Sample Category Title

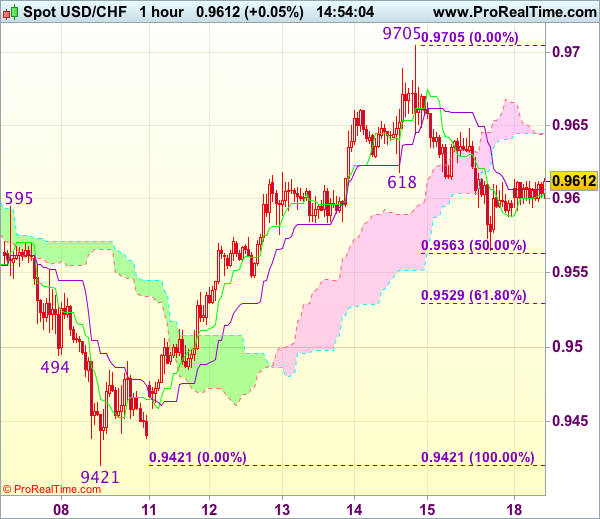

Trade Idea : USD/CHF – Sell at 0.9645

USD/CHF - 0.9612

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9605

Kijun-Sen level : 0.9602

Ichimoku cloud top : 0.9645

Ichimoku cloud bottom : 0.9645

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

Although the greenback has recovered after finding support at 0.9565 on Friday and consolidation above this level would be seen, if our view that top has been made at 0.9705 last week is correct, reckon upside would be limited to minor resistance at 0.9648 and bring another decline later, below 0.9563-65 (50% Fibonacci retracement of 0.9421-0.9705 and said support) would extend weakness to 0.9525-30 (61.8% Fibonacci retracement), however, downside should be limited to 0.9500 and 0.9480-85 should hold.

In view of this, would not chase this fall here and would be prudent to sell dollar again on further recovery as 0.9648 should limit upside. Above 0.9680 would risk retest of said last week’s high at 0.9705, break there would extend recent rise from 0.9421 to 0.9740-50 later.

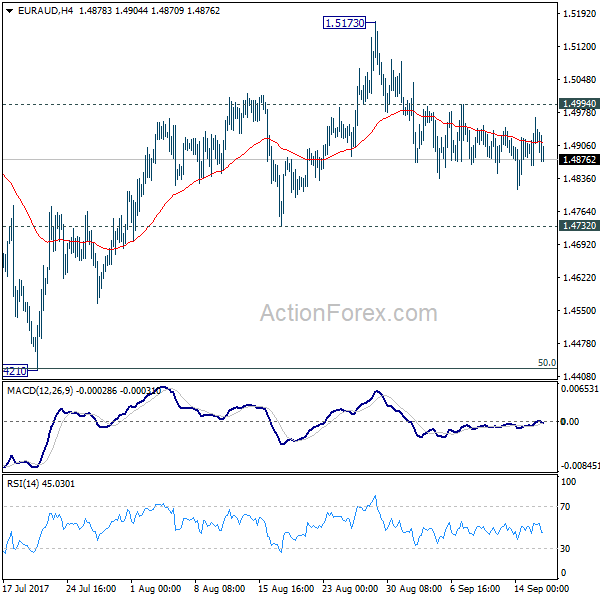

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4865; (P) 1.4916; (R1) 1.4968; More....

Intraday bias in EUR/AUD remains neutral for the moment. Another fall is mildly in favor as long as 1.4994 minor resistance holds. Break of 1.4732 will confirm that fall from 1.5173 is the third leg of consolidation pattern from 1.5226. In that case, further fall should be seen to 1.4421 again. But we'd expect strong support from there to contain downside and bring rebound. On the upside, above 1.4994 minor resistance will turn bias back to the upside for 1.5173/5226 resistance zone instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

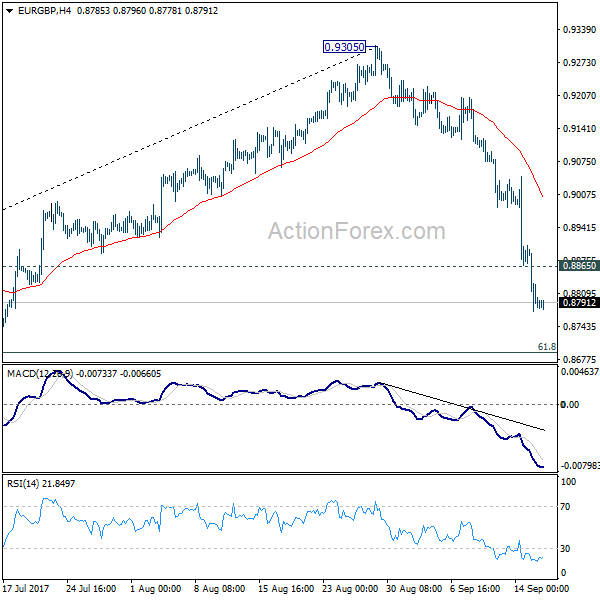

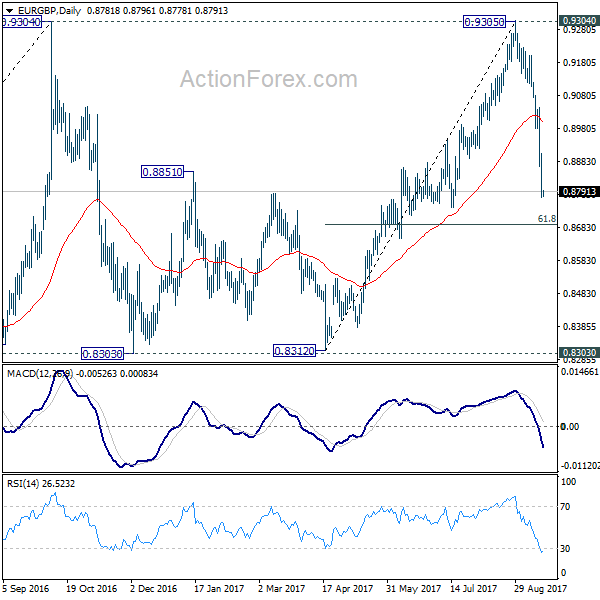

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8740; (P) 0.8822; (R1) 0.8872; More

Intraday bias in EUR/GBP remains on the downside for 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. Fall from 0.9305 is seen as the third leg of the consolidation pattern from 0.9304. We'll look for bottoming signal again at it approaches 0.8303 support. On the upside, above 0.8865 minor resistance will turn intraday bias neutral and bring recovery, before staging another fall.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Aussie Dollar Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.8006 on Friday.

LME Copper prices rose 0.6% or $38.5/MT to $6457.0/MT. Aluminium prices rose 0.2% or $3.0/MT to $2068.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.8027, with the AUD trading 0.26% higher against the USD from Friday's close.

Earlier today, in China, Australia's largest trading partner, the house price index climbed 8.3% on a yearly basis in August. The index had risen 9.7% in the previous month.

The pair is expected to find support at 0.7998, and a fall through could take it to the next support level of 0.7968. The pair is expected to find its first resistance at 0.8046, and a rise through could take it to the next resistance level of 0.8064.

Looking forward, minutes of the Reserve Bank of Australia's (RBA) latest meeting, scheduled to release in the early hours of tomorrow, will garner a lot of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

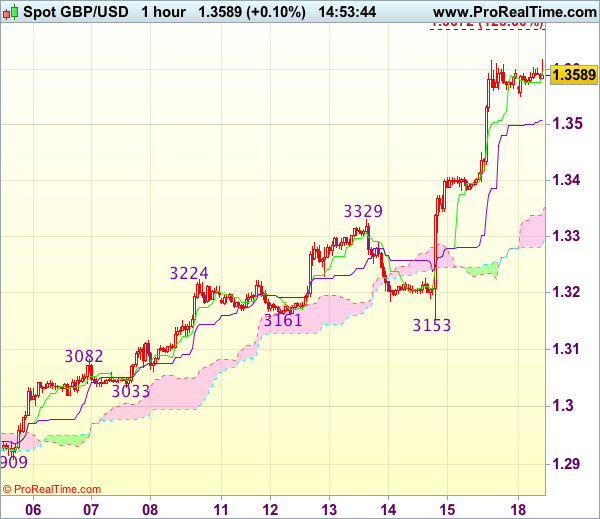

Trade Idea : GBP/USD – Buy at 1.3420

GBP/USD - 1.3577

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.3595

Kijun-Sen level : 1.3518

Ichimoku cloud top : 1.3359

Ichimoku cloud bottom : 1.3302

Original strategy :

Buy at 1.3490, Target: 1.3600, Stop: 1.3455

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3420, Target: 1.3600, Stop: 1.3385

Position : -

Target : -

Stop : -

Although cable edged higher in London morning to 1.3619, lack of follow through buying on break of Friday’s high at 1.3617 and current retreat suggest consolidation with initial mild downside bias would be seen and pullback to the Kijun-Sen (now at 1.3518) cannot be ruled out, however, reckon downside would be limited to 1.3420-30 and bring another rise later, above said resistance at 1.3619 would extend recent upmove to 1.3650 and possibly towards 1.3675 but upside should be limited to 1.3700-10, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as 1.3420-30. Only below 1.3380-85 would defer and signal a temporary top is formed, bring retracement of recent rise to 1.3350, then 1.3320-25 but lower Kumo (now at 1.3302) should remain intact.

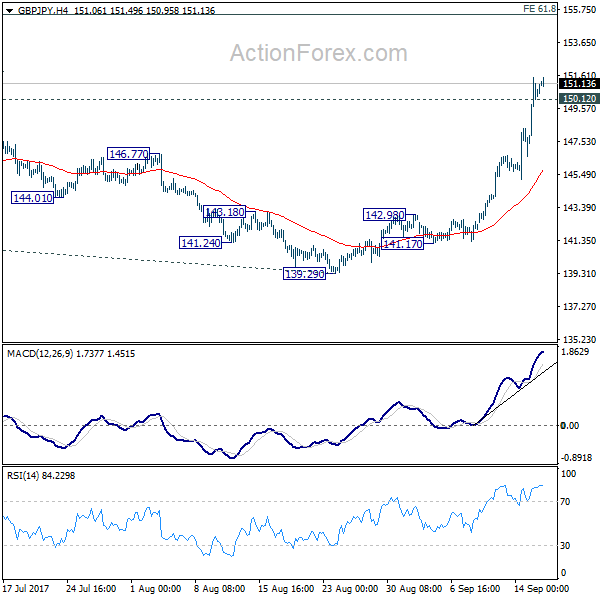

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.53; (P) 149.54; (R1) 152.53; More

Intraday bias in GBP/JPY remains on the upside for the moment. Current medium term rise from 122.36 should target 61.8% projection of 122.36 to 148.42 from 139.29 at 155.39 next. On the downside, below 150.12 minor support will turn intraday bias neutral and bring consolidation before staging another rally.

In the bigger picture, the consolidation from 148.42 should have completed and medium term rebound from 122.36 is resuming. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. For now, the bullish scenario is preferred as long as 139.29 support holds.

Euro-Zone’s Trade Surplus Shrunk In July

For the 24 hours to 23:00 GMT, the EUR rose 0.5% against the USD and closed at 1.1953 on Friday.

On the macro front, the Euro-zone's seasonally adjusted trade surplus narrowed more-than-expected to €18.6 billion in July, from a revised trade surplus of €21.7 billion in the previous month, while market participants were expecting the region to post a surplus of €20.3 billion.

The greenback lost ground against a basket of currencies, dragged down by a slew of downbeat economic reports from the US.

Data indicated that advance retail sales in the US unexpectedly fell 0.2% in August, dipping to a six-month low level, as sales were partially disrupted by impact of the Hurricane Harvey. Advance retail sales had climbed by a revised 0.3% in the previous month, whereas investors had envisaged for a gain of 0.1%.

Moreover, the nation's industrial production surprisingly declined 0.9% in August, dropping to a more than eight-year low level, as massive storm depressed the nation's oil drilling, petroleum refining and other industrial activity. Markets had anticipated industrial production to rise 0.1%, after recording a revised rise of 0.4% in the prior month. Additionally, the nation's manufacturing production recorded an unexpected drop of 0.3% in August, confounding market consensus for an increase of 0.3%. In the previous month, manufacturing production had recorded a revised flat reading.

In other economic news, the US flash Reuters/Michigan consumer sentiment index eased to a level of 95.3 in September, less than market expectations for a fall to a level of 95.0. In the prior month, the index had registered a reading of 96.8. Also, the nation's New York Empire State manufacturing index slightly fell to a level of 24.4 in September, compared to a reading of 25.2 in the prior month. On the contrary, the nation's business inventories rose 0.2% in July, in line with market expectations. In the previous month, business inventories had risen 0.5%.

In the Asian session, at GMT0300, the pair is trading at 1.1945, with the EUR trading 0.07% lower against the USD from Friday's close.

The pair is expected to find support at 1.1904, and a fall through could take it to the next support level of 1.1862. The pair is expected to find its first resistance at 1.1987, and a rise through could take it to the next resistance level of 1.2028.

Moving ahead, traders will focus on the Euro-zone's final consumer price inflation data for August, slated to release in a few hours. Moreover, the US NAHB housing market index for September, scheduled to release later in the day, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Trade Idea : EUR/USD – Buy at 1.1905

EUR/USD - 1.1940

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1945

Kijun-Sen level : 1.1951

Ichimoku cloud top : 1.1917

Ichimoku cloud bottom : 1.1900

New strategy :

Buy at 1.1905, Target: 1.2005, Stop: 1.1870

Position : -

Target : -

Stop : -

Although the single currency retreated after meeting resistance at 1.1988 on Friday, last week’s anticipated rebound from 1.1838 suggests low has possibly been formed there and downside should be limited to 1.1900-05, bring another rebound later to 1.1995-00 (previous resistance and 61.8% Fibonacci retracement of 1.2093-1.1838), however, break there is needed to signal the fall from 1.2093 has ended, bring subsequent rise to 1.2030-35 and then 1.2050-55.

In view of this, we are looking to buy euro again on dips as 1.1900-05 should limit downside and bring another rebound. Below 1.1865-70 would abort and suggest the rebound from 1.1838 (last week’s low) has ended, bring retest of this level first.

Interest Rate Could Rise In The Coming Months: BoE’s Vlieghe

For the 24 hours to 23:00 GMT, the GBP rose 1.45% against the USD and closed at 1.3597 on Friday, propelled by upbeat comments from one of the dovish Bank of England's (BoE) committee member.

The BoE policymaker, Gertjan Vlieghe, vowed for a near-term interest rate hike, if the economy continues to strengthen as expected.

In the Asian session, at GMT0300, the pair is trading at 1.3593, with the GBP trading slightly lower against the USD from Friday's close.

Overnight data revealed that the nation's Rightmove house price index eased 1.2% on a monthly basis in September, following a drop of 0.9% in the prior month.

The pair is expected to find support at 1.3447, and a fall through could take it to the next support level of 1.3302. The pair is expected to find its first resistance at 1.3677, and a rise through could take it to the next resistance level of 1.3762.

Trading trend in the Pound today is expected to be determined by a speech from the BoE Governor, Mark Carney, scheduled later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

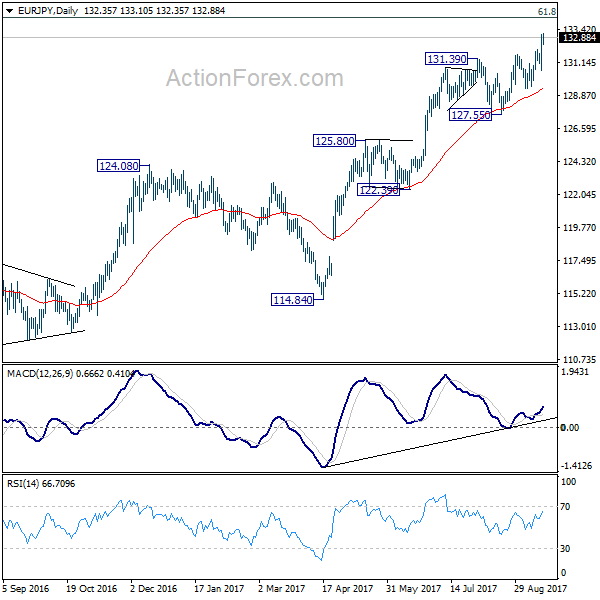

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.97; (P) 132.02; (R1) 133.46; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Current medium term rise should target 134.20 fibonacci level next. Firm break there will pave the way to 141.04 resistance next. On the downside, break of 130.60 support is needed to indicate short term topping. Otherwise outlook will remain bullish in case of retreat.

In the bigger picture, current rise from 109.03 is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). as long as 124.08 resistance turned support holds, further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. ON the downside, break of 127.55 support is needed to be the first signal of medium term reversal. Otherwise, outlook will remain bullish.