.2035-50, or range trade between 1.2000 and 1.1850. The first three days may be quiet, waiting for the FOMC on Wednesday.

Further strong rise in the Pound (1.3596) on Friday to a high of 1.3616, breaking strongly above our projected resistance at 1.3415-65. We're not sure where the Pound will go from here, but it would be good to watch Resistances on the UK Gilt yields (see Interest Rates below) for clues.

Dollar-Yen (111.21) rose past our projected range high of 110.70 on Friday to a high of 111.33. Going forward, if it now rises further past 111.50, it would have potential to rise towards 113.50 as well. Otherwise, it could dip back to 110.50 or lower. Watch for a couple of days. Weakness in the Yen has pulled Euro-Yen (132.85) higher, past the resistance at 132 that was holding for most of last week. There is another crucial Resistance near the current level. Let us see how it behaves today.

The Aussie (0.8027) has obliged by moving up to our target of 0.8025. Look for further strength towards 0.8060 this week.

Dollar-Yuan (USDCNY = 6.5469) looks poised to rise towards 6.5750 enroute to 6.60, which may take some time. As expected, Dollar-Rupee (64.0750) continues to trade sideways and might even dip a bit towards 64.02 today on account of the dip in the Dollar Index.

INTEREST RATES

Although UK Gilts have shot up since last Thursday, after the BOE meeting, there are crucial Resistances near the current levels on the UK 10Yr (1.30%) and near 0.75% on the UK 5Yr (0.72%). These need to be watched for a couple of days at least. Note, at the same time, that the UK Libors have also moved up since Thursday.

The US FOMC comes up Wednesday and the BOJ meeting is on Thursday. For now, Resistance at 2.80% is holding well on the US 30Yr (2.77%) and the 10Yr (2.20%) is also not looking very perky. These depict the market's lack of conviction about the Fed's intentions to hike rates. However, given that the US CPI (1.93%) has moved up again and that Brent (55.73) trades higher, we would think that the Fed may be more likely to lean towards tightening, and even talk about balance sheet normalisation.

The Japanese 10Yr (0.01%) looks well set to continue to respect its long-term trend Resistance coming down from levels just below 1.90% in March 2008.

The German-US 10Yr Spread (-1.77%) continues to hold above -1.79%, and is supportive of Euro strength overall.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push lower last week bottomed at 1.1837 but closed higher at 1.1947. The bias is neutral in nearest term but as long as stay above 1.1823 key support the major bullish trend should remain strong with nearest bullish target seen around 1.2175 region. Immediate support is seen around 1.1900 – 1.1870 area. Immediate resistance is seen around 1.2000. A clear break and daily close above that area could trigger further bullish pressure testing 1.2100 – 1.2175 region. On the downside, a clear break and daily close below 1.1823 key support would take price to a bearish correction zone testing 1.1700 – 1.1600 region.

GBPUSD

The GBPUSD continued its bullish momentum last week, topped at 1.3616. Price is moving strongly above the EMA 200 on H1, H4 and daily chart suggests a valid and strong bullish trend. The bias remains bullish in nearest term testing 1.3700 – 1.3750 area. Immediate support is seen around 1.3500. A clear break below that area could lead price to neutral zone in nearest term testing 1.3450 – 1.3400 region but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy.

USDJPY

The USDJPY had a strong bullish momentum last week slipped above 111.00 key resistance area as you can see on my H4 chart below. This fact changes my H4 chart technical bias to a neutral condition. The bias is bullish in nearest term testing 112.15 area. Immediate support is seen around 110.50. A clear break below that area could lead price to neutral zone in nearest term as direction would become unclear. Overall I remain neutral.

USDCHF

The USDCHF attempted to push higher last week topped at 0.9703 but closed lower at 0.9595. We have a bearish pin bar formation on daily chart as you can see on my daily chart below suggests a bearish scenario. The bias is bearish in nearest term testing 0.9525 area. A clear break and daily close below that area would expose 0.9450 key support which remains a good place to buy with a tight stop loss. Immediate resistance is seen around 0.9650. A clear break above that area could lead price to a neutral zone in nearest term as direction would become unclear.

USDCHF – Remains Vulnerable, Faces Further Downside Pressure

USDCHF - With the pair following through lower on the back of Thursday losses on Friday, more decline is envisaged as enter a new week. On the downside, support lies at the 0.9550 level. A turn below here will open the door for more weakness towards the 0.9500 level and then the 0.9450 level. On the upside, resistance resides at the 0.9650 level where a break will clear the way for more strength to occur towards the 0.9700 level. Further out, resistance comes in at the 0.9750 level. Above here if seen will turn attention to 0.9800. All in all, USDCHF faces further downside pressure.

GOLD – Targets Further Weakness Towards Psycho Support At 1,300.00 Zone

GOLD - The commodity closed lower the past week to open the door for more weakness. On the downside, support comes in at the 1,310.00 level where a break will turn attention to the 1,300.00 level. Further down, a cut through here will open the door for a move lower towards the 1,290.00 level. Below here if seen could trigger further downside pressure targeting the 1,280.00 level. Conversely, resistance resides at the 1,330.00 level where a break will aim at the 1,340.00 level. A turn above there will expose the 1,350.00 level. Further out, resistance stands at the 1,360.00 level. All in all, GOLD looks to weaken further.