Sample Category Title

Trade Idea : USD/JPY – Target met and stand aside

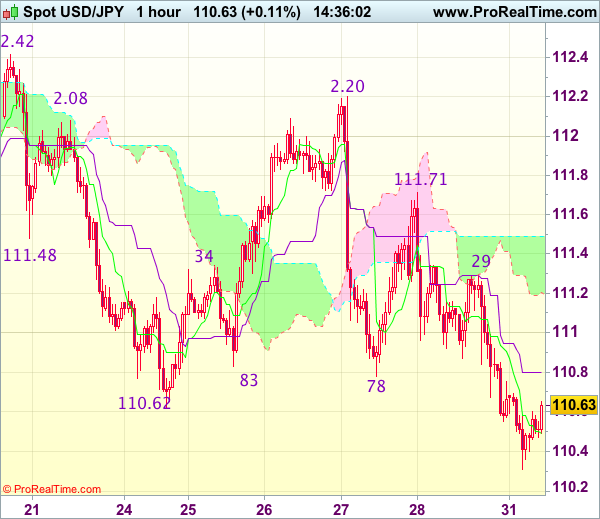

USD/JPY - 110.65

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.51

Kijun-Sen level : 110.80

Ichimoku cloud top : 111.49

Ichimoku cloud bottom : 111.21

Original strategy :

Sold at 111.45, met target at 110.45

Position : - Short at 111.45

Target : - 110.45

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback finally resumed recent decline as the pair broke below indicated previous support at 110.62, adding credence to our bearishness and our short position entered at 111.45 met target at 110.45 (with 100 points profit), however, as dollar has recovered from 110.31, suggesting minor consolidation above this level would be seen and test of the Kijun-Sen (now at 110.80) cannot be ruled out but upside should be limited to 111.00-05 and resistance at 111.29 should hold, bring another selloff.

As we have taken profit on our short position entered at 111.45, would not chase this fall here and would be prudent to stand aside for now. Below said support at 110.31 would extend recent decline to 110.00-05 but near term oversold condition should limit downside to 109.75-80 and 109.50 would hold from here, risk from there is seen for a rebound later.

The Week Ahead: Is It Time To Buy The U.S. Dollar?

Six months ago it was hard to believe that the Greenback will be plummeting against all of its major peers. Back then the Fed was the only central bank tightening monetary policy, economic data was very supportive and most importantly Trump’s expected policies of cutting taxes as well as spending on infrastructure were meant to push the dollar higher. The USD index peaked on 3 January and since then it has been moving in a downward trend, with declines exceeding 10%.

President Trump blamed himself for the dollar strength. He stated that it is the confidence in him causing the dollar to surge. Six months into his presidency has already passed without any significant legislative achievement and not even the ‘skinny repeal’ of Obamacare. Investors are apparently growing more concerned that his administration will not be able to agree on the rest of his agenda which is a clear sign that markets have lost the claimed confidence.

Although the U.S. GDP growth more than doubled in Q2 compared to Q1, the 2.6% expansion could not support the dollar as it came slightly short of expectations. The Federal reserve also acknowledged that the balance sheet normalization would begin relatively soon, and one more rate hike still on the table this year. Still the USD continued to slide as investors remained skeptical of another rate hike in 2017 with CME’s Fedwatch indicating only a 46.8% chance of a rate hike in December.

Despite my belief that the U.S. dollar will remain weak for the rest of the year, all metric shows that the USD is massively oversold and will likely receive a little bounce from current levels. Friday’s nonfarm Payrolls will be crucial for the USD and if data does not disappoint we are likely to see a bounce. However, the headline figure will not be as important as wage growth. Wage growth has been a major factor dragging inflation levels recently and accordingly a print of 0.3% or higher is required for the dollar to come back. Traders will likely position their trades before the NFP release. Thus it is important to monitor ISM manufacturing and non-manufacturing along with the ADP release.

It is also an important week for Sterling with the Bank of England meeting on Thursday. After three MPC members voted for an immediate rate hike in June, followed by Hawkish statements from Carney and Haldane, markets started pricing in a rate hike in August. However, data was not supportive enough and inflation pulled further away from the danger zone of 3% which will most likely keep the BoE on hold for now. The base scenario for the meeting is to keep rates and asset purchase unchanged but the message from Carney and the tone of the quarterly inflation report will play a major role in GBP’s next move. If more than two members voted in favor of a rate hike and Carney continued to deliver hawkish messages, we might see the pound rallying towards 1.33.

US Politics Also Remains In Focus

Market movers today

Focus today remains on euro area inflation following the country releases on Friday. These figures were stronger than expected and we now look for euro area headline and core HICP inflation to have remained unchanged at 1.3% and 1.1% in July, respectively. The inflation figures are not yet affected by the stronger euro as the impact will come after around six months.

The euro area unemployment rate for June is due out and weestimate another small 0.1pp drop to 9.2%, due to the ongoing economic recovery in Europe.

There are no major data releases in the Scandi countries today.

Selected market news

Asian equity markets are mostly in the red this morning after PMI figures released showed that growth in China's manufacturing sector slowed marginally in July (from 51.7 to 51.4), in line with our view that economic activity will cool in the second half of this year as borrowing costs rise and regulators clamp down on riskier types of lending.

North Korea conducted another test of what it said was an intercontinental ballistic missile (ICBM) on Friday, already the second missile test this month. The move was condemned by Japan and the US, which reacted by flying two military aircrafts over the Korean peninsula over the weekend and stepping up pressure on China to impose further sanctions. Tension between North Korea and the US has been rising steadily in recent months as its missile test s have grown in frequency (see Flash Comment: Further escalation of the North Korea crisis, 4 July).

Data on Friday showed that US economic activity picked up in Q2: real GDP grew by a solid 2.6% q/q annualised in Q2 after the disappointing 1.2% in Q1. Core PCE inflation was also slight ly higher than expected but st ill weak at 0.9% q/q annualised. Solid growth in the US with subdued inflation and an ongoing recovery in Europe is supporting the case of less Fed-ECB divergence in the future and EUR/USD reacted accordingly by moving back up towards 1.175 on Friday.

US politics also remains in focus, after President Trump replaced his White House Chief of Staff, Reince Priebus, after only six months in office, with General John Kelly. After the latest Republican effort to repeal Obamacare failed in the Senate on Friday, there are signs that Trump faces growing Republican unease about his ability to govern. The majority of Americans now want Congress to move on from healthcare reform, according to a Reuters/Ipsospoll. Republicans are now likely to move on to tax reform, however, and according to a white house press release, the reform will not include the controversial border tax adjustments.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD continued its bullish momentum last week topped at 1.1776. The bias is bullish in nearest term. We have an inside bar formation as you can see on my daily chart below. I am expecting a breakout above the 'mother bar' targeting 1.1875 – 1.2000 area this week. On the downside, a clear break below the 'mother bar' (1.1650) could trigger further bearish correction testing 1.1580 region which is a good place to buy with a tight stop loss as a clear break and daily close below 1.1580 would interrupt the bullish trend and activate my neutral mode.

GBPUSD

The GBPUSD had a bullish momentum last week topped at 1.3159. Price is still moving convincingly above the EMA 200 and the trend line support as you can see on my H1 chart below suggests a valid bullish trend. The bias is bullish in nearest term testing 1.3200 area before targeting 1.3350 region this week. Immediate support is seen around 1.3100. A clear break below that area could lead price to neutral zone in nearest term testing 1.3050 – 1.3000 support area which is a good place to buy with a tight stop loss below 1.3000.

USDJPY

The USDJPY attempted to push higher last week topped at 112.19 but whipsawed to the downside and closed lower at 110.72 and hit 110.30 earlier today in Asian session. The bias is bearish in nearest term testing a trend line support as you can see on my daily chart below, located around 109.50/00 region which is a good place to buy with a tight stop loss. Immediate resistance is seen around 110.80. A clear break above that area could lead price to neutral zone in nearest term testing 111.30 but only a clear break back above 112.19 could interrupt the current bearish phase. Overall I remain neutral.

USDCHF

The USDCHF had a strong bullish momentum last week topped at 0.9726. The bias is bullish in nearest term especially if price able to stay consistently above 0.9700 targeting 0.9765 – 0.9807 key resistance area which is a good place to sell with a tight stop loss. Immediate support is seen around 0.9620. A clear break below that area could lead price to neutral zone in nearest term testing 0.9550 region which need to be clearly broken to the downside to keep the bearish outlook remains strong retesting 0.9450 key support.

Market Update – Asian Session: China PMI Sees Multi-Year High

Asia Summary

Markets kick of the week mixed, over the weekend Venezuela held a vote that saw many dead, including a candidate, amid Venezuela protests during election for new legislative body that will reform constitution.US said to be considering oil-related sanctions against Venezuela, which could be announced by as early as today; not expected to include ban on Venezuelan oil shipments to the US. This saw crude futures rise as high as $50/bbl.

China July official manufacturing PMI came in at 51.4 slightly lower than expected and non-manufacturing PMI 54.5 also shy of expectations. Sub-component for construction rose to a high not seen since Dec 2013. China iron ore futures rose 7% early in the session; the strength in iron ore also pushed the major names in Australia higher.

Yen again pushed higher keeping pressure on the equities markets despite earnings season being in full swing. North Korea missile launch showed that it may be within striking range of US cities. South Korea and the US held a joint missile drill over the weekend. Elsewhere in geopolitical news Russia president Putin declared that Russia would kick out over 750 US diplomats by the end of Sept in retaliation to new sanctions.

Key economic data

(CN) CHINA JUL MANUFACTURING PMI (GOVT OFFICIAL): 51.4 V 51.5E; NON-MANUFACTURING PMI: 54.5 V 54.9 PRIOR

(NZ) NEW ZEALAND JUN BUILDING PERMITS M/M: -1.0% V 6.9% PRIOR

(JP) JAPAN JUN PRELIM INDUSTRIAL PRODUCTION M/M: 1.6% V 1.5%E; Y/Y: 4.9% V 4.8%E

(NZ) NEW ZEALAND JUL ANZ BUSINESS CONFIDENCE: 19.4 V 24.8 PRIOR; ACTIVITY OUTLOOK 40.3 V 42.8 PRIOR

(AU) AUSTRALIA JUN HIA NEW HOME SALES M/M: -6.9% V 1.1% PRIOR

Speakers and Press

China

(CN) China President Xi: China needs to speed up modernization of its military to fend off threats

(CN) China Commerce Ministry (MOFCOM): Irrational outbound investment 'effectively curbed'

(CN) China State Researcher Long Guoqiang: US trade calculation exaggerates deficit with China

(CN) MSCI warns that companies in China that suspend trading in their shares for too long risk being dropped

(CN) Moody's: Value of M&A transactions in China property sector is likely to reach a record high in 2017, following several major deals announced in July and Q2

Korea

(KR) South Korea and US conduct joint ballistic missile test (as announced earlier), in response to North Korea's ICBM test; South Korea is expected to hold talks with the US military about the temporary installation of additional Thaad launchers, according to South Korea's Defense Minister Song Young-moo

Japan

(JP) Japan PM Abe: After speaking with Pres Trump agreed more action needed on North Korea

Other

(SG) IMF raises Singapore’s 2017 GDP growth forecast to 2.3% v 2.2% seen in early May; Sees 2018 GDP growth at 2.5% - financial press

Asian Equity Indices/Futures (00:20ET)

Nikkei -0.1%, Hang Seng +0.8%, Shanghai Composite +0.6%, ASX200 +0.6%, Kospi -0.3%

Equity Futures: S&P500 -0.1%; Nasdaq -0.1%, Dax -0.1%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:20ET)

EUR 1.1762-1.1732; JPY 110.72-110.31; AUD 0.7990-0.7956; NZD 0.7523-0.7499

Aug Gold -0.1% at 1,267/oz; Sept Crude Oil +0.4% at $49.91/brl; Sept Copper +0.5% at $2.89/lb

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.7283 (strongest setting since Oct 14th, 2016) V 6.7373 PRIOR

(CN) China PBOC OMO injects CNY240B in 7-day and 14-day reverse repos v CNY140B prior in 7-day

(KR) South Korea sells 3-yr treasury bonds; avg yield 1.720%

(TH) Thailand sells THB5.0B in 3-month bills, avg yield 1.10140%

(HK) Hong Kong Overnight HIBOR rises to highest level since 2008

Equities notable movers

Hong Kong/China

Hutchison Telecom, 215.HK Agreed to sell Hutchison Telecommunications fixed-line phone business for HK$14.5B to private equity firm, I Squared Capital; +13%

Maanshan Iron & Steel,323.HK Gets approval for the listing of an investee company Anhui Xinchuang; +8.3%

Japan

Hitachi, 6501.JP Reports Q1 Net ¥75.1B v ¥34Be; Op ¥131.8B v ¥96Be; Rev ¥2.09T v ¥2.03Te; +5%

Isuzu, 7202.JP Isuzu expected to report a higher profit in June quarter, beating forecasts of a decline – Nikkei; +5%

Australia

Kogan.com, KGN.AU Entered into an agreement with The Hollard Insurance Company Pty Ltd for an initial period of three years to market a range of insurance offerings; 3 days of gains, +7.9%

Korea

Lotte Shopping, 023530.KR Reports Q2 (KRW) Net 4.16B v 82.3B y/y; -10%

Other

Sprint, S Charter affirms no interest in acquiring Sprint

CHTR Softbank's Masayoshi Son said to be planning a direct offer for Charter - financial press

Australia’s New Home Sales Dipped To A 4-Year Low Level In June

For the 24 hours to 23:00 GMT, the AUD rose 0.19% against the USD and closed at 0.7987 on Friday.

LME Copper prices declined 0.7% or $42.0/MT to $6283.0/MT. Aluminium prices declined 1.6% or $31.0/MT to $1892.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7978, with the AUD trading 0.11% lower against the USD from Friday's close.

Early morning data indicated that Australia's HIA new home sales fell 6.9% MoM in June, hitting its lowest level since 2013. New home sales had recorded a rise of 1.1% in the previous month. On the contrary, the nation's private sector credit climbed more-than-expected by 0.6% on a monthly basis in June, compared to an advance of 0.4% in the previous month.

Elsewhere, in China, Australia's largest trading partner, the NBS manufacturing PMI fell to a level of 51.4 in July, undershooting market consensus for a fall to a level of 51.5. In the prior month, the PMI had recorded a reading of 51.7. Moreover, the nation's NBS non-manufacturing PMI dropped to a level of 54.5 in July, compared to a level of 54.9 in the previous month.

The pair is expected to find support at 0.7941, and a fall through could take it to the next support level of 0.7904. The pair is expected to find its first resistance at 0.8011, and a rise through could take it to the next resistance level of 0.8044.

Looking ahead, traders will focus on the Reserve Bank of Australia's (RBA) interest rate decision slated to release tomorrow. Moreover, Australia's AiG performance of manufacturing index for July, slated to release overnight, will also pique investor attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

German Inflation Accelerated To A 3-Month High In July

For the 24 hours to 23:00 GMT, the EUR rose 0.63% against the USD and closed at 1.1757 on Friday, following upbeat German inflation figures.

Data showed that Germany's flash consumer price index (CPI) advanced more-than-expected by 1.7% on an annual basis in July, rising to its highest level in 3 months, aided by higher energy prices. Market participants had anticipated the CPI to rise 1.5%, following a gain of 1.6% in the prior month.

Separately, the Euro-zone's final consumer confidence index dropped to a level of -1.7 in July, confirming the preliminary print. In the prior month, the index had registered a reading of -1.3. Moreover, the region's business climate indicator dropped more-than-expected to a level of 1.05 in July, compared to a revised reading of 1.16 in the prior month.

On the other hand, the region's economic sentiment indicator surprisingly climbed to a level of 111.2 in July, hitting its highest level in 10 years and defying market consensus for a fall to a level of 110.8. In the previous month, the index had recorded a reading of 111.1.

The greenback lost ground against a basket of major currencies on Friday, after a report showed that the US economy grew less-than-expected in the second quarter.

The US flash annualised gross domestic product (GDP) expanded 2.6% in the second quarter of 2017, propelled by a pick-up in consumer spending, suggesting that the world's largest economy is gathering momentum. However, the reading fell slightly short of market expectations for an advance of 2.7%, compared to a revised rise of 1.2% registered in the previous quarter. Moreover, the nation's final Reuters/Michigan consumer sentiment index fell less than initially estimated to a level of 93.4 in July, compared to a reading of 95.1 in the previous month. The preliminary figures had recorded a drop to a level of 93.1.

In the Asian session, at GMT0300, the pair is trading at 1.1735, with the EUR trading 0.19% lower against the USD from Friday's close.

The pair is expected to find support at 1.1690, and a fall through could take it to the next support level of 1.1645. The pair is expected to find its first resistance at 1.1772, and a rise through could take it to the next resistance level of 1.1809.

Moving ahead, investors will keep a close watch on the Euro-zone's inflation figures for July coupled with the region's jobs report and Germany's retail sales data, both for June, all slated to release in a few hours. Additionally, the US pending home sales data for June, due to release later in the day, will keep traders on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.58% against the USD and closed at 1.3148 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.313, with the GBP trading 0.14% lower against the USD from Friday's close.

The pair is expected to find support at 1.3082, and a fall through could take it to the next support level of 1.3034. The pair is expected to find its first resistance at 1.3165, and a rise through could take it to the next resistance level of 1.3200.

Moving ahead, market participants will look forward to UK's net consumer credit and mortgage approvals data, both for June, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Switzerland’s KOF Leading Indicator Advanced More-Than-Expected In July

For the 24 hours to 23:00 GMT, the USD rose 0.45% against the CHF and closed at 0.9688 on Friday.

Macroeconomic data showed that Switzerland's KOF leading indicator climbed to a level of 106.8 in July, compared to a revised reading of 105.8 in the previous month, while markets were expecting it to rise to a level of 106.0.

In the Asian session, at GMT0300, the pair is trading at 0.9685, with the USD trading slightly lower against the CHF from Friday's close.

The pair is expected to find support at 0.9645, and a fall through could take it to the next support level of 0.9605. The pair is expected to find its first resistance at 0.9726, and a rise through could take it to the next resistance level of 0.9767.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Canadian Economic Growth Accelerated In May

For the 24 hours to 23:00 GMT, the USD declined 0.88% against the CAD and closed at 1.2440 on Friday.

The Canadian Dollar gained ground, following robust Canadian GDP figures.

Data indicated that Canada's GDP sharply expanded by 0.6% on a monthly basis in May, highlighting that the nation is on a robust growth path and boosting expectations that the Bank of Canada will raise interest rates again. The nation's GDP had risen 0.2% in the previous month, while investors had envisaged it to climb 0.2%. Also, on an annual basis, the GDP recorded a more-than-expected rise of 4.6% in May, after recording an expansion of 3.3% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2470, with the USD trading 0.24% higher against the CAD from Friday's close.

The pair is expected to find support at 1.2404, and a fall through could take it to the next support level of 1.2338. The pair is expected to find its first resistance at 1.2552, and a rise through could take it to the next resistance level of 1.2634.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.