Sample Category Title

Trade Idea : USD/JPY – Stand aside

USD/JPY - 111.33

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 111.20

Kijun-Sen level : 110.92

Ichimoku cloud top : 110.30

Ichimoku cloud bottom : 110.16

New strategy :

Stand aside

Position : -

Target : -

Stop : -

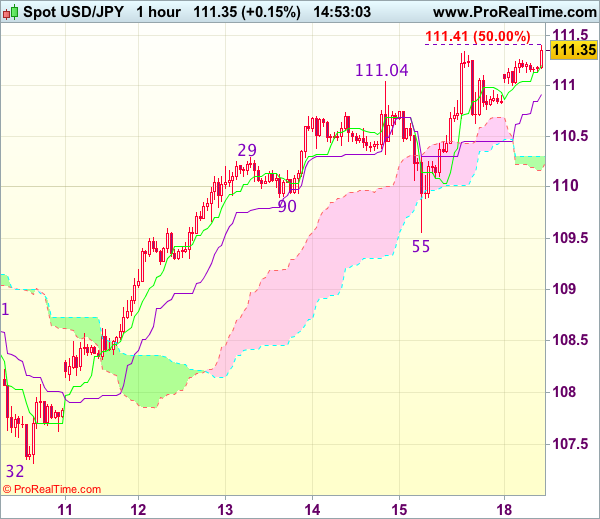

Although the greenback has edged higher again after last week’s rally and bullishness remains or recent reversal from 107.32 low to extend gain to 111.41-45 (50% projection of 107.32-111.04 measuring from 109.55), however, reckon upside would be limited to 111.85-90 (61.8% projection) and price should falter below 112.00-10, risk from there has increased for a correction later.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below the Kijun-Sen (now at 110.92) would bring correction to 110.60-65 and downside should be limited to 110.30-35, price should stay above 110.00, bring rebound later.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.38% against the JPY and closed at 110.85 on Friday.

In the Asian session, at GMT0300, the pair is trading at 111.21, with the USD trading 0.32% higher against the USD from Friday’s close.

The pair is expected to find support at 110.42, and a fall through could take it to the next support level of 109.64. The pair is expected to find its first resistance at 111.66, and a rise through could take it to the next resistance level of 112.12.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1436; (P) 1.1468; (R1) 1.1487; More... .

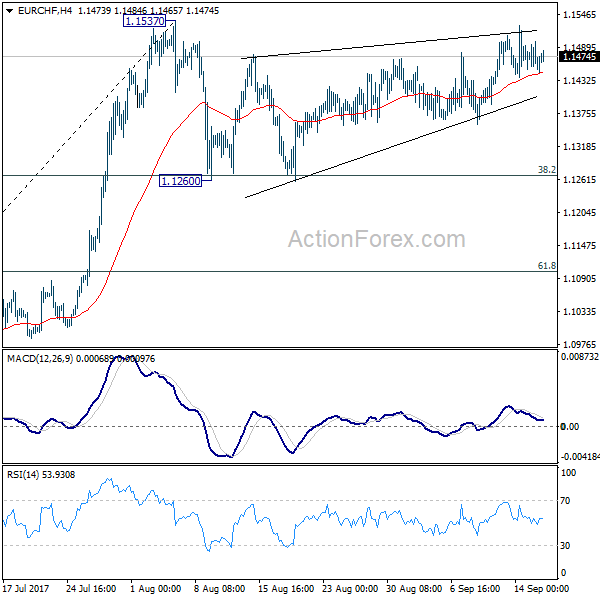

Intraday bias in EUR/CHF remains neutral as consolidation from 1.1537 is still in progress. Another fall could be seen. But in that case, downside should be contained by 38.2% retracement of 1.0830 to 1.1537 at 1.1267 to bring rebound. On the upside, break of 1.1537 resistance will confirm resumption of larger rally from 1.0629. In that case, EUR/CHF should target 1.2 key resistance level next.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Swiss Franc Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.74% against the CHF and closed at 0.9595 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9605, with the USD trading 0.1% higher against the CHF from Friday's close.

The pair is expected to find support at 0.9564, and a fall through could take it to the next support level of 0.9524. The pair is expected to find its first resistance at 0.9646, and a rise through could take it to the next resistance level of 0.9688.

With no major macroeconomic releases in the Switzerland today, investors will look forward to global macroeconomic events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Canada’s Existing Home Sales Rose For The First Time In 4 Months In August

For the 24 hours to 23:00 GMT, the USD traded flat against the CAD and closed at 1.2179 on Friday.

Macroeconomic data showed that Canada's existing home sales rebounded 1.3% on a monthly basis in August, advancing for the first time since March 2017. In the previous month, existing home sales had dropped 2.1%.

In the Asian session, at GMT0300, the pair is trading at 1.2181, with the USD trading a tad higher against the CAD from Friday's close.

The pair is expected to find support at 1.2129, and a fall through could take it to the next support level of 1.2078. The pair is expected to find its first resistance at 1.2225, and a rise through could take it to the next resistance level of 1.2270.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1862; (P) 1.1892 (R1) 1.1947; More...

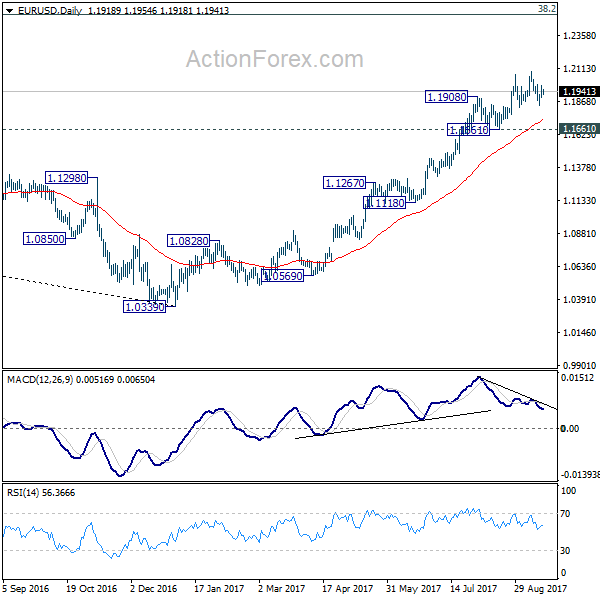

Intraday bias in EUR/USD remains neutral for the moment. With 1.1822 support intact, near term outlook stays bullish for another rise. Above 1.1994 minor resistance will turn bias to the upside for 1.2091 first. Break there will extend larger rise from 1.0339 and target next key fibonacci level at 1.2516. But considering bearish divergence condition in 4 hour MACD, break of 1.1822 will confirm short term topping and bring deeper fall back to 1.1661 support and below.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall fro 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

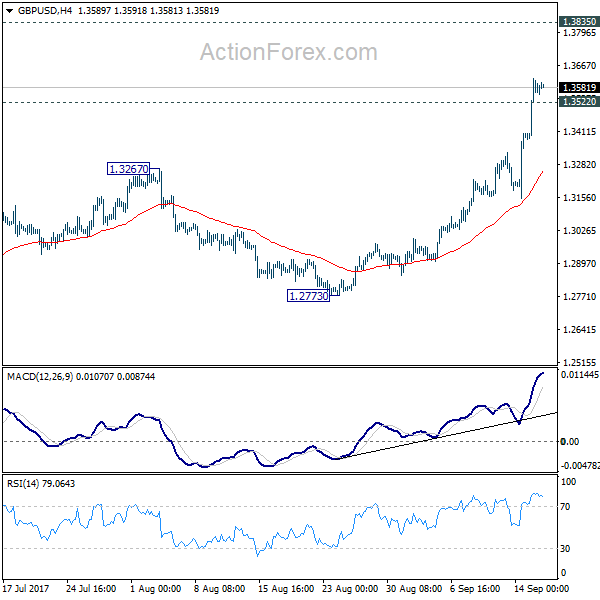

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3435; (P) 1.3526; (R1) 1.3674; More...

Intraday bias in GBP/USD remains on the upside for the moment. current medium term rally should extend to 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405). On the downside, below 1.3522 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, the strong break of 1.3444 key resistance now argues that the long term trend in GBP/USD has reversed. That is a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

European Open Briefing: Asia-Pacific Equity Markets Were Higher On Monday

Global Markets:

- Asian stock markets: Nikkei up 0.52 %, Shanghai Composite rose 0.25 %, Hang Seng gained 0.99 %, ASX 200 rose 0.5 %

- Commodities: Gold at $1321.49 (-0.28 %), Silver at $17.63 (-0.35 %), WTI Oil at $50.46 (+0.04 %), Brent Oil at $55.70 (+0.14 %)

- Rates: US 10-year yield at 2.20, UK 10-year yield at 1.30, German 10-year yield at 0.43

News & Data:

- (AUD) New Motor Vehicle Sales m/m 0.0 % vs -2.4 % previous

- (USD) Core Retail Sales m/m 0.2 % vs 0.5 % expected

- (USD) Retail Sales m/m -0.2 % vs 0.1 % expected

- (USD) Empire State Manufacturing Index 24.4 vs 18.2 expected

- (USD) Capacity Utilization Rate 76.1 % vs 76.8 % expected

- (USD) Industrial Production m/m -0.9 % vs 0.1 % expected

- (USD) Prelim UoM Consumer Sentiment 95.3 vs 95.1 expected

- Oil markets firm on rising refinery demand, falling U.S. rig count- RTRS

- Dollar edges up vs yen, hovers near seven-week high ahead of Fed- RTRS

CFTC Positioning Data:

- EUR long 86K vs 96K long last week.

- GBP short 46K vs 54K short last week.

- JPY short 57K vs 73K short last week.

- CHF short 2K vs 2K short last week.

- CAD long 50K vs 54K long.

- AUD long 63k vs 65k last week.

- NZD long 12K vs 15K long last week.

Markets Update:

Asia-Pacific equity markets were higher on Monday following a record-breaking Wall street session and Australia’s benchmark index rebounding from three straight sessions of declines as investors piled into risk assets amid optimism that the U.S. favors a peaceful resolution to North Korea’s nuclear threats and no new provocation by North Korea over the weekend.

USDJPY opened up around 40 pips early on Monday and has since stabilized around 111.20 currently. Overall, the Japanese Yen continues to lose value as it lost 0.3 percent against the US Dollar, extending Friday’s 0.5 percent drop. Bank of Japan is widely expected to maintain its massive asset buying campaign at a meeting on Thursday.

EURUSD is little changed from its late levels on Friday and is currently seen trading around 1.1934. The Euro had hit a 2-1/2-year high reaching $1.2092 earlier this month. The dollar index, which tracks the dollar against a basket of currencies was flat and is currently valued at 91.87 after losing 0.3 percent on Friday.

AUDUSD is currently seen Trading at 0.8024 as the Australian Dollar put up a strong show outperforming on the session rising 0.3 percent against the US Dollar. Australia’s main index added 0.5 percent rebounding from three straight sessions of declines. Similarly, the New Zealand dollar is seen trading at 0.7320 after the Kiwi added 0.3 percent against the USD.

Upcoming Events:

- All Day – JPY Bank Holiday

- 08:00 GMT – (EUR) Italian Trade Balance

- 09:00 GMT – (EUR) Final CPI y/y

- 09:00 GMT – (EUR) Final Core CPI y/y

- 10:00 GMT – (EUR) German Buba Monthly Report

- 12:30 GMT – (CAD) Foreign Securities Purchases

- 14:30 GMT – (GBP) ECB's Lautenschlaeger Speaks

- 20:00 GMT – (USD) TIC Long-Term Purchases

The Week Ahead:

Tuesday, September 19th

- 01:30 GMT – (AUD) Monetary Policy Meeting Minutes

- 01:30 GMT – (AUD) HPI q/q

- 09:00 GMT – (EUR) German ZEW Economic Sentiment

- 12:30 GMT – (CAD) Manufacturing Sales m/m

- 12:30 GMT – (USD) Building Permits

- 12:30 GMT – (USD) Current Account

- 12:30 GMT – (USD) Housing Starts

- 12:30 GMT – (USD) Import Prices m/m

- 22:45 GMT – (NZD) Current Account

Wednesday, September 20th

- 08:30 GMT – (GBP) Retail Sales m/m

- 14:00 GMT – (USD) Existing Home Sales

- 14:30 GMT – (USD) Crude Oil Inventories

- 18:00 GMT – (USD) FOMC Economic Projections

- 18:00 GMT – (USD) FOMC Statement

- 18:00 GMT – (USD) Federal Funds Rate

- 18:30 GMT – (USD) FOMC Press Conference

- 22:45 GMT – (NZD) GDP q/q

Thursday, September 21st

- Tentative – (JPY) Monetary Policy statement

- Tentative – (JPY) BOJ Policy Rate

- Tentative – (JPY) BOJ Press Conference

- 08:30 GMT – (GBP) Public Sector Net Borrowing

- 12:30 GMT – (CAD) Wholesale Sales m/m

- 12:30 GMT – (USD) Unemployment Claims

- 12:30 GMT – (USD) Philly Fed Manufacturing Index

Friday, September 22nd

- All Day – (NZD) Parliamentary Elections

- 07:00 GMT – (EUR) French Flash Manufacturing PMI

- 07:00 GMT – (EUR) French Flash Services PMI

- 07:30 GMT – (EUR) German Flash Manufacturing PMI

- 07:30 GMT – (EUR) German Flash Services PMI

- 08:00 GMT – (EUR) Flash Manufacturing PMI

- 08:00 GMT – (EUR) Flash Services PMI

- 12:30 GMT – (CAD) CPI m/m

- 12:30 GMT – (CAD) Core Retail Sales m/m

- 12:30 GMT – (CAD) Common CPI y/y

- 12:30 GMT – (CAD) Median CPI y/y

- 12:30 GMT – (CAD) Retail Sales m/m

- 12:30 GMT – (CAD) Trimmed CPI y/y

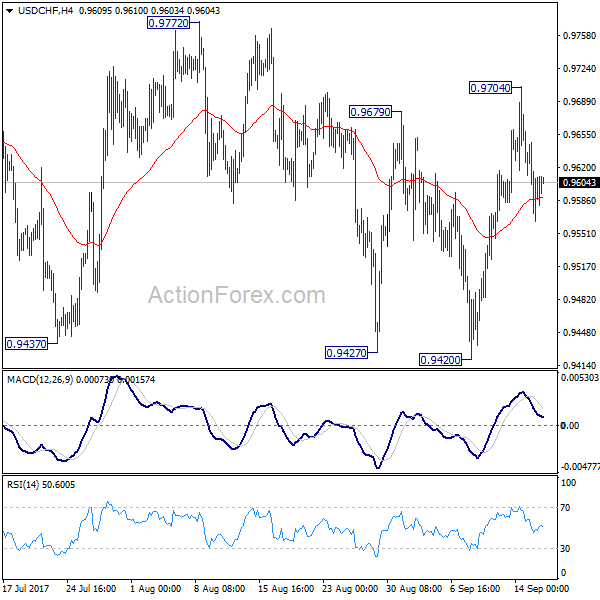

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9556; (P) 0.9602; (R1) 0.9638; More....

Intraday bias in USD/CHF remains mildly on the downside for 0.9420 support. With 0.9772 resistance intact, outlook remains bearish. Break of 0.9420 will resume medium term fall from 1.0342 and target next long term fibonacci level at 0.9090. However, firm break of 0.9772 will indicate trend reversal and turn outlook bullish.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

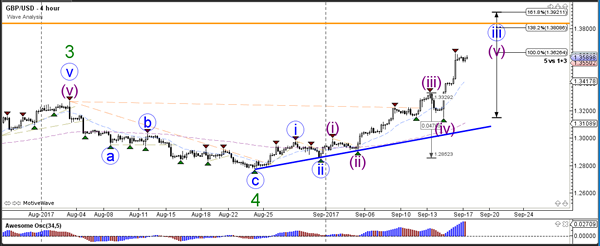

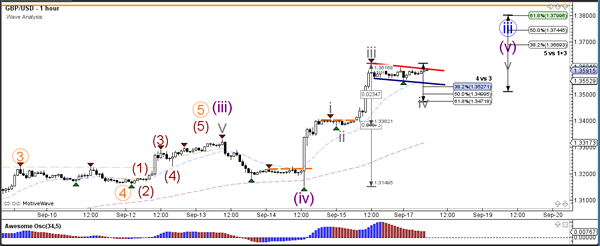

Daily Technical Analysis: GBP/USD Bull Flag Continuation Chart Pattern Targets 1.3750

Currency pair GBP/USD

The GBP/USD bullish momentum is strong and probably part of a wave 3 (blue). The resistance line (orange) is a potential resistance from the daily chart.

The GBP/USD is building a bull flag chart pattern (red/blue), which is a continuation pattern within the uptrend. The Fibonacci levels of wave 4 vs 3 (grey) are most likely support whereas a break above the bull flag could see price challenge the Fibonacci targets of wave 5 (grey/purple).

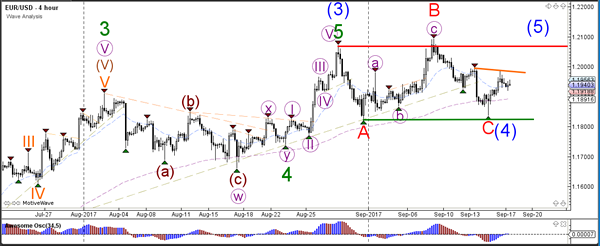

Currency pair EUR/USD

The EUR/USD seems to have completed an ABC correction (red) within the wave 4 (blue). A bullish breakout could indicate the continuation of the uptrend via wave 5 (blue).

The wave 4 (blue) might become extended via a WXY formation (red) if price develops a 3 wave pattern (purple).

Currency pair GBP/USD

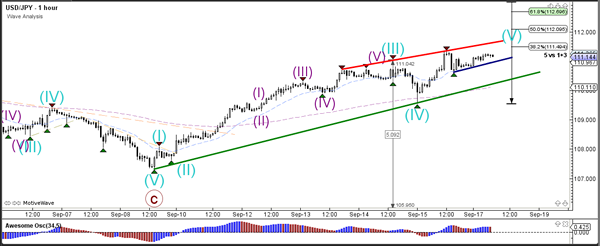

The USD/JPY is challenging the strong horizontal resistance level (red), which could indicate the end of a wave 1 (light green) or alternatively wave A (green).

The USD/JPY break below the support trend lines (green/blue) could indicate a bearish ABC correction. Otherwise price could still continue slightly higher within the wave 5 (blue).