Sample Category Title

GBP/USD Analysis: Encounters New Resistance Level

Despite the fact that a released information on the UK Retail Sales beat experts expectations, the Pound lost 0.6% in value against the American Dollar and fell below the weekly PP at 1.3008 as well as the 200-hour SMA near the 1.2968 level. For this reason, the pair is expected to spend this Friday in attempts to recover the lost ground. Nevertheless, the road upstairs most probably will be blocked by a new combined resistance level formed by a combination of the 55-hour SMA and the above weekly PP. In addition, a rebound at this point would return the pair into a short-term inner descending channel and, thus, move it closer to the bottom channel-line of the dominant ascending pattern.

EUR/USD Analysis: Trades Above 1.1650

Yesterday, as Mario Draghi spoke, the common European currency skyrocketed against the rest of the markets. After the ECB press conference the EUR/USD currency exchange rate stopped at the upper trend line of the long term descending channel patter near the 1.1560 mark. Immediately afterwards the markets were watching, will or will not the pair break out of the pattern. The result is that the pattern was broken. The breakout resulted in a 100 base point surge. Moreover, it indicates that the Euro is set to continue to score gains against other currencies in the long term. Meanwhile, it has to be noted that the next target for the pair is the combined resistance of a large scale ascending pattern and the 2015 high level near the 1.1710 mark.

Technical Outlook: Spot Gold Heads Towards Target At $1250

Spot Gold extended gains on Friday and dented barriers at $1246/47 (converged 55/10SMA's) en-route towards targets at $1250 (50% retracement of $1296/$1296 descend) and $1255 ( daily cloud base) in extension.

The yellow metal regained traction on Thursday after fresh weakness of dollar boosted gold price and left higher base at $1235 (Wed/Thu consolidation lows).

Strong bullish structure was reinforced by 10/200SMA golden cross, formed on daily chart, with gold price being on track for the second strong weekly bullish close, signaling firm bullish stance.

Strongly overbought slow stochastic on daily chart warns of rally's stall and corrective action in the near-term.

Session low at $1243 offers initial support, followed by broken Fibo 38.2% barrier at $1239, which is expected to hold and guard $1235 higher base.

Res: 1250, 1255, 1258, 1261

Sup: 1243, 1239, 1235, 1230

GBP/USD: Retail Sales

The stronger-than-expected UK retail sales report failed to support the British Pound, as the gain was thought to be related to temporary warm weather effects. At the moment of data release, the Sterling rose 0.20% against the US Dollar to 1.3018. According to forecasts, Britain’s retail sales were set to increase just 0.4% in June, but the release beat expectations with a 0.6% rise for the month. The higher volume of sales was supported by solid growth in clothing sales, which offset declines in fuel and food sales. Despite the uptick, the release is unlikely to convince the Bank of England to consider interest rate hike in the near term.

AUD/USD: Employment Change

The fourth consecutive healthy Australian employment report boosted a 30-basis point increase in the AUD/USD exchange rate, sending the Aussie to fresh 2017 highs right after the data was released. Analysts anticipated the number of employed people to increase by 14.4K in June, while the actual report showed a modest rise of 14K in the observed period, mainly supported by full-time employment, which surged by 62K. However, the unemployment rate did not manage to surprise the markets, matching with projections and drawing a rather uncertain picture with no clear trend established as of yet.

EUR/USD Strong Bullish Momentum, GBP/USD Weakening, USD/JPY Consolidating.

EUR/USD Strong bullish momentum.

EUR/USD bullish pressures continue. Hourly resistance given at 1.1584 (18/07/2017 high) has been broken. Hourly support can be found at 1.1371 (13/07/2017 high). Stronger support lies at 1.1292 (28/06/2017 low). Expected to show continued bullish pressures.

In the longer term, the momentum is clearly negative. We favour a continued bearish bias towards parity. Key resistance holding at 1.1714 (24/08/2015 high) is on target while strong support lies at 1.0341 (03/01/2017 low).

GBP/USD Weakening.

GBP/USD is bouncing lower way below the 1.3000 mark. Hourly resistance is given at 1.3126 (16/07/2017 high). Hourly support is given at 1.2933 (20/07/2017 low). Expected to show continued bearish pressures.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment

USD/JPY Consolidating.

USD/JPY still lies in a bearish momentum despite ongoing consolidation. Hourly support is given at 111.48 (19/07/2017 low). Stronger support is located at a distance at 108.13 (17/04/2017 low). Expected to show continued bearish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

ECB Appears Dovish, But Can’t Hold The Euro Down

The European Central Bank kept its policy unchanged yesterday, maintaining in its forward guidance the easing bias that QE can be expanded both in terms of size and duration if needed. In his press conference, President Draghi maintained a very dovish tone as well, indicating that policymakers were unanimous both in making no changes to their forward guidance and in not providing a timeline for changes to the QE programme.

Even though the Bank did not remove its QE easing bias, as had been widely speculated ahead of the meeting, the euro still gained significantly on Draghi's remarks. We think that may be due to Draghi's comment that financial conditions remain broadly supportive, and that although longer-term yields have risen recently, they remain low by historical standards. This implies that the Bank is not particularly worried about the recent rise in euro-area yields or the appreciation in the euro, which may have given investors a reason to add to their long-EUR positions.

EUR/USD skyrocketed after it hit the support hurdle of 1.1485 (S3) to eventually stop at 1.1660 (R1). The price structure still points to an uptrend and thus, we would expect a break above 1.1660 (R1) to open the way for our next resistance of 1.1710 (R2), defined by the peak of the 24th of August 2015.

However, given that we are already close to that key hurdle, we would be careful that a corrective setback may be on the cards soon. Looking at the weekly chart, the 1.1710 (R2) obstacle appears to be the upper bound of the long-term sideways range that has been containing the price action since January 2015. As such, we prefer to wait for a decisive close above that zone before we get confident on larger upside extensions.

As for the big picture, besides pushing back the timing of an announcement on QE changes, not much has changed in our view. Draghi pointed out that a discussion on tweaks to QE should take place in the autumn, suggesting we are likely to get some signals on stimulus changes either in September or October.

Although a lot will depend on incoming data, we think that a likely scenario is that the Bank removes its QE easing bias at the September meeting, thereby laying the groundwork for a formal announcement in October that the pace of QE purchases may be reduced by the turn of the year. Draghi's speech at the Jackson Hole towards the end of August could provide clearer signals as to whether the Bank is setting up for something like that. Speculation about a QE-reduction announcement by October could keep the euro supported, but as we already noted we would wait for a clear move above 1.1710 (R2) in EUR/USD before we assume the continuation of the existing uptrend.

Aussie slides as RBA's Debelle pours cold water on rate-hike talk

Overnight, RBA Deputy Governor Guy Debelle said no significance should be read into the RBA's discussion in the June meeting minutes about the neutral rate of interest, and that Australian rates don't have to rise simultaneously with other major central banks. He added that an appreciating AUD reduces the benefits of faster global growth for Australia. The Aussie slid on his comments, as they may have scaled back rate-hike expectations, and also signalled that the Bank is uncomfortable with the levels AUD is currently trading at. Even though the outlook for AUD remains positive amid strong economic data, we have to highlight the risk that further dovish signals from the RBA aimed at bring Australian yields back down could cause AUD to give back more of its latest gains.

AUD/USD slipped during the Asian morning Friday, falling below the support (now turned into resistance) line of 0.7900 (R1). The rate continues to trade above the key obstacle of 0.7800 (S2), which acted as the upper bound of the long-term sideways range that contained the price action from March 2016 until the 14th of July 2017. Thus, we still consider the outlook to be positive. Nevertheless, we see signs that the overnight slide may continue for a while, perhaps to challenge the key territory of 0.7800 (S2) as a support this time. Our short-term oscillators support the case. The RSI edged south after it exited its above-70 territory and is now testing its 50 line, while the MACD, although positive, lies below its trigger line, pointing down.

Today's highlights:

We only get economic data from Canada. The nation's CPIs for June are due out and expectations are for the headline CPI rate to have declined, while no forecast is available for the core print. Even though a potential slowdown in the CPI could hurt CAD on the news, we doubt that it will deter the BoC from hiking rates again this year, as the Bank already expects inflation to slow further in Q3, before picking up again. We also get the nation's retail sales for May and expectations are for a slowdown.

EUR/USD

Support: 1.1615 (S1), 1.1585 (S2), 1.1485 (S3)

Resistance: 1.1660 (R1), 1.1710 (R2), 1.1785 (R3)

AUD/USD

Support: 0.7840 (S1), 0.7800 (S2), 0.7740 (S3)

Resistance: 0.7900 (R1), 0.8000 (R2), 0.8070 (R3)

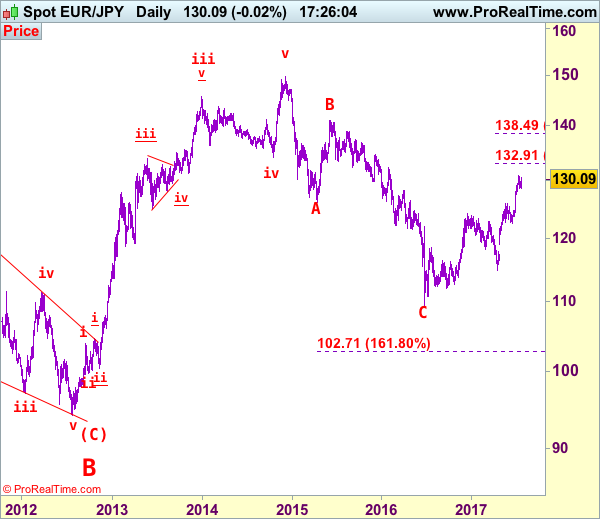

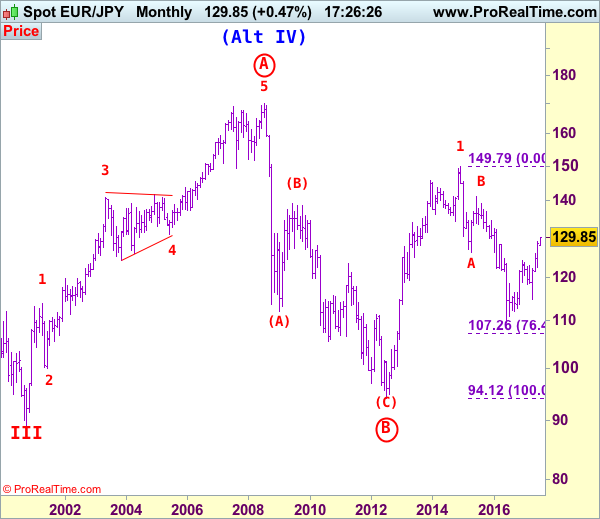

EUR/JPY Elliott Wave Analysis

EUR/JPY - 129.99

EUR/JPY: Wave v as well as larger degree wave (C) ended at 94.11 and first leg of larger degree wave C upmove has possibly ended at 149.79 and wave 2 correction has possibly ended at 109.49.

Although the single currency met resistance at 130.77 last week and has traded narrowly since, reckon downside would be limited to 128.50-60 and renewed buying interest should emerge around 127.50-60, bring another rise later, above said resistance at 130.77 would extend recent upmove to 131.00, however, near term overbought condition should prevent sharp move beyond 132.00 and price should falter below 132.90-00 (1.236 times projection of 109.49-124.10 measuring from 114.85), risk from there has increased for a retreat to take place later.

The daily chart is labeled as attached, early selloff from 169.97 (July 2008) to 112.08 is wave (A) of B instead of end of entire wave B and then the rebound from there to 139.26 is wave (B), hence, wave (C) has possibly ended at 94.12 with a diagonal triangle as labeled in the daily chart, hence upside bias is seen for further gain. Recent rally above indicated retracement level at 116.69 (50% Fibonacci retracement of the intermediate fall from 139.26-94.12) adds credence to this view and signal major reversal has commenced but first leg of this wave C has possibly ended at 149.79, hence wave 2 has commenced with wave A ended at 126.09, followed by wave B at 141.06, wave C commenced and could have ended at 109.49, above 126.00 would add credence to this view, then headway to 130.00 would follow.

On the downside, although initial pullback to 129.00-10 and 128.00 cannot be ruled out, reckon 127.40-45 would limit downside and bring another rise to aforesaid upside targets. Only a drop below support at 126.49 would suggest top is possibly formed, bring test of previous resistance at 125.82 (now support), a sustained breach below this level would add credence to this view, bring correction to 125.15-20 but previous resistance at 124.65 would hold, bring another upmove later. In the unlikely event, euro drops below 124.65 on a daily basis, this would signal a temporary top is formed instead, then further fall to 124.00 and later towards support at 123.66 would follow.

Recommendation: Buy at 127.50 for 130.50 with stop below 126.50.

To re-cap the corrective upmove from the record low of 88.93 (18 Oct 2000), the wave A from there is subdivided as: 1:88.93-113.72, 2:99.88 (1 Jun 2001), 3:140.91 (30 May 2003), 4:124.17 (10 Nov 2003) and 5 ended at record high of 169.97 (21 Jul 2008). The brief but sharp selloff to 112.08 is viewed as a-b-c x a-b-c wave (A) of B. The subsequent rebound to 139.26 is (B) of B and (C) of (B) has possibly ended at 94.12 and in any case price should stay well above previous chart support at 88.93, bring rally in larger degree wave C towards 150.00.

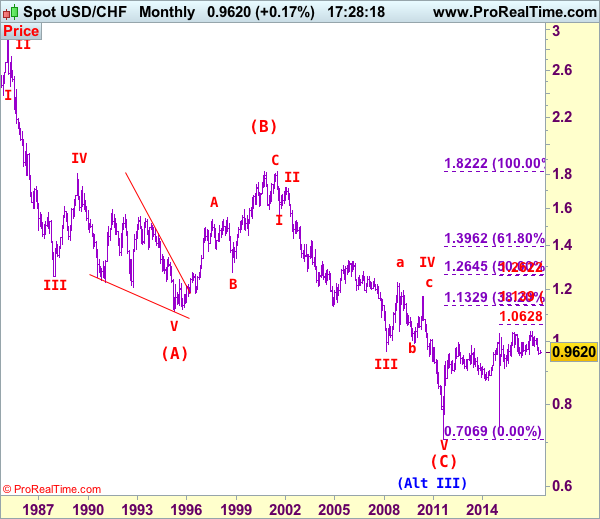

USD/CHF Elliott Wave Analysis

USD/CHF – 0.9505

USD/CHF – Wave IV ended at 1.1730 and wave V has possibly ended at 0.7068

The greenback only recovered to 0.9701 before meeting renewed selling interest and has fallen again, adding credence to our bearish view that the erratic decline from 1.0344 top (formed back in late 2016) is still in progress and downside bias remains for this move to extend weakness to 0.9444 support (2016 low), however, break there is needed to bring further subsequent fall to 0.9390-00, however, loss of downward momentum should prevent sharp fall below 0.9300-10, risk from there has increased for a rebound to take place probably next month.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the upside, whilst initial recovery to 0.9550-55 is likely, reckon resistance at 0.9622 (yesterday’s high) would cap upside and bring another decline. A daily close above this level would defer and bring a stronger rebound towards said resistance at 0.9701 but break there is needed to signal a temporary low is possibly formed instead, bring retracement of recent decline to resistance levels at 0.9771 and then 0.9808 which is likely to hold from here.

Recommendation: Stand aside for this week

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.

ECB: The Currency War Is On, Buy High Beta EM Despite Pullback

European Central Bank tries to restrain the EUR/USD, but it won’t work

Unsurprisingly the European central bank has held its rates steady yesterday at 0% for 17th consecutive month. The ECB meeting took place against a backdrop of strengthening of the single currency. The EURUSD pair has reached 1.16 for the first time in two years.

ECB President Mario Draghi appeared dovish, certainly in an effort to calm down financial markets and the euro appreciation. Markets did not buy it and they still believe that further tightening are on the roadmap and this sentiment is largely boosting the Eurodollar.

While he mentioned in June that the ECB monetary policy would follow the Eurozone recovery, which had already been interpreted as hawkish by markets at the time, he appeared yesterday concerned about the Eurozone inflation path. He mentioned that the current QE could be increased. In other words, a larger volume of bonds could be purchased and with larger duration.

In our view, this is unlikely. We believe that the bonds scarcity in the markets would prevent such a possibility and Draghi’s verbal intervention was more of an attempt to devalue the euro. At next September meeting will be discussed the bonds purchase and it is clear that the program will be held unchanged until its term in December just because the ECB cannot increase it. The single currency is definitely on its way up.

Buy high-beta emerging-market currencies such as Indonesian rupiah

As was widely expected the Bank of Indonesia held its key 7day repo rate at 4.75%. Yet the overall effect and tone was slightly dovish. The decision was based on the central banks effort to keep a balanced approach between supporting recovering economic growth and maintaining financial vigilance. On the growth front BI indicated that the economic recovery would decelerated but continue at a decent pace on the back of solid export expansion.

BI forecast anticipated GDP growth at 5.0% to 5.4% in 2017. Despite the stable growth and holiday season inflation remained subdued well within the 4% 2017 target area. In regards to the IDR, the banks was not concerned over recent appreciation as the price movement was due to stable capital inflows. We anticipate policy strategy will remain unchanged with a bias towards easing to support slowing growth for the remainder of 2017. BI decision to not begin slashing rates and overall risk supportive environment should further support our view to be long carry, specifically IDR.

Expectations for a Fed December 25bp rate hike continue to decrease (helped by Yellen’s dovish comments) while the ability for the Trump administration to pass anything of value is in significant doubt. In addition ECBs Draghi was unable to convince the markets that his next more would not be towards normalization which resulted in massive USD selling.

Thin summer trading volume often distorts the meaning of normal market moves, such as the case with the risk of trading today. Yet this would be an opportunity to reload longs on high beta and interest rate EMs for conditions are prime for further upside momentum.