Sample Category Title

Governing Council Worried Over Appreciating Euro And Low Inflation: ECB Minutes

For the 24 hours to 23:00 GMT, the EUR declined 0.42% against the USD and closed at 1.1728, following the release of dovish minutes from the European Central Bank's July meeting.

According to minutes, policymakers expressed concerns over stubbornly low inflation as well as continuous strength in the Euro and were highly aware of the risk that an excessive rise in the currency could threaten the central bank's efforts to spur inflation.

On the macro front, the Euro-zone's final consumer price index (CPI) rose 1.3% on an annual basis in July, confirming the preliminary print. In the prior month, the CPI had registered a similar rise. Additionally, the region's seasonally adjusted trade surplus widened more-than-anticipated to a level of €22.3 billion in June, notching its highest in six-months. Markets were expecting the region to post a surplus of €20.3 billion, after recording a revised surplus of €19.0 billion in the previous month.

The US Dollar traded mostly higher against a basket of currencies, after data indicated that initial jobless claims in the US dropped to a six-month low level of 232.0K in the week ended 12 August, higher than market consensus for a fall to a level of 240.0K. In the prior week, initial jobless claims had recorded a level of 244.0K. Moreover, the nation's leading indicators rose 0.3% in July, meeting market expectations and compared to an advance of 0.6% in the previous month.

Another set of data showed that industrial production in the US climbed 0.2% on a monthly basis in July, undershooting market consensus for a gain of 0.3%. Industrial production had risen 0.4% in the previous month. On the other hand, the nation's manufacturing production recorded an unexpected drop of 0.1% MoM in July, defying market expectations for a rise of 0.2%. In the previous month, manufacturing production had increased 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.1733, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1667, and a fall through could take it to the next support level of 1.1600. The pair is expected to find its first resistance at 1.1795, and a rise through could take it to the next resistance level of 1.1856.

Going ahead, investors will look forward to the Euro-zone's construction output data for June, slated to release in a few hours. Additionally, the US flash Reuters/Michigan consumer confidence index for August, scheduled to release later today, will be on investors' radar.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

British Retail Sales Grew Better-Than-Expected In July

For the 24 hours to 23:00 GMT, the GBP declined 0.16% against the USD and closed at 1.2874.

Macroeconomic data revealed that Britain's retail sales advanced above market expectations by 0.3% on a monthly basis in July, driven by strong sales in food. Retail sales had registered a revised similar rise in the prior month, while markets anticipated for a gain of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.2886, with the GBP trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2856, and a fall through could take it to the next support level of 1.2827. The pair is expected to find its first resistance at 1.2912, and a rise through could take it to the next resistance level of 1.2939.

With no economic releases in the UK today, investors will keep a close watch on Britain's 2Q GDP report, slated to release next week, to gauge strength in the nation's economy.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Marginally Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.55% against the JPY and closed at 109.49.

In the Asian session, at GMT0300, the pair is trading at 109.45, with the USD trading a tad lower against the JPY from yesterday’s close.

The pair is expected to find support at 109.04, and a fall through could take it to the next support level of 108.64. The pair is expected to find its first resistance at 110.11, and a rise through could take it to the next resistance level of 110.78.

Next week, market participants will focus on Japan’s national consumer price index and flash Nikkei manufacturing PMI data.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the CHF and closed at 0.9628.

In the Asian session, at GMT0300, the pair is trading at 0.9620, with the USD trading 0.08% lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9584, and a fall through could take it to the next support level of 0.9549. The pair is expected to find its first resistance at 0.9677, and a rise through could take it to the next resistance level of 0.9735.

Going forward, Switzerland's trade balance and industrial production data, set to release next week, will attract investor attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading On A Stronger Footing, Ahead Of Canada’s Inflation Data

For the 24 hours to 23:00 GMT, the USD rose 0.41% against the CAD and closed at 1.2679.

In economic news, Canada's manufacturing shipments declined 1.8% on a monthly basis in June, higher than market expectations for a drop of 1.0%. In the previous month, manufacturing shipments had registered a revised rise of 1.3%.

In the Asian session, at GMT0300, the pair is trading at 1.2664, with the USD trading 0.12% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2605, and a fall through could take it to the next support level of 1.2546. The pair is expected to find its first resistance at 1.2707, and a rise through could take it to the next resistance level of 1.2750.

This afternoon will bring a crucial Canadian release, namely the consumer price index for July.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 140.51; (P) 141.28; (R1) 141.73; More

GBP/JPY's decline resumed by taking out 141.24 and reaches as low as 140.60 so far. Intraday bias is back on the downside. Fall from 147.76 is still in progress and would extend through 138.65 support. Nonetheless, GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. Break of 143.18 resistance is needed to indicate short term bottoming. Otherwise, outlook stays bearish in case of recovery.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. But we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

Yen Surges on Spain Terrorist Attack and Trump Turmoil

The Japanese Yen takes the driving seat on risk aversion again. The global financial markets are rocked by the deadly terrorist attack in Barcelona and extended turmoil in the US White House. DOW closed down -274.14 points or -1.24% at 21750.73, taken out near term support at 21842.74. Same picture is seen in S&P 500 as it lost -38.1% or -1.54% to close at 2430.01, also taken out near term support at 2437.75. Nikkei follow in Asian session and slumps to 3-month low, and is trading down -1.1% at the time of writing. In other markets, gold is firm above 1290 but yet to find follow through buying for 1300 handle. WTI crude oil is trying to regain 47 after extending recent decline to as low as 46.46.

The terrorist attack in Barcelona, Spain is seen as the most violent one in recent years. It's reported that at least 13 people were killed and 100 more injured after a van plowed through the crowds in the popular tourist spot of Las Ramblas. ISIS took credits for the attack with its media wing, Amaq, describing the attackers as "soldiers of the Islamic State". But ISIS they didn't claim responsibility explicitly.

Trump ends plan for infrastructure council

Following Donald Trump's decision to disband business councils after resignation of a number of CEOs, he is ending plans for an advisory council on his USD 1T infrastructure project. There were also rumors that Gary Cohn, a key force behind Trump's tax reform program, might be resigning as the director of the US National Economic Council. It was reported that Cohn was "upset" and "disgusted" with Trump's response to the "alt right" Charlottesville, Virginia rally over the weekend. Trump equated neo-Nazi and counter protestors and noted that "both sides" were to blame for the incident. Although it later revealed that Cohn would stay in the role, Trump's leadership is in doubt and his political agenda might be delaying implementation of any meaningful policies to boost growth.

Dallas Fed Kaplan "patient" on another hike

Dallas Fed President Robert Kaplan he would like to see more progress in inflation "before I consider another rate increase". And he added that "I'm being patient in terms of another rate increase". He clarified that "I don't need to see that we're going to meet that target in the near-term. I just want to see evidence, or belief, that we're going to meet that target in the medium term." Meanwhile, Kaplan also noted that yield curve is getting "flatter and inverted", and "that is a sign of economic trouble".

ECB accounts show concerns on Euro strength

At revealed in the July ECB minutes, policymakers were increasingly concerned over euro's appreciation, warning of "a possible overshooting in the repricing by financial markets, notably the foreign exchange markets, in the future". They emphasized that "the still favourable financing conditions could not be taken for granted and relied to a considerable extent on a continued high degree of monetary policy support". Indeed, the strength in the single currency might affect the central bank's plan to taper asset purchases.

The minutes indicated that the members discussed making "incremental" changes to the forward guidance. They worried that "postponing an adjustment for too long could give rise to a misalignment between the Governing Council's communication and its assessment of the state of the economy" and could "trigger more pronounced volatility in financial markets when communication eventually had to shift". President Draghi noted at the post meeting press conference that the discussion of tapering might begin in the fall.

More in ECB Warned of Euro Appreciation, Asset Purchase Reference to be Changed Soon

On the data front

German PPI and Eurozone current account are the main features in European session. Canada CPI is the main focus later in the day and U of Michigan confidence will be featured.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 140.51; (P) 141.28; (R1) 141.73; More

GBP/JPY's decline resumed by taking out 141.24 and reaches as low as 140.60 so far. Intraday bias is back on the downside. Fall from 147.76 is still in progress and would extend through 138.65 support. Nonetheless, GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. Break of 143.18 resistance is needed to indicate short term bottoming. Otherwise, outlook stays bearish in case of recovery.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. But we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | German PPI M/M Jul | 0.00% | 0.00% | ||

| 06:00 | EUR | German PPI Y/Y Jul | 2.20% | 2.40% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Jun | 30.1B | |||

| 12:30 | CAD | CPI M/M Jul | 0.00% | -0.10% | ||

| 12:30 | CAD | CPI Y/Y Jul | 1.20% | 1.00% | ||

| 12:30 | CAD | CPI Jul | 130.4 | |||

| 12:30 | CAD | CPI Core - Common Y/Y Jul | 1.40% | |||

| 12:30 | CAD | CPI Core - Trim Y/Y Jul | 1.20% | |||

| 12:30 | CAD | CPI Core - Median Y/Y Jul | 1.60% | |||

| 14:00 | USD | U. of Michigan Confidence Aug P | 94 | 93.4 |

Market Morning Briefing: The Aussie Bounced Back Sharply This Week

STOCKS

Stock indices are in a correction period and could remain weak to sideways in the near term except Shanghai which looks potentially bullish.

Dow (21750.73, -1.24%) fell sharply in line with our expectation but closed at levels below our expectation of 21800. While the index trades below 21800, it can come down to test 21670-21600 levels in the near term. Immediate trend looks bearish.

Dax (12203.46, -0.49%) is holding well above the support of 11940 and could trade sideways in the 12500-12000 region for some sessions. We prefer a rise towards 12500 in the next few sessions.

The Nikkei (19497.52, -1.04%) came down sharply to test 19450 again yesterday and in case it fails to bounce back from current levels, we could see a fresh fall towards 19250-19000 or even lower in the near to medium term.

Support near 3200 is holding good for Shanghai (3258.23, -0.31%) and while that holds, the upside potential remains open towards 3300. Overall near term looks bullish.

Nifty (9904.15, +0.07%) could come off towards 9800 again today while immediate resistance near 9960 holds. A dip towards 9800-9700 is on the cards for the medium term.

COMMODITIES

Gold (1292) is hovering around its key physiological resistance of 1300 and if this resistance breaks, a quick bounce towards 1317-25 can’t be ruled out. Otherwise it remains in a sideways move which may take it to the support of 1275 and 1259. Silver (16.95) is also moved higher and trading within the range of 16.50-17 regions. A daily close above 17.05 could open up 17.50 levels as well.

Copper (2.92) moved higher but trading within the narrow range of 2.85-98. Only above 2.98, higher resistances of 3.05 and 3.12 can come into consideration. We will remain bullish on copper while it is trading above 2.85 regions.

8th consecutive week of fall (-8.9M B) in U.S oil inventory which could be supportive for the entire energy pack. Brent (50.92) is out of its midterm bearish channel. Immediate resistance comes at 51.50 and 53 and a close above those levels could open up 56 as well. WTI (47.01) is still trading within the midterm bearish channel but there could be a decent chance of a upswing towards 50 and 52 within a few days of time. We will remain bullish on Brent and WTI, while they are trading above 49.50 and 45.50 levels on a weekly closing basis.

FOREX

The US Dollar Index (93.64) is holding well above the support of 92.54 but has come up to test immediate resistance near 94.00-94.50 which if holds could push the index again towards 92.50 in the coming sessions. In case the index breaks above 94.00 just now, we may expect a further rise towards 95.00 and higher going forward.

The Euro (1.1729) could come down to test support near 1.1650 but in case the Dollar Index comes off from immediate resistance levels, Euro could strengthen towards 1.1800-1.1850 levels again. Near term trend likely to be seen within 1.1650-1.1850 region.

Dollar-Yen (109.438) is trading above important support near 108.13 and could possibly bounce back from there. Only on a break below 108, if seen, can we look at lower levels of 106. Till then we prefer a bounce from 108 in the near term.

The Euro-Yen (128.40) is also trading above important support at 128 and while that holds, has some chance of moving up towards 129 again. On a break below 128, we may revise our targets towards 125.

Pound (1.2886) is also trading just at crucial support levels and if that holds could take the currency pair towards 1.2930 or higher in the near term. We also do not negate some chances of testing 1.2790 before a sharp bounce is seen. Overall some sideways movement is possible in the coming sessions.

The Aussie (0.7892) bounced back sharply this week from just above important support near 0.78. There is enough room on the upside towards 0.80/81 while above 0.78.

Dollar-Rupee may open slightly higher today but it remains important to see if it is able to break above 64.27. Above 64.27, the next important resistance is near 64.50 which may not be very easy to break on the upside just now. We expect a dip from levels near 64.50 or 64.27, bringing the currency pair back to levels below 64.00. Note important support near 64.10 which could hold for a few sessions keeping the currency pair ranged within 64.50-64.10 zone.

INTEREST RATES

The US yields are all trading lower and could come off in the near term. The 5Yr (1.76%), 10Yr (2.20%) and the 30Yr (2.79%) can come off towards 1.70%, 2.10% and 2.70% respectively and looks bearish just now.

The US-Japan 10Yr (2.16%) is testing medium term support near current levels and while that holds, it could possibly bounce back in the near term. A failure to bounce back just now could be another possibility which could pull down Dollar Yen and Nikkei in the near term. We need to keep a close watch as this might be an important cue.

The German-US 10Yr (-1.77%) has bounced back sharply and has got enough room on the upside towards -1.70%. While the spread rises, Euro strength could be on the cards for the medium term.

GBP/JPY On The Way Down

Price goes down aggressively erasing everything in its way as the Nikkei stock index has dropped sharply on Thursday. JP225 index failed to stay above the 19700 major static resistance and now is approaching the 19309 previous low. A further Nikkei’s drop will help the Yen to dominate the currency market. GBP/JPY should reach the warning line (WL1) in the upcoming days.

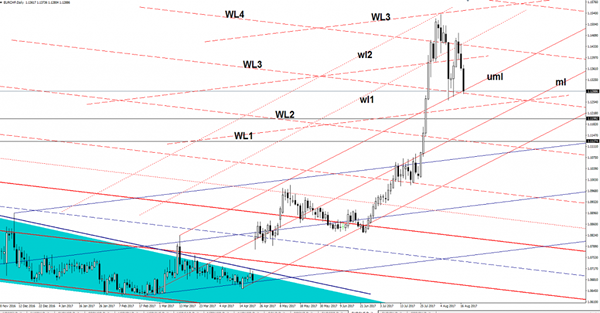

EUR/CHF Reached Critical Support

EUR/CHF plunged and extended the sell-off, but now has touched a crucial support area. A valid breakdown below the confluence between the upper median line (uml) with the WL3 will validate a further drop. Technically is expected to drop further after the failure to stay above the wl1 and above the WL4. We’ll have an important downside target at the median line (ml) of the minor ascending pitchfork.