Sample Category Title

Majors Move Sideways ahead of Busy Weekly Calendar; Oil Down as Texas Energy Refineries Shut Down

With today's economic calendar lacking important data, major currencies were trading sideways during European trading hours, while market watchers were weighing the damage from the life-threatening tropical storm Harvey which forced the closure of the Texas oil industry on Monday. However, in the coming days, forex markets will be on the receiving end of important data releases from major economies.

The dollar struggled to recover from the 2-½-year lows it recorded against its rivals during early Asian session after the Fed Chief Janet Yellen avoided commenting on future monetary policy plans on Friday at the Jackson Hole conference. Instead, she sounded more dovish when she supported that any adjustments on financial rules should be "modest". With the political mess in the background and the US President currently dealing with the disastrous effects of the thunderstorm Harvey in Texas, investors will also keep a close eye on data releases out of the country in the following days. Particularly, releases will include an update on second quarter GDP on Wednesday, PCE figures, and housing numbers on Thursday, while on Friday the widely expected non-farm payrolls will offer clues on labor conditions and likely affect the Fed's take on the monetary policy outlook.

Moreover, NAFTA members are expected to launch a second round of talks in Mexico City on Friday, following Trump's renewed threat on Sunday to terminate the trade deal. Specifically, Trump characterized the deal as the "worst trade deal made ever" questioning whether the 23-year old agreement should end.

Meanwhile, the Bureau of Economic analysis published data on the goods trade balance while the US Census Bureau released initial figures on wholesale inventories for the month of July. According to the numbers, the goods trade deficit came in higher than expected at $65.10bn compared to the $64.50bn that was expected and the $64.01bn seen in the previous month. Wholesale inventories also weakened in the aforementioned month based on preliminary estimates but came in above expectations. Specifically, they grew by 0.4%, below June's mark of 0.7% but above the forecasted 0.2%.

The dollar index, which gauges the strength of the dollar against a trade-weighted basket of major currencies, traded flat at 92.34, slightly above the 15-month low of 92.27 reached earlier on Monday.

Dollar/yen rebounded to 109.21, recovering from losses made earlier when the Japanese government maintained its upbeat view on country's economic outlook. Particularly, the Cabinet office stated that business spending, exports, and output were "picking up" while it also said that private consumption was growing moderately, signaling a solid recovery.

Versus the safe-haven swissie, the dollar touched a one-month low of 0.9525 during early European trading hours. However, it managed to climb to 0.9543 afterwards.

The euro was moving sideways at $1.1932 after it hit a 2-½-year high of $1.1958 in the early Asian session, following ECB Chief Draghi's optimism on the Eurozone's recovery expressed at the Jackson Hole symposium last week. In addition, the euro was boosted as Draghi did not express concerns about the block's strengthening currency. Now, investors will wait for further economic releases out of the Eurozone including the unemployment rate and inflation before the ECB policymakers gather to decide on interest rates next week.

In the UK, the opposition Labour party stated on Sunday that it would make efforts to keep the UK in the single market during a transitional period after Brexit. Furthermore, British officials are meeting this week in Brussels to negotiate post-Brexit regulations as the European Union refuses to discuss on the topic unless the UK accepts to pay an exit bill related to its previous commitments. The EU representative Michael Barnier and the UK's David Davis, which are the two chief Brexit negotiators, are meeting today ahead of technical level meetings on Tuesday and Wednesday which will cover other exit issues including expatriate rights and the so called divorce bill.

Cable managed to reverse earlier losses, rising to 1.2920 in the late European session.

The commodity-linked loonie edged up against its US cousin as the catastrophic thunderstorm Harvey, which is the strongest seen in more than 50 years, hit the Texas Gulf of Mexico coast which is the main base of US energy production – producing half of the oil output – and forced major refineries in the area to shut down their operations. So far, a quarter of the oil production was affected at the US Gulf of Mexico, driving gasoline prices up by 7% to more than a two-year high. Dollar/loonie was last seen at 1.2475.

Regarding oil prices, WTI crude dropped by 1.13% to $46.74 per barrel while Brent fell by 0.54% to $51.87.

Gold was last trading above the $1,300 an ounce mark at $1,307, reaching its highest since early November when Donald Trump won the US presidency.

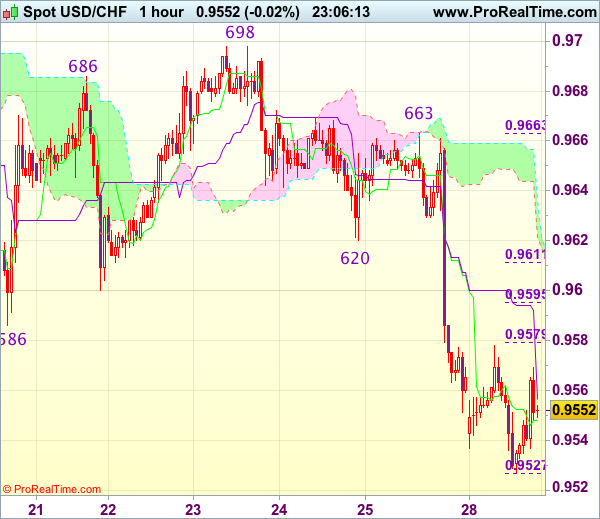

Trade Idea Wrap-up: USD/CHF – Sell at 0.9590

USD/CHF - 0.9552

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 0.9548

Kijun-Sen level : 0.9557

Ichimoku cloud top : 0.9636

Ichimoku cloud bottom : 0.9621

Original strategy :

Sell at 0.9590, Target: 0.9490, Stop: 0.9625

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9590, Target: 0.9490, Stop: 0.9625

Position : -

Target : -

Stop : -

Friday’s selloff together with the breach of previous support at 0.9583-86 confirm top has been formed at 0.9773 earlier and bearishness is seen for the erratic decline from there to extend weakness to 0.9520-25, then towards support at 0.9490, however, near term oversold condition should prevent sharp fall below latter level. Looking ahead, A drop below 0.9490 would signal early downtrend has resumed and extend far to 0.9455-60 but recent low at 0.9438 should hold from here.

In view of this, we are looking to sell dollar on recovery as previous support at 0.9583-86 should turn into resistance and limit dollar’s upside, bring another decline. Above another previous support at 0.9620 would defer and suggest a temporary low is possibly formed, bring rebound to 0.9650 but still reckon resistance at 0.9663 would hold from here.

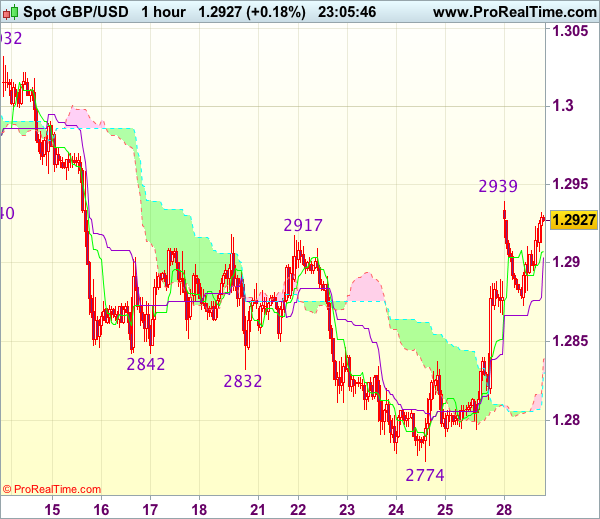

Trade Idea Wrap-up: GBP/USD – Buy at 1.2850

GBP/USD - 1.2920

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2907

Kijun-Sen level : 1.2903

Ichimoku cloud top : 1.2839

Ichimoku cloud bottom : 1.2830

Original strategy :

Buy at 1.2850, Target: 1.2950, Stop: 1.2815

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2850, Target: 1.2950, Stop: 1.2815

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after intra-day initial brief rise to 1.2939, adding credence to our view that a temporary low has possibly been formed at 1.2774 last week and bullishness remains for the rise from there to bring retracement of recent decline, above said resistance at 1.2939 would extend gain to 1.2970-80, then towards 1.3000 but price should falter below previous resistance at 1.3032.

In view of this, we are looking to buy sterling on pullback as 1.2850 should limit downside. Below previous resistance at 1.2837 would defer and risk test of 1.2810-15 but only break there would abort and signal the rebound from 1.2774 (last week’s low) has ended instead, risk weakness to 1.2775-80 first.

Trade Idea Wrap-up: EUR/USD – Buy at 1.0870

EUR/USD - 1.1963

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1943

Kijun-Sen level : 1.1915

Ichimoku cloud top : 1.1824

Ichimoku cloud bottom : 1.1824

Original strategy :

Buy at 1.1870, Target: 1.1970, Stop: 1.1835

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1870, Target: 1.1970, Stop: 1.1835

Position : -

Target : -

Stop : -

The single currency finally rallied on Friday and upmove gathered momentum after breaking indicated resistance at 1.1828 (now support) and euro eventually surged above recent high at 1.1910, adding credence to our bullish view for a resumption of recent upmove, hence upside bias remains for further gain to 1.1980, however, near term overbought condition should limit upside to 1.1200-10 and reckon 1.1250-60 would hold from here.

In view of this, would not chase this rise here and would be prudent to reinstate long on pullback as support at 1.0864 should limit downside and bring another upmove. Only below previous resistance at 1.1828 (now support) would abort and suggest a temporary top is possibly formed, risk test of 1.1800 but break of support at 1.1773 (Friday’s low) is needed to confirm.

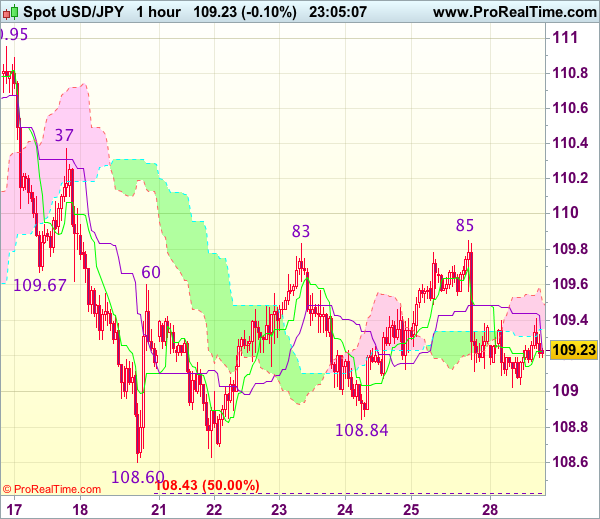

Trade Idea Wrap-up: USD/JPY – Hold long entered at 109.25

USD/JPY - 109.20

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.23

Kijun-Sen level : 109.22

Ichimoku cloud top : 109.50

Ichimoku cloud bottom : 109.35

Original strategy :

Bought at 109.25, Target: 110.25, Stop: 109.00

Position : - Long at 109.25

Target : - 110.25

Stop : - 109.00

New strategy :

Hold long entered at 109.25, Target: 110.25, Stop: 109.00

Position : - Long at 109.25

Target : - 110.25

Stop : - 109.00

Although the greenback retreated quite sharply after Friday’s marginal rise to 109.85, outlook remains consolidative, reckon downside would be limited to 109.00 and bring rebound later, above 109.50-55 would bring test of said resistance at 109.85, break there would extend the erratic rise from 108.60 low to 110.00, then towards resistance at 110.37 which is likely to hold from here.

In view of this, we are holding on to our long position entered at 109.25. Only below said support at 108.84 would abort and bring retest of said support at 108.60, break there would revive bearishness and confirm recent decline has resumed for further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.00.

Trade Idea: EUR/GBP – Buy at 0.9155

EUR/GBP - 0.9245

Original strategy :

Buy at 0.9115, Target: 0.9215, Stop: 0.9075

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9155, Target: 0.9295, Stop: 0.9115

Position : -

Target : -

Stop : -

As the single currency has maintained a firm undertone after recent rally, adding credence to our bullish view that the major rise from 0.8304 is still in progress and may extend further gain to 0.9275-80, then 0.9300-10 but weakening of near term upward momentum should prevent sharp move beyond 0.9330-35 and price should falter below 0.9350-55, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy euro on subsequent pullback as 0.9150-55 would limit downside. Below 0.9110-15 would defer and suggest a temporary top is possibly formed, risk test of support at 0.9063, however, break there is needed to add credence to this view, bring retracement of recent upmove towards 0.9005-10.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Dollar Stabilizes after Jackson Hole Sell-off

- European equities tread water in a low-volume trading session with UK markets closed for Summer Banking Holiday. US stocks markets opened marginally higher, awaiting key eco data later this week.

- Growth in EMU M3 money supply, an indicator which often predicts future economic activity, slowed sharply in July from 5% Y/Y to 4.5% Y/Y (vs 4.9% Y/Y expected), even as bank lending increased. Growth in corporate lending jumped to 2.4% Y/Y from 2.0% Y/Y, reversing most of its slowdown in June, when one-off factors dragged down growth. Lending growth to households held steady at 2.6% Y/Y for the third straight month, matching its best rate since March 2009.

- Economic confidence in Italy is at its highest level in almost 10 years, as recovery in the eurozone drives renewed optimism. The sub-index for manufacturing has been particularly strong in recent months as companies benefit from rising demand across the continent. Consumer sentiment, in contrast, had fallen back over the last year.

- The US merchandise trade deficit widened a bit in July (from -$64B to -$65.1B), while inventories at wholesalers increased (+0.4% M/M), according to preliminary figures from the Commerce Department in Washington.

- US gasoline futures jumped to two-year highs as Tropical Storm Harvey pummelled the heart of the US energy sector. The impact on oil prices is negligible so far.

- Confidence in Qatar's creditworthiness took another hit, as Fitch downgraded the country's debt rating from AA to AA-, citing concerns that the economic blockade imposed by Arab neighbours was unlikely to be lifted soon.

Rates

Slow start of the trading week

Bond trading was extremely thin and largely range-bound given today's UK banking holiday and uneventful eco calendar. Draghj's comments at the Jackson Hole symposium on Friday eve (after closure) (substantial accommodation is still needed and core inflation/wages show no signs of an uptrend yet) may help explain the modest curve steepening. The heavy rain fall, epic flooding and closure of some main ports in the Houston area had no immediate effect on the crude oil price (contrary to the gasoline price) and thus also not on bonds. Early losses of European equities and the subsequent recovery didn't cause the "usual" inverse movement with bonds. Italian manufacturing and consumer confidence printed stronger than expected, while the US trade deficit was a bit bigger than forecast, but the deviation was too small to trigger a meaningful reaction. All in all, an uneventful session. Later today, the US Treasury will sell 2- and 5-yr T-notes.

At the time of writing, the German yield curve steepens with yields slightly lower at the short end of the curve (<1 bp) and up 0.4 to 1.4 bps in the 10- to-30-yr sector. The US yield curve shows a similar pattern with yields marginally lower till the 5-yr tenor and up 0.7 bps and 1.5 bps in the 10-to-30-year sector. Intra-EMU yield spreads are virtually unchanged.

Currencies

Dollar stabilizes after Jackson Hole sell-off

EUR/USD and USD/JPY held extremely tight ranges after Friday's 'Jackson Hole rally of the euro/decline of the dollar'. Investors wait for additional input from EMU and US data later this week to assess whether those Jackson Hole moves were justified. EUR/USD trades in the 1.1930 area. USD/JPY hovers near 109.30/35.

Overnight, Asian equities traded mixed to slightly higher. Japanese indices were little changed as USD/JPY returned to the low 109 area. The PBOC set the fixing of USD/CNY at the strongest level for the yuan since August last year. The dollar remained in the defensive across the board. The trade-weighted dollar dropped to the 92.50 area. EUR/USD remained well bid and traded in the 1.1920 area.

There were only second tier eco data in Europe. The EMU money supply and lending data (July) were on the soft side. As usual, the report was largely ignored. European equities opened with losses of 0.50%. The post-Jackson hole rise of the euro was part of the explanation. US equity futures also traded with a slightly negative bias. EUR/USD held a tight sideways range in the 1.1925/45 area. Changes in US/EMU interest rates/differentials were limited. At least for now, the rise of the euro doesn't cause an outright outperformance of German bunds over US Treasuries. USD/JPY quite easily stayed north of USD/JPY 109 even as equities traded with a negative bias.

Sentiment on risk improved as US dealers joined the fray, even as there is uncertainty on the impact of the hurricane Harvey. For now, the market impact remains limited. WTI maintains a tight range in the $ 47 area. The dollar stabilizes after the post-Jackson hole setback. The US July trade deficit was slightly wider than wider an expected. However, there was hardly any market impact. Investors are looking forward to series of key eco data later this week to decide whether the Jackson Hole decline of the dollar is justified or not.

EUR/GBP: holiday-thinned trading

Today, sterling trading volumes were low as UK markets were closed for the Summer Bank holiday. Cable and EUR/GBP basically maintained the moves after the Jackson hole speeches of Yellen and Draghi on Friday. EUR/GBP held in the mid-0.92 area. Financial news wires elaborated extensive on the start of the 3th round of Brexit negotiations. However, until now, there was hardly any 'new news' on the issue. The EMU still wants significant progress on the terms of the separation. The UK wants to take a start with the negotiations on the future EU-UK relationship. EUR/GBP trades currently around 0.9245. Cable holds just north of 1.29.

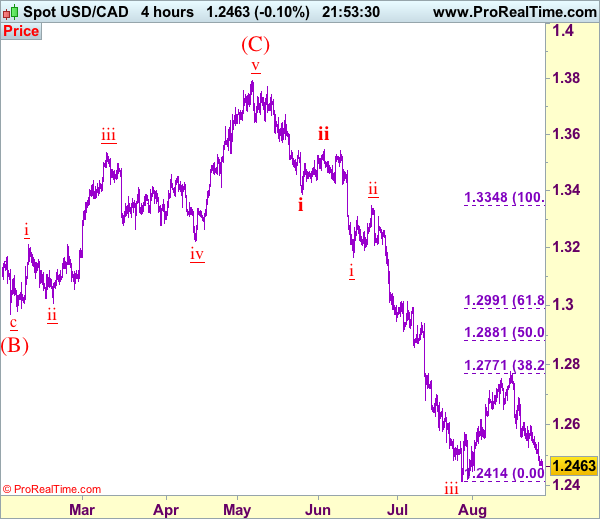

Trade Idea: USD/CAD – Hold short entered at 1.2690

USD/CAD - 1.2467

Original strategy :

Sold at 1.2690, met target at 1.2490

Position: - Short at 1.2690

Target: - 1.2490

Stop: -

New strategy :

Sell at 1.2550, Target: 1.2350, Stop: 1.2610

Position: -

Target: -

Stop:-

The greenback extended the selloff from 1.2778 in line with our bearish expectation, our short position entered at 1.2690 finally reached our downside target at 1.2490 (with 200 points profit), this anticipated selloff adds credence to our view that the wave iv correction from 1.2414 (wave iii trough) has ended at 1.2778, hence wave v is underway for retest of 1.2414 but break there is needed to provide confirmation and extend weakness to 1.2350, then towards 1.2300. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction possibly ended at 1.2778, wave v should extend towards 1.2300.

In view of this, we are looking to sell again on recovery as 1.2550-60 should limit upside. Only above indicated resistance at 1.2607 would defer and prolong consolidation, risk rebound to 1.2660 but resistance at 1.2691 should hold from here, bring further consolidation. Above 1.2691 resistance would risk a stronger rebound to 1.2740-50, however, said resistance at 1.2778 should hold. In the event the pair breaks said resistance at 1.2778, this would abort and signal the rebound from 1.2414 is still in progress for retracement of recent decline to 1.2825-30 but still reckon upside would be limited to 1.2880-85 (50% Fibonacci retracement of wave iii) and price should falter well below 1.2990-95 (61.8% Fibonacci retracement), bring retreat later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Harvey to Cloud Outlook

Hurricane Harvey went from a tropical storm to what will likely be one of the most damaging storms in history. The rains are expected to last through Wednesday and the scenes in Texas already point to a massive calamity that will cloud forecasts for many quarters. The euro was the top performer last week while the New Zealand dollar lagged. CFTC positioning showed specs making bigger bets on the euro against the pound.

Harvey was a Category 2 storm when markets closed Friday but grew to a rare Category 4 storm when it first made landfall a few hours later. After pounding southwest Texas the system then went back out to sea and is now working its way up the coast to Houston where scenes of incredible flooding are already underway.

It's far too premature to assess the scope of the damage but much of the oil refining in the area is offline and may stay that way all week. The result will be a squeeze on gasoline prices. Oil is a more-tricky trade because imports are cut off. The kneejerk reaction when markets open may be to bid up prices.

Economically we suspect the storm will surpass the damage from Sandy and may even rival Katrina. Those storms skewed growth lower immediately but led to stronger GDP during the rebuilding. The impossible task is knowing just how much is related to the storm and how much was unrelated. That uncertainty will be another reason for the Fed to hold off hiking in December and maybe beyond.

Other weekend news included some tidbits from Jackson Hole. Kuroda warned GDP won't continue at 4%, which isn't a surprise to anyone.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +88K vs +79K prior

- GBP -46K vs -32K prior

- JPY -74K vs -77K prior

- CHF -2K vs -1K prior

- CAD +51K vs +51K prior

- AUD +60K vs +60K prior

- NZD +22K vs +25K prior

The euro longs remain near the most extreme levels since 2011 while specs are increasingly convinced that Brexit is going to hit harder than thought a few months ago.

Second Round of NAFTA Renegotiation to Begin…

US President Donald Trump's renewed threat to withdraw from the North America Free Trade Agreement (NAFTA) reminds us that renegotiation of this 23-year-old deal has begun. While the US has accused Canada of both lumber and dairy trades, its focus is more on Mexico with Trump keeping demanding its third trading partner to pay the bill for construction of the wall along the border. In our opinion, the core of NAFTA renegotiation is to narrow US' trade deficit. With US' trade deficit with Canada on the fall, it would put harder pressure on Mexico in the negotiations. The market reaction towards NAFTA renegotiation has been muted, overshadowed by other events including North Korean peninsula tensions, US debt ceiling, and central banks' monetary policy outlook. Indeed, we do not expect to see material developments for the rest of the year. However, the parties, especially the US and Mexico, would be eager to complete a deal by mid-2018, ahead of and Mexican election in July and US mid-term election in November.

What is NAFTA?

NAFTA is a trade agreement between Canada, Mexico and the US that became effective in 1994 under President Bill Clinton. Like other FTAs, NAFTA eliminated almost all tariffs among the three states. Barriers on the cross-border flow of services are removed. However, it upholds the protection of intellectual property rights and allows each country to apply its own environmental standards. NAFTA is currently the world's largest free trade agreement with the three states contributing over US$20 trillion in terms of GDP.

Aim of Renegotiation

During his election campaign, Donald Trump had repeatedly criticizing NAFTA, claiming that it is a "disastrous trade deal" and the cause of the US job loss. Since he has been in office as the US President, Trump has sometimes threatened to terminate the deal although and sometimes indicated the willingness to renegotiate a new agreement. Despite his inconsistence, USTR on May 18 gave formal notice to the Congress that the President intended to commence negotiations with Canada and Mexico with respect to the agreement. After the 90-day consultation period, the first round of talks eventually took place in the US and concluded in August 20, failing to narrow down the divergence amongst the three countries, though. The second round of NAFTA talks would be held form September 1-5 in Mexico, followed by another round scheduled later in September in Canada, before returning to the US.

Reduction on US Trade Deficit

At the "Summary of Objectives for the NAFTA Renegotiation" released in July, the Office of the United States Trade Representative (USTR) lain down the rationale for the renegotiation of this 23-year-old free trade relations among the US, Canada and Mexico. The essence of this 17-page summary is to "improve the US trade balance and reduce the trade deficit with the NAFTA countries". Other critical issues, including the rules of origin, elimination of the Chapter 19 dispute settlement mechanism and the increase in duty-free threshold (DMT) on e-commerce, are aimed at achieving a better trade position for the US

US-Canada

Together with China, Canada and Mexico are the top three trading partners with the US. The US has incurred most deficit with China but this would be dealt separately. In 2016, the US incurred a trade deficit of US$11B in goods with Canada but at the same time enjoyed a trade surplus in services of US$ 24.6B. Therefore, the focus of the US is in goods, not services. Indeed, the US goods deficit with Canada mainly lies on oil and gas trade. In a report released in March, the EIA indicated that energy accounted for about 5% of the value of all US exports to Canada and more than 19% of the value of all US imports from Canada in 2016. The value of US energy imports from Canada was US$ 53B, while the value of US energy exports to Canada was US$14B, last year. As a result, the US incurred a deficit of US$39B in energy trade alone with Canada last year. We expect the "problem" would ease in coming years as the US has become more and more self-reliant on oil production. Meanwhile, we notice that US' deficit with Canada has decreased for a second consecutive year, falling to the current level from US$ 36.5B in 2014

US-Mexico

Assuming US' self-reliance on oil production would lead to the decline in demand for Canadian oil, US' goods trade deficit with Canada would continue to narrow in the future. It is therefore prudent to believe that the US to put more pressure on Mexico in the NAFTA negotiation. Widening for three years in a row, US' trade deficit with Mexico increased +4.3% to US$ 63B in 2016, with vehicles, machinery, agricultural products the major imports to the US.

Lack of progress has been made in the first round of talks. Trump even renewed threat to leave NAFTA over the weekend, days before the beginning of the second round. Trump twitted that Canada and Mexico were "very difficult" over the renegotiation. He repeated that it was the "worst trade deal ever made", adding "may have to terminate?". Mexico responded by indicating it would not negotiate the trade deal via social media! The third largest trading partner of the US has recently trying to strengthen the relations with China, as it looks for an alternative in trade.

We do not expect any breakthrough in the second round of talks that begins on September 1. All parties would unlikely compromise in early stages of the negotiation. Our base case is that a deal would be reached eventually as we believe the US withdrawal from NAFTA is a "lose-lose" scenario that no party wants. While there might lack progress for the rest of the year, the parties would hope to reach a deal in the first half of 2018, before the Mexican election in July and the US mid-term election in November. The case would be complicated if a deal cannot be completed before the Mexican election. Opinion polls show that the leftist Morena party still gets the most support. Its leader, the populist Andrés Manuel López Obrador (a.k.a. AMLO), is opposing more aspects of the NAFTA and is against Trump. Although market reaction to recent rounds of negotiations would remain rather muted, we believe financial market volatility would increase as we approach July 2018.