Sample Category Title

Trade Idea : USD/JPY – Stand aside

USD/JPY - 111.81

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.90

Kijun-Sen level : 111.95

Ichimoku cloud top : 111.97

Ichimoku cloud bottom : 111.94

Original strategy :

Exit long entered at 111.80,

Position : - Long at 111.80

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback fell marginally to 111.48, lack of follow through selling and the subsequent bounce suggest consolidation would be seen and above 112.05-10 would bring another corrective rebound towards resistance at 112.42 but break there is needed to signal a temporary low is possibly formed, bring retracement of recent decline to 112.70 and then test of resistance at 112.87.

In view of this, would be prudent to stand aside for now. Below said support at 111.48 would signal recent decline from 114.50 top has resumed and extend further weakness to 111.20-25, however, reckon 111.00 would hold from here due to near term oversold condition, bring rebound later.

Daily Technical Analysis: EUR/USD Continues Bullish Trend After Bouncing At 1.15

Currency pair EUR/USD

The EUR/USD continued the uptrend yesterday after bouncing in the 1.15 support zone. Price reached the 161.8% Fibonacci target at 1.1650 and could continue to higher Fib targets when considering the strength of yesterday's daily candle close near the high.

The EUR/USD showed strong bullish momentum after breaking above the resistance trend line (dotted red). The EUR/USD completed a wave 4 (grey) correction as expected in yesterday's analysis and is continuing with wave 3 (orange). Currently price is building a small triangle. A bullish break could see an extension towards the Fibonacci targets whereas a break below support could price retest 1.1575-1.16.

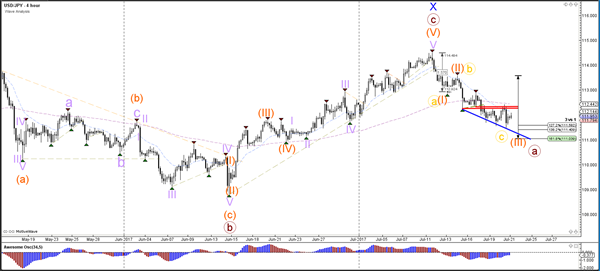

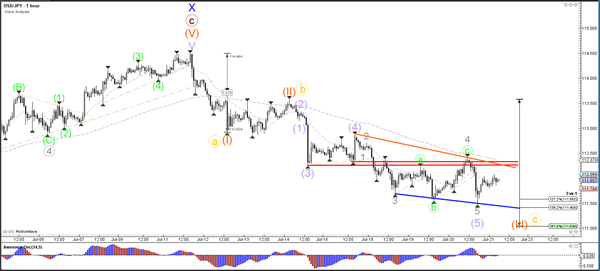

Currency pair USD/JPY

The USD/JPY did not manage to break above the horizontal resistance levels (red) and continued with the downtrend. Price will need to break below the support trend line (blue) to confirm a wave 3 (orange) otherwise a wave C (yellow) could be the alternative.

The USD/JPY will need to break below support (blue) or above resistance (red) before a wave 123 or ABC becomes more likely.

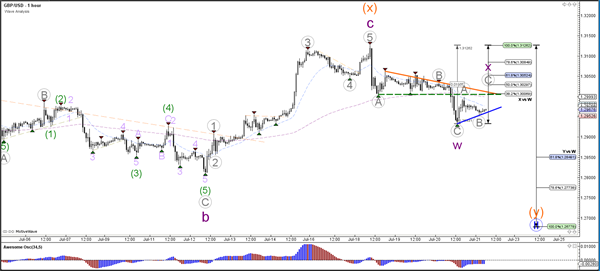

Currency pair GBP/USD

The GBP/USD broke below the support trend line (dotted green) and round level of 1.30 which makes a bullish impulse less likely. Price is therefore most likely extending its correction towards the Fibonacci targets of wave Y (orange).

The GBP/USD seems to have completed a wave B (grey) triangle and an ABC (grey) within wave W (purple). The GBP/USD could potentially complete a new ABC (grey) within wave X (purple), which means that the Fib levels of wave X vs W could act as resistance.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, USD/JPY, AUD/USD, NZD/USD, USD/CAD, XAU/USD, WTI

EUR/USD

The Euro broke above 1.1585 resistance yesterday and extended gains to 1.1650. The pair is overbought in the short-term, but demand is likely to remain high on any dips and it should recover quickly.

Look for initial support at 1.1585, followed by stronger support at 1.1540. In the near-term, losses are likely to be limited to 1.1490/1.15. Following the clear breakout above 1.16, the next significant resistance level lies at 1.1714 (summer 2015 high).

GBP/USD

The break below 1.30 confirms the recent high at 1.3120. Cable is now approaching major support at 1.2930 and is near the rising trendline support from the late June low.

Should 1.2930 fail to hold, a larger retracement seems likely, with the next notable support level then lying at 1.2820.

USD/JPY

The break below 1.30 confirms the recent high at 1.3120. Cable is now approaching major support at 1.2930 and is near the rising trendline support from the late June low.

Should 1.2930 fail to hold, a larger retracement seems likely, with the next notable support level then lying at 1.2820.

AUD/USD

The Aussie Dollar failed at 0.80, but remains resilient. Initial support is seen around 0.79. AUD/USD has stronger support at 0.7840 should that level fail. A bounce off 0.7840 would confirm that the short-term uptrend remains intact and pave the way for a rally towards 0.80.

NZD/USD

NZD/USD broke above a significant area of resistance between 0.7380 and 0.7410. However, the Stochastic is showing heavily overbought conditions on the hourlies, as well as Daily & Weekly chart. Therefore, the New Zealand Dollar is unlikely to keep up the momentum it had so far.

Strong resistance is noted at 0.7490 and 0.75. However, NZD/USD will likely need a retracement before the uptrend continues. Key support is now seen at 0.7340/50.

USD/CAD

The Canadian Dollar continues to struggle. Trendline resistance on the hourlies have capped the topside so far, and heavy resistance is noted in the area between 1.2630 and 1.2660. CAD traders can expect to see a bounce around the 1.25 level, but a larger rally seems unlikely in the near-term.

XAU/USD

Gold is approaching an important area of resistance between $1250 and $1255. Should it be able to overcome that obstacle, a rally back towards $1300 seems likely.

A daily close above $1255 would be a strong confirmation of the short-term uptrend. The recent bounce off $1232 shows that momentum is solid, and Gold should continue to benefit from the USD weakness as well.

WTI

Oil briefly broke above $47.30 resistance, but failed to close the trading day above it. This shows that WTI still has not enough momentum to clear that major resistance level. A break back below $46.15 would signal a correction to $45.

To the topside, should WTI be able to close the day above $47.30, momentum is likely to increase and a rally towards the falling trendline resistance could follow.

European Open Briefing: The Aussie Dollar Failed To Break Above 0.80

Global Markets:

- Asian stock markets: Nikkei down 0.25 %, Shanghai Composite lost 0.20 %, Hang Seng declined 0.05 %, ASX 200 dropped 0.60 %

- Commodities: Gold at $1243 (-0.15 %), Silver at $16.30 (-0.30 %), WTI Oil at $46.90 (-0.05 %), Brent Oil at $49.25 (-0.15 %)

- Rates: US 10 year yield at 2.26, UK 10 year yield at 1.20, German 10 year yield at 0.54

News & Data:

- Euro at two-year high, Asian shares barely budge – RTRS

- Dollar near two-year lows vs euro after Draghi comments – RTRS

- PBOC sets USD/CNY mid-point today at 6.7415 (vs. yesterday at 6.7464)

Markets Update:

The Euro rallied after the market saw Draghi’s comments during the ECB press conference as hawkish. While he tried to maintain a neutral tone, the market interpreted his positive outlook for the economy as a sign that the ECB will soon its QE programme and signal a shift of its monetary policy. EUR/USD rallied from 1.1490 to a high of 1.1650. In Asia, it retraced some of those gains, but remained well bid overall. Support is now seen at 1.16, followed by 1.1550. EUR/JPY rallied back above 130. In the near-term, a test of 132 resistance seems likely.

The Pound fell back below 1.30 yesterday, and the outlook is rather weak amid the recent decline in inflation and the Brexit uncertainty. Meanwhile, USD/JPY had a solid performance in the past 48 hours, despite broad USD weakness. It bounced once again off 111.50 support and is currently consolidating around 112. A break above 112.50 resistance would then signal a move towards 113.60.

The Aussie Dollar failed to break above 0.80. However, the positive risk sentiment and rising commodity prices should keep the currency supported in the near-term. Intraday, expect good support at 0.79 and 0.7830.

Upcoming Events:

- 13:30 BST – Canadian Retail Sales

- 13:30 BST – Canadian CPI

Is The Euro Headed Sharply Higher?

Key Points:

- ECB's Draghi takes a hawkish tone in his latest commentary.

- Highlights low inflation but suggests the economy is growing strongly.

- Potential for a QE taper in September ECB meeting.

The Euro Dollar has been on a significant bullish run over the past 24 hours as ECB Chair Mario Draghi stoked the fires of speculation with his latest commentary on the state of the Eurozone economy. Although there was plenty of mixed information for the average trader to digest, the unmistakable message was one of positivity which sent the Euro soaring.

So let's start with the one negative factor within Draghi's monetary policy statement, inflation. There is no doubt that persistent inflation has largely been absent from the Eurozone over the past decade. However, this is no different from most of the other Western nations and, in fact, EU inflation isn't actually looking that bad with the latest statistics showing inflation running at around 1.3%. Subsequently, there is no doubt that inflation could potentially improve and this is effectively what the ECB Chair suggested when he stated that he expects it to pick up over the medium term.

In addition, unemployment and consumer sentiment is also strongly improving with the former having dipped to 9.3% recently. In fact, if you exclude the PIGS from the figures, the unemployment rate actually looks relatively good for the broader Eurozone. Also, wage growth is proving relatively supportive of consumer spending with wages have risen by over 1.4% q/q. Retail Spending and consumer confidence are subsequently also starting to pick up and the flow on effects are interesting indeed.

Subsequently, there has been plenty of upward momentum in the Euro Dollar and the currency pair has managed to smash through the 1.16 handle and currently trades around the 1.1628 mark. Infact, this marks the strongest level in over 23 months for the pair and could be a precursor of things to come.

However, much of the forward guidance provided by the ECB hinted at strongly building domestic pressures within the economy. Subsequently, the ECB might have actually teased the bulls somewhat with suggestions that they may look to “tweak” their QE levels in their September meeting. Considering the range of improving economic conditions, any tweaking would surely have to be a reduction or removal of some QE and asset purchases. Any move along these lines would prove to be a highly bullish one for the Euro Dollar.

Ultimately, we will all have to wait and see what September's ECB meeting brings with it. However, the risks are all skewed to the upside and we are likely to see building bullish pressure in the EURUSD as we move towards the critical meeting. In fact, right now 1.1714 looks relatively achievable, as does the 1.18 handle. Subsequently, it is entirely conceivable that we might yet see the venerable Euro Dollar trading above 1.20 if the ECB continues to follow through and doesn't seek to jawbone the market.

USDCHF Ready To Rebound

Key Points:

- The current downtrend is unlikely to remain in place.

- Support is technically robust.

- A reversal could reach as high as the 0.9659 handle.

The Swissy has moved to test a critical technical support level over the past 24 hours and this could result in a reversal for the pair in the immediate future. Overall, it is unlikely that any such reversal breaks free from the bearish channel that has been constraining the pair since May. Nevertheless, it could at least carry the USDCHF back to the upside of the structure – not an immaterial gain for the embattled pair.

As shown below, the Swissy has been under pressure over the past few sessions which has, quite understandably, gotten the bears excited. Indeed, given the pace of recent losses, it looks as though momentum has shifted and that they are finally going to break through the long-term trendline – potentially sending the USDCHF reeling. However, upon closer inspection, numerous technicals are suggesting that the latest attempt to breakout to the downside is going to be yet another failure.

For one thing, the latest downtrend is nowhere near as strong as it at first appears. Whilst not shown, the ADX reading is sitting somewhere around the 16.00 level – effectively signalling that the bearish push is not particularly voracious. This is important to note as the support that the bears are hoping to overcome is actually rather robust and probably unlikely to buckle unless significant selling pressure can be mustered.

Indeed, breaking through support requires breaching not only the long-term trendline but also the downside of the more recent channel. On their lonesome, these hurdles could potentially be overcome but, much to the disappointment of the bears, there are two other key factors standing between them and their much desired push below the 0.9503 handle.

Firstly, the stochastics can’t be ignored as they are convincingly in oversold territory which would typically suggest further losses are going to be limited, if not non-existent. Secondly, the pair is now resting directly on top of the lower Bollinger band which only adds to the already impressive degree of support around the 0.9503 level. However, these two indicators also indicate something else. Specifically, they suggest a correction to the upside is warranted.

Ultimately, any rally that is seen is likely to terminate around the 0.9659 handle as the pair comes into conflict with the upside of the channel. Nevertheless, this is still a rally of around 140 pips which isn’t an immaterial amount. However, do remember to keep an eye on the fundamental side of things as this could slow or even prevent any near-term bullishness for the USDCHF if the US data continues to disappoint.

EURUSD Is Currently Trading At 1.1630

Market Movers Today

The ECB's Survey of Professional forecasters is due for release today where focus will be on the longer-term inflation expectations. The survey-based inflation expectations have been fairly stable at 1.8% but the distribution has shifted to more forecasters expecting inflation to stay below 2% in five years. Some dovish ECB members have argued the distribution of inflation expectations still needs to shift but recently the ECB has been more focused on the stronger economic recovery. See ECB Review, 20 July 2017.

As the Bank of Canada has embarked on a tightening cycle recently with the rates market pricing in another hike by year-end, financial markets will take stock of the Canadian CPI and retail sales data due for release today, to see whether data supports tighter monetary policy in Canada.

The oil market will focus on the release of the weekly US oil rig count and looks for more signs of negative supply response among US producers to low oil prices. Furthermore, the oil market will watch out for headlines from OPEC as the cartel is set to review compliance to current output cuts over the weekend in addition to starting talks with Libya and Nigeria over whether to include the two nations in the deal.

Finally, US politics has gained attention this week and the market will look to see if further progress is made in the attempt to repeal Obamacare and also for news on the ongoing investigation of President Trump.

Selected Market News

The ECB kept all policy measures unchanged and maintained its readiness to increase the size and/or duration of QE purchases. According to President Mario Draghi, the Governing Council was unanimous in setting no precise date on when to discuss changes to the QE programme but argued that, 'our discussion should take place in the autumn '. Additionally, Draghi said the ECB has not tasked its staff with looking at QE options beyond December 2017. The above suggests the ECB is not ready to make an announcement at the September meeting on how QE purchases will continue in 2017. We maintain our view that the ECB will continue its QE purchases but at a reduced pace of EUR40bn per month in H1 18, but now believe this will be announced at the October meeting (previously September).

EUR/USD rose on the back of the ECB meeting as Draghi did not provide the market with a reason to sell the single currency. EUR/USD is currently trading at 1.1630, so is not only hitting the 1.16 level, on news about the ongoing investigation on President Trump, which will now also include his business transactions.

The South African central bank cut its key policy rate to 6.75% from 7.00% yesterday. This was a surprise cut as consensus had expected the central bank to keep the rate unchanged. USD/ZAR rallied above the 13.00 level on the decision.

Market Update – Asian Session: Antipodean Currencies Dominate Action In Asia

Asia Summary

Following the flattish session in the US, most of the equity markets in Asia are slightly weaker. Australia’s ASX 200 has somewhat underperformed amid some weakness in BHP, Woodside Petroleum and the banking sector.

Key economic data

(NZ) New Zealand June Credit Card Spending M/M: 0.2% v 0.9% prior; Y/Y: 8.3% v 7.6% prior

(NZ) NEW ZEALAND JUNE NET MIGRATION SA: 6.4K V 5.9K PRIOR

(JP) JAPAN FOREIGN BOND BUYING: 947.8 ¥ V ¥839.5B PRIOR; STOCK BUYING ¥438.6B V ¥324.9B PRIOR - WEEK ENDED JULY 14TH; Foreign Buying of Japan Bonds ¥413.7B v -¥408.5B prior; Foreign Buying of Japan Stocks ¥341B v -¥35.0Be prior

(KR) South Korea July Exports 20 Days Y/Y: 22.4% v 24.4% prior; Imports: 13.3% v 20.7% y/y

Speakers and Press

Australia

(AU) RBA ASSIST GOV DEBELLE: NO SIGNIFICANCE IN BOARD DISCUSSING NEUTRAL RATE; Higher Aussie works against benefits of faster global growth

China

(CN) China said to ask state owned enterprises (SOE)s to avoid blind financial investments - Chinese Press; Also, asks SOEs to strengthen financial risk management.

Japan

(JP) Japan Fin Min Aso: Reiterates no change to goal of reaching primary balance surplus; Want to continue trend of issuing fewer govt bonds; Discussion to 'pick up' on consumption tax.

(JP) Japan Foreign Minister Kishida: UK Foreign Sec Boris Johnson promised to minimize Brexit impact on corporate activity

Other

(GR) IMF confirms approval of $1.8B conditional loan for Greece (as expected)

(KR) South Korea urges North Korea to respond to military talks offer which is valid until July 27th - Korean press

(NZ) New Zealand Fin Min Joyce: 'Unperturbed' by NZD strength, kiwi dollar strength reflects strong economy; Domestic firms dealing 'well' with Kiwi at current levels.

(PH) Philippines Central Bank (BSP) Deputy Gov Guinigundo: Very little reason to start mulling raising rates

(TW) Taiwan President's Office denies report that Premier to resign

(US) US President Trump said to ask lawyers about pardoning abilities in relation to Russia probe – US press

(US) President Trump said to have made changes to legal team – CNN; Trump’s longtime personal attorney Marc Kasowitz said to be taking a lesser role with regards to the US special counsel Mueller’s probe into Russia.

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.3%, Hang Seng -0.2%, Shanghai Composite -0.2%, ASX200 -0.2%, Kospi +0.3%

Equity Futures: S&P500 flat ; Nasdaq -0.2% , Dax flat, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1637-1.1620; JPY 112.08-111.81; AUD 0.7960-0.7876; NZD 0.7429-0.7394

Aug Gold -0.1% at 1,244 /oz; Aug Crude Oil flat at $46.91/brl; Sept Copper flat at $2.72/lb

GLD SPDR Gold Trust ETF daily holdings unchanged at 816 tonnes

(AU) Australia sells A$500M in 2.0% Dec 2021 bonds, avg yield 2.1996% v 2.1693 prior, bid to cover 6.58x v 5.46x prior

(CN) China PBOC OMO injects CNY140B in 7 and 14 day reverse repos v CNY60B prior

(CN) PBOC SETS YUAN REFERENCE RATE AT V 6.7415 V 6.7464 PRIOR

(CN) China MOF sells 30-year bonds at avg yield 4.05%, bid to cover 1.7x

Australia 3-year bond yield declines over 8bps as RBA’s Debelle plays down Neutral Rate comment in recent RBA minutes

Equities notable movers

Hong Kong/China

BYD, 1211.HK H1 Guidance; +1.5%

CK Instructure, 1038.HK H1 net earnings and raised dividend; +4.5%

Japan

Yaskawa Electric, 6506.JP Q1 earnings speculation; +10%

Nikon, 7731.JP Positive broker commentary; +2%

US markets on close: Dow -0.1%, S&P500 flat, Nasdaq +0.1%, Russell flat

Best Sector in S&P500: Utilities +0.7%

Worst Sector in S&P500: Materials -0.7%\

At the close: VIX 9.58 (-0.21 pts); Treasuries: 2-yr 1.356% (flat), 10-yr 2.266% (-0.2%), 30-yr 2.831% (-0.7%)

US Market Summary

Stock markets were quiet today, with mixed sentiment showing little volatility in price, although the Nasdaq still managed to post a new all-time high. The Transports underperformed notably for the second straight session as traders appear to be ready to take profits in those names. Stocks dropped on the initial news that Special Counsel Mueller is investigating President Trump's financial dealings, but pared its losses within a half-hour. The VIX index continued to decline, falling by 2% to 9.60.

US Afterhours Movers

ATHN Reports Q2 $0.51 v $0.40e, Rev $301.1M v $298Me; Affirms FY17 Rev $1.21-1.25B v $1.24Be (prior $1.21-1.25B) ; +9.8% afterhours

COF Reports Q2 $1.94 v $1.90e, Rev $6.70B v $6.7Be; +4.6% afterhours

MSFT Reports Q4 $0.98 v $0.71e, Rev $24.7B v $24.2Be; Productivity and Business Processes Rev $8.4B, +21% y/y, +23% constant FX ; +1.9% afterhours

V Reports Q3 $0.86 v $0.80e, Rev $4.57B v $4.36B; Affirms FY17 op margin mid 60's% (prior mid 60's%) ; +1% afterhours

SKX Reports Q2 $0.38 v $0.44e, Rev $1.03B v $966Me

Guides Q3 $0.42-0.47 v $0.56e, Rev $1.05-1.08B v $1.06Be; -1.5% afterhours

EBAY Reports Q2 $0.45 v $0.45e, Rev $2.33B v $2.31Be; approves $3B buyback (7% of market cap)- Guides Q3 $0.46-0.48 v $0.48e; R$2.35-2.39B v $2.32Be ; -2.6% afterhours

MXIM Reports Q4 $0.63 v $0.62e, Rev $602M v $608Me; Raises quarterly dividend by 9.1% to $0.36/shr (indicated yield 3.01%)- Guides Q1 $0.52-0.58 v $0.58e, R$555-595M v $596Me, adj gross margin 65-68%; -5.5% afterhours\

NCR Reports Q2 $0.80 v $0.75e, Rev $1.59B v $1.61Be; Guides Q3 $0.88-0.93 v $0.93e, R$1.66-1.70B v $1.73Be ; -7.2% afterhours

MANH Reports Q2 $0.50 v $0.48e, Rev $154.1M v $154Me; Cuts FY17 $1.85-1.89 v $1.90e, R$590-600M v $611Me (prior $1.89-1.93, R$606-620M); -8.3% afterhours

Earnings from GE expected in the New York morning.

Aussie Dollar Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.09% against the USD and closed at 0.7951.

LME Copper prices declined 0.4% or $26.0/MT to $5930.0/MT. Aluminium prices declined 0.5% or $9.0/MT to $1898.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7881, with the AUD trading 0.88% lower against the USD from yesterday's close.

The pair is expected to find support at 0.7848, and a fall through could take it to the next support level of 0.7814. The pair is expected to find its first resistance at 0.7942, and a rise through could take it to the next resistance level of 0.8002.

Next week, traders will keep a close watch on a speech by the Reserve Bank of Australia's Governor, Philip Lowe accompanied with Australia's consumer price index data.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

ECB Leaves Policy On Hold, Stays ‘Patient’ On Stimulus Exit

For the 24 hours to 23:00 GMT, the EUR rose 0.86% against the USD and closed at 1.1628, after the European Central Bank (ECB) President, Mario Draghi, hinted that tapering of its ultra-loose monetary policy is on the table this autumn and painted a positive outlook of the common currency region.

The ECB, at its latest monetary policy meeting, unanimously voted to hold interest rates at 0.00% and pledged to continue the asset purchase plan through December or beyond, if financial conditions become inconsistent in future. In a post-meeting statement, the ECB Chief, Mario Draghi, stated that governing council agreed in setting no precise date for a discussion about potential changes to the central bank's quantitative easing programme, but noted that it would occur in the autumn. Draghi further added that underlying inflation is likely to rise in the coming months, albeit gradually.

In other economic news, the Euro-zone's flash consumer confidence index unexpectedly fell to a level of -1.7 in July, while market participants expected it to advance to a level of -1.2. The index had registered a reading of -1.3 in the previous month. Meanwhile, the region's seasonally adjusted current account surplus widened to a level of €30.1 billion in May, following a revised current account surplus of €23.5 billion in the prior month.

Separately, in Germany, the producer price index remained flat on a monthly basis in June, after recording a drop of 0.2% in the prior month.

The greenback traded mixed against a basket of major currencies, amid reports that Special Counsel, Robert Mueller, who is investigating possible ties between the Trump campaign and Russia, was looking into business transactions involving the US President, Donald Trump.

On the macro front, initial jobless claims in the US dropped to a nearly five-month low level of 233.0K in the week ended 15 July, boosting optimism over the health of the nation's labour market. In the prior week, initial jobless claims had registered a revised reading of 248.0K, while and markets anticipated for a fall to a level of 245.0K. Further, the nation's leading indicators advanced more-than-expected by 0.6% in June, following a gain of 0.3% in the prior month.

On the contrary, the nation's Philadelphia Fed manufacturing index declined more-than-anticipated to a level of 19.5 in July, hitting its lowest level since November 2016. In the prior month, the index had recorded a reading of 27.6, compared to market consensus for a drop to a level of 23.0.

In the Asian session, at GMT0300, the pair is trading at 1.1626, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.1517, and a fall through could take it to the next support level of 1.1409. The pair is expected to find its first resistance at 1.1696, and a rise through could take it to the next resistance level of 1.1767.

With no major economic releases in the Euro-zone today, investors will focus on the flash Markit manufacturing and services PMIs for July, across the Euro-zone coupled with Germany's preliminary inflation numbers, slated to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.