Sample Category Title

EUR/GBP On The Move

EUR/GBP is trading in the red after the retest of the median line (ml) of the minor ascending pitchfork. The next downside target will be at the 50% Fibonacci line (ascending dotted line), but it could drop at least till will reach the 0.9000 psychological level. Could be attracted by the confluence area formed by the ML with the lower median line (lml).

Cable Broke above 1.3200 Barrier in Extended Bullish Acceleration

Cable broke above 1.3200 barrier in extended bullish acceleration, returning to the levels last visited in early August. The pair is driven by strong bullish sentiment, with thick daily cloud, above which the price emerged yesterday, underpinning the action. Extended wave C from 1.2852 met target at 1.3224 (FE 176.4%) and showing scope for final push towards key barriers at 1.3268 (03 Aug peak) and 1.3273 (Fee 200%). Strongly overbought slow stochastic on daily chart and RSI at the border of overbought territory suggest corrective action ahead, but without firmer signals so far. Daily cloud top at 1.3086 is key near-term support.

Res: 1.3224; 1.3268; 1.3300; 1.3346

Sup: 1.3200; 1.3151; 1.3100; 1.3086

Euro, Dollar and Gold in focus

Mario Draghi's cautious tone during Thursday's ECB press conference was unable to tame the rampant Euro bulls, sending the EURUSD to levels not seen since January 2015, to above 1.2050.

The Euro's aggressive appreciation continues to suggest that bullish investors have built immunity into Draghi's dovish mantra, with most focusing on Europe's encouraging macro fundamentals and QE tapering expectations. While Draghi stated that the recent volatility in the Euro required close attention and is a source of uncertainty, investors seemed to be more interested in the stronger than expected Eurozone growth seen so far this year. What really gave the Euro bulls a shot in the arm, was when Draghi stated that the bulk of the QE decision will be made in October.

The EURUSD also found ample support in Dollar weakness, which encouraged bulls to start renewed rounds of buying. Technical traders will be paying close attention to see if prices can stay above 1.2000. A breakout above 1.2080 should encourage a further incline higher towards 1.2140.

Dollar bears unstoppable

King Dollar was beaten black and blue by sellers this week, as expectations rapidly faded over the Federal Reserve raising U.S interest rates in December.

This has been another painful week for the beleaguered currency, as the combination of dovish comments from Federal Reserve Governor Lael Brainard, and reports of Federal Reserve Vice Chairman Stanley Fischer announcing his resignation, compounded the downside. Sentiment remains heavily bearish towards the Dollar moving forward, with further weakness expected as heightened political uncertainty in Washington and diminishing rate hike expectations weigh heavily on the currency.

From a technical standpoint, the Dollar Index is bearish on the daily charts. Sustained weakness below 91.00 should encourage a further depreciation towards 90.00.

Gold shines as Dollar tumbles

Gold's glimmer has attracted investors like a moth to a flame, with the metal appreciating to a yearly high above $1355 during Friday's trading session.

Jitters created from the tensions between North Korea and the United States have attributed to Gold's resurgence, while a weaker Dollar amid fading rate hike expectations, continues to fuel the upside. With uncertainty across the board and overall caution likely to stimulate the flight to safety, safe-haven assets such as Gold remain heavily supported. From a technical standpoint, the yellow metal is heavily bullish on the daily charts. There have been consistently higher highs and higher lows while prices are trading above the daily 20 SMA. The breakout above $1350 may open a path higher towards $1365. Daily bulls remain in firm control and are likely to secure more control, if Gold concludes the week above $1340.

Currency spotlight - USDCAD

The Canadian Dollar appreciated to a two-year high against the Greenback on Friday, as market players continued to digest the unexpected rate hike by the Bank of Canada.

A vulnerable Dollar has also played a leading role in the USDCAD's decline, with further downside expected as market players weigh on the prospects of more rate hikes by the Bank of Canada. From a technical standpoint, the USDCAD is heavily bearish on the daily charts. Sustained weakness below 1.2100 should encourage a further selloff towards 1.2000 and 1.1930, respectively.

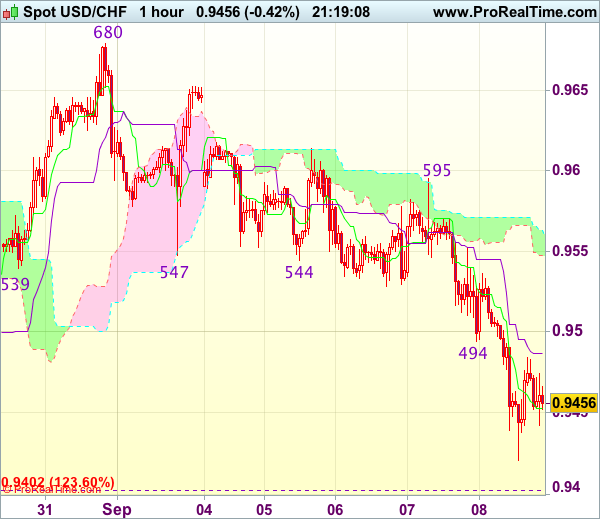

Trade Idea Update: USD/CHF – Hold long entered at 0.9450

USD/CHF - 0.9461

Original strategy :

Bought at 0.9450, Target: 0.9550, Stop: 0.9415

Position : - Long at 0.9450

Target : - 0.9550

Stop : - 0.9415

New strategy :

Hold long entered at 0.9450, Target: 0.9550, Stop: 0.9415

Position : - Long at 0.9450

Target : - 0.9550

Stop : - 0.9415

As the greenback has dropped again and has remained under pressure, marginal weakness from here cannot be ruled out, however, loss of near term downward momentum should prevent sharp fall below 0.9415-20 and prospect of a rebound remains, ab one the Kijun-Sen (now at 0.9496) would bring subsequent gain to 0.9550 but dollar needs to penetrate resistance at 0.9595 to signal low is formed.

In view of this, we are holding on to our long position entered at 0.9450. Below 0.9415-20 would risk weakness to 0.9390-00, having said that, further sharp fall below 0.9370-75 should not be repeated and reckon 0.9350 would hold from here, bring rebound later.

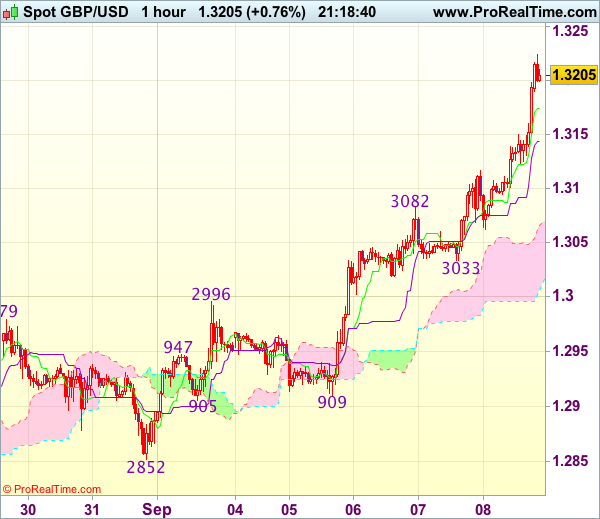

Trade Idea Update: GBP/USD – Buy at 1.3125

GBP/USD - 1.3200

Original strategy :

Buy at 1.3075, Target: 1.3175, Stop: 1.3045

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3125, Target: 1.3225, Stop: 1.3090

Position : -

Target : -

Stop : -

As cable has surged again after brief pullback, adding credence to our bullish view that recent upmove from 1.2774 is still in progress and upside bias remains for further gain to 1.3225-30, then towards 1.3250, however, loss of near term upward momentum should prevent sharp move beyond latter level and price should falter below recent high at 1.3269, bring retreat later.

In view of this, would not chase this rise at current level and would be prudent to buy cable on subsequent pullback as 1.3120-25 should limit downside. Only below 1.3082 (previous resistance turned support) would abort ad suggest top is possibly formed, risk test of 1.3062 but reckon support at 1.3033 (yesterday’s low) would hold.

Trade Idea Update: EUR/USD – Buy at 1.1985

EUR/USD - 1.2046

Original strategy :

Buy at 1.1985, Target: 1.2090, Stop: 1.1950

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1985, Target: 1.2090, Stop: 1.1950

Position : -

Target : -

Stop : -

Although the single currency surged again after breaking above previous resistance at 1.2070 and bullishness remains for recent upmove to extend gain to 1.2100, loss of upward momentum should prevent sharp move beyond 1.2130-40 and reckon 1.2150-55 (61.8% projection of 1.1119-1.1910 measuring from 1.1662) would limit upside, price should falter below 1.2175-80, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on subsequent pullback as support at 1.1980-84 should limit downside and bring another upmove later. Below 1.1950 (previous resistance turned support) would signal a temporary top is formed instead bring weakness to 1.1925-30 first.

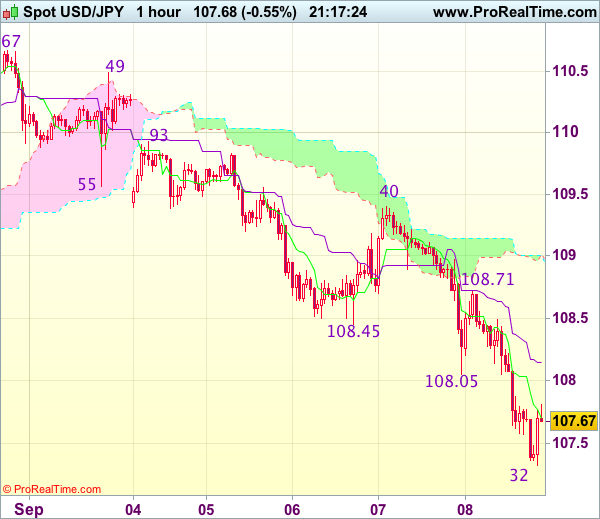

Trade Idea Update: USD/JPY – Sell at 108.45

USD/JPY - 107.68

Original strategy :

Sell at 108.45, Target: 107.45, Stop: 108.90

Position : -

Target : -

Stop : -

New strategy :

Sell at 108.45, Target: 107.45, Stop: 108.90

Position : -

Target : -

Stop : -

The greenback only recovered to 108.71 before dropping again as suggested (missed our short entry at 108.75) and price exceeded our indicated downside target at 107.75, bearishness remains for recent decline to extend further weakness to 107.20-25, however, near term oversold condition should limit downside and reckon 106.80-82 (61.8% projection of 114.50-108.27 measuring from 110.67) would hold from here, bring rebound later.

In view of this, we are still looking to sell dollar on recovery as 108.45-50 should limit upside. Above said resistance at 108.71 would defer and risk rebound to 109.00, break there would suggest low is possibly formed but only break of indicated resistance at 109.40 would confirm and signal recent decline has ended instead.

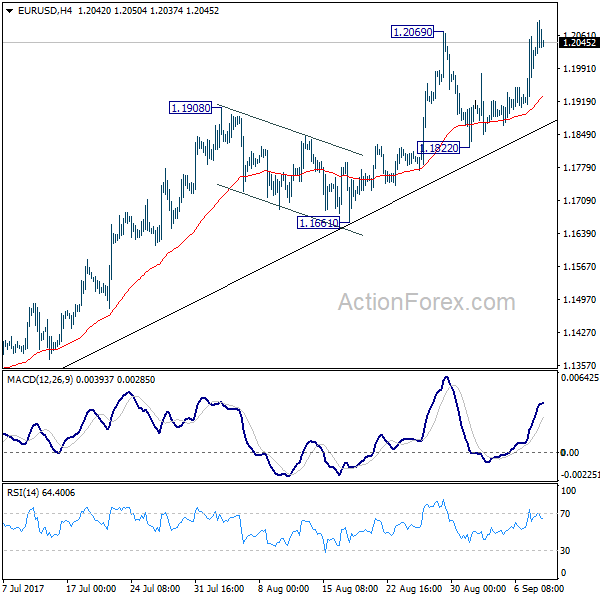

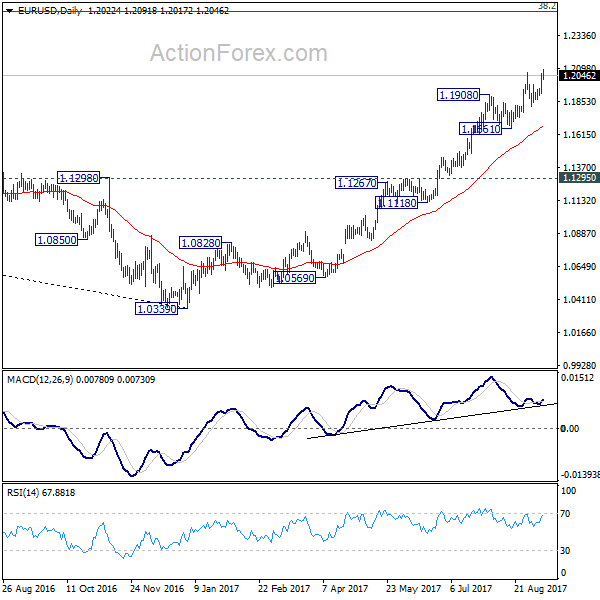

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1936; (P) 1.1997 (R1) 1.2082; More...

Intraday bias in EUR/USD remains on the upside for the moment. Medium term rise from 1.0339 has just resumed and further rise should be seen to next key fibonacci level at 1.2516. On the downside, break of 1.1822 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1774) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9468; (P) 0.9530; (R1) 0.9568; More....

Intraday bias in USD/CHF remains on the downside for the moment. Whole decline from 1.0342 should be resuming. Next target will be 61.8% projection of 1.0099 to 0.9437 from 0.9772 at 0.9363. On the upside, above 0.9493 minor resistance will turn bias neutral first. But outlook will stay bearish as long as 0.9679 resistance holds.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 107.91; (P) 108.59; (R1) 109.13; More...

Intraday bias in USD/JPY remains on the downside as the medium term decline from 118.65 has just resumed. Further fall should be seen to 61.8% retracement of 98.97 to 118.65 at 106.48. We'll look for support from there again to bring rebound. On the upside, above 108.45 minor resistance will turn intraday bias neutral first. But outlook will now stay bearish as long as 110.66 resistance holds.

In the bigger picture, pull back from 118.65 is viewed as a corrective pattern for the moment and downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound. Rise from 98.97 is expected to extend later to retest 125.85 high. However, sustained break of 106.48 will dampen this view and bring deeper fall to retest 98.97 instead.