Sample Category Title

USDJPY Pushes Above Fibonacci Resistance

The USDJPY pair has moved above strong historical Fibonacci resistance, hitting 108.95, after intraday sellers failed to push price-action below the August monthly price low, found at the 108.26 level.

After reaching a new September price low of 108.44, the USDJPY found strong intraday buying demand, with the pair now testing its calculated daily pivot point, at 108.88.

The USDJPY pair is currently neutral on an intraday basis, whilst trading above the 108.88 level. However, traders should note the bullish higher monthly price low, created on the charts, at 108.44.

Key intraday technical resistance is located at the 50-hour moving average, at 109.17, and the September 4th swing price low, at 109.38.

Key intraday USDJPY support is located at the long-term Fibonacci retracement level, 108.81, with further technical support at 108.60 and 108.44.

Below the 108.44 level, traders should look for further selling towards 108.26, 108.13 and 107.81.

GBP/JPY Switched To Uptrend

After a risk on sentiment where the Yen gained substantial strength versus its counterpart GBP, the pair is having a retracement now. Turmoil between the US and NK has turned the sentiment to risk on, leaving the retail gap behind on most Yen pairs. At this point we see a trend change and buying the dips could be the option. 141.55-70 is the POC zone (D L3, trend line, 50.0, ATR pivot) and another retracement in the pair should push it to the upside. 4h close and strong 1h momentum above 142.00 will target 142.16 as the first target then 142.50. Reaching 142.50 will open the door for the close of the retail gap. Only below 141.30 we could see 141.15, 141.00 and resume of downtrend.

Financial Markets Gripped by Geopolitical Turmoil

Financial markets were firmly gripped by geopolitical risks on Tuesday, as brewing tensions between the United States and North Korea weighed heavily on global sentiment.

Risk aversion is becoming a dominant theme amid escalating North Korean tensions, and the jitters punished Asian stocks during early trading on Wednesday. In Europe, shares ended mostly lower yesterday and have extended losses today, as the cautious mood from Asia encouraged investors to avoid riskier assets. The lack of appetite for risk sent U.S stocks to their lowest level in almost three weeks on Tuesday, with further downsides on the cards as the mixture of geopolitical tension and political uncertainty sours risk appetite.

The movements observed in stock markets and safe-haven assets suggest that markets have become increasingly sensitive to geopolitical influence. Recent comments from a North Korean diplomat threatening that the country was prepared to deliver 'gift packages' to the U.S is likely to fuel further risk aversion.

Dollar punished by Fed doves

King Dollar struggled to hold ground against a basket of major currencies during Wednesday's trading session, after dovish comments from Federal Reserve Governor Lael Brainard prompted investors to re-evaluate the likelihood of another rate hike this year.

Brainard stated that inflation was "well short" of targets and the central bank should be cautious about tightening policy until policy makers are confident that inflation will rebound. These dovish remarks have effectively trimmed market expectations of a December rate hike, exposing the Greenback to further pain.

As the trading month of September gets underway, Dollar weakness is likely to remain a dominant theme; political instability in Washington and fading rate hike expectations will weigh heavily on the currency. From a technical standpoint, the Dollar Index is under intense selling pressure on the daily charts. Repeated weakness below 92.00 should encourage a further depreciation towards 90.00.

Commodity spotlight - Gold

The heightened geopolitical risks over North Korea and ongoing concerns about stubbornly low inflation in the United States have supported Gold, with prices trading around $1340 as of writing.

The yellow metal has found itself back in fashion, with further upside expected as geopolitical tensions and political uncertainty in Washington accelerate the flight to safety. From a technical standpoint, Gold is bullish on the daily charts as there have been consistently higher highs and higher lows. A solid breakout and daily close above $1340 should open a path higher towards $1350.

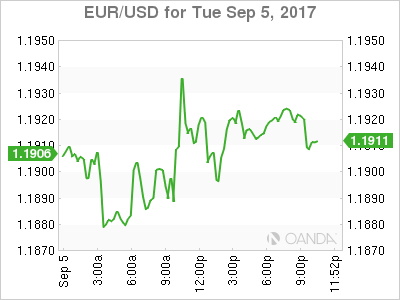

Currency spotlight - EURUSD

Thursday's main risk event for the Euro will be the highly anticipated European Central Bank meeting, which is expected to conclude with interest rates left unchanged.

The prospects of the European Central Bank tapering QE have heavily supported the Euro and, with the current QE program due to end in September, tomorrow's ECB meeting will be in sharp focus. While markets were widely expecting the central bank to announce the winding down of its QE program this week, the resurgent Euro and the impact it may have on the inflation target may prompt the central bank to wait until October.

From a technical standpoint, the EURUSD remains bullish on the daily charts. The breakout above 1.1900 should encourage a further appreciation towards 1.1970 and 1.2000, respectively. In an alternative scenario, repeated weakness below 1.1900 is likely to trigger a selloff towards 1.1770.

DAX Unchanged, Shrugs Off Soft German Factory Orders

The DAX index is unchanged in the Wednesday session. Currently, the DAX is currently trading at 12,118.50, down 0.05% on the day. On the release front, German Factory Orders dropped 0.7%, well off the forecast of a 0.2% gain. Eurozone Retail PMI edged lower to 50.8 points. On Thursday, the ECB releases its rate statement, followed by a press conference with ECB President Mario Draghi. As well, Germany releases Industrial Production and the Eurozone publishes Revised GDP.

German business leaders are closely following developments at the ECB, as the current quantitative easing (QE) scheme winds down in December. On Wednesday, Deutsche Bank chief executive John Cryan weighed in on the matter, calling on the ECB to alter course and stop providing “cheap money” to the markets. Cryan warned that the ECB’s monetary stance threatened to cause bubbles in the capital markets, including property, stocks and bonds. Cryan added that the stronger euro should not serve as an excuse for the ECB to continue its QE program. Turning to Brexit, Cryan argued that Frankfurt is ideally suited to take over from London as the financial hub for European banks. There is fierce jockeying in Europe as to who will take over from London, with Paris, Dublin and Amsterdam all hoping to pick up the spoils after Britain leaves the European Union.

The euro continues to trade at high levels, and EUR/USD broke above the symbolic 1.20 level in August.The euro has gained some 13% against the dollar in 2017, with two main reasons for the appreciation. First, the euro-area economy has looked impressive this year, led by robust growth in Germany. Second, there is increasing speculation that the ECB will taper its asset purchase program (QE), which is scheduled to terminate in December. The ECB is yet to decide what to do next, and analysts do not the details of the new program to be announced until October or possibly December. ECB policymakers must weigh competing interests – Germany would like nothing more than the ECB to simply exit the program, which was brought in as an emergency measure to begin with. However, other eurozone members, which are not enjoying German-style growth, favor a gradual tapering of the program, perhaps lowering monthly asset purchases from EUR 60 billion to EUR 45 billion. The stronger euro is equivalent to a raise in interest rates and has resulted in monetary tightening, so the ECB may favor a slow exit. Aside from the headache of a stronger euro, ECB policymakers must wrestle with the dilemma of a stronger economy that remains gripped by very low inflation. Will the ECB address these concerns at the Thursday meeting? Any hints about a change in monetary policy could have a sharp impact on the euro.

Australian Q2 GDP Growth Puts Pressure On The Aussie

A day after the Reserve Bank of Australia decided to hold cash rates at a record low of 1.5% and maintained its optimism about the future economic performance of the country, the Australian Bureau of Statistics (ABS) published the GDP growth figures for the second quarter on Wednesday. These surprised analysts to the downside pushing consequently the aussie down.

The Australian economy expanded by 0.8% quarter-on-quarter in the three months to June, 0.5 percentage points higher than in the previous quarter and registering its 26-year consecutive growth without a recession. Although this was a sign of improvement, analysts anticipated GDP to grow slightly higher by 0.9%. On an annual basis, the figure was up by 0.1 to 1.8% but below the 1.9% forecasted.

In current prices, GDP growth declined by 0.1% due to decreasing coal and iron prices. The chief economist at the ABS said that lower iron and coal prices, observed in the second quarter, weighed on export revenues and real incomes. However, export volumes continued rising in the aforementioned period.

Looking at the GDP components, final consumption increased by 0.2 percentage points to 0.8%, posting the highest rise since September 2016, while capital expenditure more than tripled to 1.5% from an upwardly revised 0.4% (from -0.6%) in the prior period. Consequently, households saved less, with the saving rate dropping from 5.3% to an 8 ½-year low of 4.6%.

The report also mentioned that the compensation of employees increased by 0.7% as Australians’ worked more despite the subdued wage growth.

While the above data justify the RBA’s positive view on the country’s economic performance, the central bank’s 2018 GDP growth forecast of 3.0% might be overestimated as household debt- to- income ratio remains at the extremely high level of 190% – one of the highest indebtedness levels in the world – while wage growth rose at the inflation rate of 1.9% on a yearly basis in the second quarter. The monetary policy statement published after the RBA monthly meeting yesterday indicated that policymakers agreed to keep rates steady at a record low of 1.5% as household debt continues fluctuating at high levels, while the exchange rate remains strong. Nevertheless, the RBA Governor Philip Lowe explained on Tuesday that the current monetary policy is accommodative as it limits the risks arising from the high and rising household debt. Moreover, he remained optimistic about country’s economic outlook and specifically about labor market developments, saying that “It is likely that as our economy strengthens and the demand for labor picks up, growth in wages will pick up too”.

In the forex markets, the aussie dropped immediately by 0.46% to an intra-day low of $0.7973 after the release of the data. Before the release, dollar/aussie was trading above the 0.80 key level, near the one-week high of 0.8027 reached yesterday.

Euro Edges Up Despite Weak German Factory Orders

EUR/USD is showing little movement this week, as the pair hovers close to the 1.19 level. Currently, the pair is trading at 1.1942, up 0.24% on the day. In economic news, German Factory Orders declined 0.7%, well off the forecast of a 0.2% gain. Eurozone Retail PMI edged lower to 50.8 points. In the US, today's key event is the ISM Non-Manufacturing PMI, which is expected to strengthen to 55.8 points. On Thursday, the ECB releases its rate statement, and the US publishes unemployment claims.

The streaking euro broke above the symbolic 1.20 level in August, and could make another run at 1.20 this week. The euro has gained some 13% against the dollar in 2017, with two main reasons for the appreciation. First, the euro-area economy has looked impressive this year, led by robust growth in Germany. Second, there is increasing speculation that the ECB will taper its asset purchase program (QE), which is scheduled to terminate in December. The ECB is yet to decide what to do next, and analysts do not the details of the new program to be announced until October or possibly December. ECB policymakers must weigh competing interests – Germany would like nothing more than the ECB to simply exit the program, which was brought in as an emergency measure to begin with. However, other eurozone members, which are not enjoying German-style growth, favor a gradual tapering of the program, perhaps lowering monthly asset purchases from EUR 60 billion to EUR 45 billion. The stronger euro is equivalent to a raise in interest rates and has resulted in monetary tightening, so the ECB may favor a slow exit. Aside from the headache of a stronger euro, ECB policymakers must wrestle with the dilemma of a stronger economy that remains gripped by very low inflation. Will the ECB address these concerns at the Thursday meeting? Any hints about a change in monetary policy could have a sharp impact on the euro.

US employment numbers were anything but impressive last week, as nonfarm payrolls tumbled to 156 thousand and wage growth slowed to just 0.1%. The soft numbers weren't lost on the Federal Reserve, as FOMC member Leal Brainard weighed in interest rate policy on Tuesday. Brainard noted that inflation remained “well short” of the Fed's target of 2%, and urged the Fed to act cautiously and resist raising interest rates until inflation moves higher. Brainard did acknowledge the rebound in the US economy, saying that the economy was on “solid footing”. A December rate hike remains very much in doubt, with odds of an increase at just 30%. With the likelihood of a rate hike pegged at less than 2% at next week's policy meeting, the markets will be focusing on the Fed's balance sheet, which stands at $4.2 trillion. Earlier in the year, the Fed outlined plans to reduce the balance sheet, and analysts expect further details at the September meeting.

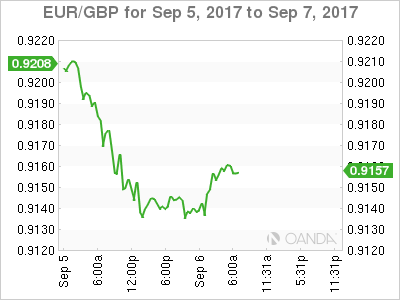

Elliott Wave Analysis: EURGBP Intra-day View

EURGBP made a new drop lower, which suggests, that black wave ii of a higher degree is completed at the 0.92300 region. This means, that current drop can now represent blue wave 1 of three, that can follow in days ahead. At the moment we see price specifically trading within sub-wave 4) of one, that can search for resistance near the Fibonacci ratio of 38.2.

EURGBP, 1H

BoC Decision Eyed As Geopolitical Risk Continues To Weigh

- North Korea concerns weigh on risk appetite;

- USD struggling at lows as more Fed officials voice inflation concerns;

- BoC may signal another rate hike this year;

- EURUSD approaches 1.20 to the dismay of the ECB.

US futures are almost flat ahead of the open on Wednesday, broadly reflecting the kind of moves seen elsewhere as safe haven flows subside but risk appetite remains weak.

There is clear concern about the escalating tensions between the US and North Korea which has culminated in repeated stints of risk off trading in recent weeks. With the increasingly frequent tests in North Korea triggering such moves, it's making traders a little more anxious than normal and it seems that for now, sitting on the side-lines is preferred.

The verbal back and forth isn't helping matters, although it is having less of a negative impact than it was a few weeks ago. Should the tests in the North and military exercises in the South continue in the coming weeks, it is possible that traders start to pay less and less attention on the belief that this is as far as it will go. For now though, no such confidence clearly exists.

The US dollar's traditional position as a safe haven currency is doing little to support it at the moment. Dovish remarks from three Federal Reserve officials on Tuesday appeared to further drive home the belief that another rate hike this year now looks increasingly less likely. It seems that few voters on the FOMC are still confident that inflation is on the right trajectory and instead a wait and see consensus has been building. With the market implied odds of a rate hike now standing at 37% and Fed commentary now reflective of this, a significant improvement in the inflation outlook may be needed to secure the third hike the central bank previously anticipated.

The only interest rate decision that matters today though is that from the Bank of Canada, which began tightening at its last meeting in July – its first hike since September 2010 – and is expected to do so one more time this year. This meeting may come a little soon though, with investors expecting the central bank to remain on hold for now but they will be keen to hear whether expectations of another are correct. With inflation so far below target, there is good reason for the central bank to leave it at one for now but with the last having also come at a time when inflation was low, it may not act as a deterrent should they wish to go again.

The euro is creeping higher against the dollar again today, moving ever closer to the 1.20 level that is proving tough to overcome. Not only are traders apparently wary of this level but the ECB has shown itself to be as well. I guess we'll find out just how uncomfortable the ECB is tomorrow when it makes its monetary policy announcement and Mario Draghi holds his press conference. September had long been touted as the meeting at which further reductions to asset purchases would be announced but recent remarks would suggest they'll hold off until later in the year before doing so, with the euro rate clearly a concern to them.

Will The Bank Of Canada Surprise With A Rate Hike?

Wednesday September 6: Five things the markets are talking about

For investors, looking past North Korea geopolitical concerns, another hurricane bearing down on the U.S and the American debt ceiling looming, there are two central banks decisions that should provide a test for capital markets – there is today's Bank of Canada (BoC) decision (10 am ETD) and tomorrows European Central Bank (ECB) rate announcement and the accompanying press conference.

The BoC rate decision is a coin toss – Canadian policymakers hiked +25 bps in July to +0.75%. Recent consumer, housing and labor-market data also support getting on with hikes. However, the naysayers suggest that some receding in business activity indicators suggest policymakers can afford to take a more standard path of hiking on a quarterly schedule and wait until next month's meeting (Oct. 25) to back up rates again.

Of all asset classes, the euro is likely to react the most to tomorrow's European Central Bank (ECB) policy decision (07:45 EDT).

The 'single' currency strength is hindering the central bank's efforts to drive inflation higher and may prompt the ECB to delay announcing plans to reduce monetary easing. Many expect President Draghi to address the pace of EUR (€1.1936) appreciation during his press conference accompanying the policy decision.

Later this afternoon, the market will focus on Fed's Beige Book for inflation outlook clues (2pm EDT).

1. Stocks remain on the back foot

Global equity markets trade broadly weaker on uncertainty in U.S policy and North Korea's latest nuclear test on the weekend.

In Japan, stocks ended little changed overnight as retail investors' buying in small-to-mid sized stocks offset losses incurred when the market tumbled to four-month lows on heightened tensions in the Korean Peninsula. The Nikkei ended -0.1% lower, while the broader Topix ended +0.1% higher.

In Hong Kong, stocks retreated, mirroring Wall St. as geopolitical worries prompted investors to take profits on this year's +25% rally. The Hang Seng index fell -0.5%, while the China Enterprises Index lost -0.6%.

The Kospi index in South Korea slid -0.3%, as did Australia's S&P ASX 200 when Q2 GDP came in slightly lower than expectations.

In China, stocks dip but reform hopes largely offset N. Korea worries. The CSI300 index fell -0.2%, while the Shanghai Composite Index closed little changed.

In Europe, regional bourses trade largely lower following Asia and Wall St., although the indices trade off the session lows on market jitters ahead of the ECB rate decision tomorrow.

U.S stocks are set to open in the 'black' (+0.1%).

Indices: Stoxx600 -0.3% at 372.5, FTSE -0.5% at 7336, DAX -0.1% at 12110, CAC-40 -0.2% at 5077, IBEX-35 -0.4% at 10141, FTSE MIB +0.4% at 21829, SMI =0.6% at 8817, S&P 500 Futures +0.1%

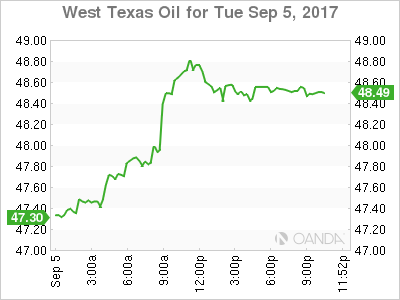

2. Oil markets subdued by Harvey fallout; gold higher

Ahead of the U.S open, oil is trading with caution, as crude demand and shipments remain subdued due to refinery closures following Storm Harvey and the arrival of an even bigger hurricane in the Caribbean.

Note: With many refineries, pipelines and ports beginning to come back on line, it's expected to take weeks before the U.S petroleum industry is back to capacity.

As of yesterday, approximately 20% of U.S daily refining capacity remained shut, while several other refineries were running at reduced rates.

The markets attention is now shifting towards the massive Category 5 storm Hurricane Irma, which is now in the Caribbean and set to head towards Florida where it could disable other U.S refineries.

Brent crude futures have dipped -8c to +$53.20 a barrel, while U.S West Texas Intermediate (WTI) crude futures were at +$48.69 barrel, little changed from yesterday's close.

Note: Fuel storage data due for release later today by API and EIA tomorrow should give a better view of the extent of Harvey's impact on U.S fuel inventories.

Gold is up for a fifth consecutive day overnight as geopolitical risks over North Korea remain elevated, and as low U.S inflation concerns has left some Fed officials to back delays in further interest rate hikes. Spot gold is up +0.1% at +$1,339.87 per ounce – it touched an intraday high for the month at +$1,344.21 yesterday.

3. Sovereign yields track lower

Geopolitical safe haven demand coupled with insights from two of the most 'dovish' Fed officials yesterday has helped guide U.S 10-year Treasury yields to fresh low yields for the year.

Governor Brainard has urged monetary policy makers to “wait for more realized progress” on the Fed's inflation goal before lifting rates again, while Minneapolis Fed President Kashkari warned that the central bank's tightening cycle “may have harmed the U.S economy.”

Note: Fed speak continues, with regional Fed Presidents Robert Kaplan and Loretta Mester slated to deliver remarks.

10-year Treasury yield dropped -10 bps to +2.07%, while the 10/30 curve spread has widened slightly to +62 bps.

In the U.K, 10-year Gilt yield fell -2 bps to +1.011%, the lowest in more than a week, while German Bund 10-year yield dipped less than -1 bps point to +0.34%, the lowest in more than 10-weeks.

4. Dollar under the weather

The USD price action is moving in tow with lower U.S treasury yield spreads that have been pressured by 'dovish' Fed remarks over the past 24-hours. U.S 2/10 spread has flattened to its lowest level in 12-months. Today's Fed's Beige book (2.00 pm EDT) should give investors an insight on how the Fed is thinking about inflation.

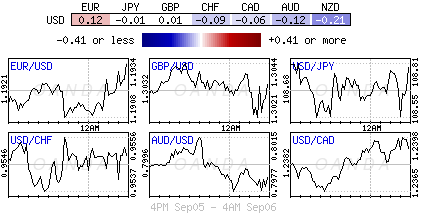

EUR/USD (€1.1940) is +0.25% higher outright as shape of yield curves Euro peripheral countries continued to return to normal levels as anticipation mounts that the ECB will taper–and eventually exit–its QE program. Tomorrow's ECB press conference is expected to shed more light on that.

USD/JPY (¥108.70) is little changed, while GBP (£1.3048) has rallied to a four-week high ahead of the U.S open.

Down-under overnight, the AUD (A$0.7978) briefly held some strength for most of the session before falling back after Australia's Q2 GDP came in slightly lower than expectations (see below).

5. Aussie economy solid in Q2

Despite being lower than expectations, the +0.8%, q/q, and +1.8%, y/y, solidly beat Q1 results.

The headline print should sit well with the RBA's optimism about the economy there. Still, concerns hang over the combination of record-low wage growth and record household debt. The strong Aussie dollar is also a risk to growth.

The solid report prompted Treasurer Morrison to talk up the prospect of an improved deficit compared to forecasts in May's budget. For that year, the Aussie government in May projected a -A$37.6B deficit.

Morrison says a more-conservative approach to forecasting has helped the government surpass market expectations and maintain its AAA credit rating.

Market Update – European Session: Focus On Fed Beige Book For Inflation Outlook

Notes/Observations

USD is the most sensitive to moves in the bond market in the whole time history back to the late 1990s

Fed’s Beige looked for on insight on how the Fed is thinking about inflation

Overnight

Asia:

Australia Q2 GDP registered a slight miss (Q/Q: 0.8% v 0.9%e; Y/Y: 1.8% v 1.9%e)

Japan July Real Cash Earnings registers its fastest decline since June 2015 (Y/Y: -0.8% v 0.0%e)

China PBoC performs its 1st injection in reverse repo operation after 4 consecutive skips

Europe:

Britain reportedly plans to end free movement of labor following the Brexit. Intends to decrease the number of lower-skilled EU migrants in its immigration document. All but the most highly skilled workers would have to leave after two years

UK Brexit Sec Davis commented to parliament: Clear both sides in Brexit talks have very different legal stances on Brexit bill: expected argument about Brexit bill to go on for full duration of negotiation

Latest Forsa poll on upcoming German Federal elections: Chancellor Merkel's conservatives (CDU/CSU) seen winning 38% (unchanged); Social Democrats 23% (-1)

German Stern-RTL Poll: CDU/CSU 38%(-1); SPD 23% (unchanged)

Americas:

Fed's Kaplan (moderate, voter) reiterated should be patient on rates. Fed may still raise rates this year, but he wants to see more information..Reiterated wants to get going on the balance sheet. Will be well-served to work down balance sheet so has 'dry powder' for a future crisis.

Fed's Kashkari (dove, voter): Fed rate hikes may have done real harm to the economy; premature Fed rate hikes are not free

US House Majority Leader Mccarthy (R): House to vote on Harvey, debt bill if Senate passes measure

President Trump is sticking with his target of 15% (current 35%) for the corporate rate, even though advisers working on tax reform have told him it's not a workable figure

Trade Rep Lighthizer: no NAFTA issues have been totally completed after two rounds of talks; thinking of terminating NAFTA is not a crazy position but hopes to reach deal that Trump can support

Brazil Attorney General alleges former Presidents and allies took millions of dollars in bribes over a 14-year period which caused $9.0B loss to the national treasury

Energy:

Russia Energy Min Novak: Confirms OPEC and Russia may extend oil output cap if needed; OPEC deal terms may change after Q1

Hurricane Irma: categorized as Cat 5 hurricane and expected to be most powerful Atlantic storm in a decade

Economic data

(DE) Germany July Factory Orders M/M: -0.7% v +0.2%e; Y/Y: 5.0% v 5.8%e

(SE) Sweden July Industrial Production M/M: -0.9% v -0.2%e; Y/Y: 5.3% v 6.5%e

(IT) Italy July Retail Sales M/M: -0.2% v -0.2%e; Y/Y: 0.0% v 1.2%e

Fixed Income Issuance:

(IN) India sold total INR170B vs. INR170B indicated indicated in 3-month and 6-month Bills

(DK) Denmark sold total DKK2.62B in 2020 and 2027 Bonds

(EU) ECB allotted $85M in 7-day USD Liquidity Tender at fixed 1.66% vs $35M prior

(SE) Sweden sold total SEK2.5B vs. SEK2.5B indicated in 2028 and 2032 Bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 372.5, FTSE -0.5% at 7336, DAX -0.1% at 12110, CAC-40 -0.2% at 5077, IBEX-35 -0.4% at 10141, FTSE MIB +0.4% at 21829, SMI =0.6% at 8817, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade largely lower following on from the retreat on Wall Street yesterday, although Indices trade off the session lows on continuing geopolitical worries and jitters ahead of the ECB rate decision tomorrow. Microfocus outperforms after results from HPE, while Home builders Barratt Development and Berkeley group trade lower after results. OCI NV in the Netherlands trade sharply higher after results and naming a new CFO, and Petrofac trades 5% higher after being awarded a significant contract award.

European Autos outperform after being upgraded at Goldman Sachs, with out performance in Daimler.

Looking head into the US morning, retail earnings continue with notable earners including Freds, GIII Apparel and HD Supply.

Equities

Consumer discretionary [Sports Direct [SPD.UK] +2.8% (Trading update), Clas Ohlssen [CLASB.SE] -4% (Earnings), Boohoo [BOO.UK] +4.8% (Analyst upgrade), Straumann [STMN.CH] -2.6% (treasury share sale)]

Industrials: [BAE [BA.UK] -1.1% (UK Seeking to increase competition in Naval shipbuilding business - press), OCI [OCI.NL] +6.7% (Earnings, new CFO)]

Technology: [Wandisco [WAND.UK] -7% (Earnings), Micro Focus [MCRO.UK] +8% (HPE results)]

Healthcare [Vectura (VEC.UK) -11.7% (Earnings, VR410 agreement)]

Energy: [Petrofac [PFC.UK] +4.6% (Contract win)]

Real Estate: [Barratt Dev [BDEV.UK] -3.0% (Earnings), Berekley Group [BKG.UK] -2.4% (Trading update)]

Speakers

ECB's Nouy (SSM chief): EU banks face a series of challenges.Banks must be allowed to fail without disrupting system

EU's Moscovici reiterated view of need to push through economic reforms. EU to unveil internet tax proposal soon

Italy Treasury official 2017 GDP growth could exceed 1.5%

Sweden National Financial Management Authority (ESV) fiscal watchdog) raised its 2017 and 2018 GDP growth forecasts. Raised 2017 GDP growth forecast from 2.8% to 3.1% and 2018 GDP growth forecast from 1.9% to 2.1%

Council of the Catalan Parliament accepted referendum bill for debate

Turkey Dep PM Simsek: Inflation is likely to fall back to single digits in December

Russia President Putin reiterated view that North Korea situation could not be resolved through sanctions and pressure. Discussed North Korea situation with South Korea President Moon; believes joint projects between the two nations will help stabilize the Peninsula

South Korea President Moon: Oil cutoff for North Korea was unavoidable

South Korea Defense Min Han Min-koo: Remaining THAAD missile launchers to be deployed on Thurs, Sept 7th

Currencies

USD price action appears to be moving in line with lower US treasury yield spreads. The US 2-year/10-year yield spread has flattened to the lowest level since September 2016. The greenback failed to respond after the US treasury sold new four-week bills at 1.3% for its highest yield since 2008 as Fed officials appear more subdued inflation. Fed’s Beige being eyed on insight on how the Fed was overall thinking about inflation

EUR/USD higher by 0.25% as shape of yield curves of peripheral countries continued to return to normal levels as anticipation mounts that the ECB will taper--and eventually exit--its QE program

USD/JPY little changed at 108.70 just ahead of the NY morning

Fixed Income

Bund futures trades at 162.59 down 29 ticks, as bund futures gradually edge lower as stocks bounce from the open as new low-delta downside is added in options ahead of ECB meeting. Downside targets 160.50 followed by 160.29. To the upside the 163.75 to 165.00 remains key resistance.

Gilt futures trades at 128.50 down 15 ticks off the session highs as the 7-15year buyback comes into focus. A resumption to the upside could eye 128.71 then 130.10. A move back below 126.51 targets 125.04

Wednesday’s liquidity report showed Tuesday’s excess liquidity rose to €1.780T from €1.776T and use of the marginal lending facility rose to €248M from €106M.

Corporate issuance saw $22.1B come to market via 14 issuers, a new 2017 record for highest number of deals. Apple announced a $5B 4-part note unsecured note offering

Looking Ahead

05:30 (ZA) South Africa Aug SACCI Business Confidence: No est v 95.3 prior

05:30 (DE) Germany to sell €3.0B in 2022 Bob

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell combined RUB40B in 2022 and 2033 OFZ Bonds

07:00 (US) MBA Mortgage Applications w/e Sept 1st: No est v -2.3% prior

07:00 (BR) Brazil Aug FGV Inflation IGP-DI M/M: +0.2%e v -0.3% prior; Y/Y: -1.6%e v -1.4% prior

07:30 (TR) Turkey Aug Effective Exchange Rate (REER): No est v 89.39 prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (HU) Hungary Central Bank (NBH) Aug Minutes

08:00 (BR) Brazil Aug IBGE Inflation IPCA M/M: 0.3%e v 0.2% prior; Y/Y: 2.6%e v 2.7% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) July Trade Balance: -$44.6Be v -$43.6B prior

08:30 (CA) Canada July Int'l Merchandise Trade (CAD): -3.3Be v -3.6B prior

08:30 (CA) Canada Q2 Labor Productivity Q/Q: No est v 1.4% prior

08:55 (US) Weekly Redbook Sales

09:45 (US) Aug Final Markit Services PMI: 56.9e v 56.9 prelim, Composite PMI: No est v 54.6 prior

10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.75%

10:00 (US) Aug ISM Non-Manufacturing Composite: 55.5e v 53.9 prior

10:00 (PL) Poland Central Bank Gov Glapinski to hold post rate decision press conference

10:20 (BR) Brazil Aug Vehicle Production: No est v 224.8K prior; Vehicle Sales: No est v 184.8K prior; Vehicle Sales: No est v 184.8K prior; Vehicle Exports: No est v 65.7K prior

11:00 (BR) Brazil to sell 2023 LFT

11:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills

11:30 (BR) Brazil weekly Currency Flow data

14:00 (US) Federal Reserve Releases Beige Book

16:00 (BR) Brazil Central Bank (BCB) Interest Rate Decision: Expected to cut Selic Rate by 100bps to 8.25%

16:30 (US) Weekly API Oil Inventories