Sample Category Title

USDJPY Falls to 107.40

The U.S dollar continues to slide sharply lower against the Japanese Yen, with the USDJPY pair so far finding intraday support from the 107.40 level, trading at its lowest level since November 15th, 2016.

Broad-based weakness in the U.S index is accelerating, after yesterday's weaker than expected U.S initial jobs claims, which increase by 62,000, marking the highest level for initial claims since April 18, 2015.

Weakness in the U.S economy is starting to accelerating the decline seen in the USDJPY pair. Traders should pay close attention to the damage caused by hurricane IRMA over the weekend, further limiting the U.S economies domestic data.

Key intraday technical support is found at 107.30 and the November 14th, 2016 price low, at 106.86. Below 106.86 level, the 106.60 level represents the key 38.2 Fibonacci retracement level.

Any intraday upside price movements for the USDJPY pair, should find resistance at 107.70, 108.13 and the former weekly price low, at 108.26.

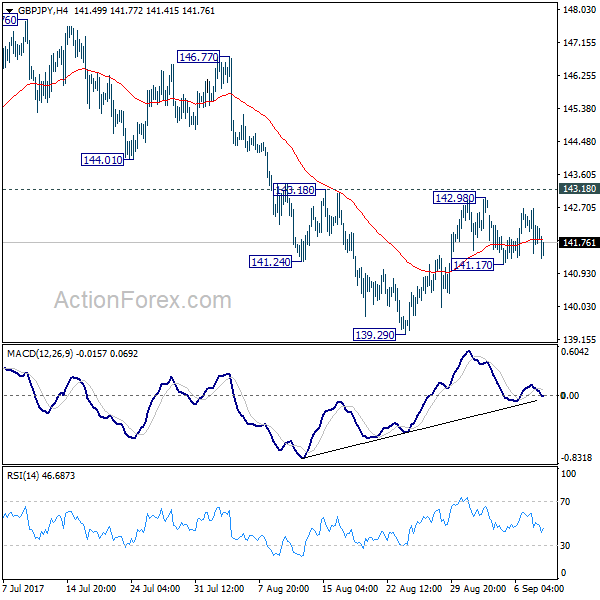

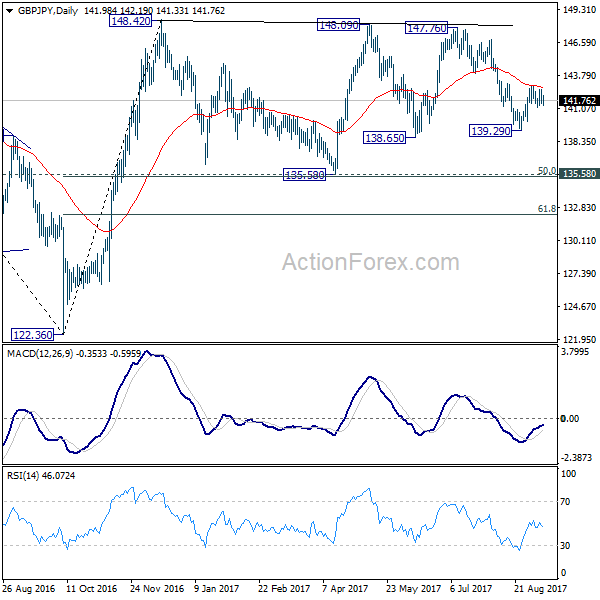

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.48; (P) 142.08; (R1) 142.68; More

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, below 141.17 will target 139.29 support first. Break will extend the fall from 147.76 and target 135.58 key support level. At this point, price actions from 148.42 are seen as a sideway consolidation pattern. Hence, we'll expect strong support from 135.58 to contain downside and bring rebound. Meanwhile, break of 143.18 will indicate short term reversal and turn bias back to the upside.

In the bigger picture, the sideway pattern from 148.42 is still unfolding. In case of deeper fall, we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

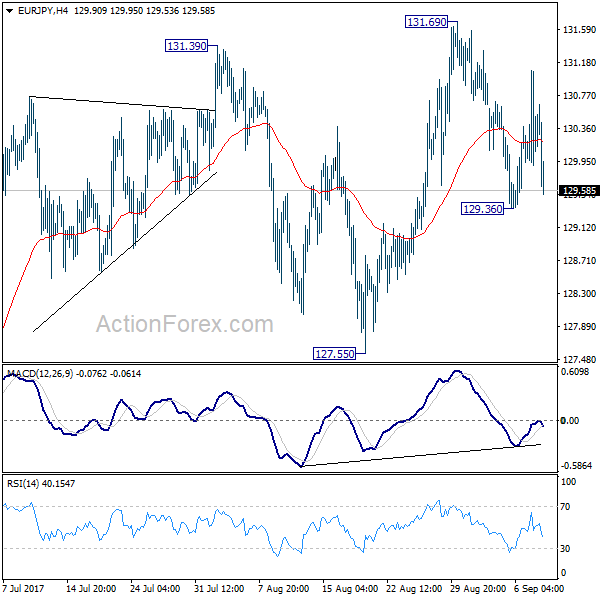

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.82; (P) 130.45; (R1) 131.00; More...

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, break of 131.69 high is needed to confirm rally resumption. Otherwise, we'd expect more corrective price action in near term, with risk of deeper fall. Below 129.36 will target 127.55 support first. Firm break there will indicate near term reversal and deeper fall would be seen back to 122.39/125.80 support zone.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds. However, firm break of 124.08 will argue that rise from 109.03 is completed and turn outlook bearish.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bullish momentum yesterday topped at 1.2059 and hit 1.2089 earlier today in Asian session. This fact ends the bearish correction phase. The bias is bullish in nearest term testing 1.2150/75 region. Immediate support is seen around 1.2017 (current low). A clear break below that area could lead price to neutral zone in nearest term testing 1.1980 region but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break and daily/weekly close above 1.2150/75 would expose 1.2350 region next week.

GBPUSD

The GBPUSD had a bullish momentum yesterday topped at 1.3115 and hit 1.3138 earlier today in Asian session. This fact nullifies the bearish pin bar scenario and changes the technical bias to the upside. The bias is bullish in nearest term testing 1.3165. A clear break above that area could trigger further bullish pressure testing 1.3200 – 1.3265 resistance area. Immediate support is seen around 1.3082. A clear break below that area could lead price to neutral zone in nearest term as direction would become unclear.

USDJPY

The USDJPY had a significant bearish momentum yesterday, closed below 108.70 key support as you can see on my daily chart below. This fact activates my bearish mode. The bias is bearish in nearest term testing 107.50/00 support area. Immediate resistance is seen around 108.70. A clear break back above that area could lead price to neutral zone in nearest term as direction would become unclear testing 109.25 resistance area.

USDCHF

The USDCHF had a bearish momentum yesterday bottomed at 0.9493 and slipped below 0.9450 key support earlier today in Asian session. The bias is bearish in nearest term but 0.9450 region is a good place to buy with a tight stop loss. Immediate resistance is seen around 0.9525. A clear break above that area could lead price to neutral zone in nearest term testing 0.9580 – 0.9600 region. On the downside, a clear break and consistent movement below 0.9450 would expose 0.9250/00 region next week.

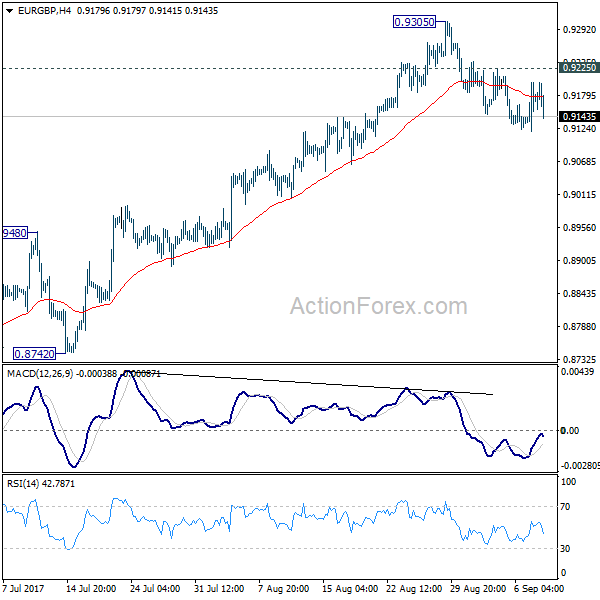

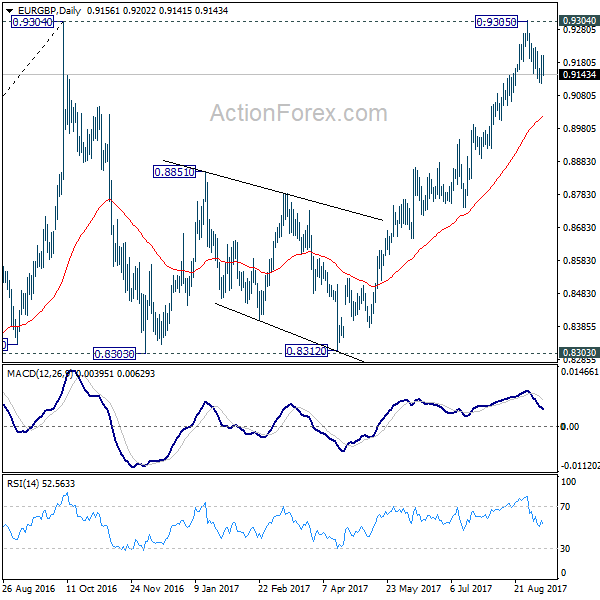

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9118; (P) 0.9141; (R1) 0.9159; More

No change in EUR/GBP's outlook. With 0.9225 minor resistance intact, deeper fall is expected to target 55 day EMA (now at 0.9019). Sustained trading below there will likely start the third leg of the consolidation from 0.9304 and target 0.8303 key support again. On the upside, above 0.9236 minor resistance will turn bias back to the upside for 0.9225 minor resistance instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes. Firm break of 0.9799 high will target 61.8% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

Dollar’s Capitulation Trade

The 'mighty' dollar has deepened its dive against the majors as investor caution on the currency grows.

Currently, there is no get out of 'jail free card' for long dollar investors who weathered another night of fresh selling, a day after the dollar index notched a 2½-year low – year-to-date, the index is down -9.2%.

Yesterdays' broad move by investors favoured owning safe-haven assets – gold and sovereign debt – fuelled partially by the ECB's raised growth forecasts that helped support a stronger EUR to print a fresh 32-month high outright (€1.2057).

In the eurozone, a robust economic recovery amidst low inflation has helped the EUR to surge more than +14% outright this year. During Thursday's press conference, ECB President Draghi expressed concern about the currency's strength without offering any proposal on how to address it as policy makers' edge toward unwinding QE in the autumn.

Note: The 'smart' money was short EUR's or small core 'long' heading into yesterday's ECB press conference – many had expected Draghi to address the pace of EUR appreciation, when that did not materialize, the market then scrambled to own the EUR to offset some shorts and for a positional buy looking for a further move up in EUR/USD on a 6-12 month horizon (€1.25-27).

The lack of progress and market faith in 'Trumponomics' – program of infrastructure spending, tax overhaul and regulatory cutbacks would cause long-muted U.S growth to accelerate – has the dollar struggling on growth and rate differentials.

Further market doubts that the Fed has the ammo, or the will, to hike interest rates again this year, given soft inflation, has intensified this week, in particular, after Hurricane Harvey mass destruction in Texas and the prospect of an even-stronger storm from Irma battering Florida this weekend.

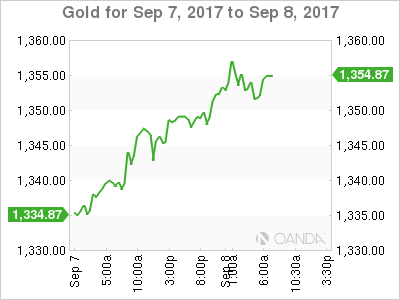

Haven moves are also at play, with rallies in precious metal and government debt.

Gold is at its highest in 12-months, printing +$1,350 an ounce, while there has been broad buying of global debt in recent days, further flattening sovereign yield curves.

The market is also concerned that North Korea will launch another missile in the next 24-hours, when the country celebrates its founding. The fear has caused a further uptick in the demand for sovereign debt – U.K 10-year Gilt yields fell back under the psychological +1% (+0.97%) overnight, while 10-year JGB's fell below zero and U.S 10-year product trades atop of the psychological +2%.

In China, authorities have strengthened the Yuan guidance for the tenth consecutive day.

The People's Bank of China (PBoC) set the 'fix' at ¥6.5032 vs. ¥6.5269. Still, the PBOC's guidance fell short of market expectations given yesterday's strength in the currency.

With the absence of intervention by China has given the market the 'thumbs up' to aggressively dump dollars – intraday, the yuan traded as high as ¥6.4617, its highest level in 18-months.

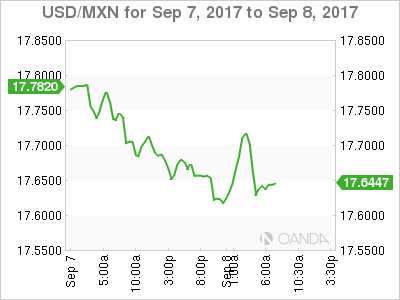

In Mexico, the most powerful earthquake (magnitude 8) this century has shook the country, adding to investor anxiety and sending the MXN ($17.64) lower.

In Canada, this morning's employment report (08:30 am EDT +17k e) will set the tone for the loonie (C$1.2117) heading into the weekend.

Three things that Bank of Canada's (BoC) Poloz has done with Wednesday's surprise hike – a gradual approach to rate rises is now a 'myth,' the hike came at a decision-only meeting (without press conference), and most importantly throws into the doubt the markets view that Poloz preferred a weaker CAD.

The BoC is now in rate 'hike' cycle, but data dependent – fixed income dealers are beginning to price in +1.75% by the end of 2018.

Intraday, CAD is very much overbought, but there is 'no' reason to want to sell it at the moment. C$1.2030 is very strong dollar support – the USD needs to break above C$1.2350 – C$1.25 with conviction to get any dollar traction. With another Fed rate hike being priced out this will be difficult to sustain.

In the medium term, any USD rallies will see CAD buying to target C$1.1950-1.20. However, the 'elephant' in the room remains NAFTA negotiations.

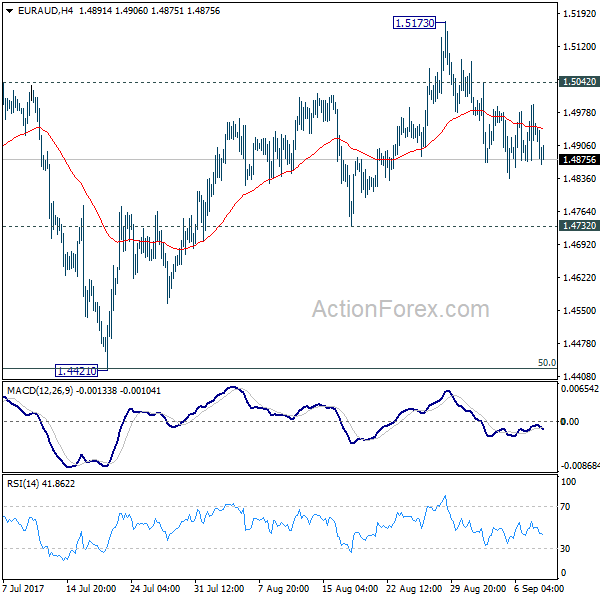

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4873; (P) 1.4934; (R1) 1.4998; More....

With 1.5042 minor resistance intact, deeper fall is expected in EUR/AUD to 1.4732 support. Break of 1.4732 support will confirm that fall from 1.5173 is the third leg of consolidation pattern from 1.5226. In that case, further fall should be seen to 1.4421 again. But we'd expect strong support from there to contain downside and bring rebound. On the upside, above 1.5042 minor resistance will turn bias back to the upside for 1.5173 resistance instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Euro Punches Past 1.20 On Draghi Tapering Comments

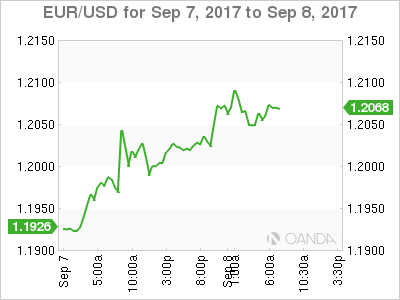

The euro rally continues, as EUR/USD has posted slight gains in the Friday session. Currently, the pair is trading at 1.2064, up 0.34% on the day. The euro has gained 1.4% this week, and is trading at its highest level since January 2015. On the release front, Germany’s trade surplus narrowed to EUR 19.5 billion, short of the forecast of EUR 20.3 billion. There are no major events in the US, but we’ll hear from FOMC member Patrick Harker.

The euro pushed above the symbolic 1.20 level on Thursday, after investors liked what they heard from ECB President Mario Draghi. As expected, the ECB maintained interest rates at 0.00%, and what investors wanted to hear was some guidance regarding the bank’s asset purchase program (QE), which is scheduled to end in December. The ECB announcement was surprisingly dovish, as policymakers said that QE would not be tapered before December, and left the door open to further stimulus in 2018, if necessary. However, Mario Draghi presented a more hawkish stance in his follow-up press conference, saying that the ECB would decide on tapering stimulus in October. Draghi made direct reference to the exchange rate, noting that “the recent volatility in the exchange rate represents a source of uncertainty which requires monitoring”. Draghi & Co. are clearly concerned by the euro’s appreciation, as the EUR/USD has soared 14 percent in 2017. The stronger euro has made imports less expensive, thus reducing inflation and hampering the ECB’s efforts to raise inflation levels. The ECB has now cut its inflation forecast to 1.2 percent in 2018 and 1.5 percent in 2019, well short of its target of just below 2 percent.

The markets have grown used to solid German numbers, so this week’s numbers have been a disappointment. Earlier this week, Factory Orders declined 0.7%, well off the forecast of a 0.2% gain. This marked a 3-month low. German Industrial Production followed suit, as the reading of 0.0% missed the estimate of 0.5%. On Friday, Germany’s trade surplus dropped to EUR 19.5 billion, the smallest surplus since January. Why the downturn? Global demand, which had been very strong in the first half of 2017, is showing signs of softening, and this had a negative impact on the manufacturing sectors in Germany and throughout the eurozone. This has also had a negative impact on exports, which was reflected in the Germany’s smaller surplus in July.

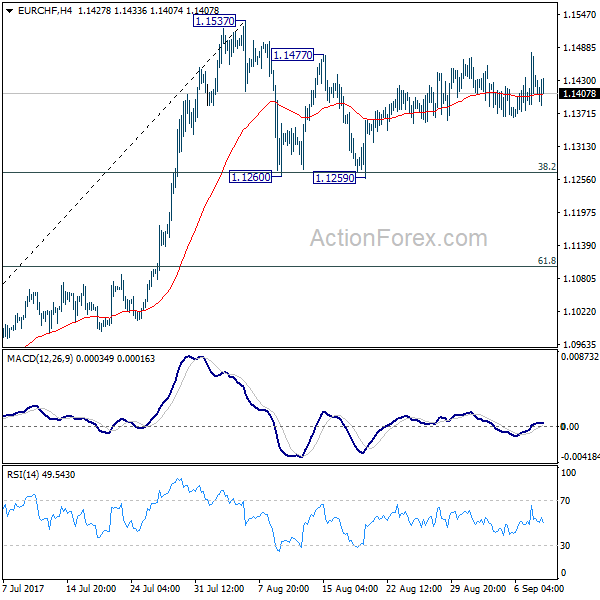

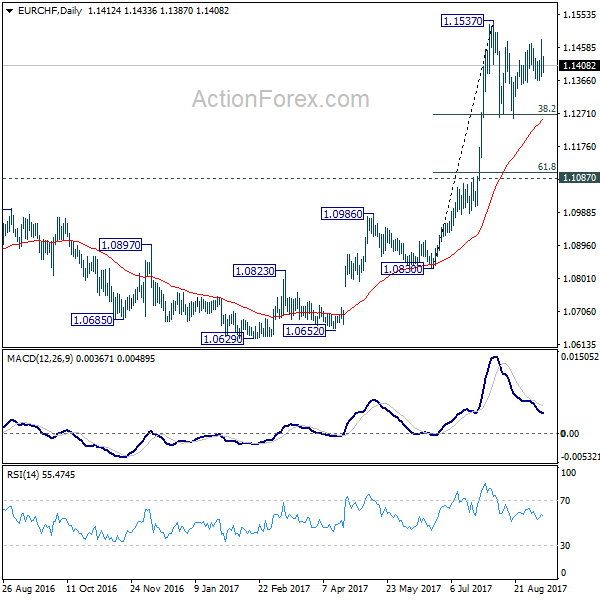

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1374; (P) 1.1428; (R1) 1.1478; More...

EUR/CHF is still bounded in consolidation from 1.1537 and intraday bias stays neutral. More sideway trading could be seen. On the upside, break of 1.1537 resistance will confirm resumption of larger rally from 1.0629. In that case, EUR/CHF should target 1.2 key resistance level next. On the downside, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Market Update – European Session: USD Can’t Find Love, ECB Said To Have Discuss 4 Options For QE Extension

Notes/Observations

USD at 2 1/2 lows over concerns of economic fallout from Hurricane Irma as doubts that the Fed has the firepower or the will to raise interest rates again this year

China CNY currency (yuan) at strongest level since Dec 2015 (both onshore and offshore markets) on speculation the PBoC will tolerate a stronger currency

France and UK July Industrial Production in-line with expectations

Overnight

Asia:

Japan Q2 Final GDP revised lower (Q/Q: 0.6% v 0.7%e; GDP Annualized: 2.5% v 2.9%e). Downward revision in annualized GDP growth was biggest under current calculation method adopted in 2010.

Japan govt official: Domestic economy continues to recover moderately as a trend, driven by domestic demand

China Aug Trade Balance registers a smaller surplus ($42.0B v $48.5Be); Components mixed (Exports Y/Y: 5.5% v 6.0%; Imports Y/Y: 13.3% v 10.0%)

PBOC set Yuan reference rate 6.5032 per USD (10th consecutive day of stronger setting with yuan fix at its strongest level since May 2016 (16-month high)

Europe:

Spain Constitutional Court suspended the Catalan referendum law, as requested by PM Rajoy

Greek PM Tsipras reiterates ready and determined to exit bailout in August of 2018

Americas:

Magnitude 8.0 Earth quake reported 87KM SSW of Tres Picos Mexico (near Gualamlia border) - Fed's Dudley (voter): Reiterates balance sheet rolloff likely to start relatively soon; Don't expect Harvey to alter trajectory of US economy. Reiterates appropriate to continue removing policy accommodation

FBI Director Wray: Have not detected any whiff of interference into Russian meddling in 2016 election

President Trump: US military action in North Korea remains option, but it's not inevitable. Lots of good reasons to get rid of the debt ceiling. Would have done a longer deal on debt ceiling but wanted to be able to spend more on military spending

President Trump and Senate Democratic Leader Schumer said to have agreed to seek a permanent repeal of the debt ceiling under a 'gentleman's agreement'

US Senate has sufficient votes to move Hurricane Harvey aid/three-month debt ceiling raise bill forward (as expected). Senate approved $15.25B in disaster aid, measures to fund Govt, raise debt limit through to Dec 8thBill now moves to the House, where it is also expected to pass

Economic data

(NL) Netherlands July Manufacturing Production M/M: -0.7 v -0.3% prior; Y/Y: 3.0% v 3.3% prior, Industrial Sales Y/Y: 5.7% v 4.7% prior

(JP) Japan Aug Eco Watchers Current Outlook: 49.7 v 49.5e; Outlook Survey: 51.1 v 50.1e

(CH) Swiss Aug Unemployment Rate: 3.0% v 3.0%e, Unemployment Rate (Seasonally Adj): 3.2% v 3.2%e

(DE) Germany July Current Account: €19.4B v €20.8Be; Trade Balance: €19.5B v €21.0Be; Exports M/M: 0.2% v 1.3%e; Imports M/M: 2.2% v 2.8%e

(DE) Germany Q2 Labor Costs Q/Q: 0.3% v 0.1% prior; Y/Y: 2.3% v 2.2% prior

(FR) France July Industrial Production M/M: 0.5% v 0.5%e; Y/Y: 3.7% v 3.6%e

(FR) France July Manufacturing Production M/M: 0.3% v 0.6%e; Y/Y: 3.9% v 4.2%e

(HU) Hungary Aug CPI M/M: 0.1% v 0.0%e; Y/Y: 2.6% v 2.5%e

(CZ) Czech Aug Unemployment Rate: 4.0% v 4.0%e

(TW) Taiwan Aug Trade Balance: $5.7B v $5.5Be; Exports Y/Y: 12.7% v 12.4%e; Imports Y/Y: 6.9% v 5.7%e

(UK) BoE/TNS Aug Inflation Expectations Survey Next 12-month: 2.8% v 2.8% prior

(UK) July Visible Trade Balance: -£11.6B v -£12.0Be, Overall Trade Balance: -£2.9B v -£3.3Be, Trade Balance Non EU: -£3.8B v -£3.9B prior

(UK) July Industrial Production M/M: 0.2% v 0.2%e; Y/Y: 0.4% v 0.4%e

(UK) July Manufacturing Production M/M: 0.5% v 0.3%e; Y/Y: 1.9% v 1.7%e

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2024, 2027, 2034 and 2051 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 373.7, FTSE -0.3% at 7374, DAX -0.1% at 12280, CAC-40 -0.3% at 5097, IBEX-35 -0.2% at 10108, FTSE MIB -0.4% at 21636, SMI -0.1% at 8897, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes: European Indices drift lower this morning in quiet trade as markets digest developments from the ECB yesterday. Concerns over the effect of Hurricane Irma and an Earthquake in Mexico also weigh. On the corporate front Akzo Nobel trades lower after trimming its 2017 out, as well as announcing new management structure. Safestyle trades sharply lower after a profit warning, while Greene king trade sharply low bad weather slowed sales. Air France trades higher after strong August metrics whilst, Finnair trades higher after lifting its outlook.

Equities

Consumer discretionary [SafeStyle [SFE.UK] -29% (Profit warnings), Greene King [GNK.UK] -13.4% (LFL Sales), Air France [AF.FR] +1.7% (Aug metrics)]

Materials: [Akzo Nobel [AKZA.NL] -2.1% (New management structure, trims outlook)]

Healthcare: [Cellnovo [CLNV.FR] - 5% (FDA requests further info), Erytech [ERYP] +3.7% (Positive Study)]

Energy: [Bourbon [GBB.FR] -1.6% (New management)]

Speakers

ECB's Liikanen (Finland): Reiterates General Council view that monetary policy must remain accommodative. Exchange rate can impact inflation

ECB said to have discussed 4 QE scenarios which included 6-month and 9-month extension options. To study bond buying reduction to €40B/month or €20B/month (from current level of €60B)

British Chambers of Commerce (BCC): Medium outlook for UK economy downgraded citing weaker than expected contribution from trade and subdued consumer spending. Weaker GBP currency (pound) failing to boost UK growth

China policymakers said to be worry about a rallying CNY currency (Yuan) as exporters come under strain. Pace of appreciation could not be too fast but China unlikely to intervene forcefully due to worries of criticism by US (**Note: USD/CNY has fallen by almost 8% in 2017)

Currencies

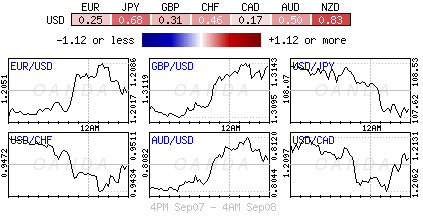

USD maintains its soft tone against the major and commodity-related pairs. Dealers were looking for fresh factors to the greenback's woes. USD was at 2 1/2 year lows against a basket of currencies. One analyst noted that the recent Hurricane Harvey and imminent threat of Irma would likely push back any additional Fed hikes. Dealers also cited comments from Fed's Dudley who did not repeat his expectation for rate hike this year.

EUR/USD holding in the mid-1.20 area after ECB Draghi failed to jawbone the euro lower at Thursday's policy meeting. The pair hit a 32-month high during the Asian session just under the 1.21 level

USD/CNY price action moving up to the front burner. PBoC Yuan fixing was the 10th straight for a stronger Yuan currency. Various reports noted that China official were becoming concerned with any further one-way appreciation of the yuan versus the US dollar as its would put additional pressure on China's exports

Fixed Income

Bund futures trade at 163.26 up 8 ticks in risk aversion flows as futures hit target session highs of 163.43 to continue the upside momentum towards 163.83, to the downside 162.92 remains initial support followed by 162.53.

Gilt futures trade down 11 ticks at 128.01 having earlier hit 128.2. Yields have seen a slight lift after strong Manufacturing Data, and in line Industrial production data. Continued downside targets 127.48.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.775T from €1.773T and use of the marginal lending facility fell to €1.01BM from €1.04B.

Corporate issuance saw a further $10.4B via 5 issuers come to market headlined by Discovery Communications $6.3B 6 part offering which brings the weeks issuance to over $45.5B above analysts forecasts of over $30B. For the week ending Sep 6th IG Funds reported outflows of $43M, marking the first outflows seen since Mid Dec 2016.

Looking Ahead

(UR) Ukraine Aug CPI M/M: -0.2%e v +0.2% prior; Y/Y: 16.0%e v 15.9% prior

(ES) Spain July YTD Budget Balance: No est v -€13.3B prior

(MX) Mexico Aug Nominal Wages Y/Y: No est v 5.8% prior

05:30 (ZA) South Africa to sell combined ZAR800M in I/L 2029, 2033 and 2046 bonds

05:30 (PL) Poland to sell Bonds

06:00 (PT) Portugal July Trade Balance: No est v -€1.0B prior

06:00 (IE) Ireland July Property Prices M/M: No est v 1.4% prior; Y/Y: No est v 11.6% prior

06:00 (UK) DMO to sell combined £6.0B in 1-month, 3-month and 6-month bills (£2.0B, £2.0B and £2.0B respectively)

06:30 (IS) Iceland to sell Bonds - 06:45 (US) Daily Libor Fixing

07:00 (CL) Chile Aug CPI M/M: 0.3%e v 0.2% prior; Y/Y: 1.9%e v 1.7% prior

07:30 (IN) India Weekly Forex Reserves

08:00 (UK) Aug NIESR GDP Estimate: No est v 0.2% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Aug Net Change in Employment: +15.0Ke v +10.9K prior; Unemployment Rate: 6.3%e v 6.3% prior

08:30 (CA) Canada Q2 Capacity Utilization: No est v 83.3% prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (HU) Hungary Central Bank Vice Gov Nagy

08:45 (US) Fed's Harker speaks on Consumer Finance in Philadelphia

10:00 (US) July Final Wholesale Inventories M/M: 0.5%e v 0.4% prelim; Wholesale Trade Sales M/M: 0.5%e v 0.7% prior

11:00 (EU) Potential sovereign ratings after EU close

(PL) Poland Sovereign Debt to be rated by Moody's

13:00 (US) Weekly Baker Hughes Rig Count data

15:00 (US) July Consumer Credit: $15.0Be v $12.4B prior

21:30 (CN) China Aug CPI Y/Y: 1.6%e v 1.4% prior; PPI Y/Y: 5.4%e v 5.5% prior