Sample Category Title

BITCOIN All-Time High!

Bitcoin keeps on surging. The digital currency has broken hourly resistance given at 3478 (08/08/2017 high) and hourly support lies very far at 2403 (26/07/2017 low). The road is wide open for another bullish move.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

EUR/CHF Selling Pressures Are Back

EUR/CHF has consolidated and short-term selling pressures are definitely back on. Hourly support is now located at 1.1260 (04/08/2017 low). Expected to show continued weakness.

In the longer term, the technical structure has reversed. Strong resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Consolidating Below 0.9100

EUR/GBP is trading around its highest levels of the year despite ongoing consolidation. Hourly resistance lies at 0.9087 (08/08/2017 high). Hourly support is given at a distance at 0.8742 (16/06/2017 low). Downside risks are nonetheless important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

AUD/USD Growing Selling Pressures

AUD/USD's short-term technical structure is bearish. Hourly support at 0.7875 (21/07/2017 low) has been broken. Hourly resistance is given at 0.8066 (27/07/2017 high) . Expected to show continued decline.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Short-Term Bullish Momentum Continues

USD/CAD's short-term bullish momentum continues. The road is wide open for further increase. Hourly support is given at a distance at 1.2414 (27/07/2017 low). Expected to show continued increase.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low) before bouncing back. Strong resistance is given at 1.4690 (22/01/2016 high). The pair should head further lower.

USD/CHF Weakening

USD/CHF is weakening after the pair failed to monitor resistance at 0.9771 (15/06/2017 high). Hourly support at 0.9631 (01/08/2017 low) has been broken. Expected to to show further downside pressures towards 0.9500.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Ready For A Breaking Strong Support

USD/JPY's bearish momentum continues. The pair has failed to break resistance implied by the upper bound of the downtrend channel. The pair is heading towards 108.83 (17/04/2017 low). Expected to show further downside pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Monitoring Support At 1.2933

GBP/USD keeps on weakening. Hourly resistance is given at 1.3267 (03/08/2017 high). Hourly support is given at 1.2933 (20/07/2017 low). Expected to show further monitoring of support at 1.2933.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Consolidating Below 1.1800

EUR/USD bullish pressures are still on despite ongoing consolidation. Hourly resistance is given at 1.1910 (02/08/2017 high). Hourly support can be found at 1.1715 (08/08/2017 high). Stronger support lies at 1.1613 (26/07/2017 low). Expected to show renewed bullish pressures.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance holding at 1.1871 (24/08/2015 high) has been broken while strong support lies at 1.0341 (03/01/2017 low).

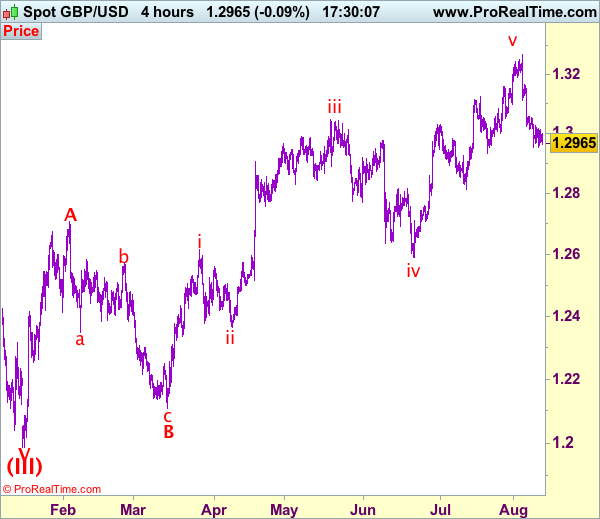

Trade Idea: GBP/USD – Sell at 1.3055

GBP/USD – 1.2962

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Sell at 1.3055, Target: 1.2860, Stop: 1.3115

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.3055, Target: 1.2860, Stop: 1.3115

Position: -

Target: -

Stop:-

As cable has remained under pressure after recent selloff from 1.3269 top, reinforcing our bearish view that the fall from 1.3269 top is still in progress and downside bias remains for this move to bring retracement of recent upmove, hence further weakness to previous support at 1.2933 would be seen, break there would extend decline to 1.2890-00 and possibly towards 1.2850-60, however, previous support at 1.2812 would hold from here, bring another rebound later.

In view of this, would not chase this fall here and would be prudent to sell cable on subsequent recovery as resistance at 1.3059 should limit upside and bring another decline. Only above previous support at 1.3112 (now resistance) would abort and signal the fall from 1.3269 has ended instead, bring a stronger rebound to indicated resistance at 1.3165 first.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.