Sample Category Title

AUD/USD Bouncing.

AUD/USD's short-term technical structure is bearish. Hourly support can be found at 0.7786 (18/07/2017 low). Hourly resistance is given at 0.8066 (27/07/2017 high). Expected to edge lower within downtrend channel.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view

USD/CAD Selling Pressure Continue

USD/CAD selling continues. Hourly support is given at a distance at 1.2414 (27/07/2017 low). Expected to show continued short-term bearish move.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low) before bouncing back. Strong resistance is given at 1.4690 (22/01/2016 high). The pair should head further lower.

USD/CHF Drifting

USD/CHF recovery bounce has stalled failing to break any key levels. Higher resistance is given at 0.9771 (15/06/2017 high). Hourly support lies at at 0.9584 (08/11/2017 low). Expected to show growing upside pressures.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Recovery Bounce

USD/JPY has bounced strongly off support. The pair is likely to retest towards former support at 108.13 (17/04/2017 low) . Expected to show another leg lower.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Bearish Pause

GBP/USD bearish momentum has stalled near key support at 1.2757. Hourly resistance is given at 1.2917 (18/08/2017 high). Hourly support at 1.2812 (12/07/2017 low) has been broken. Expected to show continued bearish pressures.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Fails To Break Trend Resistance

EUR/USD short-term bullish pressures are slowing down. Down trend resistance is located at 1.1816. Hourly resistance can be found at 1.1910 (02/08/2017 high) while hourly support lies at 1.1613 (26/07/2017 low). Expected to show renewed bearish pressures.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance holding at 1.1871 (24/08/2015 high) has been broken while strong support lies at 1.0341 (03/01/2017 low).

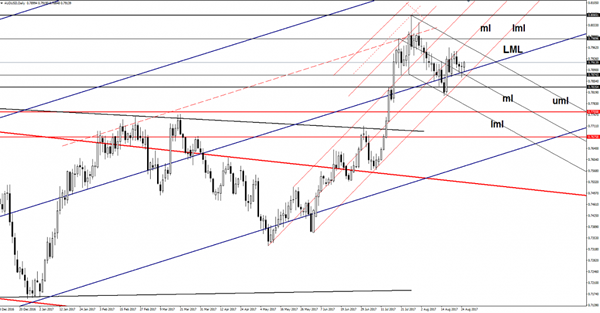

AUD/USD Throwback

AUD/USD climb higher after the retest of the lower median line (LML) of the major ascending pitchfork and now is targeting the upper median line (uml) of the minor descending pitchfork. Technically should jump much higher after the failure to close on the LML. Only the fundamental factors will send it below the dynamic support.

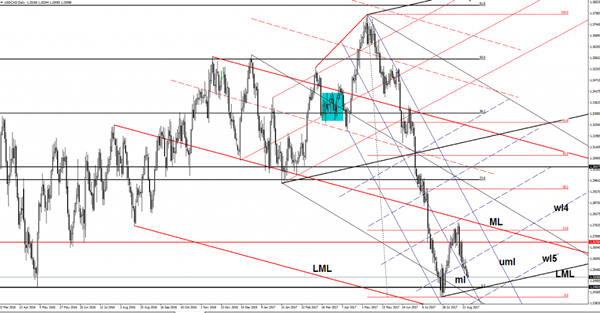

USD/CAD Losing Altitude

Price continues to drop and is expected to reach the major confluence area formed by the 1.2460 static support with the lower median line (LML) of the major black ascending pitchfork. It slips lower along the median line (ml) of the minor descending pitchfork, signaling that the bears are in full control.

EUR/USD Bloodless

Price changed little today and waiting to the afternoon's fundamental events to bring some volatility. Is still located in the buyer's territory, but needs a bullish spark to be able to resume the upside movement. Continues to move somehow sideways right now, is consolidating the latest gains, so we have to wait for a fresh trading signal.

Has shown some exhaustion signs in the last weeks, but maintains a bullish perspective as is located above some important support levels. We may have a high volatility in the afternoon as the economic calendar is filled with high impact data. The fundamental factors will take the lead, so you should be careful not to suffer a heavy loss.

The German Ifo Business Climate will be sent to the public earlier and is expected to drop from 116.0 to 115.0 points, while the German Final GDP could increase by 0.6%, matching the 0.6% growth in the former reading period.

The Yellen's and Draghi's speeches will shake the markets, remains to see how the EUR/USD will react, that's why will be better to stay away tonight.

Price hovers above the 1.1712 major static support, but failed to retest the upper median line (uml), signaling that could come down to retest the median line (ml) of the ascending pitchfork. The perspective remains bullish despite the minor retreat, should climb towards new peaks as long as the median line (ml) and the ML are intact.

FX Market Is Quiet Ahead Of Jackson Hole

Jackson Hole to be a non-event

After a soft start yesterday evening with comments from Fed’s George and Kaplan, who took opposite side about the highly discussed inflation issue, Janet Yellen and Mario Draghi will have the opportunity to present their views. We anticipate that Janet Yellen won’t take any risk and should come with a rather neutral stance, meaning that she’ll leave the door open for a tightening move before the end of the year, while at the same time maintaining a cautious tone in response to weak price pressures. However, keep in mind that the Fed Chair will talk about financial stability, which give her plenty of room to avoid any hot topic. There is great chance is will be a non-event.

However, Mario Draghi will have the difficult task to talk down the euro, which has surged substantially over the last weeks - the single currency reaching 1.1910 against the USD on August 2nd before stabilising at around 1.17 - while preparing the market for the end of the ECB’s quantitative programme. Indeed, the ECB’s September meeting is just around the corner and Draghi won’t have much opportunity to prepare at best investors.

The bottom line is that we expect the Jackson Hole Symposium to have much effect on the EUR and USD crosses. EUR/USD continues to trade within the 1.1662-1.1910 range. We still believe that maintaining a downside bias is the best choice.